TMHC - Taylor Morrison: Don't Let Housing Market Doldrums Offset Cheap Shares

2023-04-10 10:37:36 ET

Summary

- The homebuilding market is really taking a hit from an order and backlog perspective.

- This is due to higher interest rates and the impact of inflation on home buying.

- Normally, investors might be advised to stay away, but Taylor Morrison Home Corporation shares are cheap enough to create a favorable risk to reward prospect at this time.

Times of crisis and uncertainty can be some of the best to buy shares in high-quality companies. This is because the market sometimes overreacts, pushing shares down unjustifiably low. And right now, with the possible exception of the banking industry, no space is likely being negatively affected by current economic conditions more than the home building market.

In recent years, one of the leaders in this space has been Taylor Morrison Home Corporation ( TMHC ). Strong demand for housing and low interest rates fueled a tremendous amount of expansion for the company. But now, we are seeing meaningful signs of weakening. Some investors may view this as the time to bail on their holdings. But unless you assume something similar to a doomsday scenario, I have a hard time seeing the stock as being any worse than fairly valued. Because of this, I do believe that the company offers a favorable risk-to-reward opportunity that justifies a bullish outlook for the foreseeable future.

The housing market is getting worse

When the Federal Reserve began hiking interest rates last year, most anybody who is well connected with the market knew then that the housing space would likely be one of the most negatively affected. Already, there were problems because inflationary pressures had pushed prices up materially. But then when you add on rising interest rates, it makes buying that much more costly and results in financial institutions becoming pickier with whom they lend their capital to.

{kind=link}

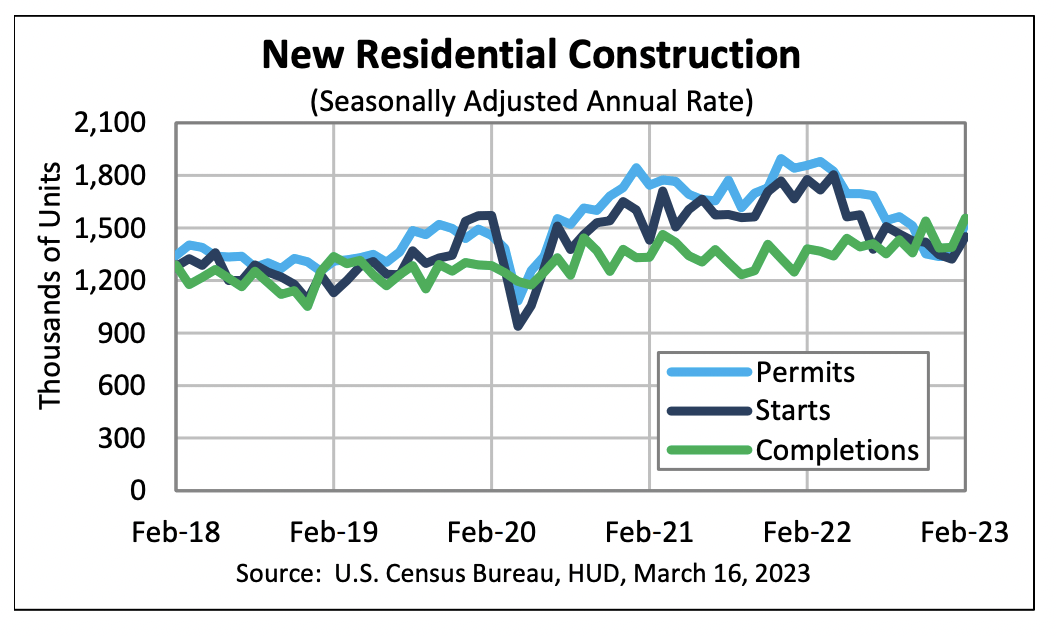

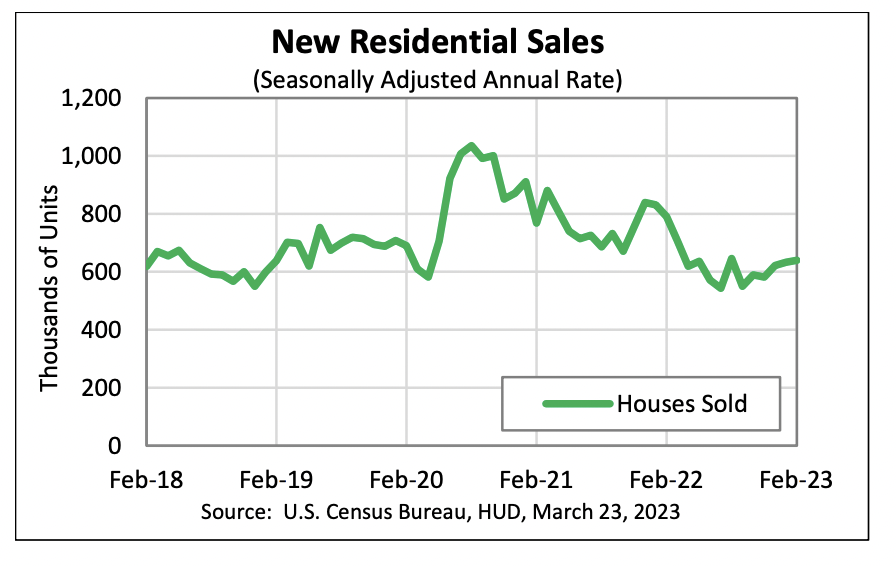

The most recent data involving the new residential construction space was published by the U.S. Census Bureau on March 16th of this year. For the month of February, the data showed only 1.45 million housing starts and 1.52 million building permits across the country. The housing starts data was actually 18.4% below the 1.78 million reported one year earlier. Meanwhile, the building permits data was down 17.9% from the 1.86 million seen in February of 2022. The Bureau came out with a subsequent report on March 23rd covering new residential sales. The number of houses sold for the month of February totaled 640,000. That was, perhaps unsurprisingly, a 19% decline from the 790,000 seen one year earlier. The median sales price was still up year over year, having risen 2.5%. But the overall average, as measured using the mean, was down 4.5%.

{kind=link}

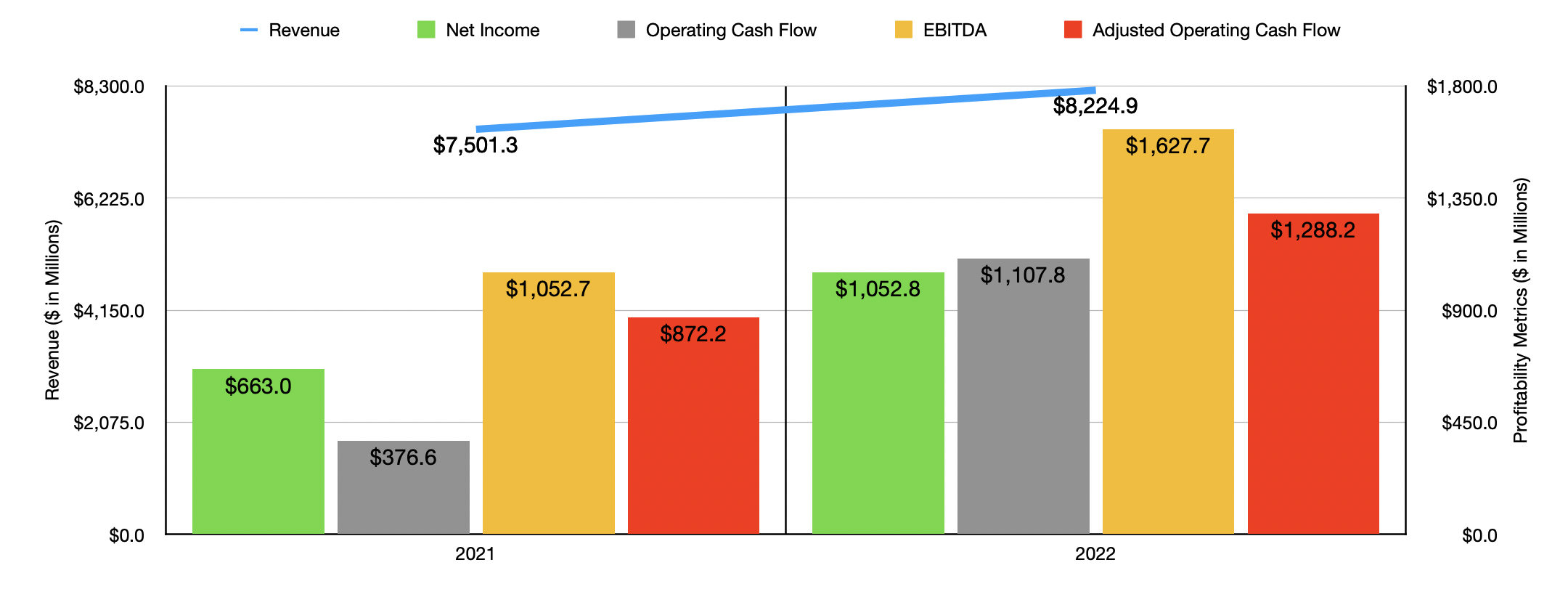

When looking at the data from Taylor Morrison, you might not see any of this pain right now. Consider how the company performed during its 2022 fiscal year. Sales during that time totaled $8.22 billion. That was up 9.6% over the $7.50 billion reported one year earlier. A 19.1% surge in the average sales price of the homes that the company delivered more than offset the 7.7% drop in the number of homes closed. As a result of this sales increase and the manner of the increase, profits for the company shot up from $663 million to $1.05 billion. Operating cash flow skyrocketed from $376.6 million to $1.11 billion. If we adjust for changes in working capital, the metric would have gone from $872.2 million to $1.29 billion. And finally, EBITDA managed to grow from $1.05 billion to $1.63 billion.

{kind=link}

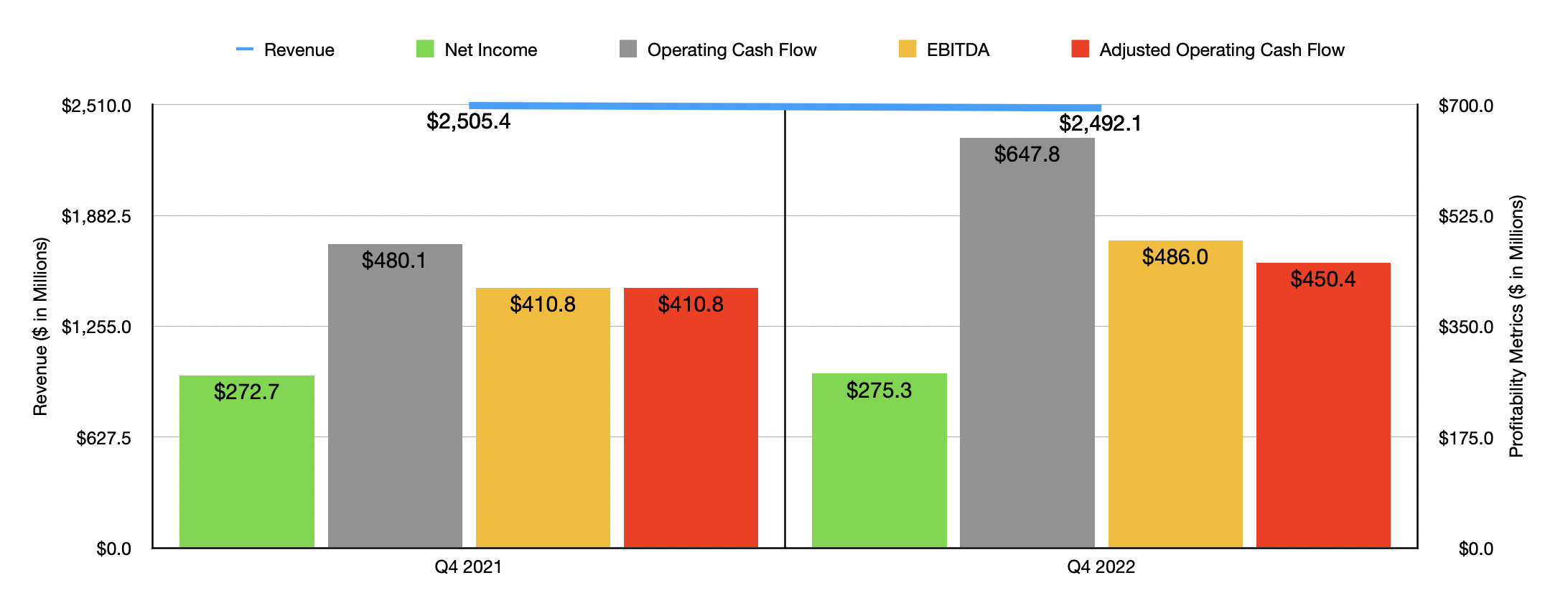

As you can see in the chart below, results were largely still positive year over year even in the final quarter. Although sales did decline during this time, profits still managed to inch up modestly. Operating cash flow, as well as the adjusted figure for this, managed to increase year over year, as did EBITDA. To anybody who really digging into these numbers, this may look like just a slowdown. But when you look at the picture deeper, you see significant pain building. Consider backlog. By the end of the 2022 fiscal year , backlog totaled only 5,954 homes. This represents a 34.7% decline from the 9,114 units the company had one year earlier. In fact, in order to see backlog figures lower than this, you would need to go back to 2019 when the reading came in at 4,711 units.

{kind=link}

A good portion of this decline was driven by a surge in the cancellation rate of orders. 24.4% of all orders in the fourth quarter were canceled compared to only 15.6% one quarter earlier and 8.2% in the final quarter of 2021. But a plunge in sales orders also affected the company. In the final quarter of the 2021 fiscal year, the company received net sales orders of 3,124 homes. In the final quarter of 2022, this number came in at only 1,810 homes, translating to a year-over-year decline of 42.1%.

When it comes to the 2023 fiscal year, management is forecasting home closings of between 10,000 and 11,000. That would mark a decent decline compared to the 12,647 that the company had for 2022. Given the long-term nature of building homes, this may be realistic. However, absent a significant improvement in the market, you can expect this number to drop even more, perhaps substantially so, in 2024.

In January of this year, I wrote a bullish article regarding Taylor Morrison. In that article, I talked about how strong the company's financial results, covering through the third quarter of its 2022 fiscal year since fourth quarter data was not yet available, had been. I did also acknowledge that the company was starting to show meaningful signs of weakening from an order and backlog perspective. Investors who were uncomfortable with volatility were advised to consider looking elsewhere for upside. But for those who don't mind it, I felt comfortable rating the company a ‘buy’ to reflect my view that shares should outperform the broader market for the foreseeable future. Since then, the company has done quite well, with shares generating upside for investors of 9.5%. That compares to the 2.6% increase seen by the S&P 500 over the same window of time.

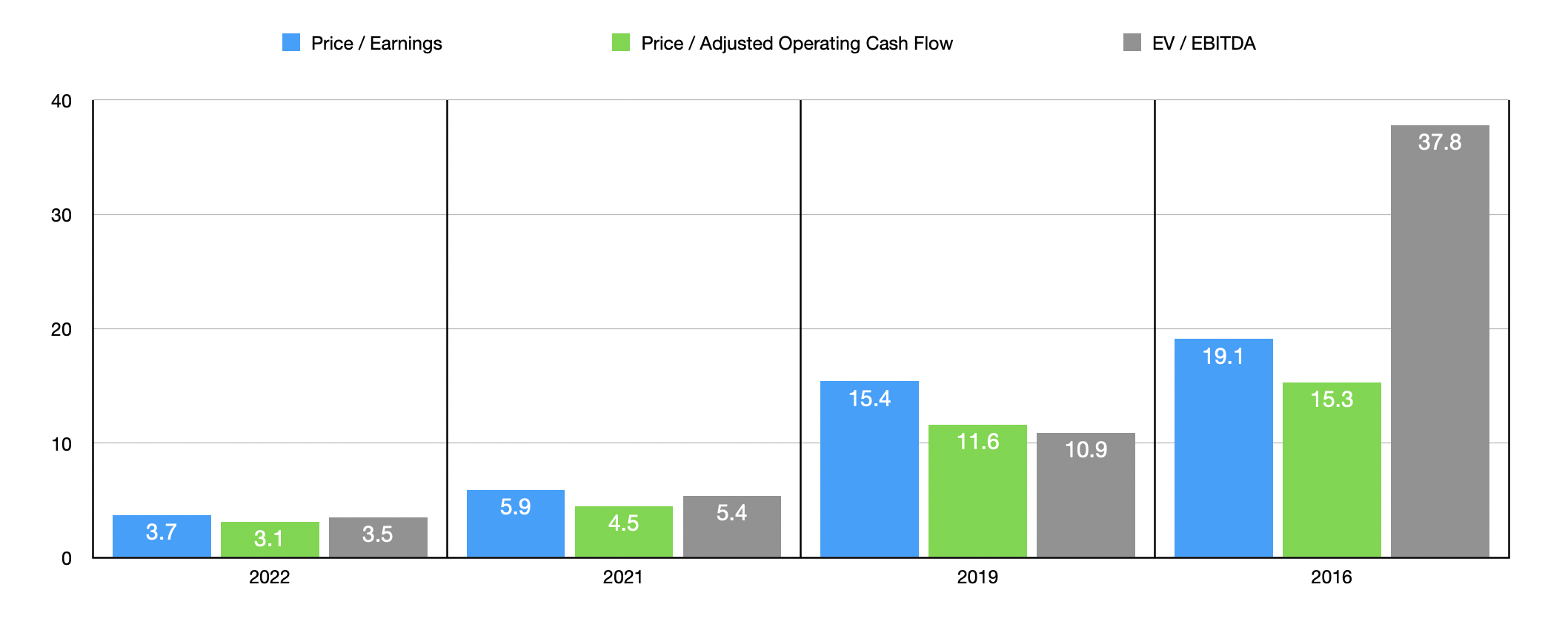

Why would I be bullish on the company showing significant and ever-growing signs of weakness? It boils down to just how cheap shares are. As you can see in the chart above, I valued the company using data from four different fiscal years. These were 2021 and 2022, as well as 2016 and 2019. The reason why I used data from 2016 was because, in that year, the company had backlog of only 3,131 homes. And I would find it difficult to imagine that backlog could fall the nearly 50% from where it is today back to those levels. So I saw this as a year in which we might experience some sort of doomsday scenario. 2019 was the last year before the pandemic struck and inflationary pressures pushed prices up. And 2021 and 2022 are just the most recent fiscal years available.

{kind=link}

Even if we do see some awful scenario where the company performs like it did in 2016, I can't imagine that it would last for much more than a year. After all, there does seem to still be a shortage of about 6.5 million homes in the U.S. So any weakness in the market can only last until market conditions encourage additional building. A more realistic downside scenario would be 2019, but I think that the stock would look more or less fairly valued at those levels. And anything better than that, would indicate significant upside. In the table below, I also compared the company to five similar firms, all using the most recent data available. As you can see, Taylor Morrison is one of the cheapest in the space, trading the lowest when it comes to the price to operating cash flow approach and with only one of the five firms cheaper than it using the other two methods.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Taylor Morrison Home Corporation |

| 3.7 |

| 3.1 |

| 3.5 |

| Legacy Housing Corporation ( LEGH ) |

| 7.9 |

| 44.3 |

| 5.9 |

| Meritage Homes ( MTH ) |

| 4.3 |

| 10.4 |

| 3.4 |

| Century Communities ( CCS ) |

| 3.8 |

| 6.3 |

| 3.9 |

| Beazer Homes USA ( BZH ) |

| 2.3 |

| 6.7 |

| 5.0 |

| KB Home ( KBH ) |

| 4.2 |

| 17.2 |

| 4.4 |

Takeaway

At this time, I understand why some investors would be hesitant to consider a stake in Taylor Morrison Home Corporation. I myself do not plan to buy any shares in the company, but only because I run a very concentrated portfolio. Having said that, shares do look very cheap and it's unlikely that they would come to be overvalued in any scenario I can see as being close to likely. Add on top of this the prospect for additional growth in the future once market conditions stabilize, and I do believe that Taylor Morrison Home Corporation warrants a solid "buy" rating even though the stock has risen nicely since I last wrote about it earlier this year.

For further details see:

Taylor Morrison: Don't Let Housing Market Doldrums Offset Cheap Shares