TATLY - Tata Steel: Risky Steel Play Ahead Of A Downcycle

2023-09-14 12:04:35 ET

Summary

- Tata Steel has benefited from robust industrial growth in India.

- But the global steel cycle is turning over, and the company won’t be spared.

- Given the challenging outlook, the stock seems too pricey here.

Tata Steel ( TATLY ), the separately listed steelmaking arm of India’s Tata Group, remains one of the lowest-cost steel producers globally, with an outsized revenue contribution (>50%) from the value-added side. The company’s crown jewel is its Tata Steel India subsidiary, though it also has a sizeable (albeit less profitable) presence in the Netherlands (Tata Steel Europe) and the United Kingdom (Tata Steel UK).

While the stock has risen in line with the broader NIFTY index in recent months, Tata Steel, like all other steel businesses, remains levered to a global steel cycle that has shown signs of weakness recently. Outside of India, the UK and European P&L have been particularly affected by weaker global demand and, depending on government subsidies, could continue to weigh on overall profitability going forward.

In the meantime, balancing its capex (growth and maintenance) and balance sheet deleveraging targets will be a tricky challenge. Against management guidance for $1bn/year debt reduction (culminating in net debt/EBITDA of 2.0x-2.5x), I suspect a steel downcycle and falling profits pose downside risk to these targets. At 6-7x EBITDA for a cyclical exposed to a likely downturn, the stock isn’t particularly cheap either. Pending the resolution of government negotiations in the UK and tangible signs of a turnaround at the European operations, I would be cautious.

Riding the Indian Growth Wave but Still at the Mercy of the Cycle

Indian GDP growth has sustained this year in the high-single-digits, not only on the back of higher consumption but also from private sector investments and a step up in infrastructure capex from the government’s end (as highlighted in the Union budget). Alongside the robust foreign direct investment flows into India, a result of the country’s favorable geopolitical positioning, the domestic steel demand outlook isn't all that bad.

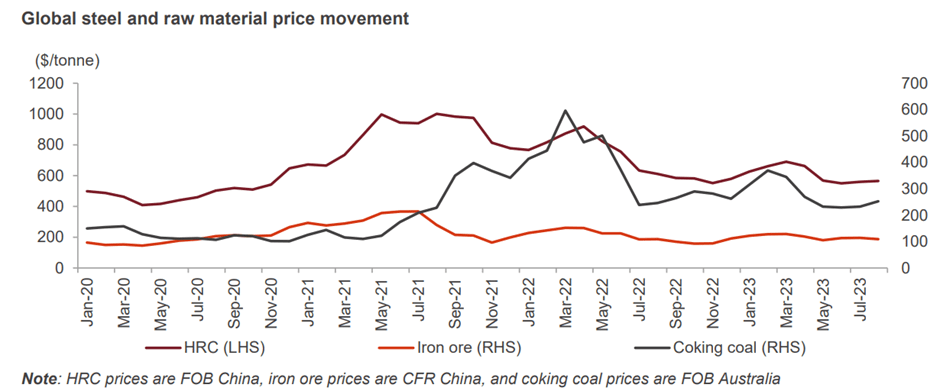

From a global perspective, though, steel prices remain levered to a slowing Chinese economy and will ultimately be decided by a combination of supply discipline and property sector stimulus. Thus far, Chinese demand weakness has kept a lid on steel prices; with manufacturing PMI data also still in contraction, I don’t see a turnaround anytime soon.

{kind=link}

CRISIL

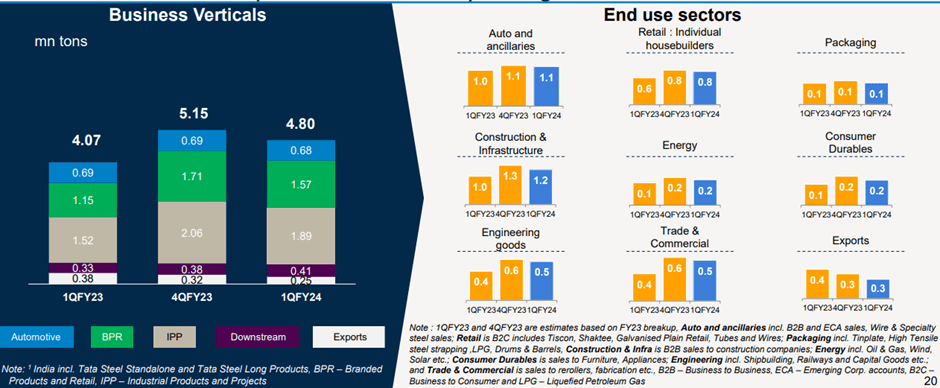

So even with Tata Steel’s Indian business still churning out strong volumes YoY ahead of a capacity increase over the next year or two (mainly from phase II expansion at its Kalinganagar plant), lower for longer steel prices should weigh on the top line. There are also input costs to consider (mainly coking coal), as these have already been driving EBITDA level declines. The guidance bar also remains high, and until management hits the reset button, I see more downside than upside to current expectations.

{kind=link}

Tata Steel

Fundamental Troubles in UK/Europe Remain

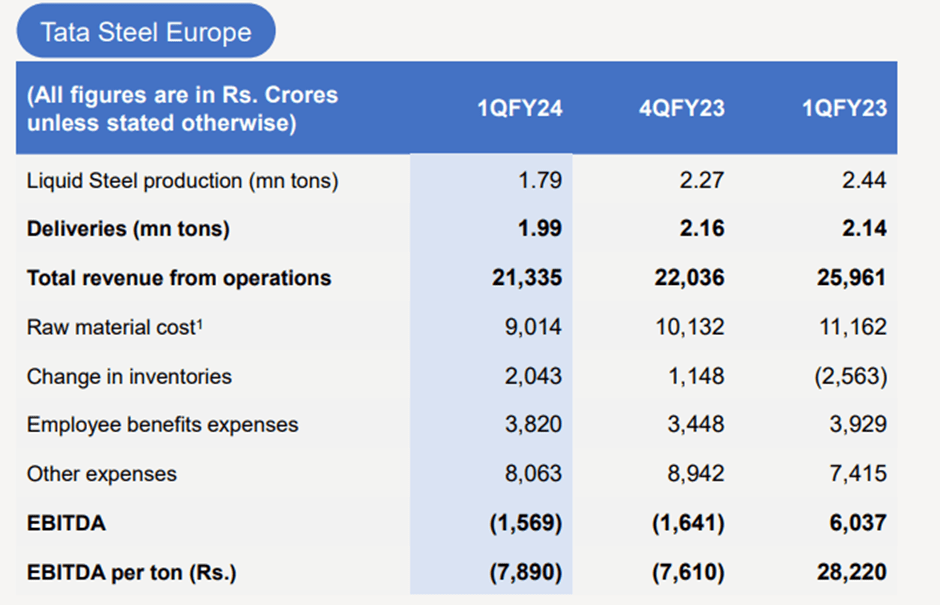

Throughout Tata Steel’s operating history, the UK/European businesses have been detractors of the overall business; recent results indicate this trend has only gotten worse. Of note, the European steelmaking operation saw lower production, deliveries, and wider EBITDA/t losses in fiscal Q1 despite locking in lower-than-expected coking coal prices, helped by supply tailwinds from Australia.

{kind=link}

Tata Steel

The silver lining here is that the company is currently in the midst of detailed discussions with an increasingly India-friendly UK Government for subsidies to the UK business (outcome likely next year). These will come with ‘green transition’ targets, though, so even if the P&L benefits, the transition to green technologies will also drain cash flows. In the Netherlands, Tata Steel is also navigating intense pressures to decarbonize, with its boiler furnace operations set to bump up against carbon taxes. Another key source of concern here is the increased electric arc furnace-based capacity coming onstream , helped by energy and scrap price tailwinds. While discussions with the Netherlands government could also yield some P&L cushion in the form of subsidies, I’m not prepared to underwrite a benign outcome just yet.

Walking the Deleveraging/Capex Tightrope

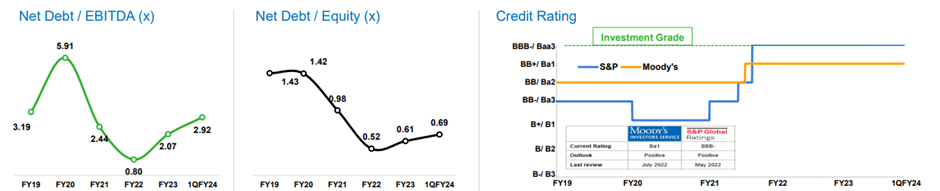

Tata Steel management has done a great job funneling the cash flows generated in the recent steel upcycle to clean up its balance sheet over the last few years. But sustaining its $1bn/year deleveraging target seems a tad ambitious as we enter a multi-year downcycle. Instead, there’s a good chance the company’s balance sheet will deteriorate as it balances a massive capex outlay with debt reduction and a weaker earnings trajectory.

{kind=link}

Tata Steel

For context, the company has earmarked capex of INR160bn this fiscal year (up from INR120bn in fiscal 2023), mostly in India (INR100bn capex), with the remainder allocated to Europe (upgrading blast furnaces and other machinery), as well as external M&A and R&D efforts. Even if the company hits its fiscal 2024 capex target, it may well be at the expense of the fiscal 2025/2026 outlay, posing downside to the long-term 30mt/year capacity target. Alongside Tata Steel’s capital-intensive decarbonization and sustainability efforts in Europe/UK, I suspect the company will opt to sacrifice some long-term earnings power by cutting back on spending over levering up the balance sheet.

Risky Steel Play Ahead of a Downcycle

As much as I like the outlook for Tata Steel’s Indian business, a key driver for its stock rally this year, the company remains exposed to a broader steel downcycle amid external challenges. More fundamentally, the UK and European operations have shown little sign of turning around, with EBITDA level losses widening in its latest quarter. Even if government subsidies help, there’s still a capital-intensive ‘green’ transition process to get through; without the profits of the last few years, it’s hard to see how the company funds its capex needs (note many of its UK/EU assets are also close to a new replacement cycle). With massive India-focused growth capex also in the pipeline, this leaves management with a difficult trade-off – further deleveraging the balance sheet or cut back on capex and, by extension, sacrifice future earnings power. Pending a meaningful reset, I would be cautious about the stock, particularly at a pricey 6-7x EV/EBITDA.

For further details see:

Tata Steel: Risky Steel Play Ahead Of A Downcycle