UA - Tapestry's Purchase Of Capri Holdings: An Uncertain Fit

2023-08-11 12:52:04 ET

Summary

- Tapestry, Inc. agreed to acquire Capri Holdings Limited in an all-cash deal valued at $8.5 billion, causing shares of Capri Holdings to soar and shares of Tapestry to plummet.

- The deal will unite six leading fashion brands and generate around $12.1 billion in annual revenue, with potential for cost savings and supply chain improvements.

- Tapestry's exposure to attractive markets will increase, and the product lineup will diversify, providing more stability and protection in the long run.

- Though the deal makes sense conceptually, there are risks involved, and it's not entirely clear that this deal is optimal.

August 10th proved to be a rather big day for the fashion community. On that day, news broke that Tapestry, Inc. ( TPR ), the owner of major fashion brands like Coach, Kate Spade, and Stuart Weitzman, had agreed to acquire Capri Holdings Limited ( CPRI ) in an all-cash deal valuing the company at $8.5 billion on an enterprise value basis. This sent shares of Capri Holdings soaring, closing up 55.7% in response to the news.

Investors in Tapestry were, to put it charitably, less enthusiastic. I say this because shares of the fashion house plummeted 15.9%. Digging into the deal, I do see a couple of reasons why the market may have behaved this way. At the same time, I also believe that there could be some value here for Tapestry if it can play its cards right.

Assessing the deal

As I mentioned already, the current deal that was just announced will have Tapestry absorb Capri Holdings, the owner of Versace, Jimmy Choo, and Michael Kors, in an all-cash transaction. The price per share that the company is paying comes out to $57. This represents a premium of 64.7% compared to the $34.61 that shares of Capri Holdings were trading at the day prior to the announcement. In response to the news, units of Capri Holdings shot up 55.7%, closing at $53.90 apiece. The total buyout price implied works out to $6.8 billion for the equity and $8.5 billion when you include net debt.

{kind=link}

As the management team at Tapestry Simply put it, this transaction will unite six leading fashion brands under a single enterprise. It's expected that the combined entity will generate around $12.1 billion worth of revenue per annum, with Tapestry’s operations accounting for roughly 55.4% of that total. There are a number of reasons why this deal, conceptually at least, makes sense. For starters, by tackling operating costs and supply chain improvement opportunities, management seeks to generate $200 million in annual run rate synergies. Of course, this will not happen overnight. The expectation is that these synergies will develop over the first three years of the companies being combined.

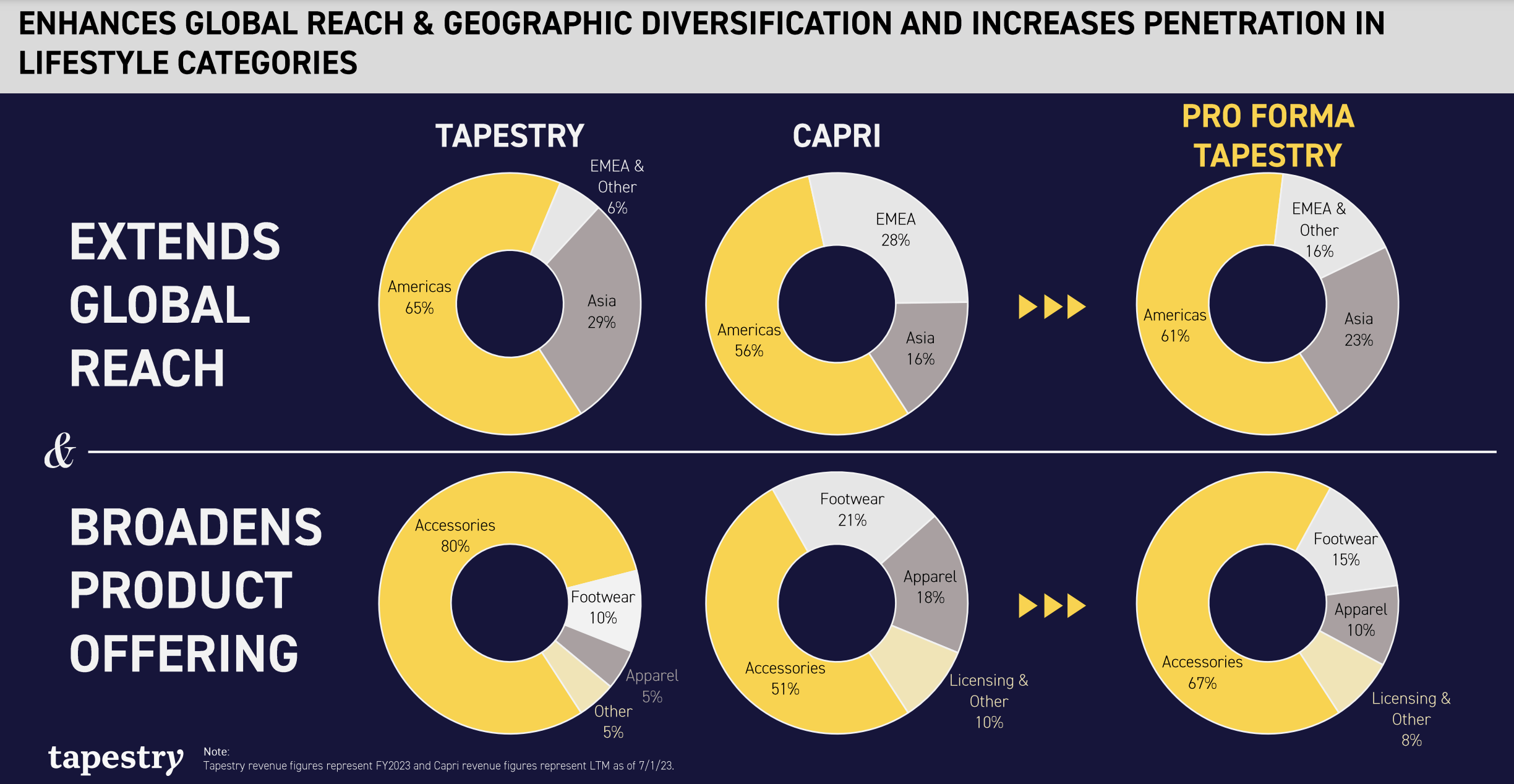

One of the really great things about this transaction is that it should result in Tapestry growing in some very attractive markets. At present, 65% of the company's revenue comes from the Americas. 29% comes from Asia, while the remaining 6% comes from the EMEA (Europe, Middle East, and Africa), as well as "other" regions. Following the completion of the transaction, its exposure to Asia will shrink some to about 23%. However, its exposure to the EMEA and other regions will grow to 16%. The product lineup will also look meaningfully different following the completion of the deal. At present, 80% of the revenue generated by Tapestry falls under the accessories category. 10% falls under footwear, while 5% is attributable to apparel. After the deal is completed, accessories exposure will drop to 67%. But footwear will grow to 15% while apparel will double to 10%. Greater diversity in terms of the products that it has should provide it with more stability and protection in the long run.

{kind=link}

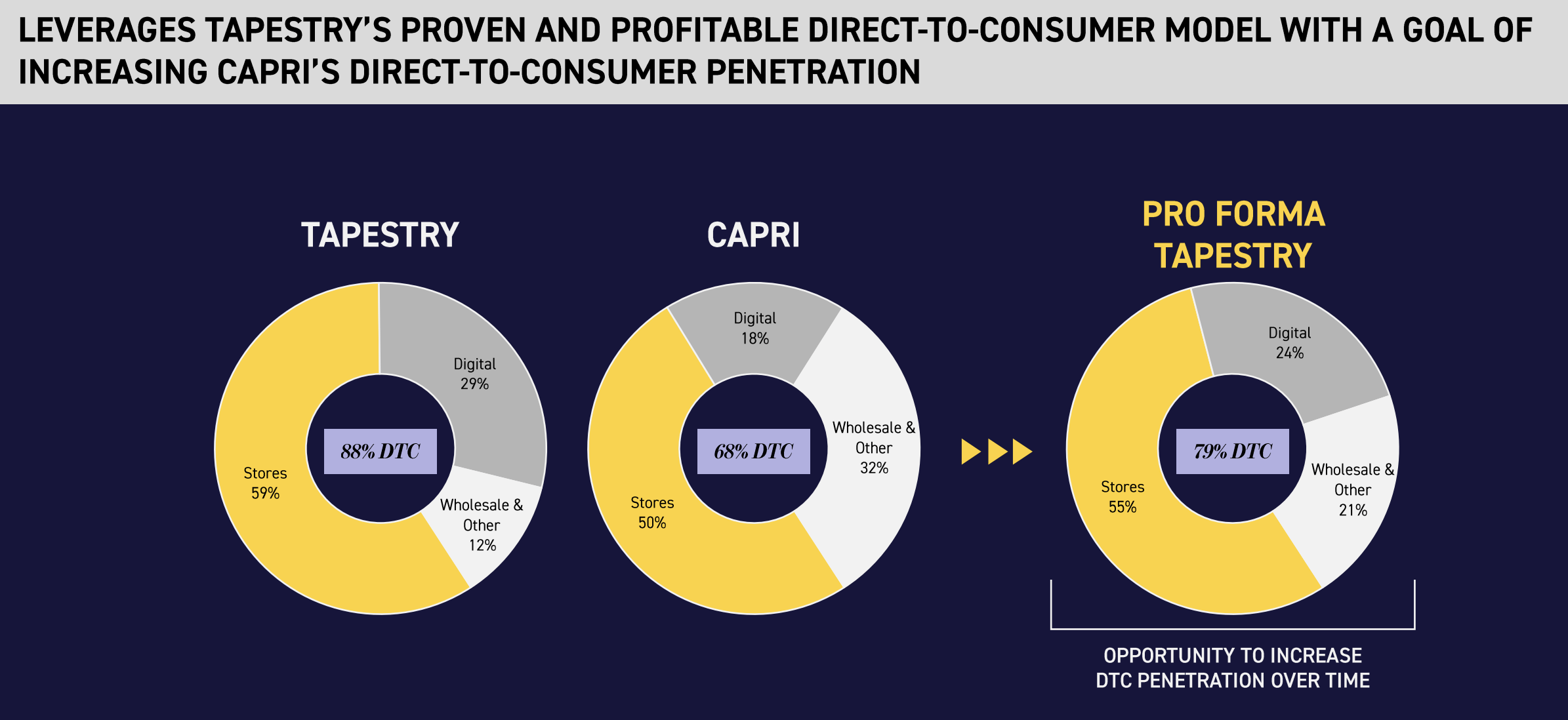

It's also likely that Tapestry can use its robust direct to consumer penetration to help grow operations for Capri Holdings. At present, 59% of the revenue that Tapestry generates comes from stores. Another 29% comes from digital means. To put this into context, these numbers for Capri Holdings are only 50% and 18%, respectively. That's a 20% difference combined between the two enterprises. Management hopes that the direct-to-consumer category can become even more significant in the years to come.

{kind=link}

Purely from a valuation perspective, the transaction does not look bad. The implied EV to EBITDA multiple that Tapestry is paying comes out to 9. If synergies are ultimately realized, this will drop to roughly 7. But investors should not bank on those synergies coming to fruition. It's better to be overly conservative and surprised in a positive way than to be surprised in a negative way. No estimates were given for operating cash flow. But I did take the EBITDA generated by Capri Holdings during its latest completed fiscal year and stripped out interest expense that the company paid for that year. I also assumed that the new financing that Tapestry locked down for the deal would come in at 6% per annum. This would result in operating cash flow of $651.5 million. That implies a price to adjusted operating cash flow multiple of 10.4 after factoring in attack shield with a 21% effective rate and no taxes on overall income. As part of my analysis, I ended up creating the table below. In it, you can see five similar firms that I compared Capri Holdings to.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Capri Holdings Limited |

| 10.4 |

| 9.0 |

| Columbia Sportswear ( COLM ) |

| 48.5 |

| 8.4 |

| Under Armour ( UAA ) |

| 36.5 |

| 8.0 |

| PVH Corp. ( PVH ) |

| 20.8 |

| 9.5 |

| Gildan Activewear ( GIL ) |

| 21.5 |

| 9.4 |

| Ralph Lauren ( RL ) |

| 20.5 |

| 8.4 |

Even with this higher price to adjusted operating cash flow multiple, the price being paid for Capri Holdings is lower than what we get for any of the five companies I compared it to. In fact, the price is considerably lower. Now, when it comes to the EV to EBITDA multiple, that picture is a bit different. Three of the five companies ended up being cheaper than our prospect. All things considered, this makes the deal look reasonable for both parties, but there are some risks that shareholders of Tapestry now have to put up with.

First, and perhaps most importantly, is the debt burden. Tapestry locked down $8 billion in financing to make this deal go through. Realistically, all or almost all of the purchase will involve debt since the firm has only $651.8 million in cash and cash equivalents on its books. Having too much debt kindly asking for trouble, especially if financial performance begins to falter. And that leads me to the second issue.

{kind=link}

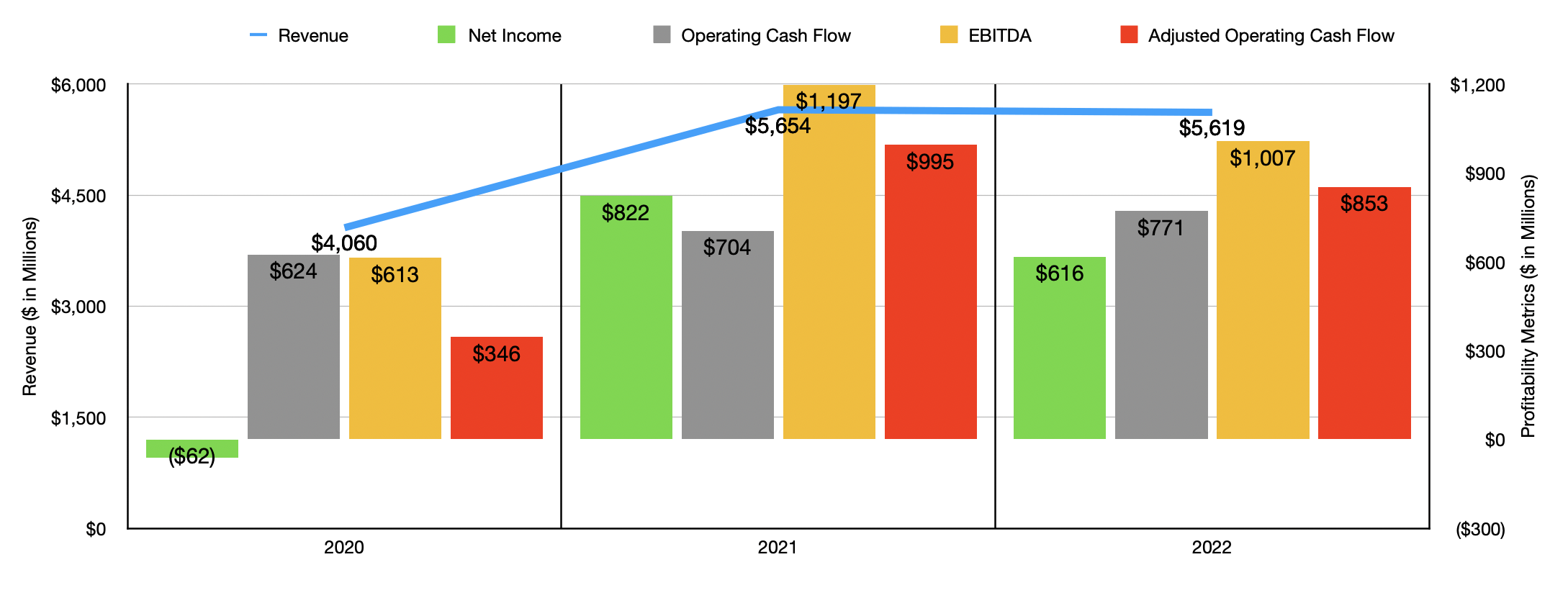

For years now, financial performance achieved by Capri Holdings has been somewhat mixed. As you can see in the chart above, revenue did pop from the 2021 fiscal year to 2022. But sales then poured back some in 2023. The good news to this is that the decline was driven by a $333 million hit associated with foreign currency fluctuations. Constant currency revenue actually grew by 5.3% from 2022 to 2023. But higher costs, combined with the foreign currency fluctuations, did hit the bottom line to some extent as well. I would definitely not call that performance bad.

But when you look at the first quarter of the 2024 fiscal year for Capri Holdings, one of the first things you might notice is that, even on a constant currency basis, the Michael Kors brand that accounts for a large chunk of the firm's revenue, reported a 13.4% drop in sales because of weak demand. The fashion industry is incredibly fickle and seeing any brand report such a steep decline in revenue can be a warning that the future might be painful. But of course, it's partially because of this that Tapestry is paying a price that is similar to what other firms are trading for on an EV to EBITDA basis rather than paying a premium.

Takeaway

I would definitely say that the transaction between Tapestry and Capri Holdings is interesting. If synergies can be realized and if the core operations of both companies can go on to continue growing, the picture for shareholders in Tapestry, Inc. could be quite positive. The deal looks fair, as opposed to rich. So if the picture does turn out well from a fundamental perspective, investors in Tapestry absolutely will be the winners from the deal.

But, as I pointed out, there are certain risks that come with it as well. High debt and recent weakness associated with Michael Kors should not be taken lightly. Until we get greater clarity into the health of Capri Holdings on a forward basis, I am taking a neutral stance on the transaction. But I would definitely continue to watch and see what transpires after the deal closes, or if it closes, in 2024 like management has indicated.

As for what investors should do now, that's entirely up to each one's risk profile. There is currently a spread between the share price that Capri Holdings Limited sports and the $57 per share that it should be acquired for. That does leave some upside, but it also brings with risk should the deal fall through. I view the latter scenario as quite unlikely, but it's definitely not 0%.

For further details see:

Tapestry's Purchase Of Capri Holdings: An Uncertain Fit