TGT - Target Vs. Kohl's: How To Compare These Stocks And Choose The Best Investment

2023-06-29 09:00:00 ET

Summary

- The article provides a detailed comparison of Target Corporation and Kohl's Corporation, two retail stocks that have seen significant declines during the 2022/23 bear market.

- TGT's and KSS's store portfolios, their operational efficiency, balance sheet quality (with a focus on dividend security), individual weaknesses, and key risks are reviewed.

- Target's issues are manageable, with the company having navigated multiple recessions successfully. TGT stock dividend looks safe, but the stock is still too expensive considering the company's position.

- In contrast, Kohl's is a high-risk, high-reward turnaround play with considerable uncertainty. KSS stock dividend could be cancelled in favor of opportunistic share buybacks, but credit risk metrics are concerning.

Introduction

As a dyed-in-the-wool value investor, I welcome the current environment that has more or less rattled all but the top retailers (e.g., Walmart Inc. ( WMT ) and Costco Wholesale Corp. ( COST )). There are issues such as the significant increase in theft that more or less plague the entire industry, but there are also individual reasons for the poor performance.

In this article, I will compare Target Corporation ( TGT ) to Kohl's Corporation ( KSS ) - two stocks that declined massively during the bear market of 2022/23. TGT stock and KSS stock are down 28% and 39%, respectively, from their 52-week highs. From a dividend perspective, Kohl's is obviously screaming bargain (or value trap) with a current yield of 8.8%. Target's yield is much more conservative at 3.3% currently, but keep in mind that the company is a dividend king with a 52-year track record .

I provide a brief overview of Target and Kohl's, have a look at their store portfolios, discuss their operating efficiencies, balance sheet strength (with an emphasis on dividend safety), point out key risks, and conclude by answering which of the two is the better retail stock now.

Overview Of Target Corp. And Kohl's Corp.

Target, the Minnesota-based retailer, is one of the largest retailers in the U.S., operating 1,948 stores at the end of fiscal 2022 (ended Jan. 28, 2023). Target sells a wide variety of merchandise, with a slight emphasis on Beauty and Household Essentials Products (28% of sales in fiscal 2022). Other categories include Food & Beverage (21%), Home Furnishings & Décor (18%), Hardlines (17%), and Apparel & Accessories (16%). The company is known for its "one-stop-shop" experience, and its procurement teams are keenly aware of current and near-term consumer expectations, which can be considered an important part of the "secret sauce" for the company's success in recent years. It's worth remembering that Target's annual sales growth over the past five years has been 8.4% on a compounded basis - not a bad figure for a company that currently generates well over $100 billion in annual sales.

Those interested in a deeper look at Target's business should read my first article from May 2022, in which I compared the company to retail giant Walmart. In a follow-up article, I focused on the company's inventory seasonality, margins and cash management. I last covered Target stock not too long ago and evaluated whether it was a safe dividend stock in the current climate.

Wisconsin-based Kohl's is 60% the size of Target in terms of the number of stores it operates, but only one-third the size in terms of retail space (245 million versus 82 million square feet). Accordingly, Kohl's stores are, on average, just over half the size of Target's stores. This puts Kohl's at a disadvantage, as it cannot compete with Target from a shopping experience perspective. However, this is not the company's intent, as it focuses on "moderately-priced private and national brand apparel, footwear, accessories, beauty, and home products" (p.3, KSS fiscal 2022 10-K ).

Private label brands accounted for 36% of the company's sales in fiscal 2022 (also ending Jan. 28, 2023). Over the past five years, Kohl's has performed rather poorly, with sales declining 2% per year on a compounded basis. To be fair, fiscal 2017 was 53 weeks, but the performance is still nothing to get excited about, especially factoring in inflation. One big problem I see with Kohl's is the declining popularity of its private brands. In fiscal 2017, the company's private brands generated nearly $8 billion in sales, but by fiscal 2022, the corresponding figure was just $6.2 billion. National brands remained stable at $11 billion.

Another problem is that Kohl's hasn't significantly reduced its store presence since at least 2017, so the decline in net sales is almost entirely due to churn. All else being equal, I like to see struggling retailers adjust their store presence to stabilize their margins (more on that later). Kohl's, in theory, should have a good incentive to downsize because it leases a large portion of its stores. While Target owns nearly 80% of its stores, Kohl's leases 44% of its stores, while 21% of its stores are built on leased land (Figure 1). However, without knowing which of its stores are underperforming (or whether this is even a local phenomenon), it would be unfair to conclude that Kohl's management is simply inactive in this regard. Similarly, it should not be forgotten that the weighted-average remaining lease term at Kohl's is currently about 20 years.

Figure 1: Target Corporation (TGT) vs. Kohl's Corporation (KSS): Fiscal 2022 year-end store ownership (own work, based on data from company filings)

More importantly, a 44% ownership rate is still significant and most likely the reason for the takeover interest in early 2022 - recall the news of a $9 billion bid from a consortium backed by Starboard Value and an $8.6 billion offer from Simon Property Group, Inc. ( SPG ) and Brookfield Asset Management Ltd. ( BAM ). By comparison, the slightly larger $15 billion Nordstrom Inc. ( JWN ) owns just 7% of its 358 stores. Macy's Inc. ( M ) owns a similar percentage as Kohl's (41%, 783 stores), so it is understandably considered a takeover candidate as well. However, I think it is important to remain cautious with takeover fantasies - locations need to be critically scrutinized, and the current environment - also due to comparatively high interest rates - is far from optimal.

TGT Vs. KSS Growth Prospects –What Do Analysts Say About These Stocks?

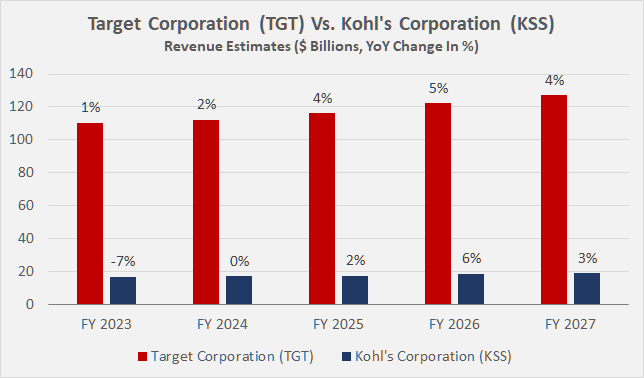

According to analyst estimates found on the Target and Kohl's stock page on Seeking Alpha, the two companies are expected to grow sales on average by 3% and 1%, respectively, over the next five years (Figure 2).

{kind=link}

Figure 2: Target Corporation (TGT) vs. Kohl's Corporation (KSS): Revenue estimates (own work, based on data from Seeking Alpha and company filings)

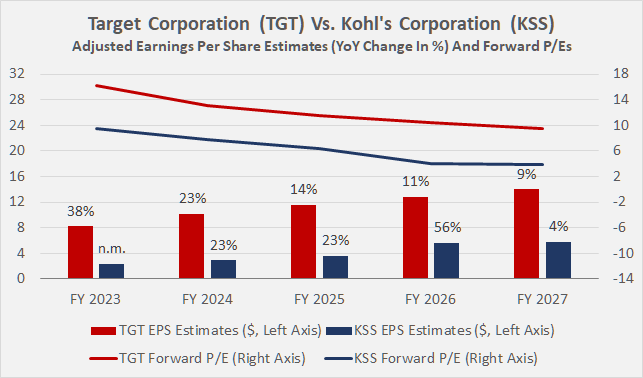

Adjusted earnings per share (( EPS )) growth estimates are much higher, but should not be over-interpreted (Figure 3). Primarily due to significant inventory issues and associated markdowns, both companies reported rather poor results for fiscal 2022. Understandably, analysts expect Target to recover much faster than Kohl's, which continues to be plagued by deeper problems (sales decline, margin issues - see below). This is also reflected in the valuation of the two stocks. Based on estimates for fiscal 2023, forward price-to-earnings (P/E) multiples for TGT and KSS shares are 16 and 9.5, respectively.

{kind=link}

Figure 3: Target Corporation (TGT) vs. Kohl's Corporation (KSS): Earnings per share estimates and forward P/E ratios (own work, based on data from Seeking Alpha and company filings)

Analysts expect Target to remain competitive and continue to grow at least in line with inflation despite short-term challenges (boycotts due to Pride Month related offerings). As I discussed in my last article, I do not believe recent events will have a lasting impact on Target's fundamentals.

Kohl's operating future is highly uncertain and depends on the performance of recently appointed CEO Tom Kingsbury, who succeeds Michelle Gass, who has overseen the opening of some 600 Sephora shop-in-shop units over the past two years (French multinational personal care and beauty products retailer). Kingsbury is not entirely new to the company, having been named interim CEO in December 2022 and a member of the board since 2021 as a result of a settlement between Kohl's and activist investor Macellum. The fact that Kingsbury came on board as a result of pressure from Macellum is a positive, in my opinion, as is his more than 10-year highly successful tenure as CEO of Burlington Stores ( BURL ). Between September 2013 and Kingsbury's departure, BURL stock returned over 40% annually, on a compounded basis.

As an aside, Kingsbury bought a significant amount of the company's stock shortly after becoming permanent CEO - at least in absolute terms. I am generally very cautious about insider transactions, as in most cases they are non-events or, at worst, window dressing. In my opinion, the $2.0 million transaction doesn't smell like window dressing, but I wouldn't overinterpret it given the CEO's current compensation of nearly $5 million annually. No other insiders have bought KSS stock recently, with three directors buying shares for $100,000 to $750,000 in the last three years. I would like to see more insider purchases that represent a significant percentage of annual compensation (similar to CEO Kingsbury's transaction) before I consider them a valid bull argument.

How Do Target's Financials Compare To Kohl's?

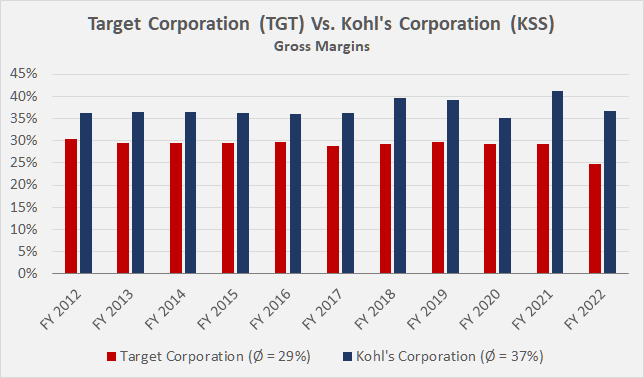

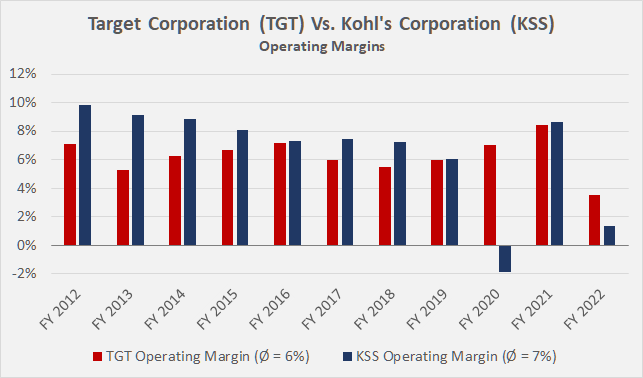

At first glance, Kohl's looks much more profitable - its average gross margin has been 817 basis points higher than Target's over the past decade (Figure 4). Of course, given the difference in merchandise assortment, this is not really surprising. More importantly, Target's operations are comparatively leaner, resulting in broadly similar operating margins over the past decade (Figure 5). This is also true for free cash flow margins. Using average free cash flow from 2020 to 2022, Target's margin is even 50 basis points higher than Kohl's (4.4% vs. 3.9%).

A closer look reveals that Target has maintained and even improved its profitability over the past decade, while Kohl's has significant issues. Granted, fiscal 2022 is probably not the best year for comparison, but it shows the disastrous impact of the inventory overhang at Kohl's. At the same time, I wouldn't over-interpret the seemingly strong performance of both retailers in fiscal 2021, which I believe is largely due to pent-up demand as a result of the lockdown measures.

{kind=link}

Figure 4: Target Corporation (TGT) vs. Kohl's Corporation (KSS): Gross margins (own work, based on data from Morningstar)

{kind=link}

Figure 5: Target Corporation (TGT) vs. Kohl's Corporation (KSS): Operating margins (own work, based on data from Morningstar)

While Target has significantly improved the efficiency of its asset base (as evidenced by an increase in asset turnover of over 30% over the past decade), Kohl's asset turnover has declined by over 10% over the same period and is also considerably worse than Target's in absolute terms (1.2x versus 2.0x). Competition in retail (online and brick-and-mortar) is fierce, and those companies that do not offer a strong value proposition or other valuable experience are falling behind. Target has really improved its direct-to-consumer ((DTC)) business in recent years and benefits from its scale. And while a comparison isn't really fair due to the significant size difference, I firmly believe that we live in a "winner-take-all" economy where footprint matters.

By now, it's pretty obvious that Kohl's is a turnaround investment, while Target - despite short-term challenges and uncertainties - is a blue-chip value investment with a solid track record.

Let's look at the free cash flow of the two companies (Figure 6). Although Target's CAGR of 17% (fiscal 2012 to fiscal 2021) looks spectacular, I consider both fiscal 2021 and fiscal 2022 anomalies. Baseline free cash flow is likely to be $4.5 billion or less, in part due to likely continued pressure from both suppliers and customers. As middle-man's businesses, both Target and Kohl's will have to absorb some of the inflationary pressures, but I am confident that Target is better positioned to keep the impact manageable.

{kind=link}

Figure 6: Target Corporation (TGT) vs. Kohl's Corporation (KSS): Free cash flow, normalized with respect to working capital movements and adjusted for stock-based compensation (own work, based on data from company filings)

Looking at the fiscal year-end 2022 balance sheets of the two companies, it is hardly surprising that Kohl's has relatively more operating and finance lease obligations (recall Figure 1). When net debt is conservatively calculated by including discounted operating and finance lease obligations and relating the results to each company's three-year average free cash flow, Kohl's leverage is extremely high (10.7x versus 3.7x). Leaving aside lease obligations, TGT and KSS are similarly leveraged (2.6x and 2.7x, respectively). As an aside, and in case you're wondering why I'm relating leverage to free cash flow, I shared my reasoning of the pros and cons of various leverage metrics in this article .

In a direct comparison, Target is obviously in a much better position. Of course, Kohl's could also benefit from sale-and-leaseback transactions, but I concede that the current environment for asset sales is far from ideal. Target's comfortable position is also reflected in its very manageable debt maturity profile (Figure 7) and conservative interest coverage ratio (10.4 x three-year average free cash flow before interest). Kohl's interest coverage ratio is extremely low, at only around 3.3 times three-year average pre-interest free cash flow, but this is due not only to the comparatively high weighted-average interest rate, currently above 5%, but also to the pronounced finance lease expense ($140 million in fiscal 2022, up 26% year-over-year).

{kind=link}

Figure 7: Target Corporation (TGT): Upcoming debt maturities, compared to 5x fiscal 2020 to fiscal 2022 average normalized free cash flow after dividends. (own work, based on data from company filings)

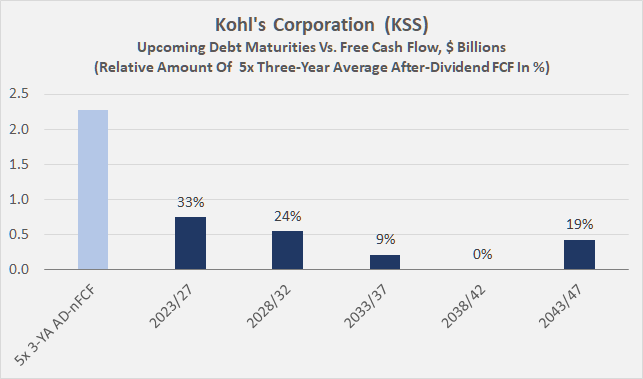

If interest rates remain "higher for longer", Kohl's could face increasing interest expense due to potential refinancing transactions (Figure 7) and the fact that bonds maturing through 2025 have relatively low coupons of 3.25% to 4.75% (with the exception of the 9.5% 2025 bond, fair value $113 million). It should also be noted that several rating downgrades resulted in an increase in the coupon rates of certain bonds (p. 49, KSS 2022 10-K). Moody's first downgraded Kohl's long-term credit rating to junk (Ba1) in December 2022, and more recently to Ba2 . The outlook for the rating remains negative. Equally concerning, Kohl's five-year credit default swap (CDS) reached a new all-time high of over 800 basis points in May 2023.

{kind=link}

Figure 8: Kohl's Corporation (KSS): Upcoming debt maturities, compared to 5x fiscal 2020 to fiscal 2022 average normalized free cash flow after dividends (own work, based on data from company filings)

TGT - despite recent events - is much less of a drama stock also from a balance sheet perspective, as evidenced by its credit rating of currently A2 (six notches higher than KSS) and reassuring debt maturity profile (Figure 8, see above). However, Moody's did change the outlook on Target's long-term rating from positive to stable, citing " considerable macroeconomic uncertainty and consumer stress that could prove difficult to navigate ." This is a very fair assessment in my view, as an upgrade of an already highly-rated retailer in the current environment would be questionable at best. Target's five-year CDS currently stands at about 50 basis points. It did rise when interest rates began to rise in early 2022, but has since declined somewhat. The fact that Target's CDS did not rise above 50 basis points during the COVID-19 pandemic underscores the company's solid footing, in my view.

Target Vs. Kohl's Dividend

At nearly 9%, Kohl's' payout to shareholders is much more enticing on the surface, but the high yield simultaneously screams value trap. Target's dividend yield is much more modest, currently at 3.3%, but that's to be expected given the company's much stronger position and only minor challenges. Both TGT's and KSS's dividend yields are currently well above their respective five-year averages of 2.2% and 5.1% .

Kohl's financials are much more volatile, highlighted by the need to suspend the dividend in fiscal 2021. However, management reinstated the dividend a year later, albeit at a much lower level. Two years after the dividend suspension, KSS doubled the payout , but it is still nearly 30% below pre-pandemic levels.

Even though the payout ratio at both Kohl's and Target is quite low (34% and 40% of three-year average free cash flow, respectively), I wouldn't overstate the dividend safety at the smaller company. While Target's dividend looks very safe to me, and the five-year average growth rate of 9.8% is solid indeed, I think the dividend safety of Kohl's stock is questionable, mainly due to its much weaker debt servicing ability, more volatile free cash flow, less recession-resistant merchandise assortment, and poor credit rating. Also, management could change its capital allocation priorities without notice and potentially use all of its excess free cash flow for share repurchases. This would make sense from a valuation perspective (forward P/E of less than 10), but not from a balance sheet perspective, even if short-term maturities are not a problem (see above, Figure 8).

Key Risks To Consider Before Investing In Either TGT or KSS

Despite its iconic brand, I have difficulty seeing an economic moat in Target. The company lacks the scale of larger competitors, has a very high number of stock keeping units (SKUs), and does not have the same omnichannel capabilities as Walmart, for example. However, and I do not want to be misunderstood, I consider Target's track record solid and value proposition is definitely strong. As a much smaller company with a focus on more problematic merchandise (e.g., apparel and footwear - highly dynamic, risk of markdowns), Kohl's is much more weakly positioned and lacks any tangible economic moat. Therefore, fierce retail competition - switching costs are virtually zero - is the single most important risk, although I believe this is much more relevant to Kohl's than Target.

Other risks (which are fairly obvious at this point) include potentially persistent inflation, deteriorating consumer sentiment (Kohl's in particular sells mostly discretionary items), and a difficult labor market. As mentioned in my previous article, I would not overstate the recent boycotts at Target. At the same time, it is worth noting that the company is likely well integrated at the local level, as it continues (since 1946) to give five percent of its profits to communities.

The retail environment will most likely continue to move toward alternative fulfillment methods, putting the major players at an advantage. At the same time, the number of brick-and-mortar stores will decline. Due to the comparatively high proportion of leased stores with relatively long average lease terms, Kohl's cannot respond dynamically and will be very slow to adjust its footprint. On a positive note, however, only 63 or 5.4% of all Kohl's stores are located in malls.

Another aspect of particular concern for Kohl's is the poor performance of its private label brands. The growing reliance on (popular) third-party brands increases the risk of obsolescence as many apparel and footwear companies (e.g., Nike ( NKE ), adidas, ( OTCQX:ADDYY / ADDDF ) or V.F. Corporation ( VFC )) are increasingly moving towards DTC to cut out the middleman.

Conclusion – Target Vs. Kohl's, Which Stock Is A Good Investment?

Primarily due to the secondary effects of government-mandated lockdown measures to contain the spread of SARS-CoV-2 in 2020 and beyond, retailers are experiencing a challenging environment. S upply chain disruptions, rampant inflation, a tight labor market, trade disputes with China and rising theft, along with rapidly increasing interest rates, are the main factors that have sent retail stocks tumbling.

Kohl's and Target are two potential value stocks that each have their own issues. Upon closer inspection, Target's challenges appear short-term and very manageable. The company has successfully navigated several recessions, and its diversified assortment has enabled it to weather the pandemic well. While I don't think Target or Kohl's have a tangible economic moat, I think it's important to keep in mind the qualities of Target's procurement teams and strong value proposition. And while Kohl's is better off from a gross margin perspective on the surface, its focus on apparel and footwear makes it more susceptible to inventory issues and related markdowns. The company's performance in fiscal 2022 illustrated this point very well. That being said, the poor performance of the company's private label brands since at least 2017 is also quite concerning.

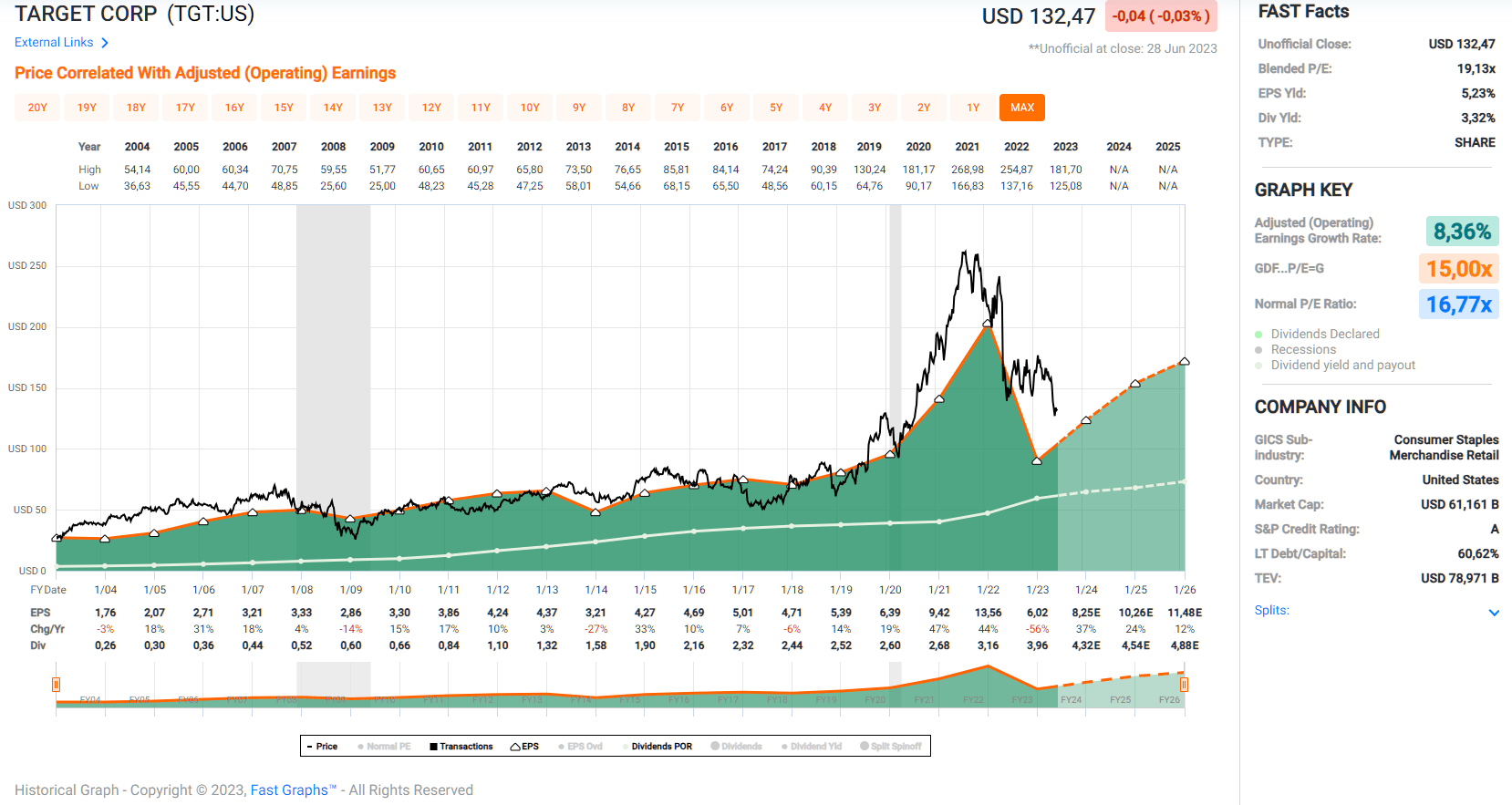

Of course, Target's earnings have also declined precipitously due to markdowns, but free cash flow should return to pre-pandemic levels by the end of fiscal 2024. And even though the company lost cash on a reportable basis in fiscal 2022, I think the dividend is very safe. Unlike Kohl's, whose debt service capacity is very poor due to comparatively pronounced finance lease obligations and a high weighted average interest rate on its debt, Target's balance sheet looks very robust to me. In my view, the company can easily maintain its dividend even in what is likely to be the most anticipated recession in modern history. However, with a forward price-to-earnings ratio of 16 (Figure 9), I still think the stock is too expensive for a retailer that is in a worse position than giant Walmart (which I think is grossly overvalued).

{kind=link}

Figure 9: Target Corporation (TGT): FAST Graphs chart, based on adjusted operating earnings per share (FAST Graphs tool)

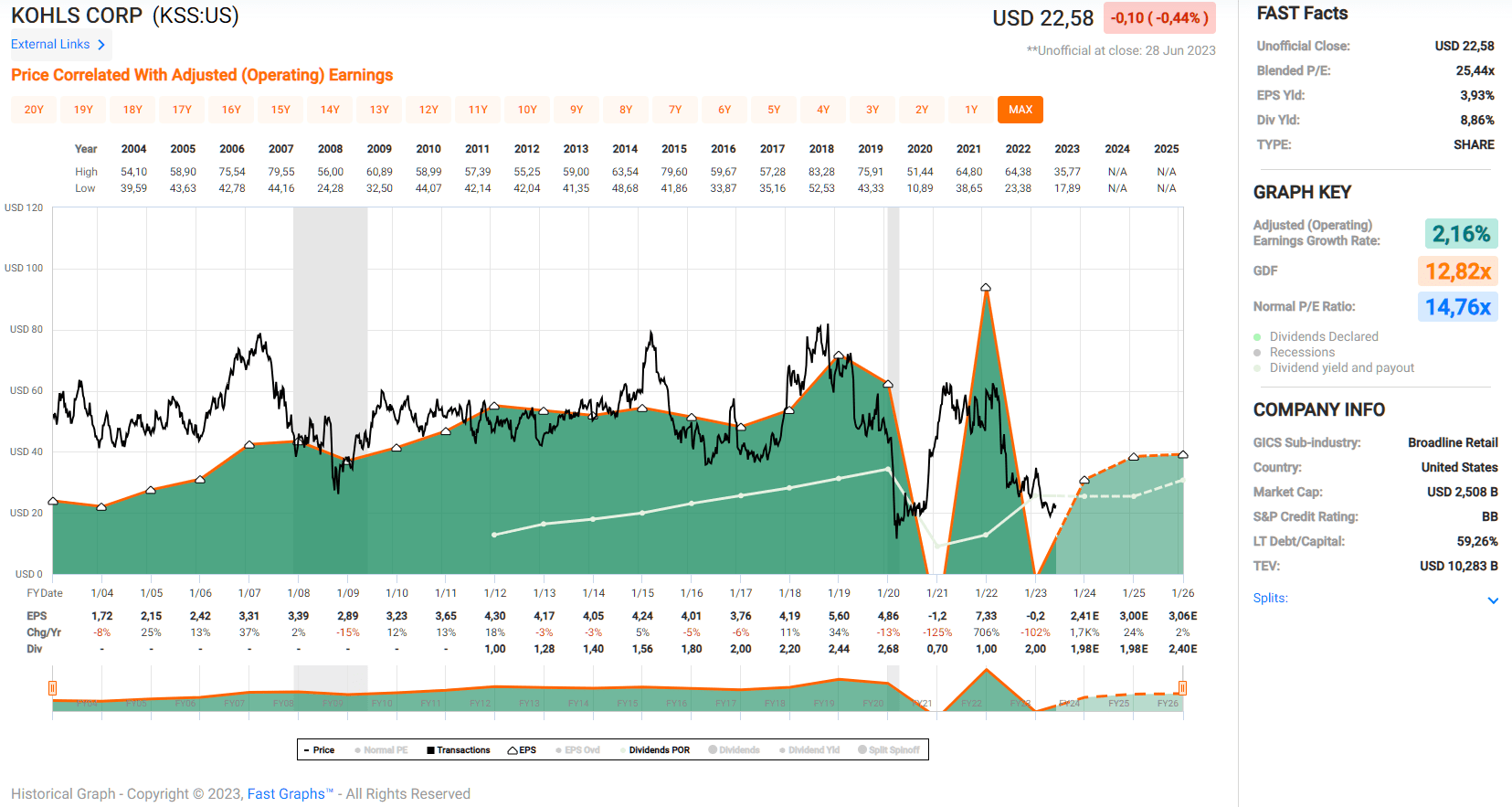

And while I wouldn't count on Kohl's nearly 9% dividend yield due to its poor debt service ability and surprisingly high CDS premium (800 basis points!), it's also the activist involvement that would give me pause as a dividend investor. Capital allocation priorities can change quickly, and given the fairly cheap valuation (Figure 10), I can imagine the dividend being eliminated in favor of opportunistic share buybacks. Leaving the dividend aside, Kohl's qualifies as a high-risk, high-reward turnaround play.

{kind=link}

Figure 10: Kohl's Corporation (KSS): FAST Graphs chart, based on adjusted operating earnings per share (FAST Graphs tool)

The track record of Kohl's' new CEO is solid, and the board appears to be adequately staffed. However, I would encourage you to critically examine whether Burlington Stores is a true blueprint for Kohl's turnaround. The first quarter results give reason for cautious optimism (good gross margin improvement and SG&A expense control). However, despite the fact that the new CEO recently bought $2 million worth of KSS stock, I would be wary of blindly following him into the stock. After all, the stake represents less than 50% of Kingsbury's annual compensation, and much work remains to be done to convince consumers of Kohl's value proposition and turn around the struggling retailer.

All in all, I don't think either TGT or KSS is currently a good investment. As a long-term investor, I am most interested in companies that have a wide economic moat, a hard-to-copy business model, and strong pricing power. Retail companies do not fit that bill in most cases.

However, if Target were to fall to a level of $100 or less (a forward P/E of 12, 4.4% dividend yield), I could see myself opening a small position, as I believe the company's value proposition is solid and I appreciate its long and solid track record. Kohl's caught my attention due to the high dividend yield and activist involvement, but on closer inspection, it is a turnaround investment with significant uncertainty, happening at a rather unfortunate time (high inflation, expected recession, junk rated debt with still negative outlook). If the economic outlook were better, I think Kohl's could represent a solid opportunity. Even though the stock trades at less than 10 times projected fiscal 2023 earnings and has room for further margin expansion, it still doesn't qualify for a position in my speculative ancillary portfolio. That being said, the stock has the potential for a short squeeze with a current short interest of about 22%. However, as the example of GameStop Corp. ( GME ) has shown, I would not hold my breath for such an event, and it is generally a poor basis on which to build an investment thesis. GME stock languished throughout the pandemic, and it took a significant and concerted effort to trigger the (arguably epic) short squeeze in early 2021.

As always, please consider this article only as a first step in your own due diligence. Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well.

For further details see:

Target Vs. Kohl's: How To Compare These Stocks, And Choose The Best Investment