IMCV - Taking Stock: Q3 2023 Equity Market Outlook

2023-06-22 02:30:00 ET

Summary

- Stocks arguably defied expectations in the first half of the year, with the S&P 500 notching double-digit returns.

- Companies remain focused on recession and interest rates.

- In the regime now forming - the post-COVID era - stock valuations, inflation, and interest rates are all higher.

By Tony DeSpirito

An ounce of optimism, a pound of prudence. It's still a good time to be measured about taking risks in equities, but we believe the longer-term horizon holds particular promise for active stock pickers. As Q3 begins, we see:

- Investor caution keeping cash on the sidelines

- Greater dispersion in earnings, valuations, and returns

- Opportunity to build and deploy shopping lists

Stocks arguably defied expectations in the first half of the year, with the S&P 500 notching double-digit returns even as inflation remained elevated and the Fed continued its fastest rate-hiking campaign since the 1980s. The big picture masks some nuances: Technology shares , after cratering in 2022, have carried index returns. And comparing the index's market-weighted (15%) and equal-weighted (5%) returns illustrates just how much the mega-cap stocks ? primarily tech-related stocks across IT, telecom services, and consumer discretionary ? have driven year-to-date performance. See the chart below. We remain selective in taking risks as we prepare our shopping lists for the cycle's next leg, and we believe stock selection will be rewarded as investors prioritize company fundamentals and market breadth widens beyond the current leaders.

A Tale of two markets

S&P 500 performance by sector, year-to-date 2023

BlackRock Investment Institute, with data from Refinitiv, June 14, 2023

The chart shows the year-to-date return of the S&P 500 index both market-weighted and equal-weighted, in which each stock is proportioned at equal measure, and each sector in the index. Past performance is not indicative of current or future results. Indexes are unmanaged. It is not possible to invest directly in an index.

Caution is the consensus

Reasons for caution are many and fund flows suggest investors are aligned in their thinking. Data from Morningstar shows $37 billion has exited U.S. equity funds this year while bonds have gathered $108 billion in assets, even as volatility in the latter asset class has remained higher. An astounding $404 billion flowed into money market funds.*

The spring banking crisis that saw the failure of Silicon Valley Bank (SIVBQ) and Signature Bank (SBNY) and the takeover of First Republic (FRCB) in the U.S. and Credit Suisse (CS) in Europe rattled already fragile investor nerves. The tightening in lending that came as an outgrowth threatens to pressure the corporate real estate market.

All of this comes as the still-inverted yield curve continues to signal recession. Our analysis of the 12 yield curve inversions since 1978 shows the average time from inversion to recession is 18 months. This cycle, the curve between two- and 10-year yields inverted 11 months ago, in July 2022.

Companies remain focused on recession and interest rates, as indicated by mentions in earnings reports. See the chart below. Macroeconomic uncertainty in general remains high on their worry list, if mentions are any indication. And certainly, macro drivers are applying the greatest influence on markets while stock fundamentals take a back seat ? for now.

Macro is still top of mind

Company mentions of key terms, 2021-2023

BlackRock Fundamental Equities, May 2023

The chart shows S&P 500 company mentions related to the noted terms during quarterly earnings reporting seasons.

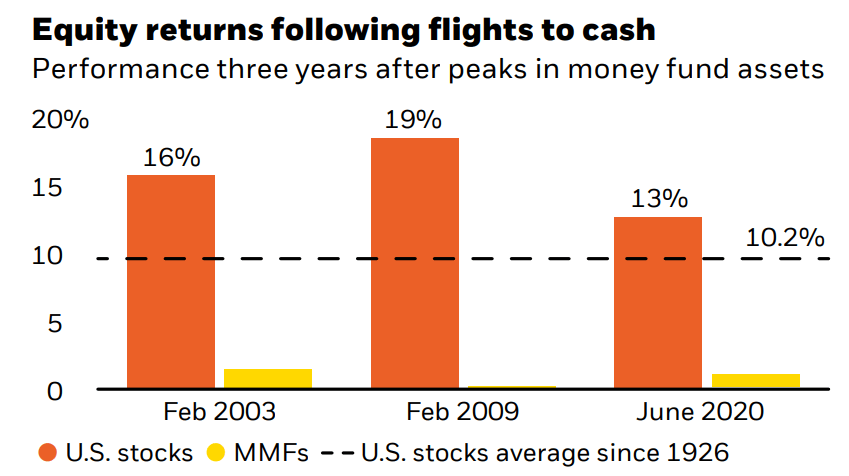

Of course, caution also means ample money waiting to be deployed. While investors have hunkered down in cash, as shown by the extraordinary flows into money market funds, this also suggests record levels of sidelined cash that could eventually make its way into the economy and markets. Past episodes of peak money fund flows have historically been followed by strong returns from equities.

{kind=link}

The chart shows the three-year average annual performance after a peak in money market fund (MMF) assets. The dates noted represent the MMF peaks. U.S. stocks are represented by the S&P 500 Index. Past performance is not indicative of current or future results. Indexes are unmanaged. It is not possible to invest directly in an index.

Alpha is the opportunity

While caution is prudent in the near term, paralysis can be detrimental to long-term financial goals. Every cycle is different, which makes investing amid uncertainty a challenge but also highlights the importance of an active and selective approach.

As recession risk looms larger, we lean into opportunities in defensive areas of the market, with healthcare still a favored sector. We looked at Russell 1000 sector performance 24 months following prior yield curve inversions and saw typically good performance from healthcare. It is lagging so far in this cycle, which only makes for a more attractive entry point into a well-priced and recession-resilient sector, in our view.

Cyclicals could slump in a recession, but this is where it's important to have shopping lists ready to capture opportunities amid the rubble. Industrials have so far been surprised by the upside versus prior post-inversion episodes, but we expect a wide range of outcomes as advancements in industrial technology and progress or plans for reshoring are already sowing the seeds of opportunity.

A good shopping list should be diversified across sectors and include companies with attractive prospects that could reprice lower should a recession temporarily punish their valuations. In cyclicals, we continue to emphasize the business quality and strength of the balance sheet since companies with these characteristics should offer greater resiliency.

The Return of Alpha: Active Equities for a new era

While our medium-term view is for the market to begin shifting its focus from macro factors to micro, or stock specifics, our longer-term outlook takes that a step further.

We foresee a return to a more normal investing landscape where alpha is at the center. This is based on changes in the underlying dynamics that coalesce to create opportunity in the stock market.

The end of easy money

In the 12 years following the 2008 Global Financial Crisis ((GFC)), there was excess supply as China continued to industrialize, inflation was muted, interest rates were at historic lows and excess money in the system was plentiful. The Fed consistently applied easy monetary policy to help consumers and businesses heal from the crisis, propping up markets in the process.

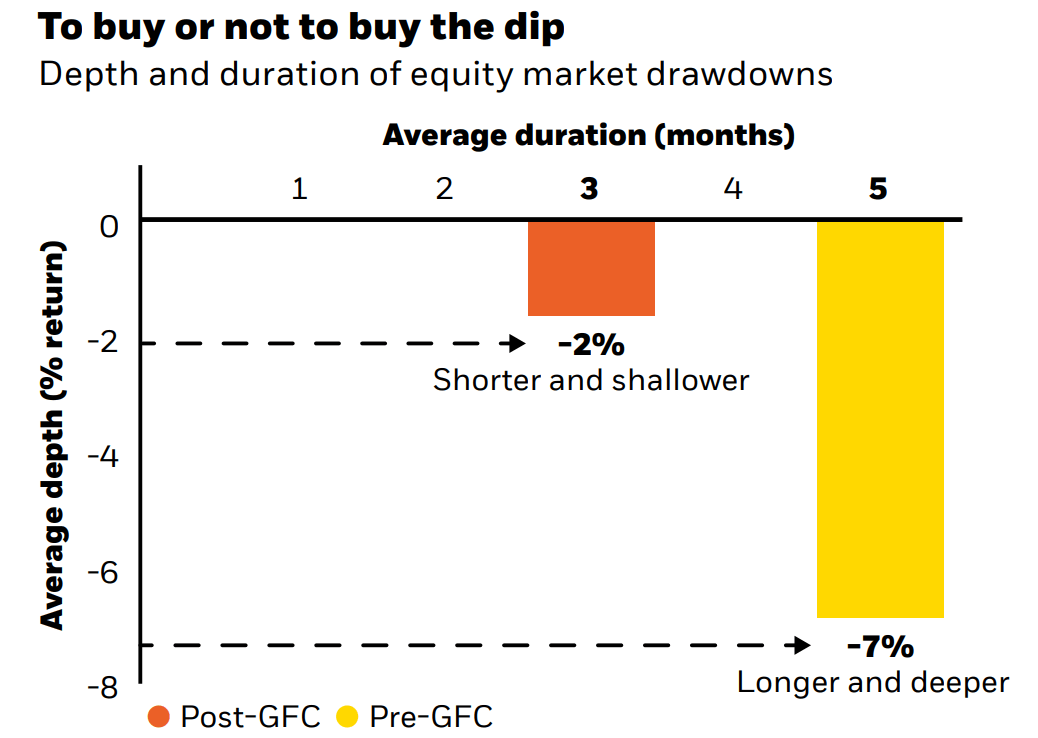

From an equity market perspective, beta (market return) was abnormally high as valuations went from very low to normal and the differentiation in returns between individual stocks was slim. Investors bought the dips and, as a result, the drawdowns were quite short and shallow. The Fed also was willing to come to the rescue in the case of any wobbles. Beta was king, as well-supported markets provided extreme performance, resulting in an average annual S&P 500 return of 15% over calendar years 2010 to 2021.

In contrast, the era before the GFC featured longer and deeper equity market drawdowns, meaning more volatility as well as greater opportunity for skilled stock picking to deliver above-market returns (or alpha). We see this dynamic returning in the new era.

{kind=link}

The chart shows the average depth (% return) and duration (in months) of Russell 1000 Index drawdowns during the pre-GFC (January 1979-February 2009) and post-GFC (March 2009-December 2021) periods. Past performance is not indicative of current or future results. Indexes are unmanaged. It is not possible to invest directly in an index.

Back to a period of greater differentiation

In the regime now forming ? the post-COVID era ? stock valuations, inflation, and interest rates are all higher. Supply is being constrained by demographic trends (aging populations and fewer workers), decarbonization, and deglobalization, all of which are inflationary. Going forward, the Fed is more likely to be in a position of having to fight inflation rather than bolster the economy, a less friendly scenario for financial markets.

Equities historically have been the highest-returning asset class over the long term, and we see nothing to alter that precedent. However, higher stock valuations than at the start of the prior regime plus higher interest rates mean less return from markets broadly (beta). We see more dispersion in earnings estimates , valuations, and stock returns ? and this suggests a greater opportunity for skilled managers to generate more alpha. The result, in our view, is that the years ahead will see active return being a bigger part of investors' overall return profiles.

*Flows data is year-to-date through April and covers U.S. mutual funds and exchange-traded funds.

This material is provided for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of June 2023 and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive, and are not guaranteed as to accuracy. Past performance is no guarantee of future results. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader. The material was prepared without regard to specific objectives, financial situation, or needs of any investor.

This material may contain "forward-looking" information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of yields or returns, and proposed or expected portfolio composition. Moreover, where certain historical performance information of other investment vehicles or composite accounts managed by BlackRock, Inc. and/or its subsidiaries (together, "BlackRock") has been included in this material, such performance information is presented by way of example only. No representation is made that the performance presented will be achieved, or that every assumption made in achieving, calculating, or presenting either the forward-looking information or the historical performance information herein has been considered or stated in preparing this material. Any changes to assumptions that may have been made in preparing this material could have a material impact on the investment returns that are presented herein by way of example.

Investing involves risk. Equities may decline in value due to both real and perceived general market, economic, and industry conditions. Diversification does not ensure profits or protect against loss.

You should consider the investment objectives, risks, charges, and expenses of any BlackRock mutual fund carefully before investing. The prospectus and, if available, the summary prospectus contain this and other information about the fund and are available, along with information on other BlackRock funds, by calling 800-882-0052 or from your financial professional. The prospectus should be read carefully before investing.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

Not FDIC Insured | May Lose Value | No Bank Guarantee

© 2023 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

This post originally appeared on the iShares Market Insights.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Taking Stock: Q3 2023 Equity Market Outlook