TRGP - Targa Offers Some Of The Best Growth In The Midstream Space

2023-12-07 09:48:51 ET

Summary

- Targa Resources is an attractive option in the midstream space with strong growth prospects tied to the Permian Basin.

- The company also has direct commodity price exposure to NGLs and natural gas, and should benefit from any rebound.

- Targa is aggressively returning capital back to shareholders through dividend hikes and buybacks and looks attractive at current levels given its growth prospects.

With some of the best growth prospects in the midstream space and tied to the Permian Basin, Targa Resources ( TRGP ) looks like an attractive option in the midstream space.

Company Profile

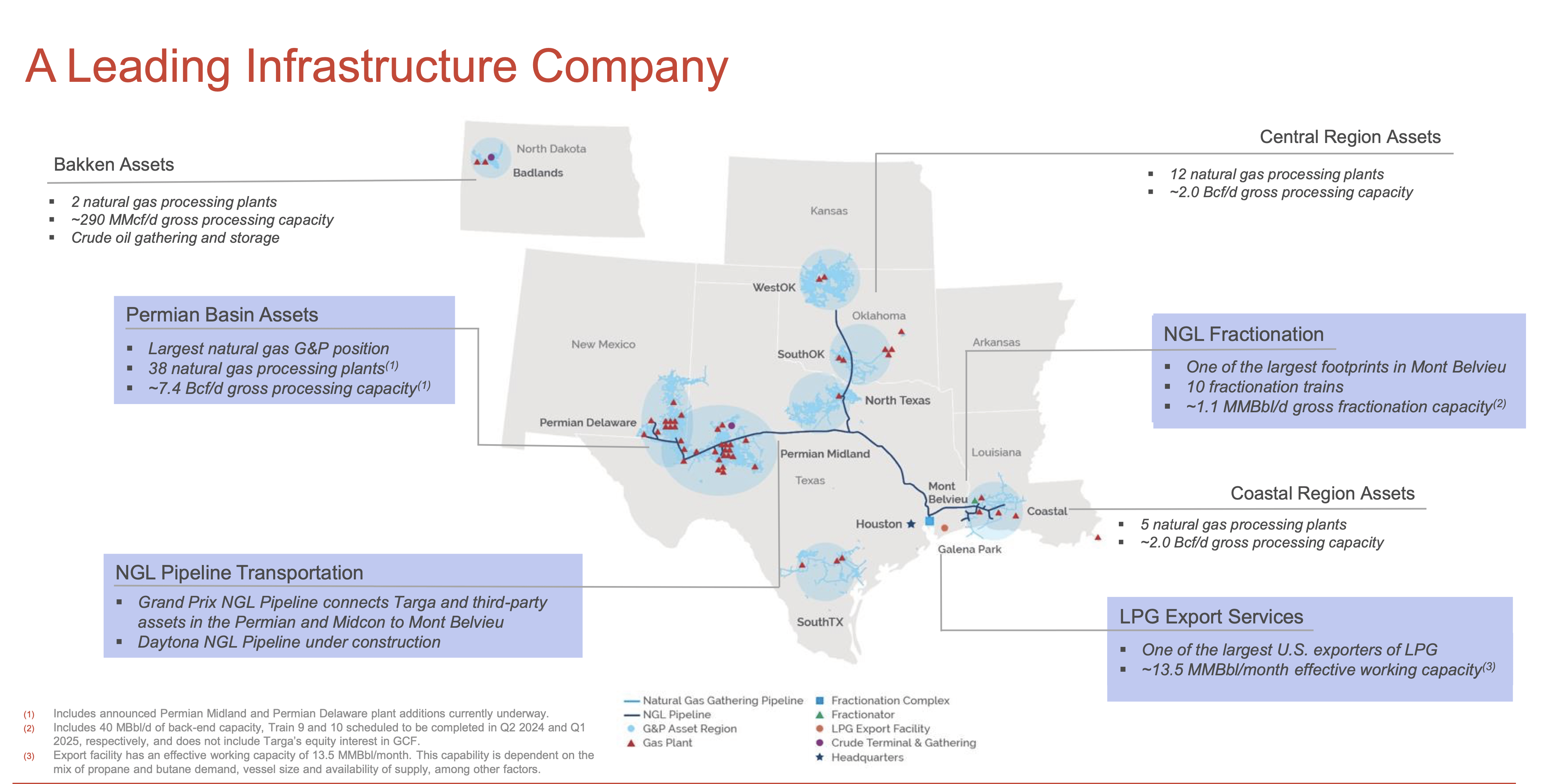

TRGP is a midstream company that operates in two segments: Gathering & Processing (G&P) and Logistics & Transportation. The segments are similar in size, with its G&P segment slightly larger. The business is largely fee-based with long-term contracts in place.

With its G&P segment, the company is involved in the gathering, processing, treating, and transporting of natural gas, and to a lesser extent the gathering, storing, terminaling of crude oil. About 80% of its 2023 volumes are fee based or percent of proceeds ((POP)) with a fee floor, while the rest is POP without a fee floor.

The segment has assets in a number of basins, including the Eagle Ford, Barnett, Williston, and Arkoma. However, the Permian is its biggest basin, representing about 75% of the segment’s operating margin.

The Logistics & Transportation, meanwhile, consists of NGL transportation & fractionation, LPG exports, and marketing. Its most important pipeline asset is its Grand Prix pipeline, which connects its gathering and processing assets throughout the Permian Basin, North Texas, and Southern Oklahoma to its fractionation and storage assets at Mont Belvieu.

{kind=link}

Opportunities and Risks

Midstream companies are generally known for being toll-road providers that have volumetric exposure but not much direct commodity price sensitivity. However, with a large network of legacy processing plants, TRGP has historically been one of the midstream companies that has had a good amount of commodity price exposure through its percent-of-proceeds and percent of liquids agreements.

Generally speaking, under POP contracts, TRGP gets an agreed upon percentage of the proceeds from the sale of NGLs (natural gas liquids) and residue gas, and in some case the percentage of an index based price. Under percent-of-liquids agreements, which it gets from the coastal portion of its G&P business, it receives an agreed upon percentage of the actual proceeds of the NGLs it extracts.

As recently as 2019, about 50% of TRGP’s G&P volumes had POP contracts without fee floors. This year, POP contracts without floors will make up about 20% of its G&P volumes. While that is a significant reduction, it still leaves TRGP with a fair amount of direct commodity price exposure.

TRGP’s exposure to natural gas and NGL prices can be seen in its Q3 G&P segment adjusted operating margins, which fell -6% year over year despite natural gas volumes being up 17% and NGL production up 23%, as nat gas prices fell -70% year over year and NGL prices were -40% lower. Now the company does hedge, but a 30% increase in nat gas and commodity prices was about $100 million in upside, while a -30% decrease was about -$60 million from its earlier assumptions.

A rebound in NGL and nat gas prices in 2024 could be a nice boost to the firm. However, there is also some risk if prices fall as well.

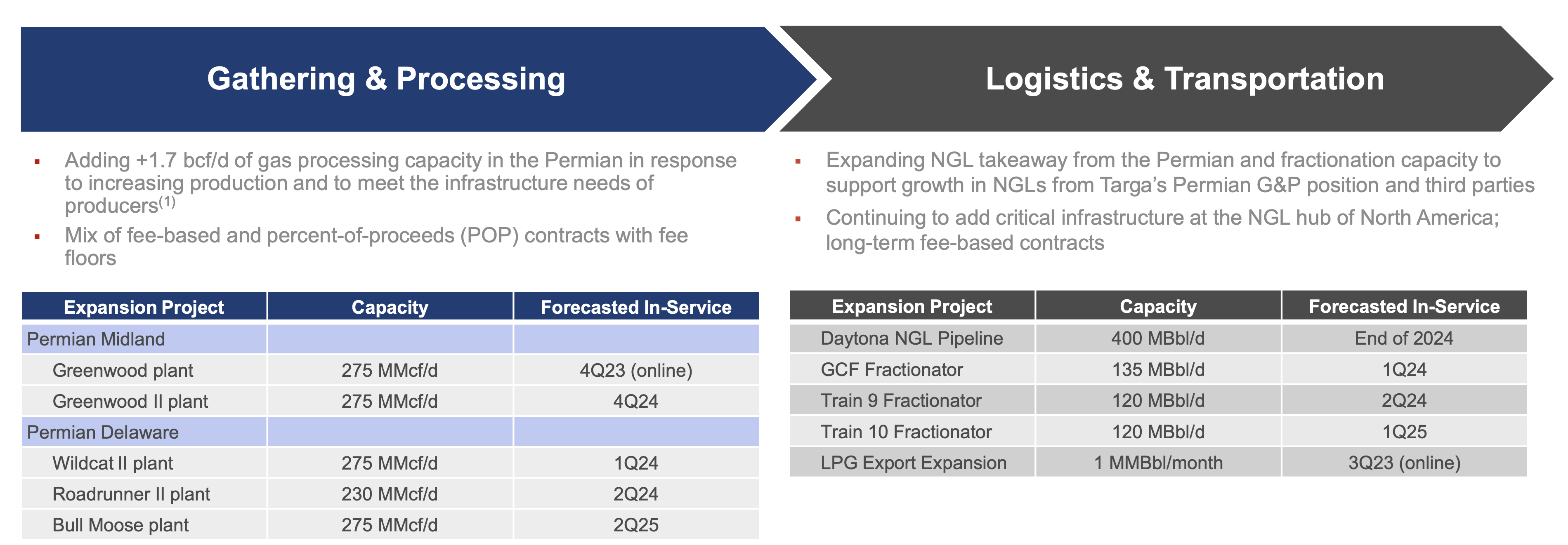

Growth projects are another big opportunity for TRGP, with six projects expected to come online in 2024 and two scheduled for 2025. The company will add over 1.7 bcd/d of gas processing capacity in the Permian over the next year and half. Its Greenwood plant in the Permian Midland came online earlier this quarter, and will be followed by an expansion set for Q4 of 2024. It will also add three Permian Delaware plants between Q1 2024 and Q2 2025.

In addition to its new gas processing plants, TRGP’s Daytona NGL pipeline is projected to come online by the end of 2024. It will also add fractionation capacity, as well as expand its LPG export capabilities.

{kind=link}

In total, TRGP will spend between $2.0-2.2 billion on growth capex this year. It expects to spend a similar amount in 2024, before seeing a significant reduction in 2025. At a 6x investment multiple, that would equal about $700 million in growth coming from these projects over the next few years.

TRGP is also looking to get more aggressive in returning cash to shareholders, saying it wants to return 40-50% of its operating cash flow to shareholders through buybacks and dividends. The company already announced a 50% dividend hike to $3.00 a share in November. It has a $1 billion buyback program in place, and it repurchased $132 million worth of stock in Q3 and $333 million year to date through September. Its end of Q3 adjusted leverage was 3.7x.

When it comes to risks outside of commodity prices, it does have basin exposure to the Permian. This is one of the best basins to have exposure to as it continues to be the oil growth engine in the U.S., but it has also been plagued by nat gas takeaway issues as well.

There is also a lot of competition for NGL takeaway in the Permian, and the company did see some volumes roll off in the Delaware Permian in Q3 as well. This led to the company seeing a -12% sequential drop in Delaware Permian NGL production and a -3% decrease in nat gas volumes.

Contract roll-offs and renewals are also a risk, but when asked the company didn’t indicate that there were any other large contracts rolling off soon.

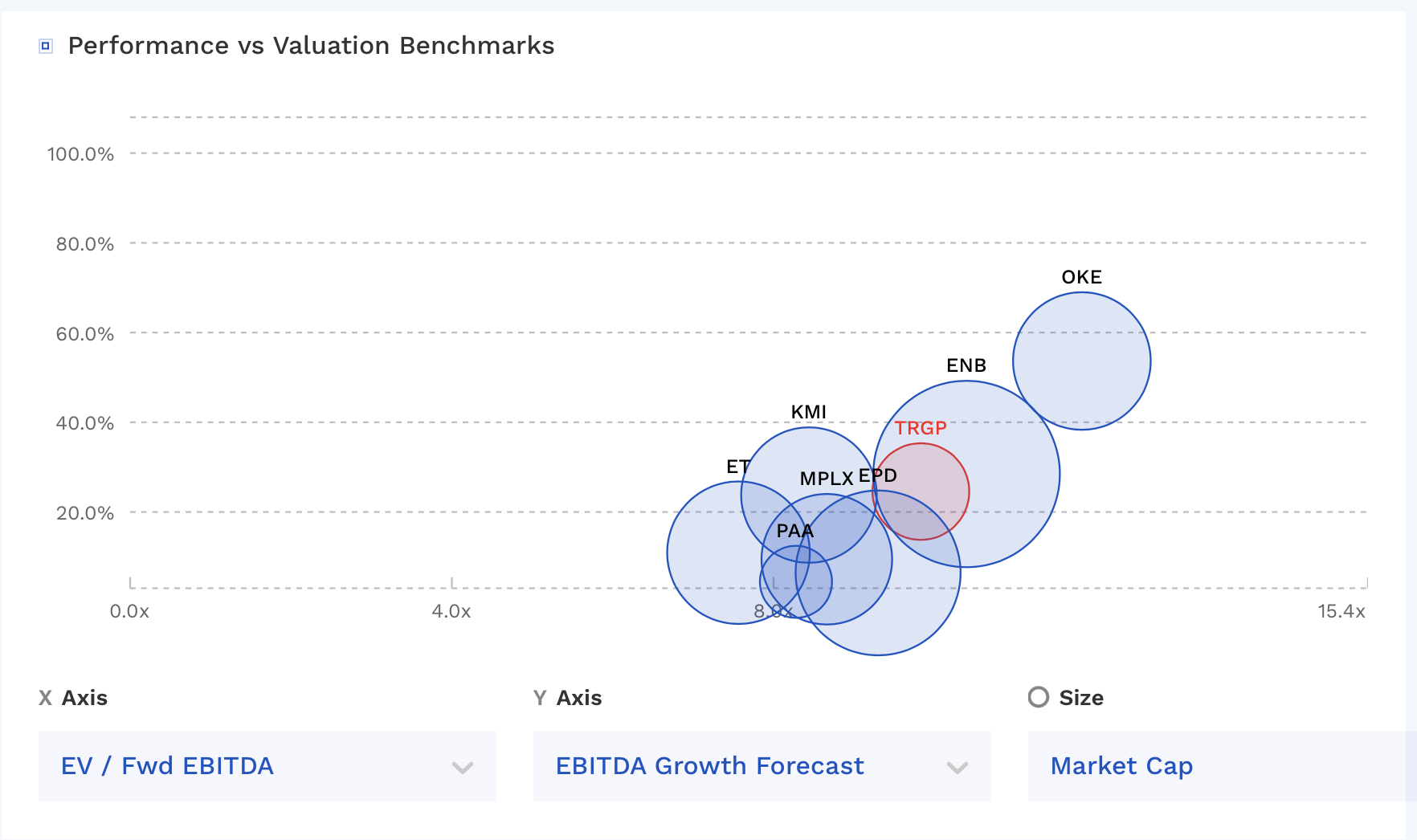

Valuation

TRGP trades at 9.9x the 2023 EBITDA consensus of $3.53 billion. Based on the 2024 EBITDA consensus of $3.88 billion, it is valued at 9.0x. Based on 2025 estimates of $4.3 billion, it trades at 8.1x.

The stock has a free cash flow yield of about 2% and DCF yield of around 12%. It pays out a dividend yield of 3.3% based on its recently increased dividend.

TRGP is one of the more expensive midstream operators, although it has some of the best growth prospects over the next couple of years due to its growth projects.

{kind=link}

Based on an 8-10x multiple on 2025 adjusted EBITDA, I’d value TRGP between $90-$127, with the midpoint at $108.50.

Conclusion

TRGP has some of the most commodity price exposure among midstream stocks, but it also has some of the best opportunities. This stems from its strong backlog of growth projects and its ability to benefit from a rebound in NGL and nat gas pricing.

TRGP doesn’t give investors the same yield as most midstream stocks, but the company recently raised its dividend aggressively and it has been buying back stock. While it does carry some risk, I think the upside in the stock warrants a “Buy” recommendation at this time. My year-end 2024 target price is around $110.

For further details see:

Targa Offers Some Of The Best Growth In The Midstream Space