TARO - Taro Pharmaceutical: Sun Pharma Deal Uncertain No Discernible Value Beyond NAV (Rating Downgrade)

2023-08-16 06:25:15 ET

Summary

- Taro Pharmaceutical's minority shareholders have resisted Sun Pharmaceuticals' offer of $38 per share, stating that Taro is worth more.

- Taro's operating economics are unattractive in my view, with declining pre-tax earnings and no revenue growth.

- Uncertainty remains on the Sun Pharma bid, placing uncertainty on price visibility.

- Revise to hold.

Investment summary

Since my June publication, the equity stock of TARO Pharmaceutical Industries Ltd. (TARO) has failed to catch a bid and trades in-line with the offer made by Sun Pharmaceuticals Ltd ("Sun") of $38 per share. Critically, Taro's minority shareholders [Sun already owns ~85% of Taro] appear displeased with the 'lowball' offer-chiefly, large shareholder Krensavage Asset Management. The firm refuted Sun's offer and said that it " can pay more" in an issued statement from July.

In the last publication, I opined the Sun offer could be a potential catalyst to see Taro rally and also see Sun forced to up its bid beyond $38. It appears Taro and its shareholders are aligned with this view. In the absence of the deal going through, however, findings in this report illustrate a set of unattractive operating economics that make future shareholder value uncertain in my view. Here I'll discuss all of the recent developments, and revise my rating to hold. I'm not in the business of event-driven gains around mergers/buyouts, despite the potentially lucrative upsides on offer in this active strategy. I am after long-term cash compounders, adding clear shareholder value, with durable economic characteristics, and long-term competitive advantage. I'm not eyeing this here. Revise to hold.

Figure 1. TARO consolidation from $38 Sun Pharma bid

{kind=link}

Recent developments

1. Sun Pharma offer

As a reminder, Sun offered to acquire all the shares it doesn't already own in Taro on May 26th on a $ 38/share all-cash offer, valuing the company at $1.4Bn at the time. These two have a long history, and Sun has made offers to buy Taro in the past. It offered $24.50/share to purchase the company back in 2011, before upping the bid to $39.50. Hence, the latest offer is at a discount to what's been put on the table previously.

Acquiring firms often put up what's called a "control premium" to purchase the assets they are buying in public markets. This is often done simply to secure the bid. Other times, it boils down to the earnings power and asset factors, including intangibles not measurable on the balance sheet. The cost of money/discount rate on valuations is also a factor here too.

Sun is clearly not offering any control premium in its latest bid. As Krensavage mentioned, Taro has a potential liquidation value of $46 in net asset value/share (adjusted for goodwill = $46.51/share; $36/share less cash). Taro, therefore, currently trades at a small premium to its NAV/share, excluding cash. Thus, the opportunity cost presents itself-if Taro simply seeks liquidation, and sells its net assets, shareholders could potentially receive $46/share, more than $8.20/share higher than Sun's offer.

This equates to a market value of $1.43Bn, roughly in-line where Taro trades as I write. Adjusted for the 8.1mm shares it doesn't own, and excluding cash, Sun's offer comes to ~$16mm.

Krensavage was more direct in its assessment of " Sun's tactics ":

"Taro boasts more than just cash and real estate. The maker of generic creams and ointments generated $2.4 billion of cash in the 10 years ended March 31...[Sun] seemingly ignores Taro's 22 generic drugs awaiting clearance in the U.S., including four with tentative approvals."

It also said it would refuse to support the transaction unless these value points were considered. In other words, unless a higher bid was made.

The critical facts from here are now twofold-is Taro actually worth $46/share, and, if the sale doesn't go through, what does Taro offer going forward?

Figure 2.

Sources: BIG Insights, Company reports

Figure 3.

Sources: BIG Insights, Company reports

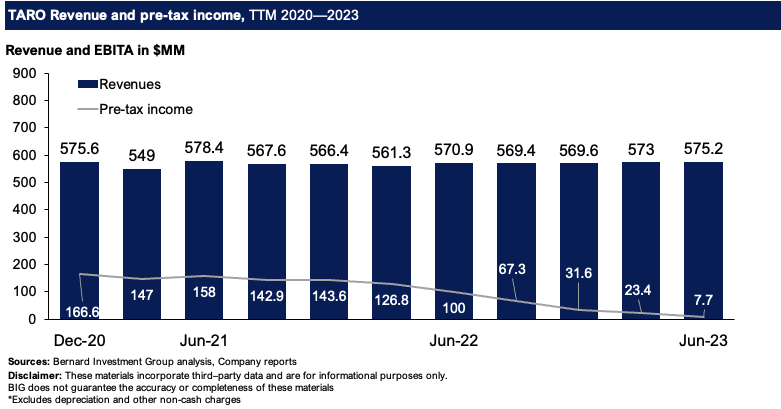

2. Softening economic characteristics

The company's Q1 FY'23 numbers were soft vs. historical averages, continuing the trend observed since Q1 2022. It booked 140bps YoY sales growth to $159mm, on gross of 40.3%, down ~12 percentage points YoY. Critically, Taro's pre-tax earnings have been dwindling for the last 2 years on my inspection. They have snipped from $167mm in 2020 to just $7.7mm last quarter, using TTM values. Meanwhile, there's been no revenue growth over this time.

Figure 4.

{kind=link}

Where has the profitability gone? There are several possible explanations for this.

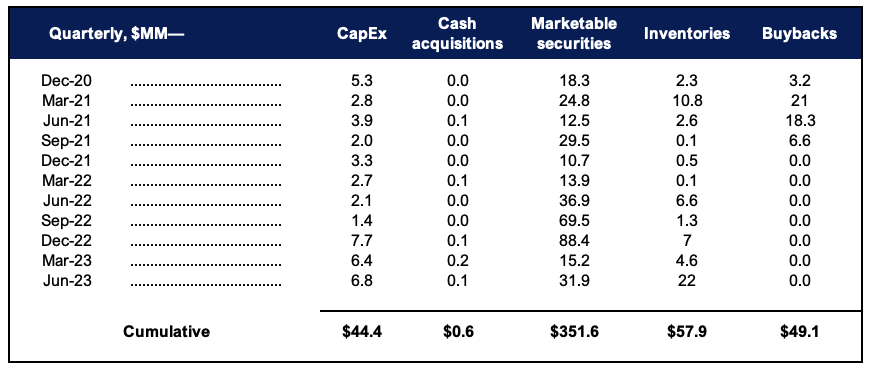

One, looking at uses of cash per quarter since 2020, the bulk of investment has been recycled back into purchasing marketable securities. More than $351mm is now tied up in short-term investments of this nature. Comparatively, just $44mm was cumulated toward CapEx. It did repurchase ~$50mm of its own stock, but this finished in 2021. Of the $503mm in total cash deployed, c.$58mm was rotated into new inventories. This tells me TARO has a lack of profitable opportunities to deploy cash back into growing the business. Instead, it sees cash and the money markets at 4-5% as more attractive.

Figure 5. Taro uses of cash

{kind=link}

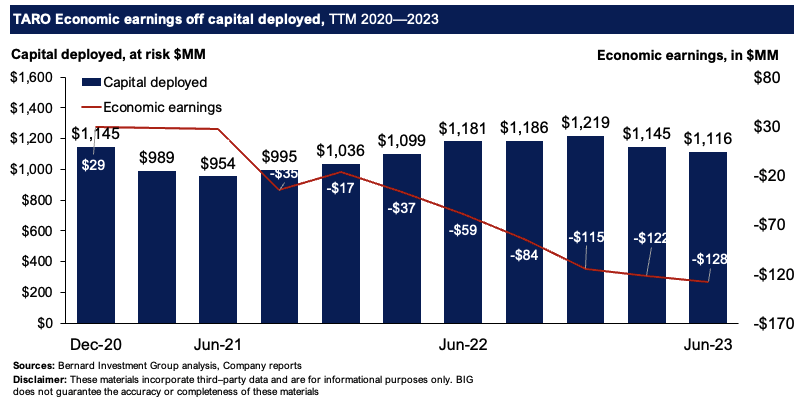

Two, as of Q2 FY'23, the firm produced just ~$6mm in earnings after tax off $1.12Bn in capital deployed into fixed and intangible assets (TTM values). That equates to $0.15/share produced off $29/share in capital. This is unacceptable as a form of value creation. The resulting economic losses are thus $128mm and have slipped from economic profitability of ~$28mm in 2020.

Three, as it relates to earnings power, if $1.12Bn gets me just $6mm in earnings, it's difficult to see Taro valued past its net asset value of $46/share. Those net assets, excluding non-operating capital, get you just 0.5% return on the capital put at risk. This would explain why TARO is rotating so much surplus capital into marketable securities vs. into its operations.

Figure 6.

{kind=link}

Market generated data

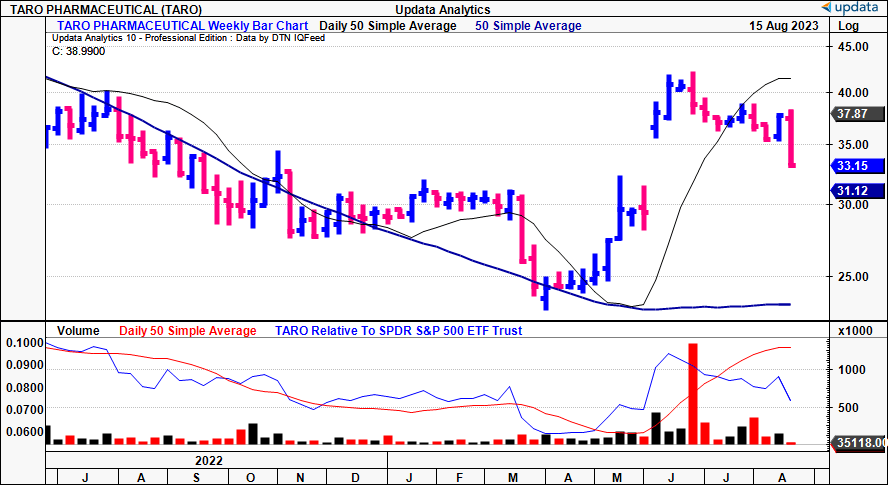

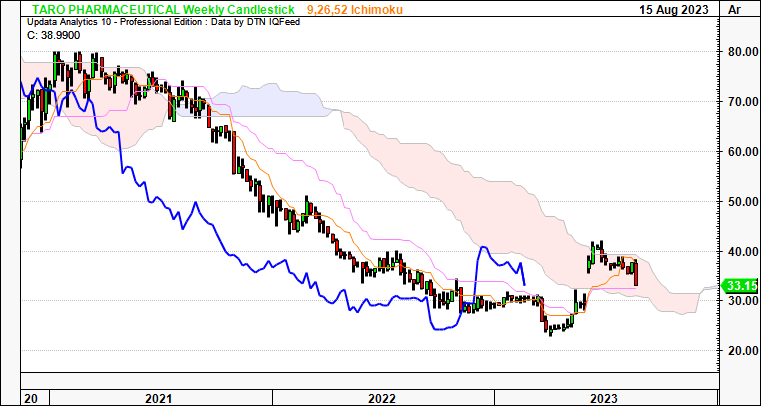

Upward bias on TARO's equity stock appears muted as well. In terms of trend analysis, the price line and lagging line, shown in the cloud chart below, are well within the neutral camp. The lagging line (in blue) is below the cloud, thus suggesting the trend could even turn bearish at a point in time. Whilst not as relevant as the fundamentals here, this clearly shows the neutral sentiment in the stock without any new catalysts.

Figure 7.

{kind=link}

Money outflows have been heavy this past month or so as well. You can see from July, when Krensavage posted its statement on the matter, the direction of equity flows-all outward [Figure 8]. This makes sense. In the absence of economic catalysts from the firm's operations, investors speculating on the buyout were likely to have been chasing the $38/share or higher bid. With uncertainties on the deal's direction, the opportunity cost of holding TARO is high (benchmarks have gained ~7% since March).

Figure 8.

Data: Updata

Investment verdict

The future of TARO's equity stock is not in the hands of the market in my view. A combination of minority and majority shareholders are set to decide its fate. Sun Pharma is being called to up its bid beyond $38/share. This could potentially create some value for the event-driven crowd, but that's not how we invest our client's capital nor the kind of investments we recommend as part of our strategy. Instead, I am always on the hunt for capital compounders, growing intrinsic value via their strong economic features.

In my view, TARO does not present with these features. Instead, you've got more than $1.1Bn in capital tied up in commitments to the business getting you ~$7mm in trailing earnings, simply unattractive. Indeed, stock prices reflect future expectations, and actual financials can change expectations-but where TARO sells today, tells me the market expects it to be bought at $38/share from Sun. Undoubtedly, the key upside risk is that Sun offers an obscene premium to its net asset value-I'm thinking like $50-$55/share here as a control premium. On the bounce of probabilities though? Unlikely.

In that vein, I am no longer bullish on the deal's potential and now think of the opportunity cost of holding TARO over more selective opportunities, especially now with cash at 4-5%, benchmarks trading higher, sector rotations out of healthcare, and hard assets like infrastructure for instance offering a premium to conventional equity strategies. Net-net, revise to hold.

For further details see:

Taro Pharmaceutical: Sun Pharma Deal Uncertain, No Discernible Value Beyond NAV (Rating Downgrade)