TBLA - Taking A Pause On Taboola.com While Still Waiting On Yahoo

2023-10-02 09:22:17 ET

Summary

- Taboola's stock has steadily increased, but it is approaching its 2023 highs, signaling a time to secure profits.

- The company's deal with Yahoo is still in development, with no hard numbers yet to support its promise.

- Taboola's focus on Yahoo integration, performance advertising, eCommerce, and bidding are its top strategic priorities.

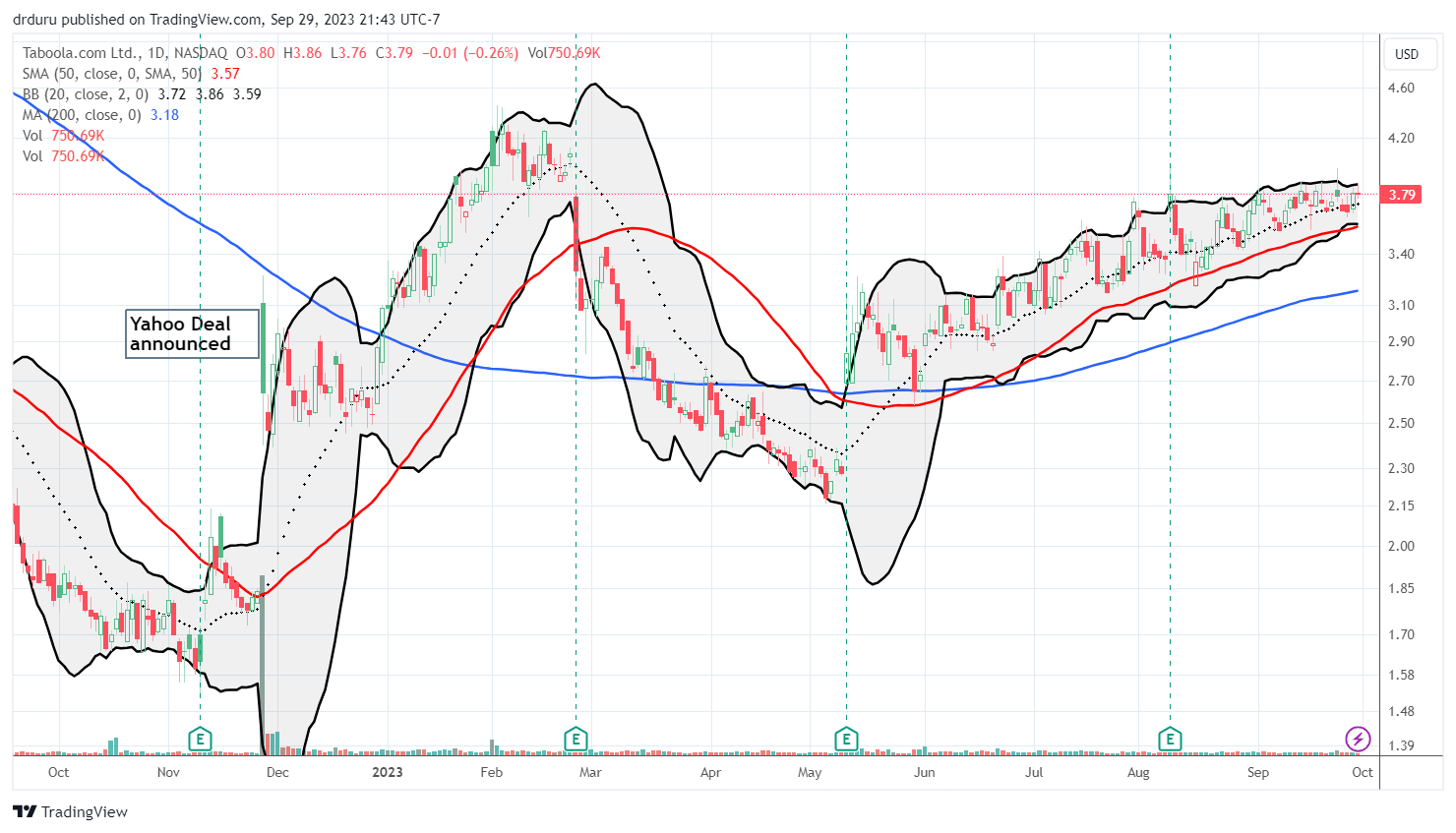

The timing of my last post on Taboola.com Ltd. ( TBLA ) turned out to be very fortuitous. Not only did TBLA carve out a higher low, but the stock has also steadily churned its way higher, mostly ignoring the swoons and pullbacks in the general market (a gain of over 50%).

However, with the stock approaching its 2023 highs, this is a time for securing some profits. The story for TBLA remains the same. It is still a buy-the-dip story, but it is also still a "show me" story. The company's big deal with Yahoo is still in the development stage. While Taboola maintains its guidance on the deal, there are no hard numbers yet to support the promise. The company reported early success with testing in international markets but did not provide any numbers to quantify that success.

After Taboola reported Q2 earnings, the stock dropped 7.1% and slid back to the bottom of its uptrend channel. That was the last good time to buy the dip on TBLA. At the time, selling was the path of least resistance because earnings did not offer any new, positive catalysts. Demonstrable performance numbers for Yahoo are still about two quarters away. Guidance for 2023 offered a minimal increase on the floor for the anticipated performance ranges. Moreover, guidance for 2024 did not change. If Q3 earnings offer more of the same, I suspect TBLA will dip again.

Until then, let's take a look at the latest developments on Taboola's top strategic priorities starting with Yahoo (mainly using the Seeking Alpha transcript of the Q2 earnings conference call ).

Waiting on Yahoo

The Yahoo integration is one of four priorities for Taboola, including Performance Advertising, eCommerce, and Bidding. CEO Adam Singolda said the company is "well underway" on its execution plan. This work focuses on building out the infrastructure to allow Taboola and Yahoo advertisers to use the integrated platform.

This platform has gone live internationally as part of early testing. In response to an analyst question about performance metrics, Singolda only offered "what's really encouraging me and us is that now that we're able to bring some Taboola advertisers onto Yahoo international markets, we've kind of validated this very important assumption that Yahoo is awesome." Earlier on the call, he also indicated that Yahoo international is included in guidance, perhaps implying that the "awesomeness" helped boost the lower part of the range.

"Our full year guidance factors in a small amount of revenue from Yahoo in those markets. It also factors in the cost of investing in the partnership so we can capture the full revenue from the partnership. We still expect the revenue to start ramping in the second half of 2023 and to reach full run rate by the middle of 2024."

Taboola effectively raised the midpoint of its 2023 guidance. Yet, with 2024 guidance unchanged, the company left a more telling message that it has not learned anything materially new about the potential for Yahoo's performance. From the Q1 2023 earnings presentation and the Q2 2023 earnings presentation :

- Revenues: from $1,427M-$1,469M to $1,438M-$1,469M

- Gross Profit: from $418M-$436M to $420M-$436M

- ex-TAC gross profit (gross profit excluding total acquisition cost for ads): $529M-$546M to $531M-$546M

- Adjusted EBITDA: $65M-$80M to $73M-$80M

- Maintained 2024 guidance of $200M in adjusted EBITDA and $100M in free cash flow

With such minimal changes in guidance, the subsequent drop in the stock made sense (for the short term). The tiny shift in the floor of 2023 guidance matters little when 2024 guidance remains the same. Moreover, without revenue guidance for 2024, it is still not possible to confirm the top-line performance expectations on the Yahoo deal (or for any of the company's other top priorities). Both EBITDA and free cash flow can be maneuvered partially independent of organic revenue growth (for example, cost efficiencies, acquisitions, etc.).

CFO Stephen Walker provided more details on the company's hiring plans connected with the Yahoo integration. He stated that Taboola will not only need to keep Yahoo sales and account managers but also the company will need to grow the team. Unfortunately, the company does not seem to anticipate material scaling efficiencies with the anticipated hiring growth (another downer for analysts).

"…we typically see that our sales and account management headcount tends to grow roughly in line with revenue. We gained some efficiencies over time, but it grows roughly in line with revenue. So those will be permanent."

In my previous post on Taboola, I expressed surprise at the company's plans to bring on a large number of temporary developers to handle the technical part of the Yahoo integration. This time around, the company also revealed that there is nothing special about the technical work. Anecdotally, every major technical transition I have seen has been "special" by throwing plans and expectations for a loop. So, I was once again surprised by the description of the staffing plans for the integration: "There's really nothing that is dramatically special about the Yahoo setup that will require permanent people on that." With such an assumption, I am betting these developers will feel double pressure to get the work done on schedule!

Taboola is still expecting to move this technical staff to other projects once they finish with Yahoo (analysts probably want to hear that Taboola will be able to relieve itself of these costs).

Performance Advertising

Taboola has a large focus on performance advertising given the use of content-based targeting. Taboola's success is measured by conversions through clicking on ads, not just viewing them like brand advertising. Accordingly, nearly half of Taboola's R&D (research and development) is spent on the success of their 18,000 advertisers through performance advertising.

SmartBid is Taboola's core machine learning algorithm that optimizes campaign bids using historical data. SmartBid adjusts bids based on impression value using a second price auction model. This model helps advertisers pay the minimum required while also offering them the ability to modify bids for specific sites. Taboola recently launched Target CPA (cost per acquisition) and Maximize Conversion to general availability after doing testing in the second quarter. Advertisers can set a cap on CPA for a given campaign and maximize conversions will deliver the highest number of conversions within that pricing constraint. The SmartBid algorithm manages these advertising processes.

Taboola expects 50% of 2024 revenue will come from Maximize Conversions using Target CPA. Next year, Taboola will allow advertisers to optimize against ROI (return on investment) targets.

Taboola is using generative AI to help advertisers generate content and copy for ad creatives. This approach reportedly reduces content costs while also improving performance. Taboola reported that advertisers using their generative AI solution doubled click-through rates versus evergreen campaigns. Welcome to a world of robotic chatter constantly urging us to click and read content.

eCommerce

Taboola entered eCommerce advertising after acquiring Connexity three years ago. Taboola reported that eCommerce is "outperforming". ECommerce "now represents nearly 20% of ex-TAC, up from 15% last quarter." The business is growing so well that Taboola plans to do additional hiring to support this part of the business.

The company is targeting its eCommerce solution at publishers and retailers. The Taboola Turnkey Commerce solution writes content for publishers and drives traffic to those articles. Monetization comes from product and service providers. In other words, Taboola writes, traffics, and monetizes content on behalf of its eCommerce advertisers. The company thinks this business could eventually grow bigger than its current core business: "if you're not offering eCommerce to publishers, you may have nothing to offer over time, because that's going to be a big portion of what they see as a growth engine."

Bidding

Taboola anticipates an auction win rate of 5% to 10% with its header bidder solution that Microsoft ( MSFT ) helped to design. The company uses a combination of AI (of course), first-party data, and technology to run this marketplace where advertisers place their bids on inventory all at once. The use of first party-data will give Taboola an advantage in a cookieless world (the cookiepocalypse). Taboola expects to enable its bidding strategy with Yahoo. Taboola's header bidding is running globally on more than 100 websites. In its partnership with Microsoft, Taboola experienced year-over-year growth in Q2 and expects even more growth in Q3. The company did not provide specific numbers.

The Macro Wildcard

Given its sensitivity to the economic cycle, advertising companies must keep close tabs on the macroeconomic environment. Taboola described the macro environment for advertising as stable since Q3 of 2022. The company even dared to utter the "B" word (emphasis mine): "And I think "…most advertisers that we talked to, what they're basically saying is, they're still watching the macro a bit. They're probably getting a bit more bullish, like a lot of people are about the potential for a soft landing and not a recession. But I think they're still cautious, but stable, their spend is stable, they're still spending kind of as they were."

Of course, it is very possible the main advertisers interested in Taboola are the ones whose businesses have been relatively stable for nearly a year.

Regardless, Taboola's report implies that the company's guidance assumes a soft landing scenario. Such an assumption is perhaps the second largest risk to the Taboola narrative, right behind the execution risk on the Yahoo deal.

Conclusion: The Trade

As I mentioned earlier, TBLA has rallied counter to the general stock market's weakness over the past two months (the divergence has brought TBLA's year-to-date performance close to the NASDAQ's, 23% vs 26% respectively). This slow and grinding rally has taken the stock close to its high of the year set in February. Given the lack of fresh positive catalysts, I think it makes sense to take profits here. The most likely new positive catalyst will come from Yahoo, and such news is not likely until Q1 or even Q2 of next year at best. Accordingly, TBLA will have a hard time punching through that high created from the excitement over the Yahoo deal.

I now rate TBLA a hold, but going forward the stock is still a buy on the dips given the bottom the Yahoo deal created for the stock .

Taboola Ltd has quietly churned higher against the general stock market's headwinds (TradingView.com)

{kind=link}

Be careful out there!

For further details see:

Taking A Pause On Taboola.com While Still Waiting On Yahoo