TMHC - Taylor Morrison Home Still Makes Sense Despite Pain That Lies Ahead

Summary

- Taylor Morrison Home Corporation continues to post fantastic fundamental results from quarter to quarter.

- But when you dig deeper, you see the pain that's right around the corner.

- Investors who don't like volatility may want to look elsewhere, but this pain seems priced into shares already.

On its face, value investing seems like a very easy way to make money. But the fact of the matter is that it's difficult and tricky. One of the biggest dangers facing value investors is the value trap. This is a company that looks unbelievably cheap but which ultimately deserves to be cheap for some reason. To many investors in the market right now, anything associated with the homebuilding space could be viewed as a value trap because multiples are incredibly low thanks to robust cash flows but significant signs of weakening are showing. While I fully suspect that pain in this space will only grow from here for the foreseeable future, I do also think that some of these firms are trading at levels that don't make sense even with the pain that lies ahead.

One example of this can be seen by looking at Taylor Morrison Home Corporation ( TMHC ), a player in the market that has a presence across various parts of the US. Recently, revenue, profit, and cash flow data have been unbelievably robust for the firm. But even now, there are significant cracks showing and its fundamental condition. Absent some miracle, the near-term future for the company will look far worse than its recent past has been. But even if we assume a continued weakening from this point, it's difficult to imagine shares looking overvalued. So while I expect that the stock might face some volatility in the quarters that lie ahead, I am still comfortable rating it a soft ‘buy’ for now.

Shares still look cheap

Back in August of 2022, I wrote an article that took a bullish stance on Taylor Morrison. In that article, I acknowledged that signs of weakness were starting to emerge. But even with that being the case, I found myself impressed by the company's fundamental health. This, combined with how cheap shares were, led me to rate it a ‘buy’ to reflect my view that shares should generate upside that should exceed what the broader market could over a similar timeframe. And so far, that call has proven to be pretty positive. While the S&P 500 is down 6.3% since the publication of that article, Taylor Morrison has generated upside for investors of 15%.

{kind=link}

Author - SEC EDGAR Data

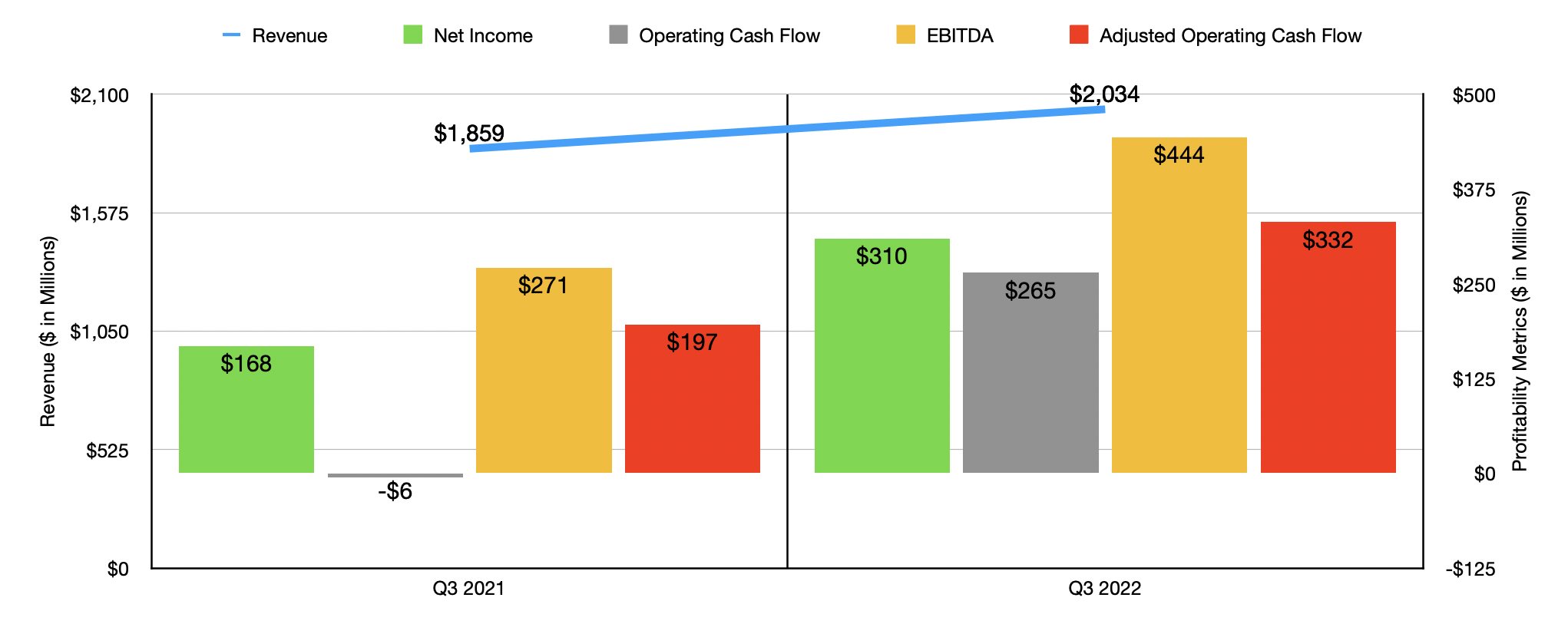

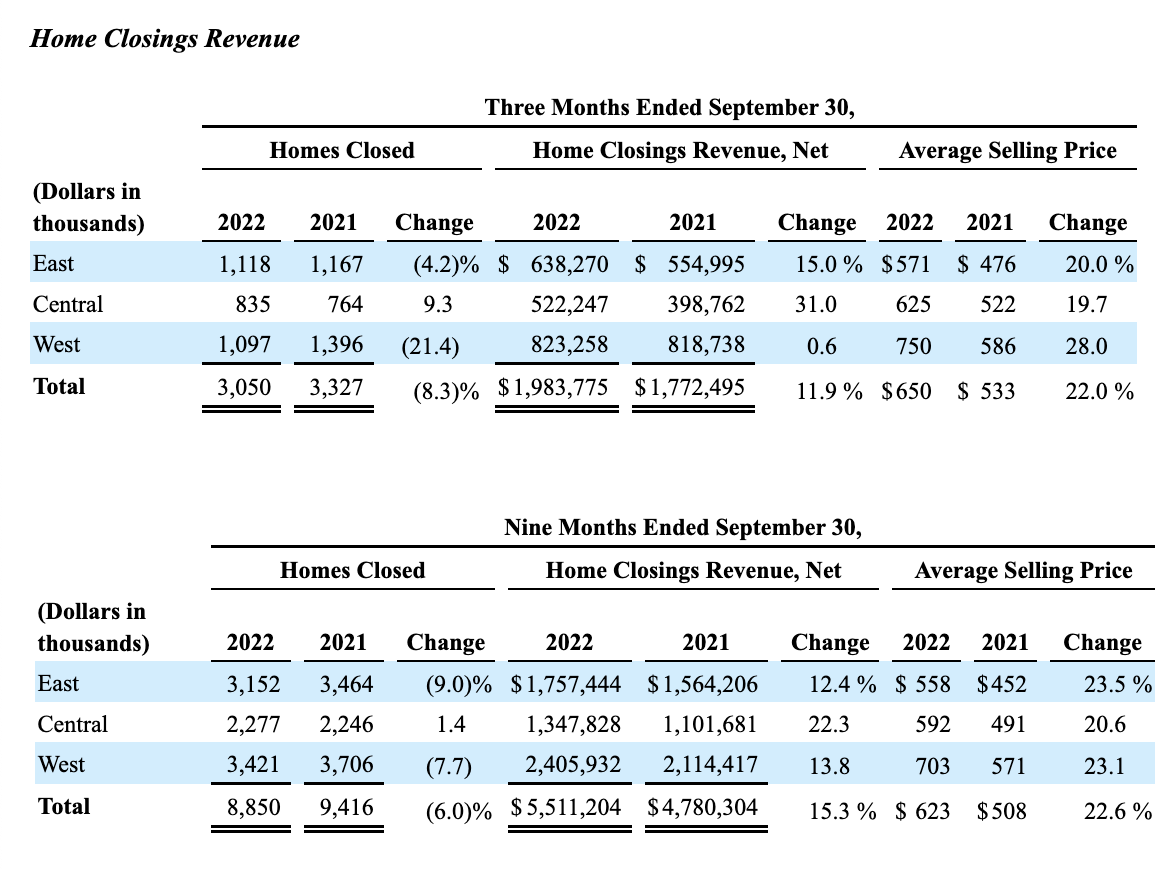

This return disparity is not without cause. To see what I mean, we need only look at data covering the third quarter of the company's 2022 fiscal year. This is the most recent quarter for which data is available and the only quarter for which new data has come out since I last wrote about the firm. Sales during that time totaled $2.03 billion. That's 9.4% higher than the $1.86 billion generated the same time one year earlier. Interestingly, this increase came even as the number of homes closed by the company dropped 8.3% year over year, falling from 3,327 to 3,050. The real driver behind this increase, then, was a surge in the average selling price of homes closed. That number jumped 22% from $533,000 to $650,000.

{kind=link}

Taylor Morrison

That move up in pricing was instrumental in pushing profits and cash flows higher for the company as well. Net income totaled $309.8 million for the third quarter. That's almost double the $168.1 million reported the same time one year earlier. Operating cash flow went from negative $5.9 million to positive $264.5 million. If we adjust for changes in working capital, it would have risen from $196.5 million to $331.5 million. Meanwhile, EBITDA increased from $271.2 million to $443.7 million.

{kind=link}

Author - SEC EDGAR Data

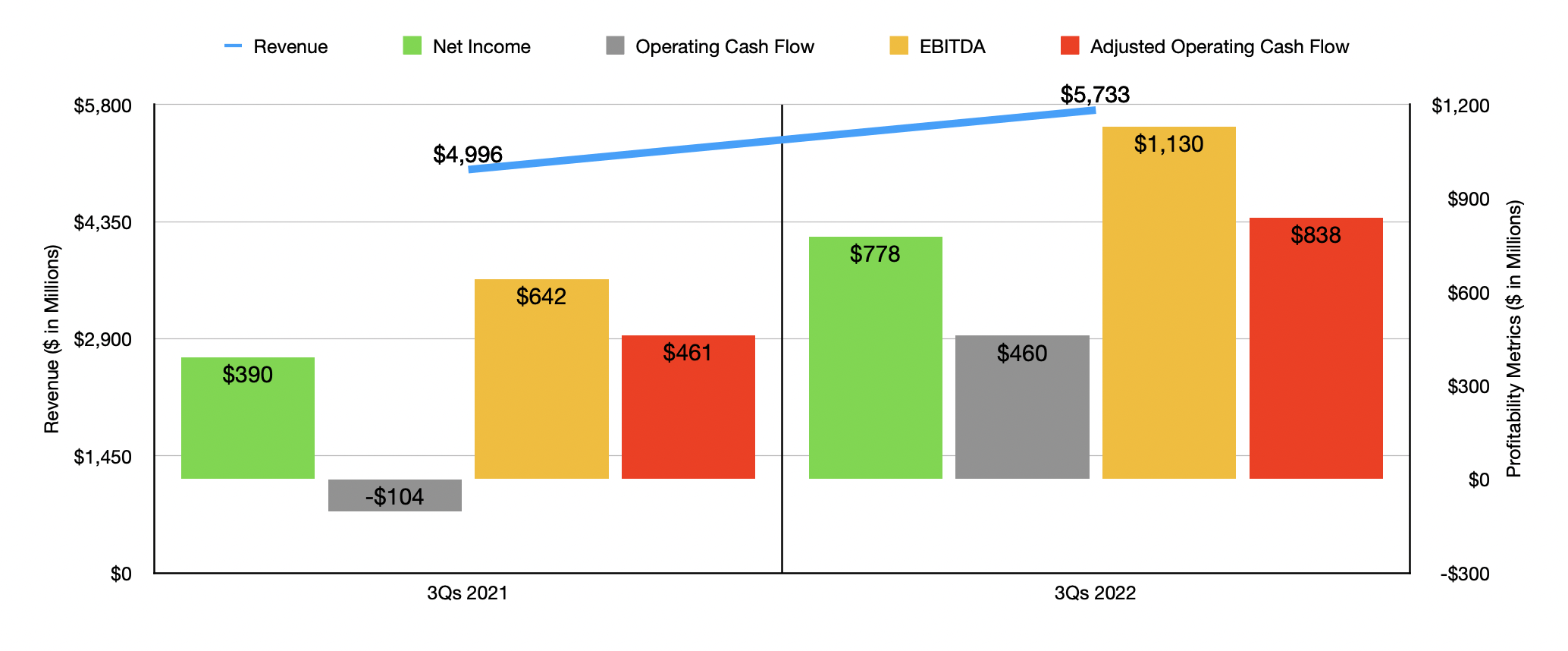

The third quarter was no fluke. The first nine months of 2022 look similar when placed against the first nine months of 2021. Revenue of $5.73 billion beat out the roughly $5 billion reported one year earlier. Even though the number of homes closed dropped by 6% year over year, the company benefited from a 22.6% increase in the average selling price of the homes. This helped to push profits higher also, with net income shooting from $390.3 million to $777.5 million. Operating cash flow went from negative $103.5 million to $460 million, while the adjusted figure for this expanded from $461.4 million to $837.8 million. And finally, EBITDA for the company almost doubled, jumping from $641.8 million to $1.13 billion.

{kind=link}

Taylor Morrison

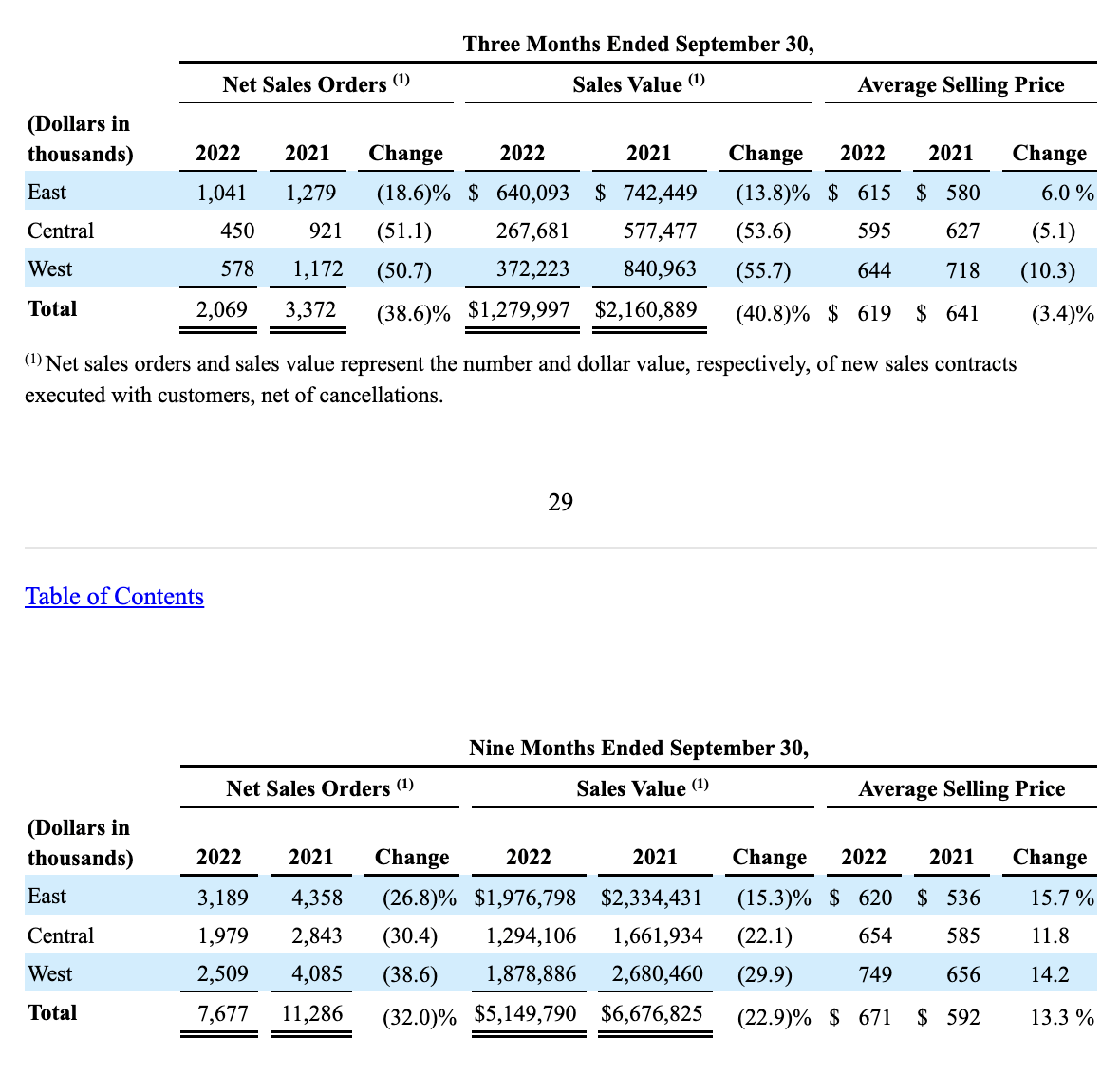

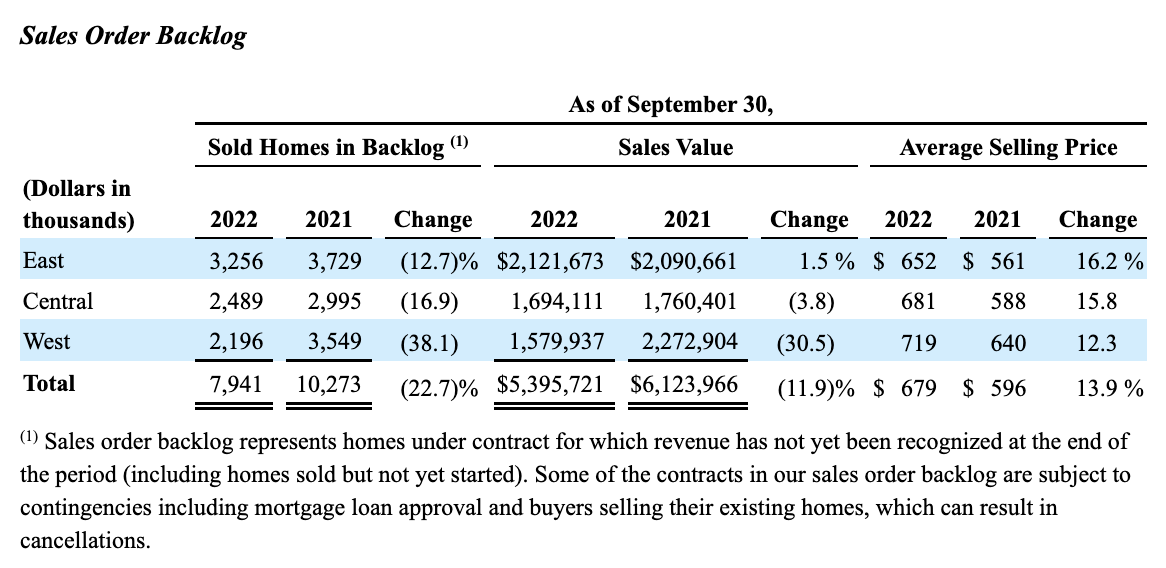

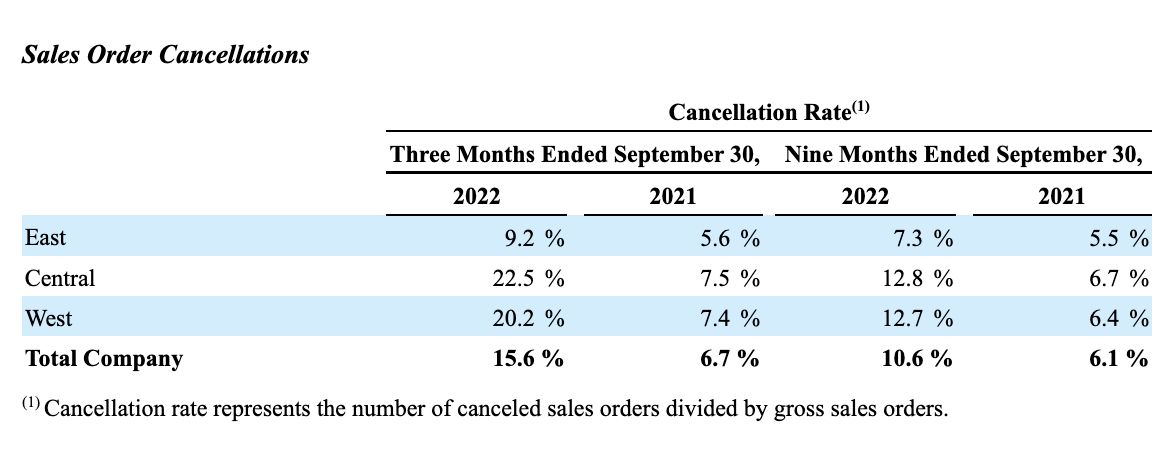

All of this looks good so far except for the decline in homes delivered. But the company is showing some other worrying signs. The number of homes in its backlog, for instance, dropped from 10,273 in the third quarter of 2021 to 7,941 the same time of 2022. Part of this drop can be attributed to the number of net sales orders plunging in the first nine months of each year from 11,286 to 7,677. the drop here was particularly bad during the third quarter, with the number of net sales orders falling from 3,372 to 2,069 for a year-over-year decline of 38.6%. What was particularly painful for the company is a surge in sales order cancellations. That picture also seems to be worsening, with 15.6% of gross sales orders canceled in the third quarter of 2022 compared to 6.7% one year earlier.

{kind=link}

Taylor Morrison

{kind=link}

Taylor Morrison

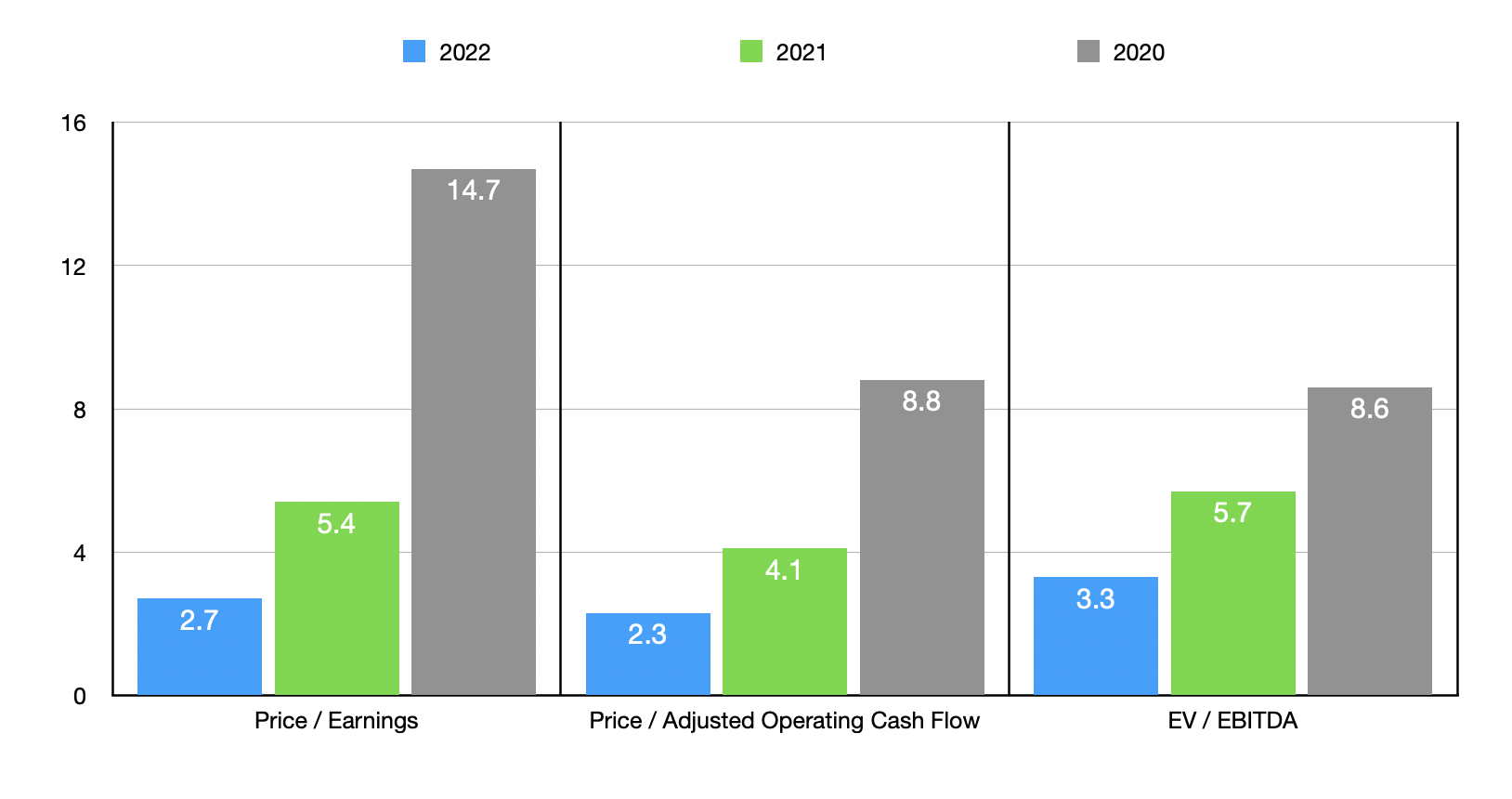

If shares of the company were not incredibly cheap, I would say that this is all the more reason for investors to consider looking elsewhere for opportunities. And in truth, there probably are better prospects on the market, not the housing market necessarily but the broader market, that might be more appealing. But if we annualize results experienced so far for 2022, we get some really interesting results. The firm should generate net income of $1.32 billion, adjusted operating cash flow of $1.58 billion, and EBITDA of $1.84 billion.

{kind=link}

Author - SEC EDGAR Data

Using these figures, I calculated that the company is trading at a forward price-to-earnings multiple of 2.7. The price to adjusted operating cash flow multiple is even lower at 2.3, while the EV to EBITDA multiple should be 3.3. But as I clearly demonstrated, these good times are not here to stay. But even if financial results revert back to what they were in 2020, shares would look quite affordable as you can see by looking at the chart above. For context, I also compared the company to five similar enterprises. On a price-to-earnings basis, these companies ranged from a low of 2 to a high of 8.2. Only one of the five was cheaper than Taylor Morrison. Using the price to operating cash flow approach, only two companies had positive results, while for the EV to EBITDA approach, we had data for all five. In both of these cases, our prospect was the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Taylor Morrison Home Corporation |

| 2.7 |

| 2.3 |

| 3.3 |

| Legacy Housing ( LEGH ) |

| 8.2 |

| 47.5 |

| 6.1 |

| Meritage Homes ( MTH ) |

| 3.9 |

| N/A |

| 3.5 |

| Century Communities ( CCS ) |

| 3.2 |

| N/A |

| 3.9 |

| Beazer Homes USA ( BZH ) |

| 2.0 |

| 5.7 |

| 4.2 |

| KB Home ( KBH ) |

| 3.8 |

| N/A |

| 4.2 |

Takeaway

From what I can see here, Taylor Morrison is doing incredibly well from a cash flow perspective at this moment. But investors would be right to be concerned about the future. With housing data looking pretty bad, it's only a matter of time before revenue and cash flows start to decline year over year. In the near term, this could get uncomfortable and shares could experience a lot of volatility as a result. But in the long run, the company should do quite well for itself, and I have no problem rating it a soft ‘buy’ with that long-term outlook in mind.

For further details see:

Taylor Morrison Home Still Makes Sense Despite Pain That Lies Ahead