SPG - Tanger: Juicy 10% Hike But Not The Best Option For Your Dollars

Summary

- We had a neutral rating on Tanger Factory Outlet Centers and felt the bears would struggle to push this down.

- The REIT has held up well, all things considered.

- We examine the current metrics and update our outlook.

- We suggest a better name for your investment dollars.

When we last covered Tanger Factory Outlet Centers Inc. ( SKT ) we recognized that the bull-bear face off was unlikely to be decided outside of a big market crash. Specifically we concluded,

SKT has made it out of the other side of the pandemic and its open-structured malls are a refreshing breath of fresh air. Longer term trends are decisively down and we don't see that changing easily. Those headwinds aside, the shorter-term situation makes it hard for bears to get traction here outside a very large generalized selloff in the market. The stock lands once again in the neutral zone and we remain sidelined.

Source: No Time To Build-A-Bear Case

Not becoming bearish was the correct call as SKT outperformed the broader S&P 500 ( SPY ) since then and by a substantial amount when total returns were examined.

Returns Since Last Article (Seeking Alpha)

SKT also has held up remarkably well in light of the recent REIT selloff. That fact and the big dividend hike made us take another look at this once famous REIT.

Q2-2022

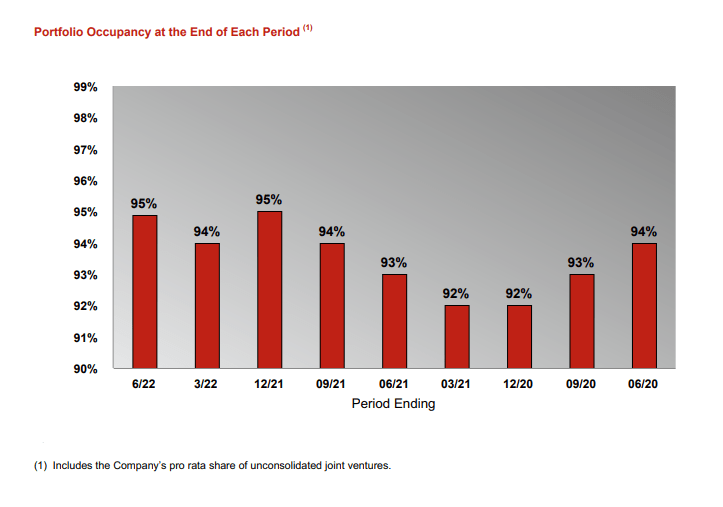

The headline numbers were good and SKT narrowed the guidance for the year. Core Funds From Operations (FFO) came in at $0.45 per share, compared to $0.43 per share for the prior year period. The numbers showed that SKT was back towards reaching its mid-50 cent run-rate which it had achieved pre-COVID-19. Portfolio occupancy grew once more and reached early 2020 levels.

{kind=link}

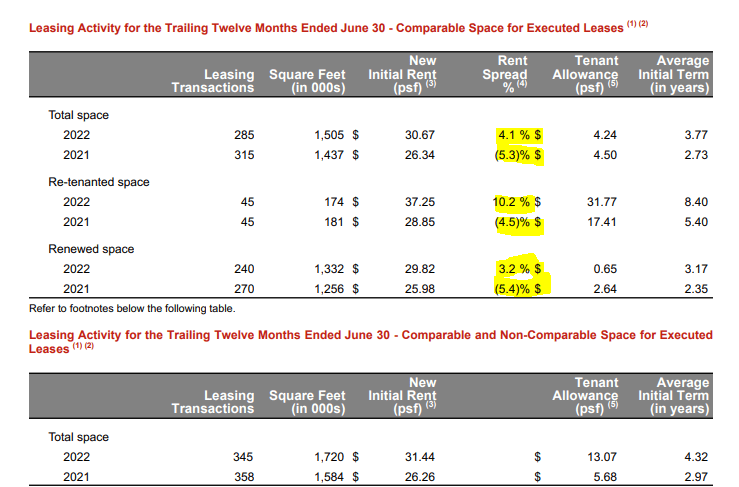

This occupancy is the critical aspect of enrolling investors. SKT has to constantly prove that the industry is not dying and so far it continues to show that the outlet model is here to stay. On our previous coverage, we had noted the extraordinarily bad leasing spreads which would reduce future income for this REIT. Those, at the time, were deep in the red. SKT has fixed this problem as well. Leasing spreads have been robust and continue to get better.

{kind=link}

This is the inflation impact flowing through as nominal prices tend to move up, and the results look good, even if they lag official inflation measures.

Outlook

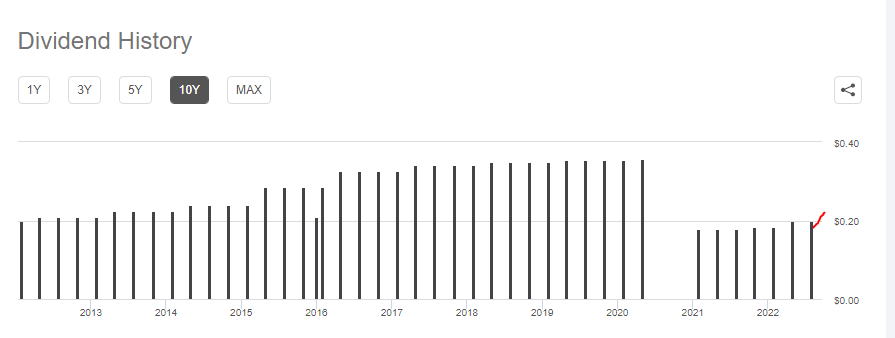

We expect Q3-2022 to be strong as well (for leasing spreads) but then we should start seeing some softness in renewals and leasing spreads as the world steps back expansions in light of the much anticipated recession in 2023. Fundamentally, SKT's stock price is supported by a low FFO multiple and a modest dividend yield. That dividend was just raised by 10% to 22 cents a quarter, but remains far below its pre-COVID-19 levels.

{kind=link}

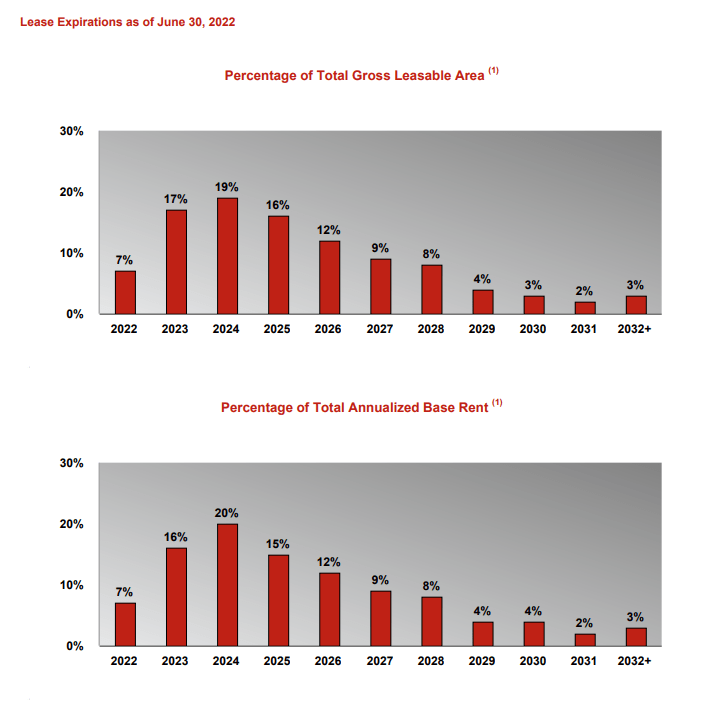

What the company deserves credit for, is managing its leasing renewals in a great manner. That work will continue and 2023-2024 should see a third of its portfolio come up for negotiations.

{kind=link}

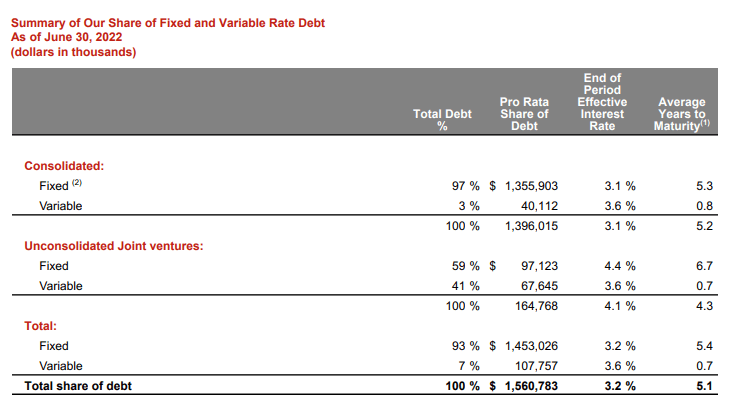

SKT has also maintained a very strong balance sheet with predominantly fixed rates and a weighted average maturity of 5.1 years.

{kind=link}

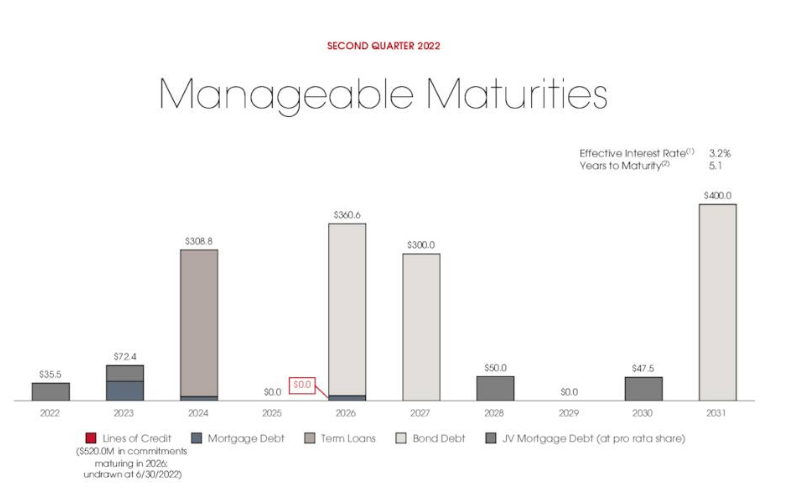

2022 and 2023 don't have significant maturities and SKT can easily pay that off with cash flow.

{kind=link}

The 2024 term loan represents a modest hump but SKT had about $290 million in current assets ( see 10-Q ) on last check.

{kind=link}

That alongside the incoming cash flow is more than sufficient to not even worry about the term loan.

Verdict

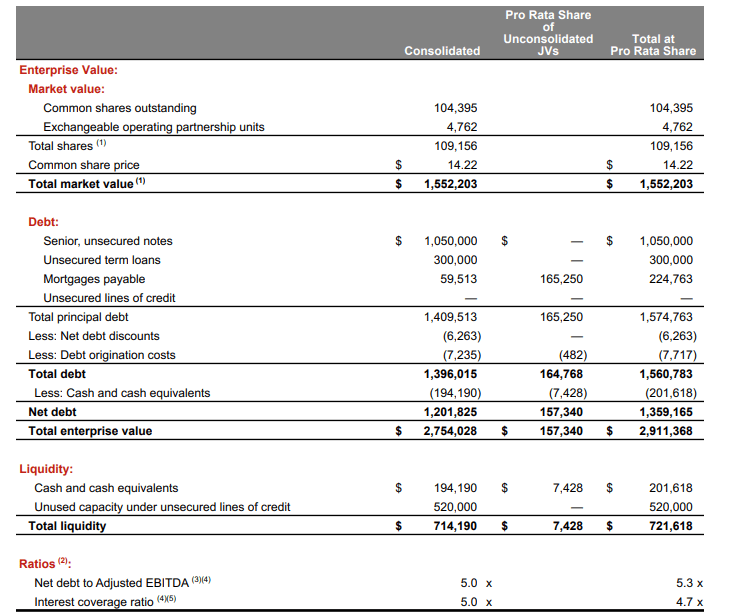

SKT looks to have come out of the COVID-19 trauma and is really well placed to handle the recession ahead. At 8X FFO with 5.0 net debt to EBITDA, there is nothing wrong with buying the stock.

{kind=link}

Well actually there is one thing wrong with it. Investing is always done on a relative and absolute front and while SKT looks ok here, there is really no reason to go with it if you have a far better alternative. We are talking about Simon Property Group ( SPG ) and if you need the retail exposure, SPG looks better for a few reasons.

The first reason being size and scale. There is really no comparison there.

The two are at about equal footing as far forward FFO multiples are concerned, so we would call that part a draw.

From a credit standpoint, SPG is better. SKT has of course done well to maintain the IG rating.

{kind=link}

But SPG's A- by S&P and A3 by Moody's ( MCO ) gives it an edge.

Finally, from a dividend standpoint, SPG"s 7.2% also gives investors some extra comfort while waiting for capital returns.

From our point of view, SPG is just in the buy-zone, while SKT is a bit outside it. We rate SKT at a Hold/Neutral.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Tanger: Juicy 10% Hike, But Not The Best Option For Your Dollars