TMHC - Taylor Morrison: Reasonable Valuation And Approaching Bottom (Rating Upgrade)

2023-11-14 13:29:07 ET

Summary

- Taylor Morrison Home Corporation's stock has underperformed the market but is now at an attractive entry point with a P/TBV ratio of ~1x.

- While TMHC's sales have declined due to rising interest rates, there are indications of potential stabilization and bottoming in the second half of FY24.

- TMHC's diverse customer base and cost reduction efforts should help shield it from a downturn, and the stock can give high teen returns by the end of the next year.

Investment Thesis

I last covered Taylor Morrison Home Corporation ( TMHC ) in June this year where I recommended moving to the sidelines given the stock’s high valuations. The stock was trading at a Price to Tangible Book Value (P/TBV) ratio of ~1.24x at that time. The stock has underperformed the broader markets since then and is down ~9% versus the S&P 500’s ( SPY ) flattish performance. While the macro environment remains tough with high-interest rates, some leading indicators like new orders and backlog levels are indicating that we are near the bottom. Further, the stock price corrections coupled with an increase in tangible book value since my previous article has resulted in the P/TBV ratio reaching ~1x at current levels which presents an attractive entry point. So, I am upgrading the stock to buy.

Revenue Analysis and Outlook

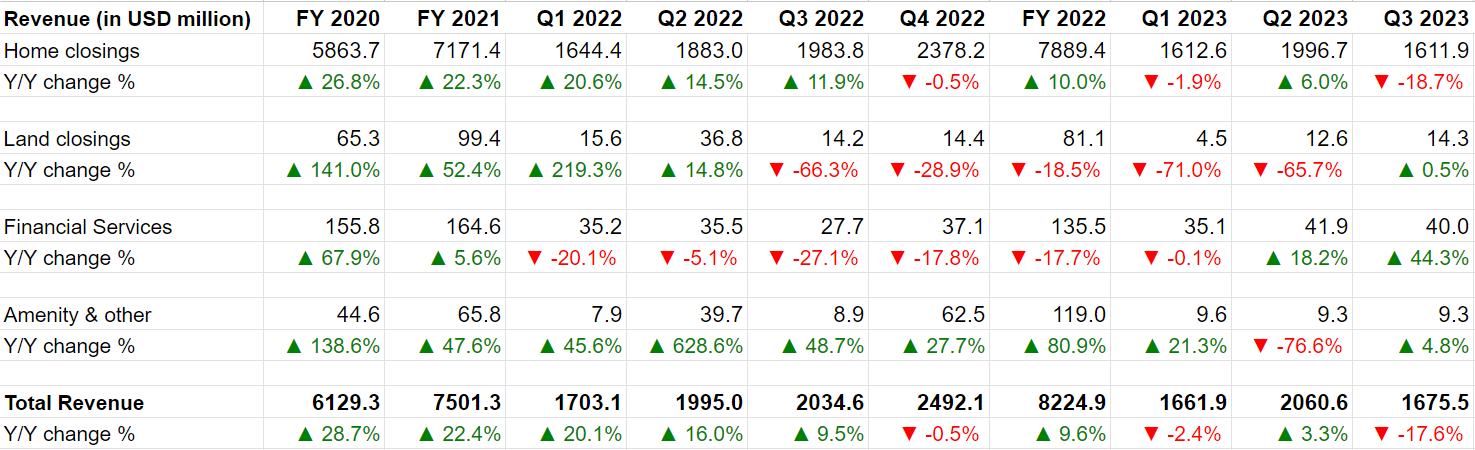

After seeing good growth in the couple of years following the pandemic, TMHC’s sales came under pressure this year due to rising interest rates. Last quarter, the company’s total revenues declined ~18% Y/Y to $1.676 bn driven by a ~19% Y/Y decline in Home Closing revenues.

{kind=link}

TMHC’s Historical Revenue Growth (Company Data, GS Analytics Research)

Looking forward, while the next quarter and early 2024 should still be down Y/Y, there are some green shoots that indicate potential stabilization and bottoming in the second half of FY24.

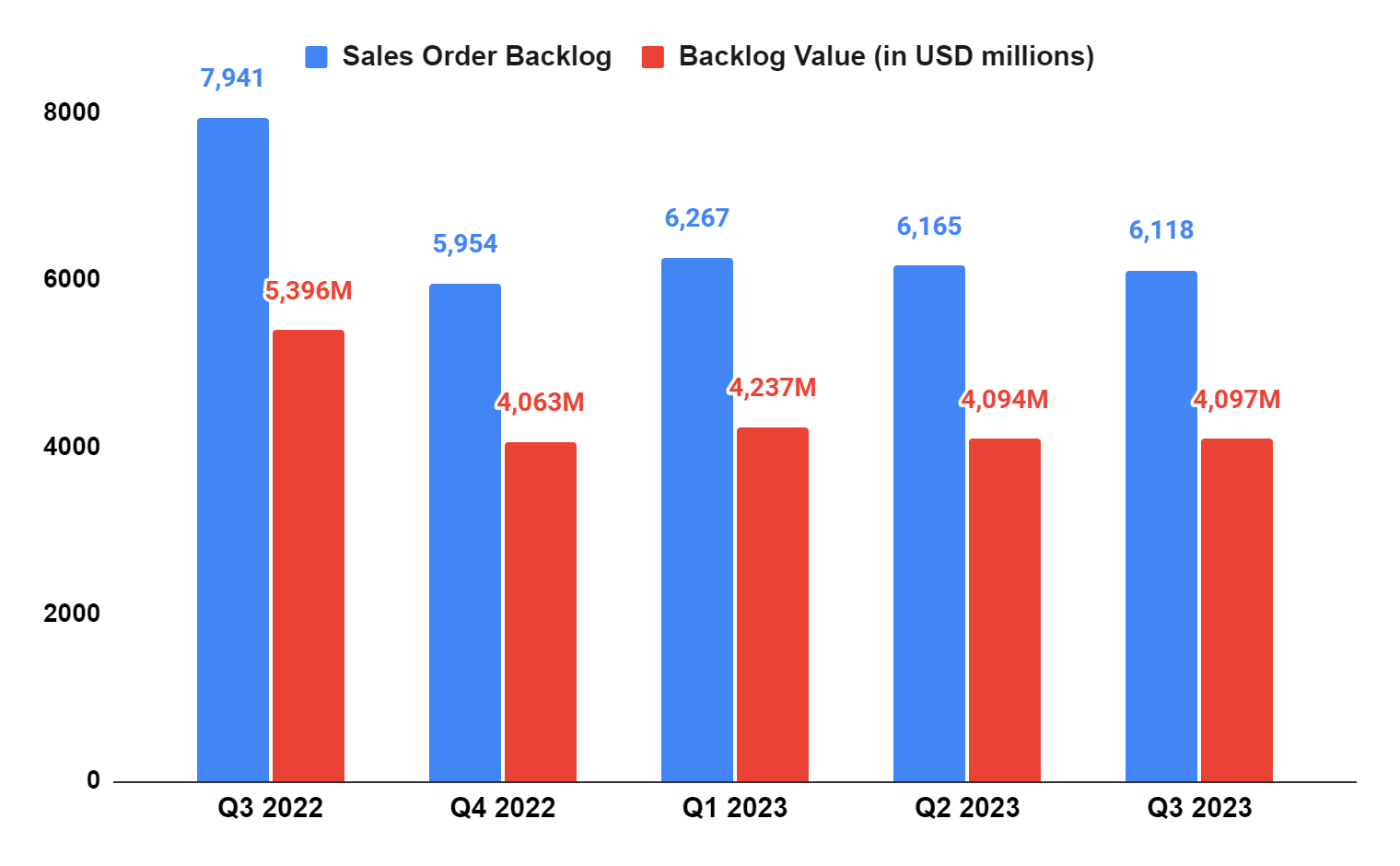

The company’s net new home sales orders increased 25.3% Y/Y to 2.592 in Q3 FY23 while its average selling Price per new order was up 1% Y/Y to $623 thousand. If we look at its backlog while it was down meaningfully Y/Y, it has been stabilizing for the last four quarters. Since orders and backlog are the leading indicators of future revenues, I believe revenue should also see some bottoming especially in the back half of FY24 when comparisons would ease.

TMHC’s Backlog units and Backlog value (Company Data, GS Analytics Research)

{kind=link}

Further, management noted that while mortgage rates have seen a significant uptick in recent months and the order pace slowed in September and October as a result, net new orders were still up Y/Y in October. This indicates a good demand environment for new homes. I believe that the significant underbuilding of new homes for over a decade after the great housing recession has resulted in a tight demand-supply environment which should support new home construction even in this high interest-rate environment. I believe once the interest rate cycle turns, we should see a sharp recovery in sales in the medium to long term.

One good thing about TMHC is that it serves a diverse range of customers, including entry-level (35% of its sales last quarter), first-and-second move-up (43% of its sales last quarter), and resort lifestyle (22% of its sales last quarter). While entry-level homes have seen good demand from younger demographics over the last few years, younger buyers have also borne the brunt of rising mortgage rates in recent times. The second move-up and resort lifestyle buyers have significant financial flexibility. On TMHC's Q3 earnings call, commenting on this trend management said ,

“.. .the vast majority of our 55-plus buyers pay all cash at a rate that is 3 times higher than younger buyers.

Their financial strength is also evident in our sizable third quarter lot premiums and option revenue, which averaged nearly $110,000 in total and can contribute up to a several hundred basis point advantage for to-be-built gross margins compared to our spec margins. This is consistent with the long-term premium commanded by to-be-built sales prior to the pandemic that we expect will persist going forward."

So, I believe the company’s diverse exposure should shield it from the downturn in the near term compared to entry-level-only homebuilders.

Overall, I believe the company can see its revenues bottoming in 2H FY24 and then recovering in the medium to long term as the interest rate cycle reverses.

Margin Analysis and Outlook

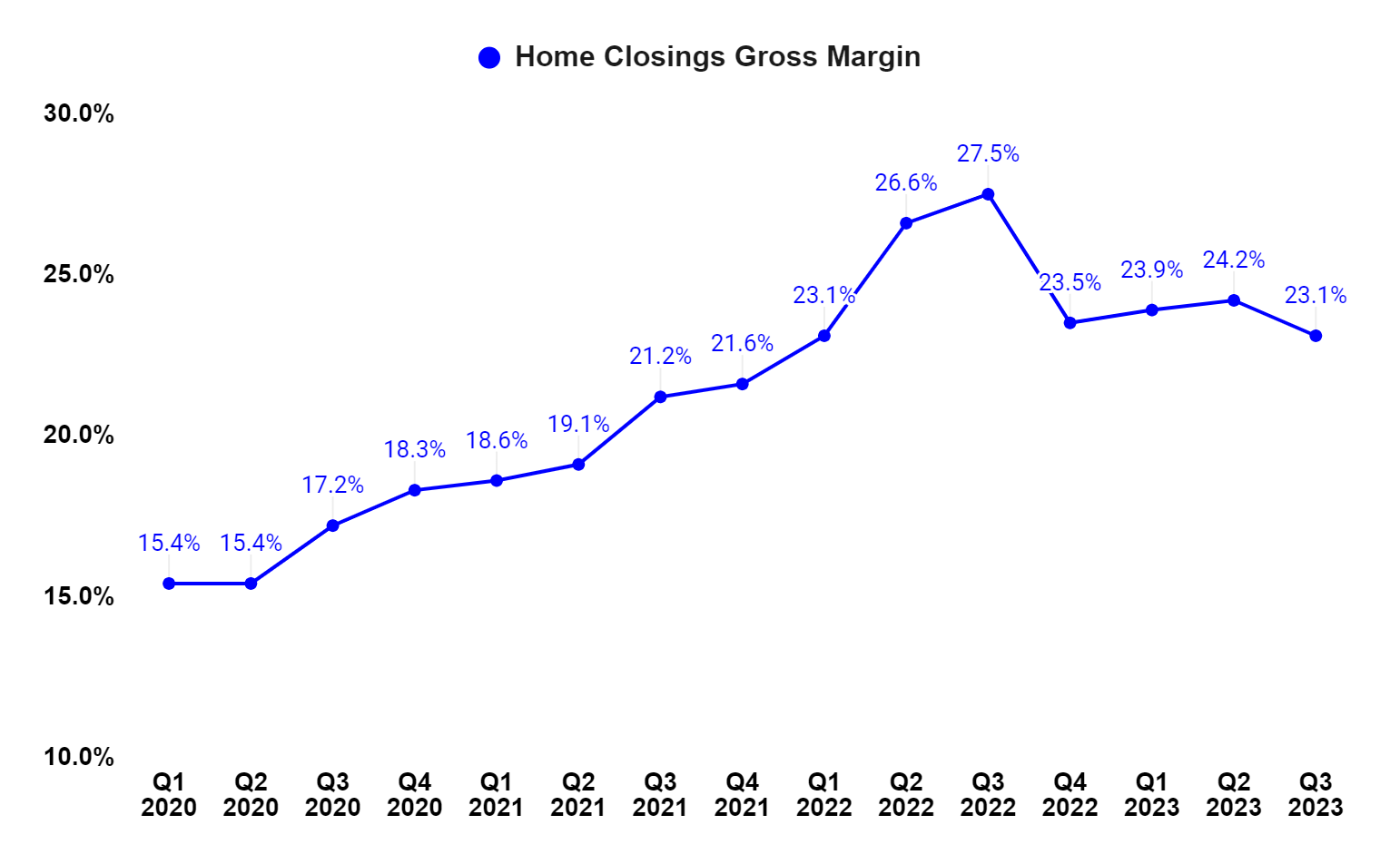

In Q3 FY23, the company saw a 440 bps decline in its home closings gross margin to 23.1%. This decline was expected as margins are now normalizing after a very strong last couple of years. However, if we adjust for inventory write-downs, the company's adjusted gross margins were 23.9% which was better than management guidance indicating good execution.

{kind=link}

TMHC’s Adjusted Home Closings Gross margin (Company Data, GS Analytics Research)

Looking forward, I believe the company’s gross margins should stabilize in the low 20s which is above the high-teen levels it had prior to the pandemic. The company has done a good job streamlining its operations in recent years and while part of the margin increase post-pandemic was due to an extraordinarily strong market and real estate price appreciation, which is now normalizing, a good part of the improvement was also due to structural cost reduction like floorplan, rationalization, SKU reduction which should continue to benefit the company.

Valuation and Conclusion

The company ended the last quarter with a Book value of $46.78 per share and a Tangible Book value of $41.84 per share. If we look at the current consensus EPS estimates, the company is expected to post an EPS of $1.79 in Q4 2023 and $6.60 in FY24. So, the company’s Tangible book value at the end of next year should be close to $50.23 (=$41.84 + $1.79 + $6.60).

If we assume the P/TBV of 1x, a valuation level it is currently trading at, the stock could reach $50.23 by the end of next year which implies a high teen upside. Given we are close to the bottom of the cycle and the valuation is reasonable, I am upgrading my rating to a buy.

For further details see:

Taylor Morrison: Reasonable Valuation And Approaching Bottom (Rating Upgrade)