TMHC - Taylor Morrison Home: Still A Buy After Strong Rally?

2023-05-19 09:18:00 ET

Summary

- Taylor Morrison Home Corporation stock has seen a 63% gain over the past 13 months, indicating a stabilizing housing market.

- Despite potential recession risks, TMHC remains an attractive investment due to its fair valuation and consistent performance.

- The company forecasts a year-over-year drop in unit sales but maintains a strong balance sheet, high gross margins, and improving pricing power.

- With a 55% increase in total cash, a large share repurchase program, and a home building net debt to capital ratio at an all-time low, TMHC is an attractive buy during market pullbacks.

Introduction

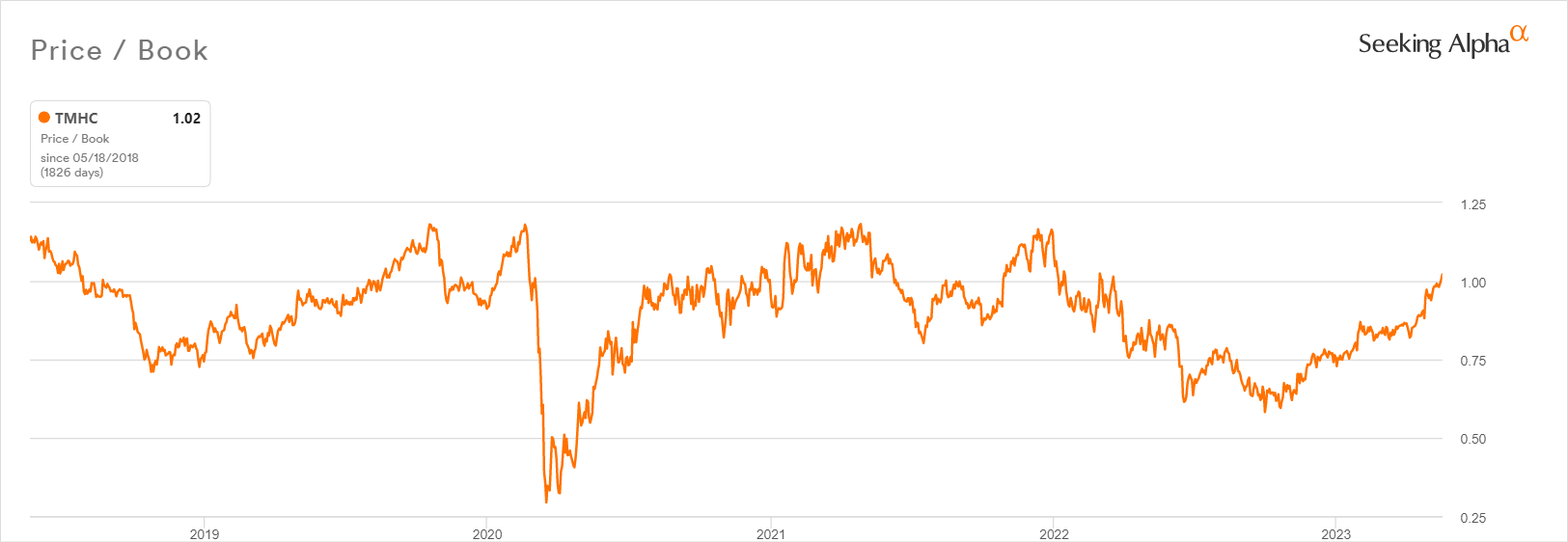

Taylor Morrison Home Corporation (TMHC) delivered a Q1 earnings report that further confirmed the stabilizing housing market that I described with the earlier earnings report from KB Home (KBH). Conditions have also improved from 13 months ago when I identified TMHC as underperforming and underappreciated . The stock is now better appreciated with a 63% gain since then, including a 16% gain since reporting Q1 earnings. The gain compares favorably to the S&P 500's 6% loss since my earlier article and even the 31% gain for the iShares U.S. Home Construction ETF (ITB). Yet, TMHC's valuation remains attractive with a price/book at 1.0 which is typically "fair value" for a home builder in a housing recession. The forward P/E for TMHC increased from the low single digits to the mid single digits.

TMHC's price/book ratio still has upside potential before reaching recent peaks. (Seeking Alpha)

{kind=link}

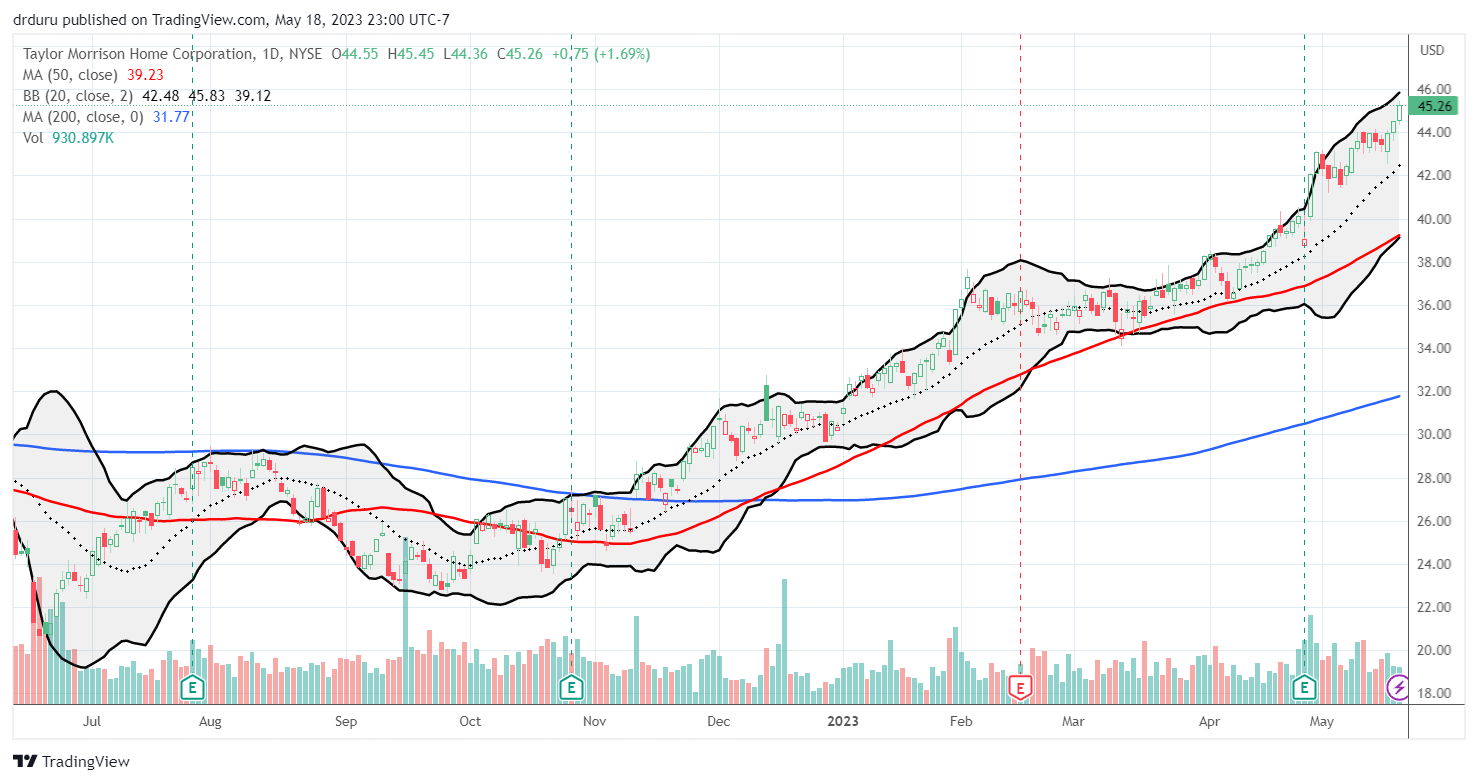

Still, new risks exist in buying TMHC. A long awaited recession for the general economy looms ever closer. Economic trouble would increase unemployment and stall the current recovery in the housing market. Moreover, the seasonally strong period for homebuilders is coming to an end. Thus, upside from current levels could be quite limited, especially relative to the S&P 500. Under these collective conditions, I would not add to shares in TMHC unless/until it pulled back to a key support levels like the 50-day moving average ("DMA") (the uptrending red line below).

THMC has enjoyed a consistent and strong uptrend since the September low stopped short of the June low. (Tradingview.com)

{kind=link}

Guidance

I like to start an earnings review with guidance since the news contained there most directly influences new trading and investment decisions. Guidance takes on even greater significance at this juncture of macroeconomic uncertainty. While Taylor Morrison is forecasting a greater year-over-year drop in unit sales, the business is not suffering any other notable impact from the housing recession. I took most of the following data and quotes from the transcript of the earnings call (other references included as needed).

Taylor Morrison expects to deliver between 2,600 to 2,700 homes in Q2, a 13% decline in home closings at the midpoint . For the full year, the company anticipates delivering between 10,000 to 11,000 homes. This 17% year-over-year decline at the midpoint is much higher than the 8% decline from 2021 to 2022. Notably, the company did not condition this guidance on economic developments. Instead, management pointed to assumptions of static cycle times and the current number of homes under construction. Thus, TMHC must be anticipating a trough year for deliveries in 2023.

Starts activity also points to a bottom in sales. The company "accelerated [its] starts volume to approximately 2,500 homes, given the improvement in sales activity and [its] focus on rebuilding inventory levels to maintain approximately one finished spec home per community." (Housing starts also increased across all regions in the U.S. from March to April ). The resulting 2.6 starts per community per month is higher than the 1.6 in Q4 but far lower than the 4.2 a year ago.

TMHC expects to have its best first half of a year since before 2000 by closing nearly half of the year's deals in this time.

The year-over-year decline in deliveries comes with a small drop in margins. The ability to protect margins is very important for assessing home builders given the amount of capital tied up in home building. For Q2, Taylor Morrison expects home closings gross margin between 23% and 23.5% based on delivery mix. This range compares favorably to Q1's 23.9% margin and full-year 2022 gross margin of 25.2% (including inventory impairment). For the full year, the company anticipates maintaining an approximately 23% gross margin. TMHC will need to demonstrate it can hold the line on this margin for the next earnings reports for the year.

Market Dynamics

Taylor Morrison reported some surprising market dynamics that support its expectations for stabilization in the housing market. First of all, a notable contingent of the customers are moving from an existing home. They are apparently not anchored by lower mortgage rates on an existing home. From the earnings conference call (emphasis mine):

"Parsing the trends by consumer group, sales were strongest among move up buyers, which accounted for nearly half of our net orders led by our second time move up category where both sales and pace were up firmly year-over-year . This was followed by our entry-level segment, where first time buyer demand for spec homes stabilized with the use of our strategic incentive programs, while our resort lifestyle segment experienced a pickup as we move through the quarter."

Moreover, 45% of the buyers in Taylor Morrison's backlog already own a home. While the company did not provide a point of reference, this data point further underscores the existence of plenty of buyers willing to exchange presumably lower rate mortgages for higher ones. I suspect many of these buyers recognize that at some point in the not-so-distant future, they should be able to refinance to lower rates. The presumed peak in rate hikes brings the refresh of refinance opportunities even closer.

In Q1, sales were strong enough to send orders per community to 3.4, their highest level since Q3 of 2021. Monthly net sales pace increased quarterly from 1.9 to 2.9 per community, just shy of the 3.1 a year ago. The cancellation rate also fell to "a more normalized level of 14% of gross orders." With buyers averaging deposits of 10% of sales price, there is a large disincentive for cancellation. Net orders, however, decreased by 7% year-over-year to 2,854 homes due to the tough comparison to the period right before mortgage rates took off and took cancellation rates upward. Still, revenue declined only slightly by 2.4% year-over-year while GAAP diluted earnings per share soared 21% year-over-year . The company attributed the earnings performance to the (year-over-year) improved home closing gross margin, better profitability in financial services, and a 10% reduction in the diluted share count thanks to buyback activity.

The financial performance drove a 55% increase in total cash, cash equivalents, and restricted cash. Cash is now back to end-of-year 2021 levels. Home building net debt to capital ratio declined to a company all-time low of 21%. Taylor Morrison's solid balance sheet makes it an attractive buy on dips created by macro-economic scares.

Pricing Dynamics

Like most home builders, Taylor Morrison has been able to reduce incentives in many communities and even increase prices in some. The shift in pricing strategy has "reinforced a sense of urgency among shoppers and solidified the value of [the] backlog." Sheryl Palmer, Taylor Morrison's CEO, explained pricing psychology this way:

"[in] a couple of our markets, we heard the narrative from the field that as builders were getting more aggressive with pricing and discounts, it actually is an unsettling feeling for the consumer, because when buyers believe that prices are continuing to drop, there is not a strong motivation to jump in. I think we saw the same thing with interest rates.

I think part of the continued momentum we've seen that we aren't seeing continuing price deterioration, interest rates have settled."

In other words, inflation motivates home buyers and a downtrend in rates can slow down buying pace. It will be interesting to see whether home buying slows down after it is clear that the Fed is done hiking rates or instead buying picks up as the market anticipates the potential to refinance in the near future.

Echoes from Home Builder Sentiment

The May report on home builder sentiment from the National Association of Home Builders (NAHB) underlined the on-going opportunity for home builders. The NAHB reported that "33% of homes listed for sale were new homes in various stages of construction. That share from 2000-2019 was a 12.7% average." Thus, some builders can continue to thrive in the housing recession by taking share from the existing home market. Yet, as described earlier, Taylor Morrison has a large share of customers moving from existing homes. So it is very possible the share tailwind will slow down soon.

The NAHB also reported improving price dynamics in favor of sellers. These data points support continued success for builders like Taylor Morrison in withdrawing incentives and slowing price reductions.

- The share of builders reducing home prices dropped to 27% in May, down from 30% in April, 31% in Feb. and March, and 36% last November.

- The average price reduction remains at 6%, unchanged for the past four months.

- 54% offered some type of incentive to bolster sales in May, down from 59% in April and 62% last December.

The Trade

Taylor Morrison is America's most trusted home builder 8 straight years for a reason. Yet, a large acquisition just ahead of the pandemic helped to turn the company into an underappreciated builder. Now, the script has flipped. Taylor Morrison is out-performing most of its peers and trades at an all-time high while continuing to sport a reasonable valuation. An on-going share buyback is helping to further boost shares. Taylor Morrison spent $4M in Q1 buying back shares at an average price of $32.64. The $276M left of its $500M share repurchase authorization offers the prospect of a floor on the stock in future sell-offs. I consider TMHC a good buy-the-dip candidate as long as margins hold and a trough in sales is confirmed with some year-over-year momentum by the time of the start of the next seasonally strong period for home builders.

For further details see:

Taylor Morrison Home: Still A Buy After Strong Rally?