TH - Target Hospitality: Hitting The Center Of Success

2023-06-06 21:35:29 ET

Summary

- Target Hospitality Corp. shows solid performance and a well-grounded financial positioning.

- The company's expansion and focus on the government and HFS-South segments, along with strategic pricing, contribute to its growth and resilience amidst market volatility.

- Market opportunities continue to outweigh market risks as recession fears ebb.

- Target Hospitality's stock price remains undervalued, with a potential 35% upside in the next 12-18 months, making it a recommended buy.

Target Hospitality Corporation (TH) shows a solid performance amidst market volatility. Thanks to its increased reliance on the government segment, this move can be a double-edged sword, but it appears more favorable for the company. As recession fears ebb, more opportunities may be on the horizon. With the rebounding oil production in North Dakota and Texas, prospects remain optimistic. But what makes it a well-grounded company is its impeccable financial positioning. Its healthy Balance Sheet shows its steady cash increase and decreasing borrowings. It remains sustainable to cover its current size, borrowings, and capital returns. Unsurprisingly, the stock price keeps increasing even after its sharp rebound in 2022. TH stock remains an ideal bargain with decent upside potential.

Company Performance

The past three years have been challenging for Target Hospitality Corporation. It suffered from limited business operations and restricted outdoor activities. Yet, it showed its durability and resilience as it regained its footing in the next two years. Over the past year, the business grew exponentially and enhanced its diversification strategies. It saw and seized more opportunities as the US economy rebounded. Also, the Russo-Ukrainian war provided unexpected tailwinds for the company. The increased demand for oil made Texas and North Dakota pivotal for the business and public sectors. The demand influx helped offset the impact of the rising prices.

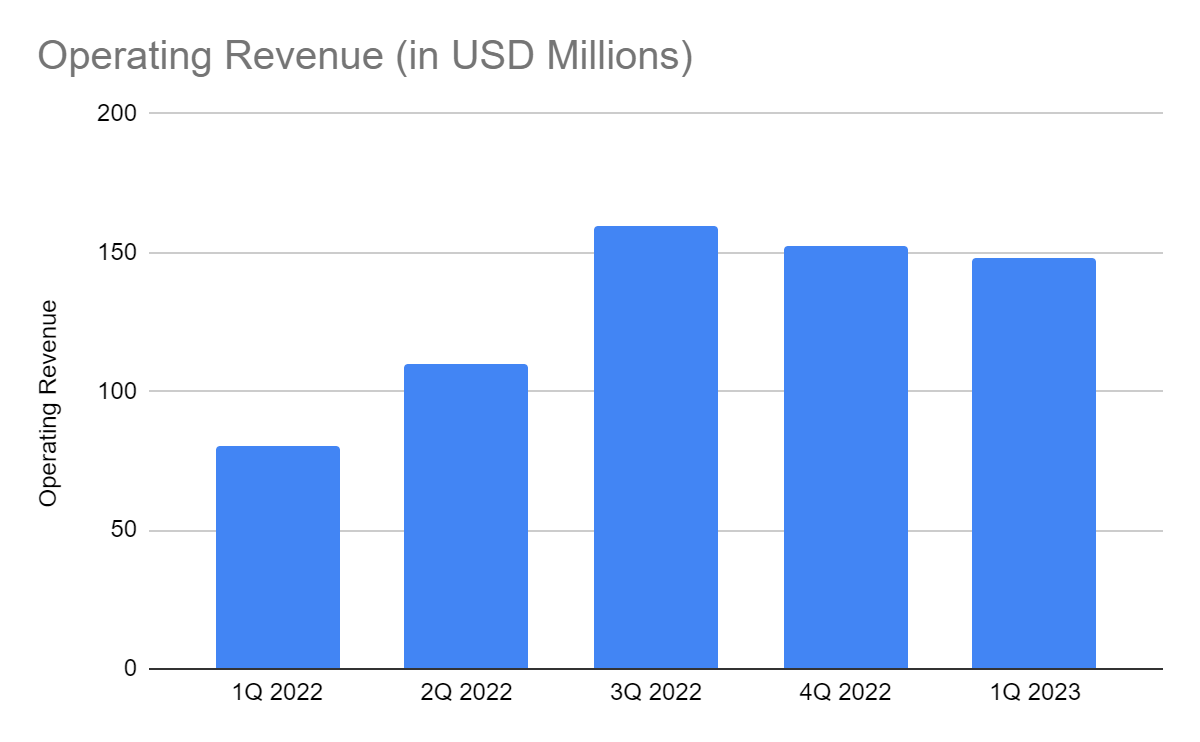

Target Hospitality started the year strong amidst the volatile market landscape. The company generated revenues of $147.82 million , an 84% year-over-year increase. This massive growth was a testament to its secure market positioning. Over the past year, the business grew exponentially and enhanced its diversification strategies. Despite inflationary headwinds, it navigated the stormy market with its strategic business model. The capitalization on expansion was instrumental in its sustained growth. In 2022, it already had 27 communities with 16,830 beds, about thrice its size in 2014.

{kind=link}

Operating Revenue (MarketWatch)

It was most evident in the government segment. It was logical since the company increased its focus there. In recent years, its percentage of total revenue has risen to 72%. So, it was no surprise that government revenues increased by 134% . It could also be attributed to its expanded humanitarian community activity. It secured $265 million in minimum revenue commitments for its 2,400-bed government services contract. Furthermore, there was a minimum revenue contract of $313 million for displaced people. It made Target reliant on the government but provided secure revenue streams. It also put Target at the forefront of humanitarian efforts, which could lead to more partnerships. It could also increase its exposure to the area and entice more contracts from the public and private sectors.

The HFS-South segment also flourished with revenues increasing by 13%. It could be attributed to the increased investing activities of the company. It had $31.8 million of CapEx, focusing on asset acquisitions to expand the segment. That way, it could meet the increasing demand and fortify its market presence.

Its active service repricing was also vital in maintaining its solid customer base amidst the elevated prices. Increasing its operating capacity with strategic pricing was a wise move. It was also timely, given the stable economy of Texas and rebounding oil production in North Dakota . These changes led to an influx of field workers in the Permian Basin and North Dakota. The rebound in oil mining and drilling meant more demand for Target’s beds.

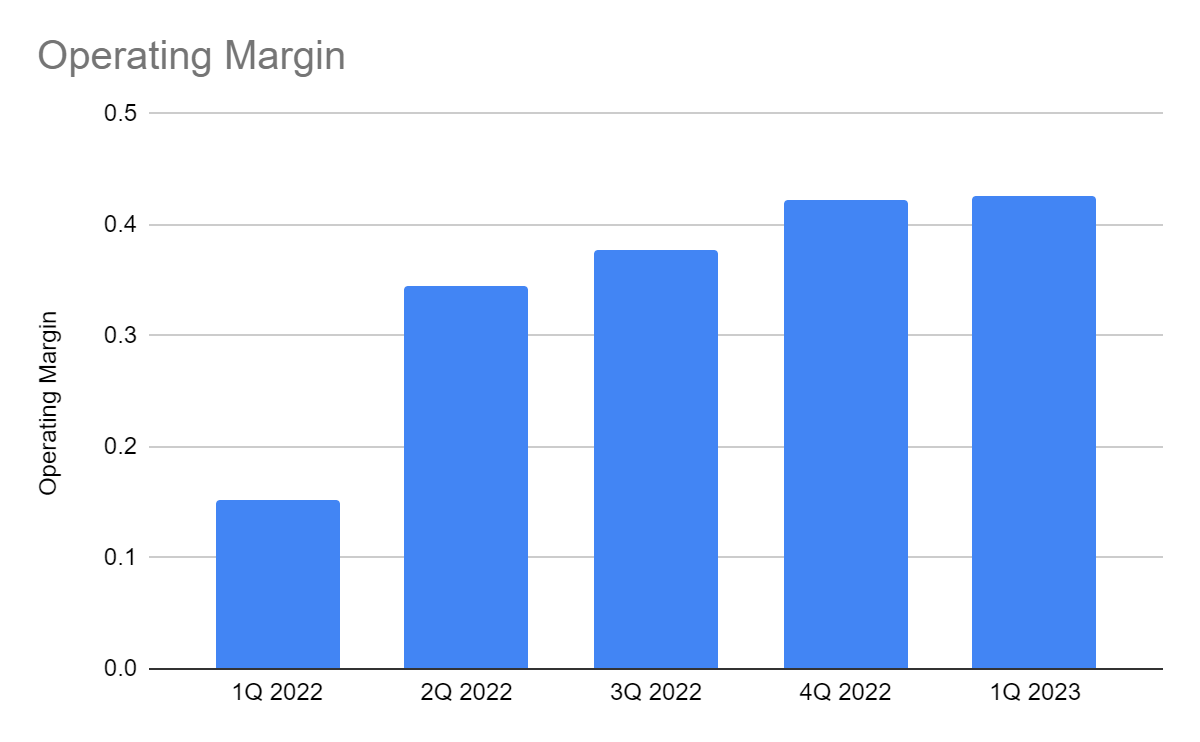

But what made Target Hospitality solid was its prudent and efficient asset management. The elevated prices were a threat to its operations. Yet, the company kept its costs and expenses low and manageable. They remained relatively flatter, which we could also attribute to the relaxing inflation. It peaked in 2Q 2022 at 9.1% before gradually decreasing. The downtrend sped up in 1Q, landing at 5%. Given this, the company managed its variable costs better. We can see its operating leverage increasing from 17% to 18%. Indeed, the company became more scalable with increased certainty in its viability. Its operating margin reached 43% versus 15% in 1Q 2022. It showed that the company stayed conservative amidst its expansion.

{kind=link}

Operating Margin (MarketWatch)

This year, the company faces the same headwinds. Prices are still elevated, so the cost of drilling and production remains high. Labor expenses may increase again to keep up with the rising prices and maintain employee productivity. But all its efforts will not go to waste since it is also expanding. Last month it acquired assets, which could support its expanded humanitarian community. This move could help support its government segment and receive more contracts. We will focus more on the risks and opportunities in the following section.

Why Target Hospitality Corporation May Remain Solid This Year

Macroeconomic risks still surround Target Hospitality Corporation. Interest rate hikes have cooled down recently, but actual rates are way higher than in the past three years. Likewise, prices stay elevated, so costs and expenses may increase more. Despite this, recession fears have started to ebb as inflation relaxes. At 4.9% , inflation has already dropped by 46% from the 2022 peak. Its positive impact may not materialize easily. But it may help TH determine its optimal production level to maximize its pricing flexibility and manage costs and expenses well. It can sustain revenue growth and stabilize margins.

The lower energy commodity prices may also be vital since Texas and North Dakota are the top energy sources in the US. On average, gasoline prices are only $3.666 per gallon, 27% lower than the 2022 peak of $5.032 per gallon. Meanwhile, oil and gasoline production in North Dakota rebounded by 11% in 1Q 2023. Even better, there may be an upsurge in the oil and gasoline industry as large economies increase their demand. The reopening of China borders after its hard lockdown is crucial since it accounts for a substantial portion of imports and exports. In the e-commerce industry, China accounts for 52% of the total sales. The US comes second with 19% of the global sales. With that, there may be increased economic activities across regions.

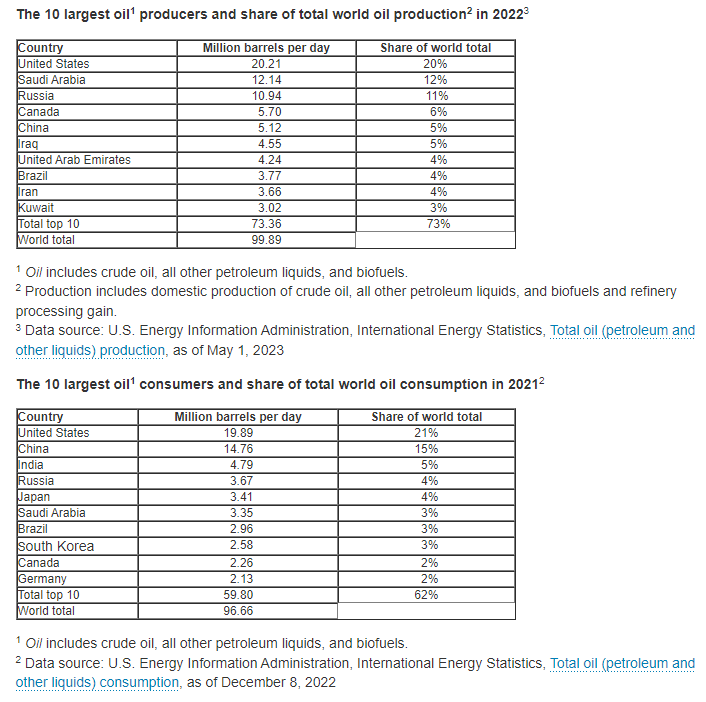

The ongoing war between Russia and Ukraine may shift the attention of many customers in the US. Note that the US is the top oil producer and consumer globally . As such, the US may need more oil reserves to suffice its needs and meet the increasing demand. Texas and North Dakota will be vital in this aspect. In turn, there may be more jobs, especially in the mining and drilling industry. Target Hospitality may capitalize on the strong market performance of the Permian Basin. In a recent report , the energy sector in Texas remains robust. Amidst the oil price decrease, rig counts and mining jobs increased. Oil production also reached a new all-time high of over five million barrels daily. Wages continue to increase, while unemployment remains stable. Given this, workers may be more attracted to stay in the area. Drilling and mining companies may see higher productivity. So, an increased demand for TH may take place. Its South and Midwest segment may expand more.

{kind=link}

Top Oil Producers And Consumers (US Energy Information Administration)

Oil Prices, Rig Counts, And Mining Jobs (Federal Reserve Bank Of Dallas)

Oil Production (Federal Reserve Bank Of Dallas)

Employment Trend (Federal Reserve Bank Of Dallas)

The current trend in the US property market may also provide unexpected tailwinds. Property sales rebound from 2022 lows is visible in Texas, particularly in the Permian Basin. With that, it may be challenging for many to purchase and rent properties. Median US prices decreased by 9% in 1Q 2023, but way higher than in the previous years. It may not lead to a property crash since shortages remain high, increasing from 6.5 million to 7.3 million housing units. Meanwhile, rental rates keep increasing, amounting to $2,018 on average, $107 higher than in 2022. In Texas, it rose by 0.31% from March to April. Given this, Target Hospitality may be crucial for many tourists and companies who plan to stay longer in Texas. Its humanitarian efforts may even entice more partnerships from institutions with similar goals. It may win more long-term contracts from the government, oil drilling companies, and mining companies. It may also receive more partnerships, which can raise its market reach and secure more demand.

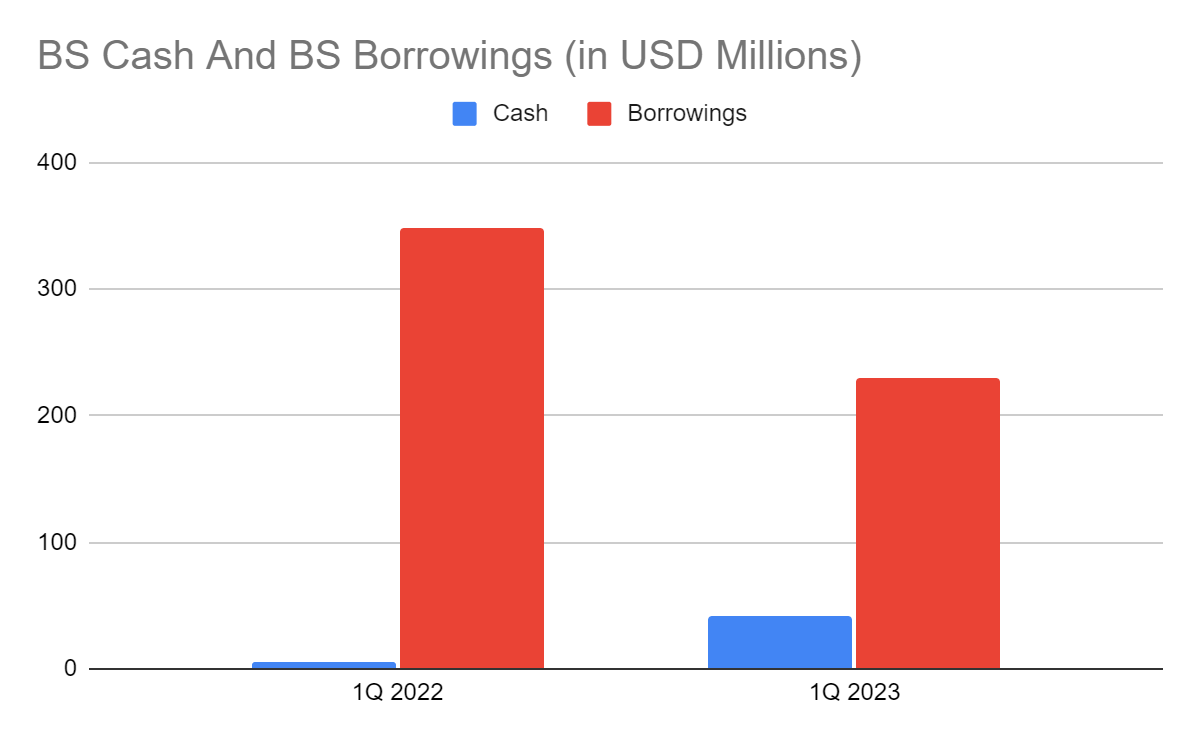

But at the end of it all, its well-grounded operations rests on its excellent financial positioning. It is an impressive aspect, given the continued expansion of the company. Its sound Balance Sheet shows its excess liquidity. Its cash levels reached $42.84 million, about eight times higher than in 1Q 2022. Meanwhile, borrowings decreased by 34%, landing at $229.92 million. It is a vital indicator, given the persistent interest rate hikes. Most importantly, its Net Debt/EBITDA Ratio remains low at 0.74x. As such, TH earns enough to cover all borrowings in a single payment. We can confirm its solid fundamentals in the Cash Flow Statement. Its Cash Flow From Operations rebounded to $17.88 million. Meanwhile, CapEx increased to $28.56 million. Despite their difference, the company has enough cash reserves to suffice it. We must note its expansion in the previous quarter to increase the capacity in the HFS-South segment. The good thing about it is that it didn’t have to raise its financial leverage. It was a wise move for the company to avoid the disruptive impact of higher interest rates. Given this, the company can maintain its current size and withstand the impact of macroeconomic volatility. The company maintains the balance between growth and viability with sustainability.

{kind=link}

BS Cash And Equivalents And BS Borrowings (Target Hospitality )

Stock Price Assessment

The stock price of Target Hospitality Corporation remains in a sharp uptrend. It maintains its momentum after rebounding from the 2021 lows. At $15.28, the stock price is 124% higher than last year’s value. Despite this, it remains a good bargain, given its sound fundamentals and expanding capacity. The Price-to-Earnings Ratio adheres to it, given the current PE multiple of 13x and NASDAQ EPS estimates of $1.43 . These give a target price of $18.59. Meanwhile, the EV/EBITDA Model shows that the stock price is fairly valued. It derives a target price of ($1.74 B EV - $0.187 Net Debt) / 101,373,000 shares = $15.32.

Target may not be a dividend-paying stock, but it has consistent capital returns through share repurchases. In 2022, it approved a program to repurchase $100 million of outstanding shares. Even better, investment returns are high using the cumulative EPS and stock price movement since 2019. It has a cumulative EPS of $0.97, but the stock price had an average increase of $1.87. So for every $1 increment in EPS, the stock price increased by $1.92. To assess the stock price better, we will use the DCF Model.

FCFF $109,500,000

Cash $42,440,000

Borrowings $229,920,000

Perpetual Growth Rate 4.4%

WACC 9.2%

Common Share Outstanding 101,373,000

Stock Price $15.28

Generated Value $20.72

The derived value also shows that the stock price is undervalued. There may be a 35% upside in the next 12-18 months. Shares are at a discount.

Bottomline

Target Hospitality Corp. is a solid company with robust operations amidst market volatility. It continues to expand with its increased focus on its best-performing segment. It maintains an excellent financial positioning to sustain its size and capital returns. Even better, the stock price remains at a discount despite its sharp increase. The recommendation is that TH stock is a buy.

For further details see:

Target Hospitality: Hitting The Center Of Success