NVO - Taking Novo Nordisk To The Next Level

2024-01-15 09:00:00 ET

Summary

- Novo Nordisk stock remains a great buy at every dips, thanks to its expanding 2030 TAM to $150B, highly profitable growth trend, and improving balance sheet.

- Readers must also note that its growing oral/injectable diabetes/obesity pipelines, with its late stage candidates being highly promising.

- Combined with the excellent patient adherence rate and raised guidance/estimates, we believe that consumers' vote of confidence may bring about NVO's sustained top/bottom line growth and shareholder returns.

We previous covered Novo Nordisk ( NVO ) stock in October 2023, discussing how its obesity/diabetes drug, Wegovy/Ozempic, are projected to outperform the best-selling drug of all time, Humira, with an estimated $38.5B in annual sales by 2030.

Despite its inflated P/E valuations over the pharmaceutical median, we had rated the stock as a Buy then, attributed to its highly profitable growth trend and potential applications for new indications.

In this article, we shall discuss why NVO's investment thesis remains robust, thanks to its healthier balance sheet, growing pipelines, and the consistently raised forward guidance thus far.

Combined with the excellent patient adherence rate and expanded 2030 TAM, we believe that consumers' vote of confidence may bring about its sustained top/ bottom line growth and shareholder returns.

The NVO Investment Thesis Remains As Robust As Its Growing Pipeline

For now, NVO reported excellent FQ3'23 results, with revenues of DKK 58.73B ( +8.1% QoQ / +28.9% YoY ) and GAAP EPS of DKK 5.00 (+15.7% QoQ/ +57.7% YoY).

Its Free Cash Flow profitability has also ballooned to DKK 35.13B (+54.8% QoQ/ +67.3% YoY) with impressive margins of 59.8% (+18 points QoQ/ +13.7 YoY) in the latest quarter, or 39.7% over the last twelve months (+4.1 points sequentially).

NVO's recent FCF margins are noteworthy indeed, especially when compared to its FY2019 margins of 31% (-0.3 points YoY) and its direct peers, such as Eli Lilly ( LLY ) at 8.8% (-13.2 points sequentially), Pfizer ( PFE ) at 11.9% (-11.5 points sequentially), and Amgen ( AMGN ) at 35% over the LTM (+0.8 points sequentially).

As a result, it is unsurprising that NVO's balance sheet has improved drastically to a net cash position of DKK 27.67B (+62.8% QoQ/ +107.4% YoY) by the latest quarter.

Its shareholders have been decent as well, with the management's sustained share repurchases resulting in 48M shares retired over the LTM or 268.4M since FY2019. This is on top of its 3Y Dividend Growth Rate of +16.52%, compared to the sector median of +5.81%.

As a result of the profitable growth trend, it is unsurprising that the NVO management has raised its FY2023 guidance to revenues growth of +35% YoY and operating profit growth of +43% YoY at the midpoint.

This is compared to the original YoY growth guidance of +16% and +16% offered in the FQ4'22 earnings call , respectively.

NVO's Diabetes/ Obesity Portfolio

Seeking Alpha

Most of the tailwind is attributed to NVO's robust portfolio, notably its diabetes/ obesity therapies: injectable Ozempic/ Wegovy and oral Rybelsus (14 milligrams).

These three therapies comprise DKK 100.21B of its sales over the past nine months (+86.4% YoY), or the equivalent 60.2% of its sales (+18.5 points YoY), easily being the pharmaceutical company's top and bottom line drivers.

Readers must also note that NVO is already in the process of submitting the relevant documents for the US FDA approval of its next-gen oral semaglutide (50 milligrams), with a reduction in body weight by -15.1% by week 68.

Part of the hurdle to its mass commercialization is the " relative low bioavailability ," also known as limited Active Pharmaceutical Ingredients [API]. This is also why the company has taken steps to scale up its manufacturing capacity moving forward, through recent investments in Denmark , France , and Ireland .

At the same time, NVO's upcoming pipeline is very exciting as well, with its next-gen obesity candidate, CagriSema , offering an excellent reduction in bodyweight by up to 15.6% from baseline by week 32 of treatment in the phase 2 clinical trials.

This candidate is already in phase 3 clinical trials , directly pitted against LLY's recently approved Zepbound , as the latter delivers a reduction in body weight of 15% by week 72 and up to 20.9% at the highest dosing.

These results show that NVO's obesity candidate may very well outperform LLY's Zepbound at a much earlier timeline, especially since CagriSema contains Cagrilintide , a long-acting amylin analogue which may promote a longer lasting weight loss.

Assuming so, we may see more physicians and patients turn to CagriSema upon successful US FDA approval and mass commercialization, since patients whom stopped taking NVO's Wegovy/ Ozempic and LLY's Mounjaro have reported rebound in weight gain after stopping.

While CagriSema is unlikely to be approved until late 2025 or early 2026, with the phase 3 clinical trial only to be concluded by October 2025, it appears that NVO's long-term tailwinds remain robust for the next half of the decade.

This is on top of twelve other diabetes/ obesity candidates in phase 1 and phase 3 clinical trials, involving oral and subcutaneous injection intakes, further underscoring the management's determination to stay on top of the game while demonstrating its market leadership with 25 years of experience.

In the meantime, NVO is likely to remain the de facto market leader in the diabetes/ obesity treatment market, with the Wegovy recording the highest adherence rate of 40% in 2022, which is "more than three times the adherence rate for older weight-loss medications."

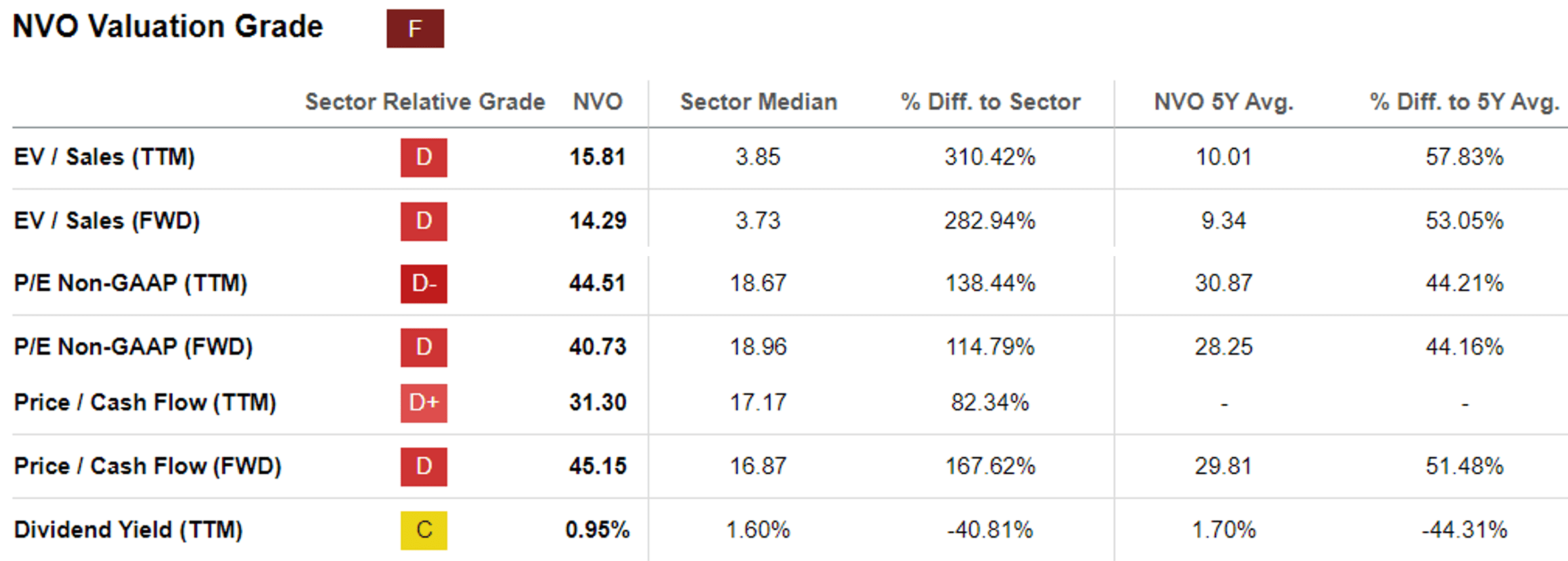

NVO Valuations

{kind=link}

As a result of its massive tailwinds, we are not surprised that Mr. Market continues to reward the NVO stock with the premium valuations, with FWD P/E of 40.73x and FWD Price/ Cash Flow of 45.15x.

This is compared to its 1Y mean of 32.35x/ 28.70x, 3Y pre-pandemic mean of 18.81x/ 18.70x, and the sector median of 18.96x/ 16.87x, respectively.

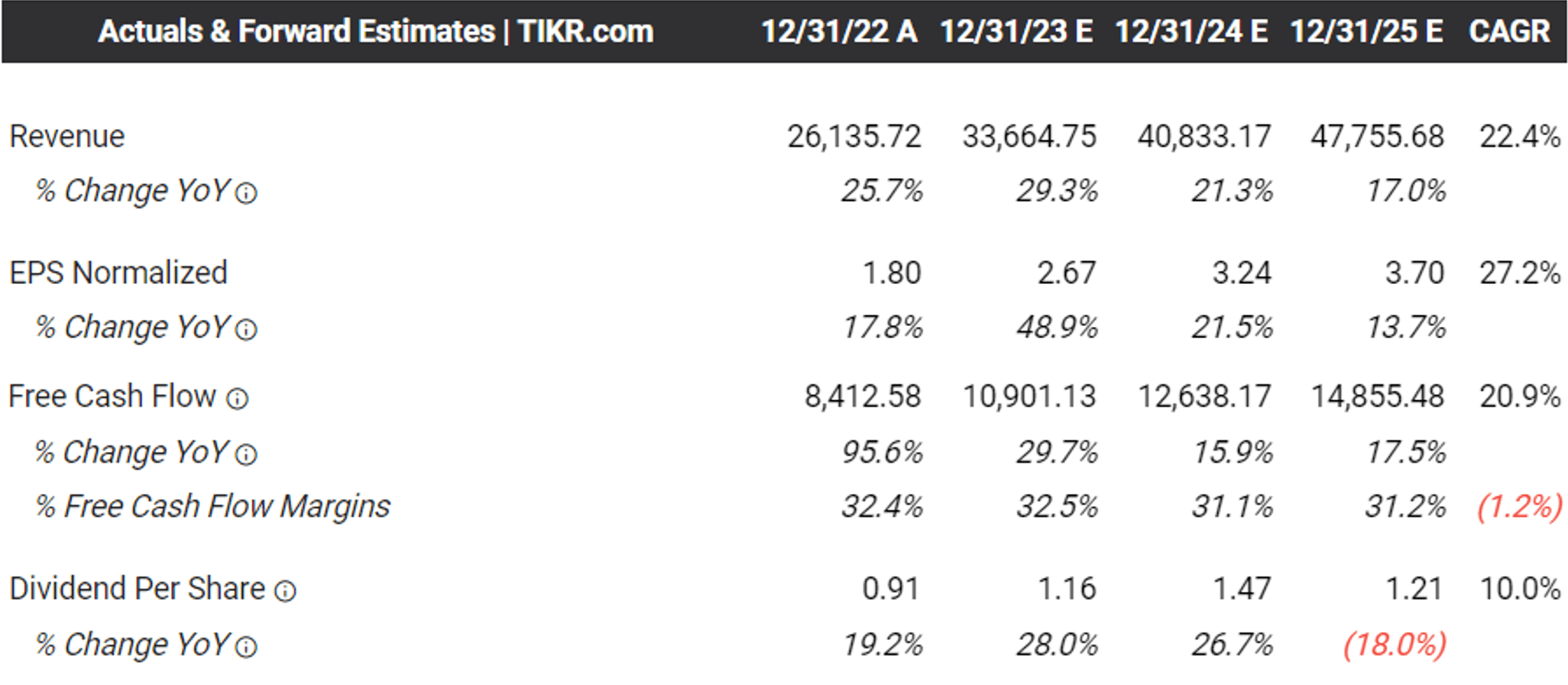

The Consensus Forward Estimates

{kind=link}

On the one hand, the consensus forward estimates remain highly optimistic for NVO, with it expected to generate an improved top/ bottom line expansion at a CAGR of +22.4% and +27.2% through FY2025.

This is compared to the previous estimates of +11.1%/ +11.5% and its historical growth of +8%/ +8.5% between FY2016 and FY2022, respectively.

Combined with the promising early results from the US FDA, with GLP-1 therapies not linked to suicidal thoughts or actions , we believe that there may be minimal legal headwinds ahead, with sales only gated by supply and production capacity.

Combined with the PFE CEO's projection in the obesity TAM of $150B by the end of the decade, expanding at a CAGR of +58.1%, we believe that NVO's premium FWD P/E valuation is somewhat warranted indeed.

Interested readers may also want to note that NVO is expected to report its FQ4'23 earnings on January 31, 2024, with the consensus estimating revenues of DKK 60B (+2.1% QoQ/ +24.9% YoY) and GAAP EPS of DKK 4.45 (-11% QoQ/ +47.8% YoY), further sustaining its growth premium.

On the other hand, it may be foolish to assume that NVO is able to maintain its exclusive two horse race with LLY throughout the decade, since multiple pharmaceutical/ biotech companies are already expediting their weight loss candidates.

For example, AMGN has an obesity candidate, Maridebart Cafraglutide, which is in clinical phase 2 trials with results expected in the year.

While it may take some time for the eventual clinical phase 3 trials and the US FDA approval, the management already expects a "more effective and more rapid weight loss" through monthly dosing, compared to NVO's weekly Wegovy and LLY's weekly Mounjaro dosing.

As a result, while NVO's intermediate term prospects are very bright indeed, investors must also temper their expectations, since its higher premium naturally imply more volatility should there be any market share losses or misses in earnings estimates.

So, Is NVO Stock A Buy , Sell, or Hold?

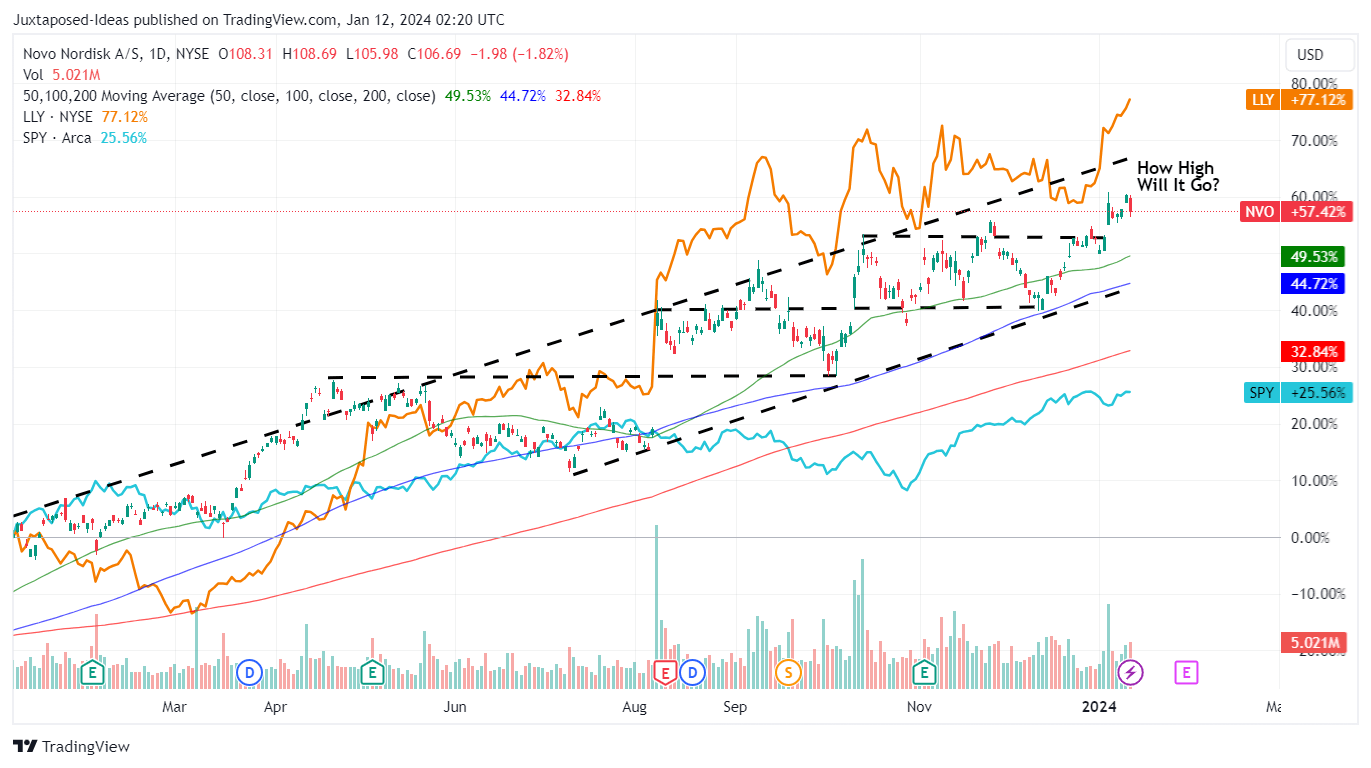

NVO 1Y Stock Price

{kind=link}

For now, NVO has climbed to new heights after rallying by +11.2% since our previous coverage in October 2023, partly aided by the cooling inflation and Fed's potential pivot from Q1'24 onwards, with the SPY similarly rising by +12.9% over the same time period.

As a result of its highly profitable growth trend and improving balance sheet, we believe that the stock's recent rally may be sustainable indeed, especially aided by its robust pipeline and expanding market TAM.

Combined with the excellent upside potential of +40.6% to our long-term price target of $150.70, based on the consensus FY2025 adj EPS estimates of $3.70 and its FWD P/E valuation of 40.73x, we are maintaining our Buy rating on the NVO stock.

Then again, there is no specific recommendation in entry point for this buy rating, with the stock currently charting new heights. Interested investors may want to observe its movement for a little longer, before adding at its previous trading range of between $95 and $100 for an improved margin of safety.

For further details see:

Taking Novo Nordisk To The Next Level