TALK - Talkspace: Opportunities In Online Mental Health And AI But Faces Competition

2024-01-19 16:17:53 ET

Summary

- Talkspace's stock is trading at a discount relative to the healthcare sector, making it an attractive investment opportunity.

- The company's virtual mental health solutions have gained traction, particularly in the B2B segment, leading to significant revenue growth.

- While this is still a loss-making company, Talkspace is making progress and has the potential to break even through the optimization of its platform.

- However, competition remains strong and it is important to obtain a management update before investing.

- This is more of a Hold currently.

For those who did not buy the dip in Talkspace Inc's (TALK) stock in the first week of November and are wondering what to do, its forward price-to-sales multiple is still trading at a 30% discount relative to the healthcare sector. However, investing merely based on favorable valuations is unadvisable as other metrics like revenue growth and profitability also need to be considered and balanced against competitive risks.

Now, since this is a company that offers mental health services using an online platform-based approach, the objective of this thesis is to show that it is in a good position to benefit from additional market opportunities as its products find wider adoption among the population and artificial intelligence disrupts this industry.

First, for investors, I highlight why the company’s products are gaining traction.

The Appeal of Online Mental Therapy

For most of us, due to our own experience with a family member or through watching movies, dispensing mental care is normally associated with physically visiting either a psychologist or psychiatrist. However, online therapy which involves connecting to a qualified therapist through the Internet using a laptop or mobile phone can be as effective as in-person treatment for various mental health conditions. Moreover, having convenience and affordability in mind, it is a good option for those residing in remote areas.

{kind=link}

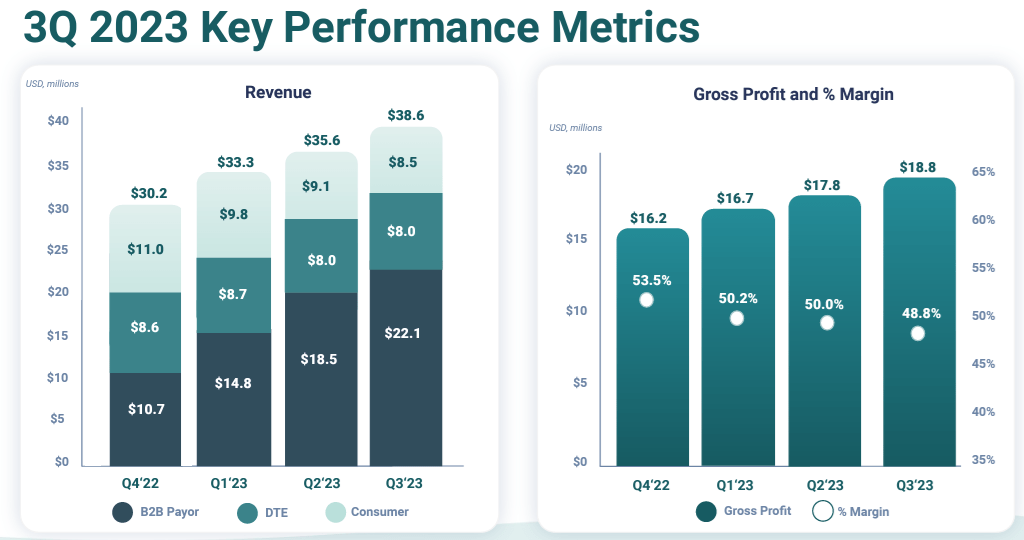

As for Talkspace, it has already disrupted the field with virtual mental health solutions which can be provided directly to people over the internet with the associated revenues recorded under the Consumer category as illustrated below. There is also B2B whereby services are provided directly to the corporations (Direct to Enterprise) and to medical providers that can include the company's services in their menus.

Company presentation (investors.talkspace.com)

{kind=link}

Now, it is precisely as a result of sustained momentum in the B2B category which grew by 79% YoY that consolidated revenues rose to $38.6 million in the third quarter of 2023 (3Q-2023), representing a YoY increase of 32%. Now B2B is further divided into B2B Payor (in deep blue in the chart above) and DTE, with the former growing by an astounding 132% YoY. This has to do with payer sessions when treatment costs for an employee is incurred by the employer.

Thinking aloud, the fact that B2B Payor's revenues have increased while the Consumer category (pale blue chart above) has been decreasing during the last four quarters suggests that more people are availing of the service through their employers instead of directly accessing Talkspace's Website, possibly as a result of corporate awareness campaigns about mental health issues.

Now, success at penetrating the corporate space which tends to be more profitable than selling products to individuals, should normally rhyme with better profits, for this loss-making company whose EPS is negative.

On a Profitability Path and Valuations

As shown in the above chart, gross profit margins declined from 53.5% in FQ4-2022 to 48.8% during the last reported quarter, which translates to 46.8% gross margins on a TTM (trailing twelve months) basis, or 17% lower than the sector median for the healthcare sector. Therefore progress still has to be made on the profitability front which I believe is helped by the platform approach.

For this matter, to satisfy the need for stringent hiring standards while delivering the " highest-quality digital mental health care at scale", relatively high costs are incurred to recruit high-caliber therapists whose numbers have increased by almost 60% to reach around 1,800. However, the associated higher expenses were partially offset by $10.4 million in cost savings achieved through optimizing the platform. Therefore, the company has room to further optimize workflows like those between counselors and patients to remove inefficiencies.

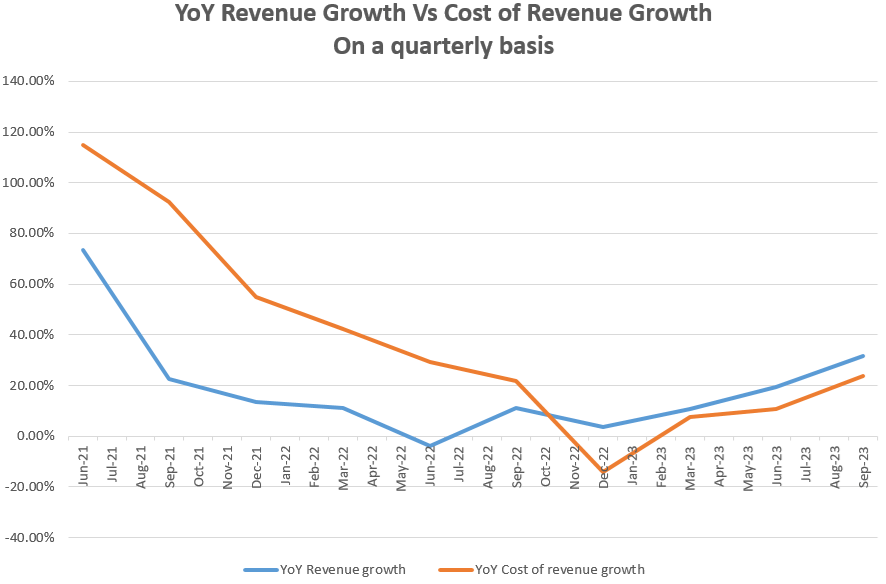

Furthermore, looking at the YoY progression of quarterly revenue and cost of revenues as per the chart below, it is found that after having mostly trailed expenses, sales (in orange) are now growing more rapidly, more specifically from the September 2022 quarter.

Charts built using data from Income Statement in (seekingalpha.com)

{kind=link}

Along the same lines, the adjusted EBITDA loss was narrowed down by 82% year-over-year to reach $2.8 million in FQ3-2023 which again shows that the trend is toward profitability, a metric that should also receive support from a rapidly growing revenue base to spread fixed costs.

Looking at growth opportunities, in addition to driving a further increase in B2B Payors, the company is now tapping into the teen mental health market of over $500 million. The objective is to deliver the Talkspace solution to adolescents in need of therapy for anxiety, depression, and other conditions. Now, with a technology that is HIPAA (Health Insurance Portability and Accountability Act) compliant and as one of the largest in-network providers of remote mental health services, the company could get a big chunk of this half-billion dollar market especially given that several announcements were planned for marketing purposes at the end of 2023.

Now, no specific guidance was provided but assuming that the company manages to capture just 5% of this market, additional revenues of $25 million (500 x 0.05) can be expected for FY-2024 (ending in December this year). Adding this figure to the $182.5 million already forecasted by analysts as per the table below, a total of $207.5 million is obtained which would in turn increase the growth to 41.7% from the 24.7% expected. This in turn reduces the forward P/S to 1.94x (2.21x(182.5/207.5)) from 2.21x. Moreover, because of the inverse relationship between price and sales in the P/S ratio, I obtained a target of around $2.7 (2.41x (207.5/182.5)) based on a share price of $2.41.

Revenue Estimates (www.seekingalpha.com)

{kind=link}

This represents only a 13.7% upside, which is much less than the 30% discount the stock is trading relative to the healthcare sector as mentioned in the introduction Still, as I elaborate further, this represents a fair price considering competitive risks.

Competitive Risks

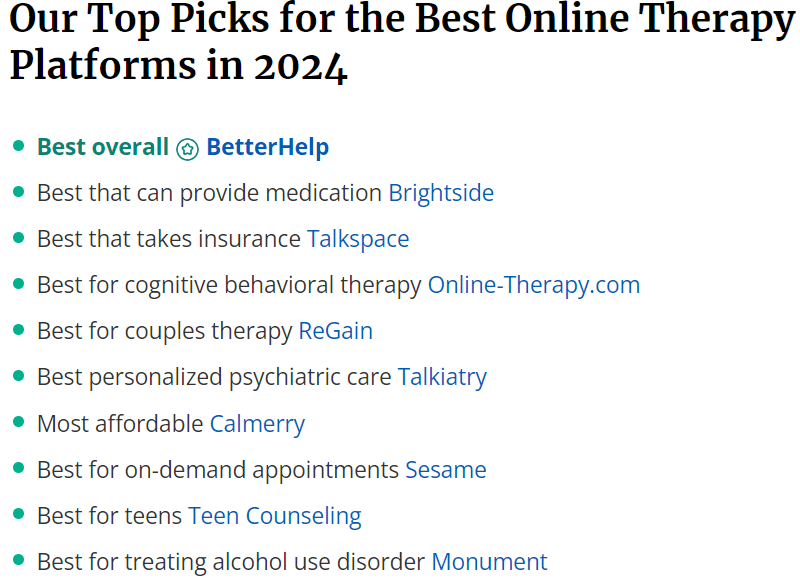

To be realistic, additional sales opportunities are based on the company continuing to gain market share but this remains a competitive environment including both traditional healthcare providers and online ones. Here, a comparison done by Everyday Health for 2024 shows that Talkspace faces competition from the likes of Better Help and Brightside as shown below. There are also companies already specializing in teen counseling services.

Comparison (www.everydayhealth.com)

{kind=link}

Still, Talkspace should continue to take share as, going beyond simply the middleman positioning that merely puts providers and potential patients in contact with each other using its platform, the company also makes sure that it is keeping abreast with the latest research, and, to this end, employs a Chief Medical Officer to oversee clinical quality. In this respect, Verywell Mind which is a mental health information website has awarded the company the most comprehensive online therapy and Wellness award for 2023. Still, Verywell Mind also mentions that E-Therapy Cafe is more affordable while Teladoc Health ( TDOC ) is better at medical insurance.

This all means that, while the company is on a path to profitability, it may take more time to become profitable as marketing expenses to drive its products are likely to be sustained. Still, with cash and equivalents amounting to $125.3 million and no debt, this is a company with a healthy balance sheet. Moreover, progress has been made in reducing the cash consumed in operations from $13.7 million in FQ3-2022 to $1.1 million during the latest reporting quarter.

In these circumstances, I have a hold position as I believe that it is better to wait and see if Talkspace can achieve the 41.7% growth target, which as per this thesis will depend on gaining market share in the teen mental health market. To obtain a hint of whether progress is being made on this front, one can look forward to the fourth quarter (FQ4-2023) earnings call around February 21. Another growth driver to check is whether the 15 million additional commercial-covered lives (for insurance purposes) launched in the fourth quarter have started to make a meaningful contribution to the top line. Then, of course, there is artificial intelligence.

More of a Hold with A Potential AI driver

In this respect, the company can also leverage the data collected as a result of its over a decade of clinical experience to deliver better patient engagement. The reason is that data remains a critical element of AI, and the more data a company possesses, the better its Large Language Models can be trained, resulting in the software applications being more intelligent.

In this respect, the company's ML (machine learning) algorithms have already surfed through existing data for detecting patterns related to behavior. These have already been applied to identify individuals at risk for self-harm and the corresponding alert escalated to the concerned therapist, but, it is important to assess the way Talkspace is monetizing this feature. One strategy is to charge for it as an optional service and another is to provide it for free in certain use cases for product differentiation purposes. However, instead of getting enthralled by AI, it is important to first get more details as to how things work out. Furthermore, according to an article in Time magazine, AI therapeutic chatbots by certain companies are now being used to treat anxiety which signifies that it is also important to assess whether these can eat into Talkspace's market share.

In conclusion, despite its undervaluation status, this is not a stock to invest in at this juncture. It is certainly growing at double-digit figures, there are additional sales opportunities, the balance sheet remains strong, and it is on a path toward profitability, but competition remains strong, and new threats may emerge. As such, a management update on sales guidance for fiscal 2024 is required.

Finally, the stock has been volatile losing 1.8% over the last five days while Teladoc has lost 1.54% as shown below, and one of the reasons could be because of a recent higher-for-longer rhetoric which casts doubts that the Federal Reserve will start easing monetary policy any time soon.

{kind=link}

Hence, since 2024 is expected to be the year of rate cuts, any associated delay can cause market conditions to be volatile.

For further details see:

Talkspace: Opportunities In Online Mental Health And AI, But Faces Competition