TMHC - Taylor Morrison Home: Digital Operating Improvements And Cheap

2023-04-11 05:49:57 ET

Summary

- Taylor Morrison is one of the most recognized companies in the United States when it comes to the development of real estate projects, administration, and acquisition of land.

- I believe that the know-how accumulated and the personnel hired may continue to deliver beneficial financial performance.

- The company acquired a significant number of targets in the past, so in my view, management counts on a lot of expertise in the M&A markets.

- I also think that recent digital improvements announced on the corporate website could serve as a beneficial revenue catalyst in the coming years.

Taylor Morrison Home Corporation ( TMHC ) recently delivered all-time low SG&A ratio, record adjusted home closing gross margins, and beneficial digital improvements. Considering the track record of individuals working for TMHC, the cash in hand, and previous experience in M&A, in my view, Taylor Morrison will likely deliver further inorganic growth in the coming years. Even taking into account risks from changing real estate markets or changing regulations, I believe that the stock is undervalued.

Taylor Morrison: A Wide Variety Of Consumers And Recent Improvement Of The Operating Efficiency

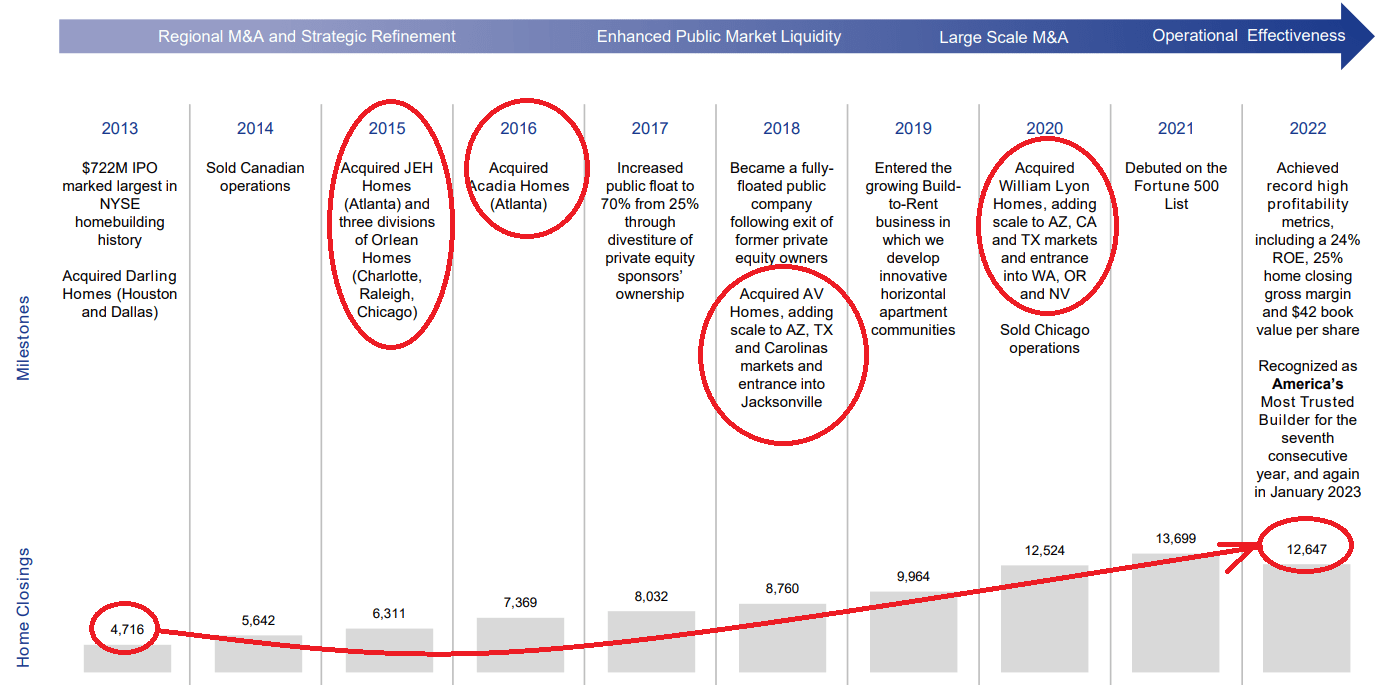

Taylor Morrison is one of the most recognized companies in the United States when it comes to the development of real estate projects, administration, and acquisition of land and residential construction. This recognition is based, for example, on receiving the award for the most reliable construction company in the country for eight consecutive years. There is also recent recognition in The Wall Street Journal that most investors may appreciate.

Our organization's strategy has always been rooted in smart growth and it is incredibly meaningful to see those efforts recognized by The Wall Street Journal as one of the most effectively managed companies in the country. Source: Taylor Morrison Home

The company has grown organically through acquisitions, serving clients looking for their first move, second move, or family move-in. This means that the company appears to have great capacity to adapt to the needs of each customer segment as well as a broad portfolio, at the construction level and in the supply of land for that construction.

Taylor Morrison distributes its operating segments geographically: East, Central, and West in addition to a fourth segment for financial services. These three segments have similar operations and share short and long-term strategies at the operating core of the company. The distribution of the operating segments intends to facilitate the optimization of the purchase, construction, and sale processes, innovation in the design and quality of its products, and improving the experience of its customers.

The clients vary according to their needs, and the company offers a portfolio oriented towards the construction of a first home, moving, or residential construction for families. In this sense, a large part of the clients arrives through its marketing programs and its digital platform. I believe that the company is worth a look considering the recent quarterly results and the recent efforts initiated in the digital platform of Taylor. In the 10-Q, the company reported a record adjusted home closing gross margin and an all-time low SG&A ratio of 8.2% in 2022. In my view, further profitability improvement will most likely bring interest from market participants.

Despite the swift change in housing market conditions that unfolded during the year, our teams delivered over 12,600 homes at a record adjusted home closing gross margin of 25.5%, which was up more than 500 basis points, and all-time low SG&A ratio of 8.2% in 2022. This produced a nearly-60% increase in our net income on a 10% increase in total revenue. Source: Taylor Morrison Home

I would also highlight the recent improvement of the balance sheet, the impressive amount of cash reported, and the cash flow generation in 2022. Have a look at the words from management before I offer further explanation about the financial stats of Taylor Morrison.

We generated $1.1 billion of cash flow from operations during the year, which was up from $377 million in 2021. In addition, we took several steps to further solidify our strong capital position during the year and ended the quarter with $1.8 billion of total liquidity, leaving us with ample flexibility to take advantage of investment opportunities as the market evolves. Source: Taylor Morrison Home Corp. - Taylor Morrison Reports Fourth Quarter 2022 Results

Assets

As of December 31, 2022, Taylor Morrison Home Corporation reported cash of $724 million, owned inventory of $5.346 billion, and land deposits of $263 million. Considering the total amount of cash and real estate assets, in my view, Taylor will likely not have significant liquidity problems. Total real estate is worth more than the total amount of liabilities.

The company also reported mortgage loans held for sale of $346 million, lease right of use assets of close to $90 million, prepaid expenses and other assets of $264 million, and other receivables of close to $191 million. Besides, with investments in unconsolidated entities worth $282 million, property and equipment of $202 million, and goodwill of $663 million, total assets stood at $8.470 billion .

Source: Annual Report

Liabilities

It is beneficial that Taylor Morrison Home Corporation reported less liabilities in 2022 than that in 2021. The company paid revolving credit facilities, and lowered its senior notes outstanding. In addition, loans payable is also less significant. In my view, management decided to lower its debt obligations as soon as the interest rates trended north.

The last balance sheet reported included accounts payable worth $269 million, accrued expenses and other liabilities of $490 million, lease liabilities worth close to $100 million, and customer deposits of $412 million.

Debt included senior notes of $1.816 billion, loans payable and other borrowings of $361 million, and mortgage warehouse borrowings of $306 million. In sum, total liabilities were equal to $3.823 billion.

Source: Annual Report

Assumptions Under My DCF Model Include Further Acquisitions, Successful Human Resources Management, And Digital Improvements

Considering that the company has gone from close to 4.7k home closings in 2023 to around 12.4k home closings in 2022, I believe that the know-how accumulated and personnel hired may continue to deliver beneficial financial performance. In the long-term, I believe that Taylor Morrison will successfully identify further valuable lands to be acquired, and will likely build distinctive communities.

I also believe that further operational effectiveness and new M&A transitions will most likely accelerate the business model. The company acquired a significant number of targets in the past, so in my view, management counts with a lot of expertise in the M&A markets.

{kind=link}

I also believe that further innovation in digital areas, low-cost operational discipline, and continued discipline in the allocation of capital could also serve as revenue catalysts. More in particular, I invite investors to have a look at the list of new digital improvements included in the website of Taylor Morrison . In my opinion, many of the new digital applications will likely have an impact on the free cash flow from 2023.

In 2022, we used consumer feedback to refine and improve our website and interactive, experiential, and highly tailored home reservation system. Our full suite of online shopping products includes: 1) a state-of-the-art customized chatbot to help provide information, engage the shopper, and capture the lead; 2) online self-service appointments to help customers schedule an appointment with ease and convenience; 3) self-guided tours to enable customers to tour our homes privately, safely, and outside of normal business hours; and 4) online home reservations, which allow shoppers to get an initial price and reserve their desired home configuration digitally.

My DCF Model Implied A Valuation Of $67.2 Per Share

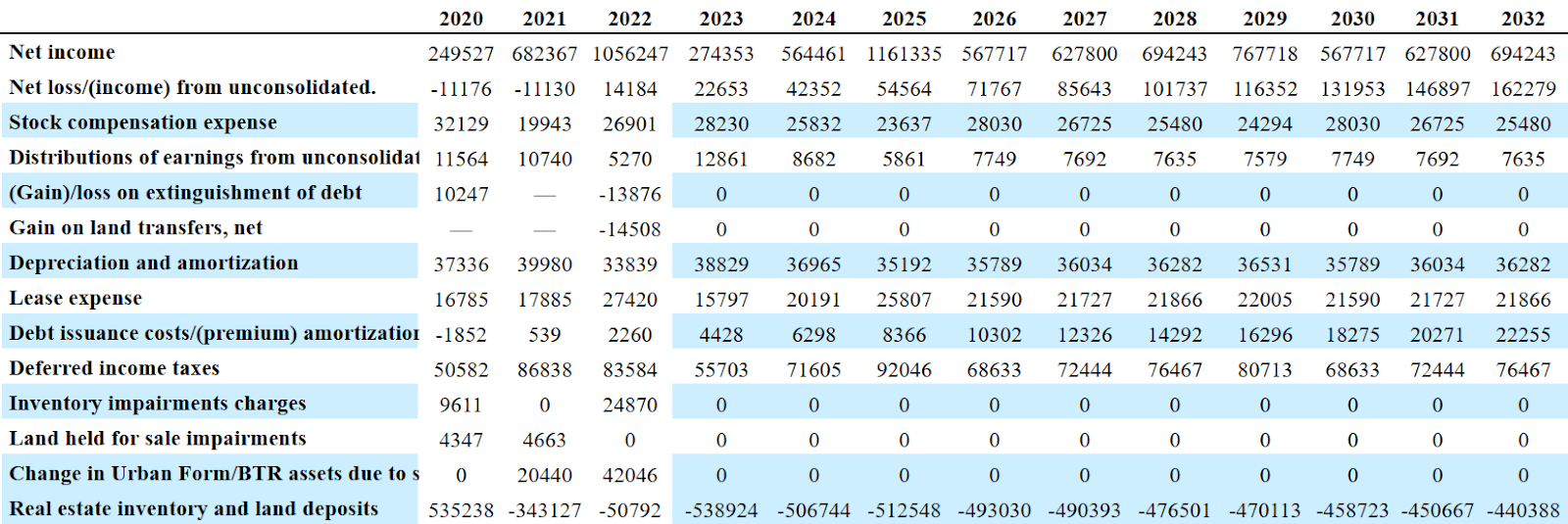

Under the previous assumptions, I included net income growth from 2023 to 2032, income growth from unconsolidated entities, no gain from land transfers, or inventory impairment changes. I also included growth in accounts payable, growth from customer deposits, and CFO growth. I believe that my numbers are very reasonable and conservative.

2032 net income included was equal to $694 million with net loss income from unconsolidated entities of $162 million, stock compensation expenses worth close to $25 million, and 2032 lease expense of $21 million.

{kind=link}

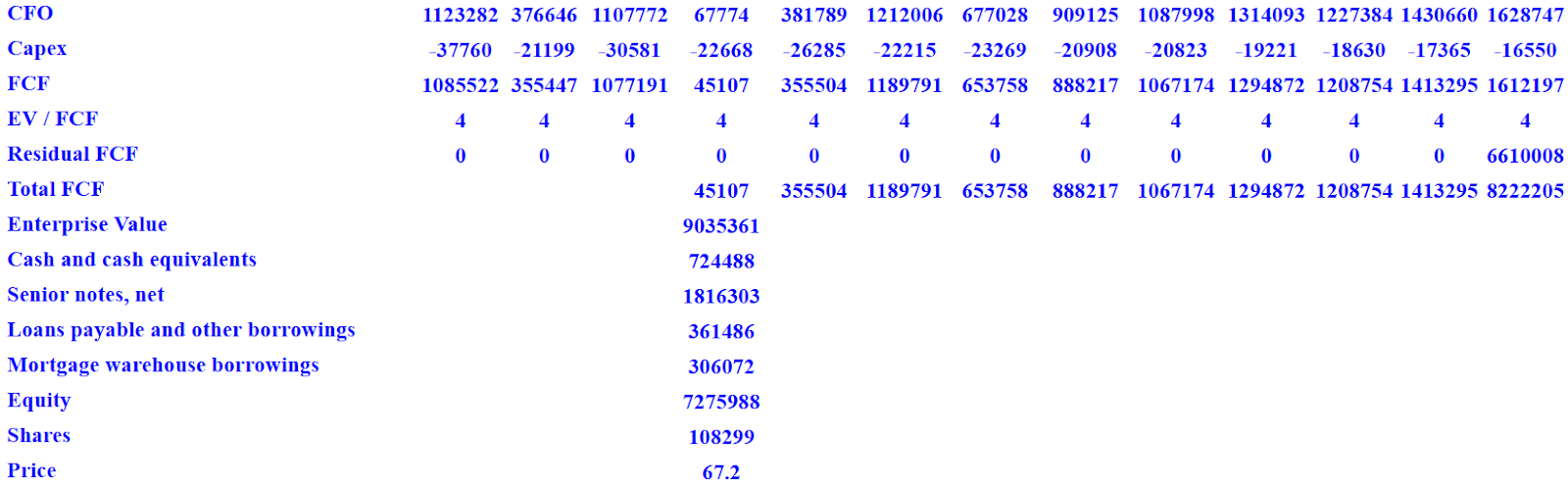

Also, with deferred income taxes of close to $76 million, changes in prepaid expenses and other assets of close to 281 million, and 2032 changes in customer deposits of $235 million, 2032 CFO would be close to 1.628 billion. If we also assume 2032 capital expenditures of -$17 million, 2032 FCF would be close to $1.612 billion.

{kind=link}

If we include a conservative EV/FCF multiple of 4x, the enterprise value would be close to $8.959 billion. If we add cash of $724 million, and subtract senior notes of $1.816 billion, loans payable and other borrowings of 361 million, and mortgages of $306 million, the equity would stand at $7.506 billion, and the fair price would be $67 per share.

{kind=link}

Competitors And Risks

The construction market is a highly competitive market in which there are large construction companies at the national level and small construction companies at the regional level. We also include financial services, raw material providers, labor force managers, and various agents that are part of the market environment. In any case, Taylor Morrison Home competes in relation to prices, quality, and services with both large construction companies and regional ones.

Taylor Morrison's business is subject to seasonality, global economic conditions, and variations in interest rates. Under the worst case scenario, I would assume that if credit markets fail to offer beneficial conditions to clients, the purchase of houses would decline, which may lead to declining business results.

Likewise, supply chain issues and failed access to raw materials are very relevant risk factors. Besides, variations in transportation prices and variations in land prices play a fundamental role in the continuous course of operations. Some of these factors could deteriorate the cash flow from operations, which may lead to lower FCF expectations. If investors lose their faith, I believe that demand for the stock could decline, which may push the stock price down.

Besides, the company's inability to carry out its growth and acquisition strategy because management fails to find suitable M&A candidates could be a disaster. The market expects new acquisitions to sustain long term revenue growth, so I hope that the company does not lower the amount of inorganic growth.

Also, I believe that we should name the permanent and necessary adaptations to the US regulation system for construction companies, specifically with regard to new adaptations to reduce gas emissions. If Taylor Morrison Home has to modify the way operations are conducted, and more capex is necessary, FCF expectations would most likely decline.

Conclusion

Taylor Morrison is not only a well regarded developer of real estate projects, the company recently delivered record adjusted home closing gross margin, all-time low SG&A ratio, and a significant amount of cash in hand. Considering the individuals working for the organization, their track record, and expertise in the M&A markets, I would expect CFO growth. I also think that recent digital improvements announced on the corporate website could serve as a beneficial revenue catalyst in the coming years. Even considering the risks from changing interest rates or changes in the real estate markets, I think that Taylor Morrison appears significantly undervalued.

For further details see:

Taylor Morrison Home: Digital, Operating Improvements, And Cheap