TMHC - Taylor Morrison: Signs Of Improvement Are Emerging

2023-08-31 13:20:40 ET

Summary

- Taylor Morrison's stock has experienced significant upside, despite mixed financial results, indicating that the worst may be behind the company.

- The company's revenue remained robust, but net income and profitability metrics worsened due to increased costs.

- The number of new orders has increased, suggesting a positive long-term outlook for the company, and the stock is cheap compared to similar firms.

When you make an investment, you should almost always expect that investment to take a while to truly pay off. There are exceptions, mostly involving special situations. But if you are a traditional investor who focuses on the long run, it really is best to plan to hold an investment for years. Sometimes, however, we end up lucky and the firm that we buy into ends up experiencing significant upside rather quickly. One example of this that I could point to involves homebuilder Taylor Morrison ( TMHC ). Even though the company has seen some mixed financial results recently, shares have shot up, largely in response to signs that the worst for the business is now behind it. Even though the stock has risen materially, shares still look cheap, both on an absolute basis and relative to similar firms. So while it might be tempting to cash out and look for opportunities elsewhere, I would argue that further upside likely exists from here.

Mixed performance and signs of a turnaround

Back in April of this year, I wrote a bullish article regarding Taylor Morrison. At that time, I acknowledged that cracks were definitely forming in the housing market. Higher interest rates and inflationary pressures led to significant decreases in backlog. Given that difficult times like this could persist for years, I can understand why some investors might have shied away from an opportunity like this. However, the stock looked incredibly cheap, and I knew that the long-term picture for the homebuilding market made the company a favorable risk to reward prospect for those willing to hold on for the long haul. This led me to rate the company a 'buy' to reflect my view at the time that shares should outperform the broader market for the foreseeable future. Since then, that is exactly what has happened. The stock is up 23.3% at a time when the S&P 500 has jumped 7.9%.

{kind=link}

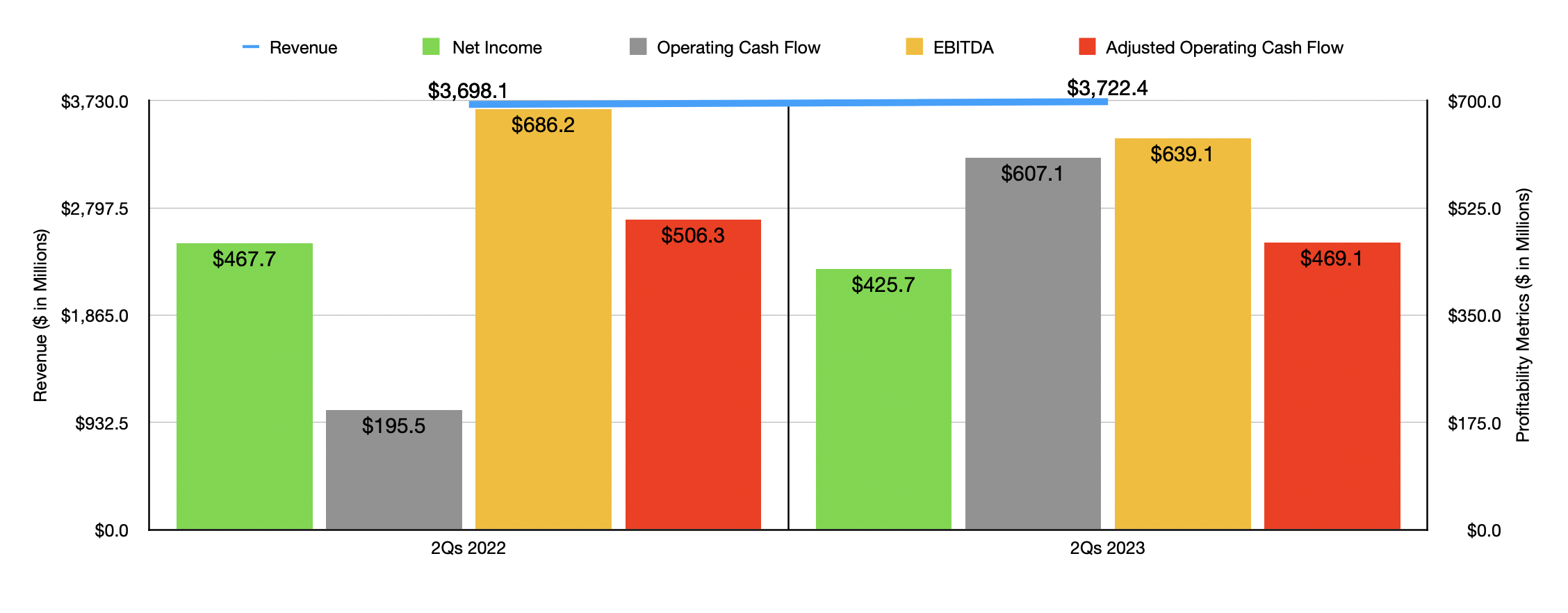

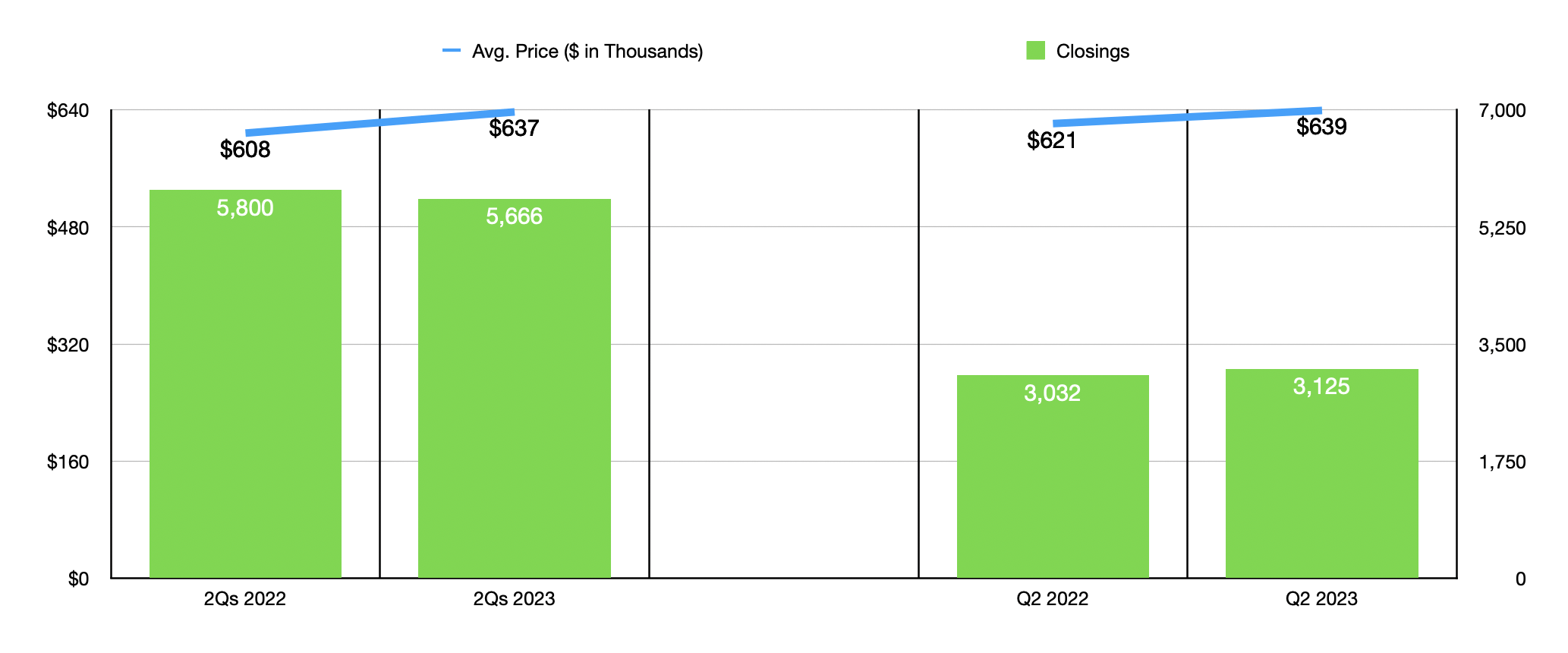

Since the publication of that article, financial data covering two additional fiscal quarters has come out. These quarters covered the first and second quarters of the 2023 fiscal year. During this time, the revenue picture for the company remained robust. Sales inched up from $3.70 billion to $3.72 billion for the first half of this year relative to the same time last year. Even though the number of home closings the company reported dropped from 5,800 to 5,666, it benefited from the average closing price climbing from $608,000 to $637,000.

{kind=link}

Bottom line results were not as appealing. In fact, the company experienced some weakness during this time. Net income, for instance, declined from $467.7 million in the first half of 2022 to $425.7 million in the first half of this year. Even though revenue increased, the company saw a drop in profits, in large part because of a decline in its home closings gross margin from 25% to 24%. Although this may not seem like a huge disparity, when applied to the revenue reported for the first half of this year, it works out to $37.2 million in missed profits on a pre-tax basis. Nearly as painful was an increase in the sales, commissions, and other marketing costs of the company in relation to sales. This expanded from 5.3% to 5.7%, mostly because of higher external commissions costs and increased advertising costs as management aimed to draw in buyers. There were other factors as well, including some that helped the company. But for the most part, the changes the business experienced on the cost side were negative.

{kind=link}

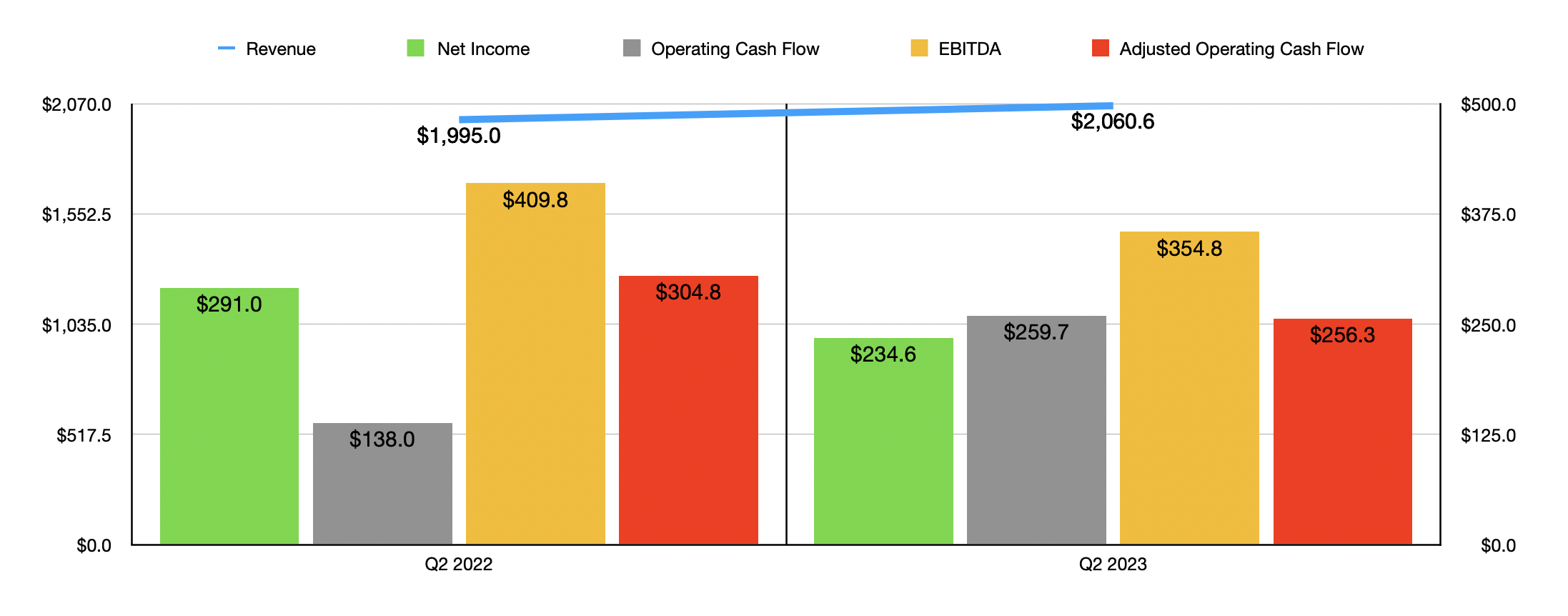

Unfortunately, this resulted in the other profitability metrics for the company also worsening. Operating cash flow was the exception, skyrocketing from $195.5 million to $607.1 million. But if we adjust for changes in working capital, we get a decrease from $506.3 million to $469.1 million. Over that same window of time, EBITDA also worsened, dropping from $686.2 million to $639.1 million. For context, I also provided, in the chart above, financial performance figures for the most recent quarter on its own. This shows many of the same trends for revenue and profits. So it is clear to me that this is an ongoing situation for the enterprise.

All of this is interesting to see, and it does paint a picture of some stresses facing the company. However, there is additional data that gives us a clear picture. First, I should start with what looks like really bad news. And this is that the backlog for the company has fallen rather significantly over the past year. At the end of the second quarter of 2022, Taylor Morrison had a backlog totaling 8,922 homes. By the end of the second quarter of this year, that figure had dropped to 6,165. At the same time, the average selling price of a property in backlog fell from $684,000 to $664,000.

{kind=link}

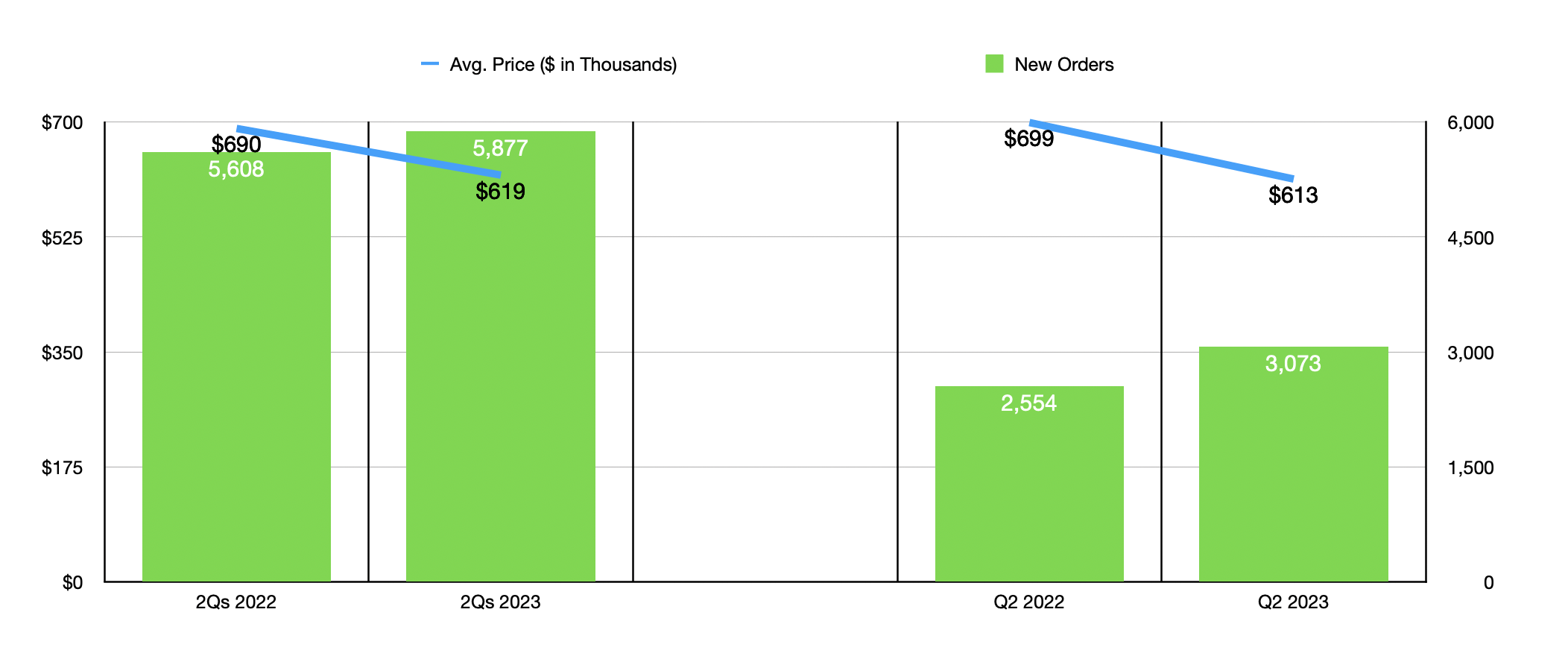

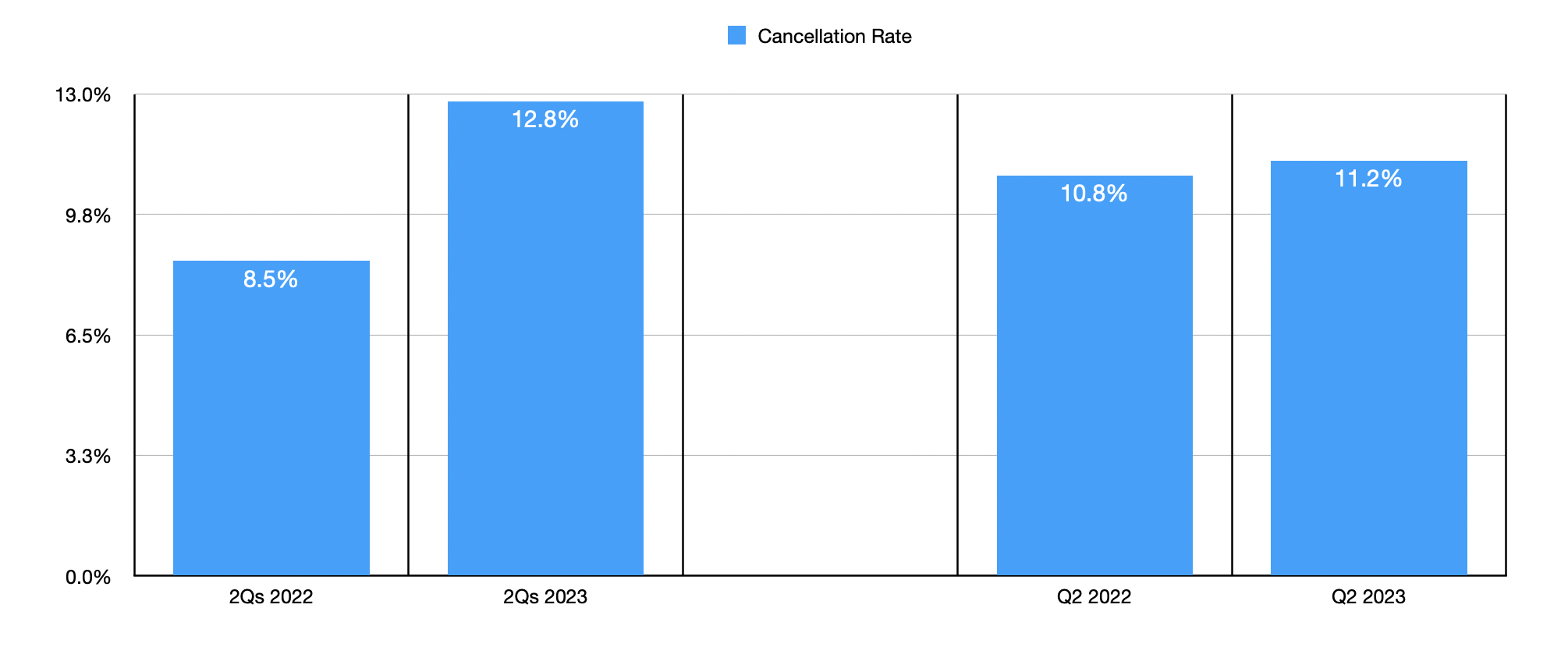

Worked out in a vacuum, this looks painful. However, there is one leading indicator that suggests that the worst for the company is behind it. And this involves the number of new orders that the company has booked. In the first half of this year, the company saw net new orders totaling 5,877 homes. That's up from the 5,608 net new orders experienced the same time last year. Orders were particularly strong in the second quarter, totaling 3,073 compared to the 2,554 reported for the second quarter of 2022. But this is not to say that everything on this front is great. As you can see in the chart above, the average price of a property that was ordered has dropped year over year. And that drop has been rather substantial. On top of this, as the chart below illustrates, cancellation rates are still higher than they were at the same time last year. So the business is not completely out of the woods yet.

{kind=link}

When you add together the good and the bad regarding Taylor Morrison, you have a company that is showing that the near future might not be as appealing as the recent past has been. Management has even said as much. For the current fiscal year, they are forecasting closings of 11,000 homes. That is up from the 12,647 reported for 2022. But the improvement in net new orders, particularly in the most recent quarter, is encouraging. It suggests that the longer-term outlook for our prospect is positive. But this is not the only reason why I remain bullish on this stock. If we annualize financial results experienced so far for the year, we would get net profits for 2023 of $958.3 million. Adjusted operating cash flow should be around $1.19 billion, while EBITDA should be about $1.52 billion.

{kind=link}

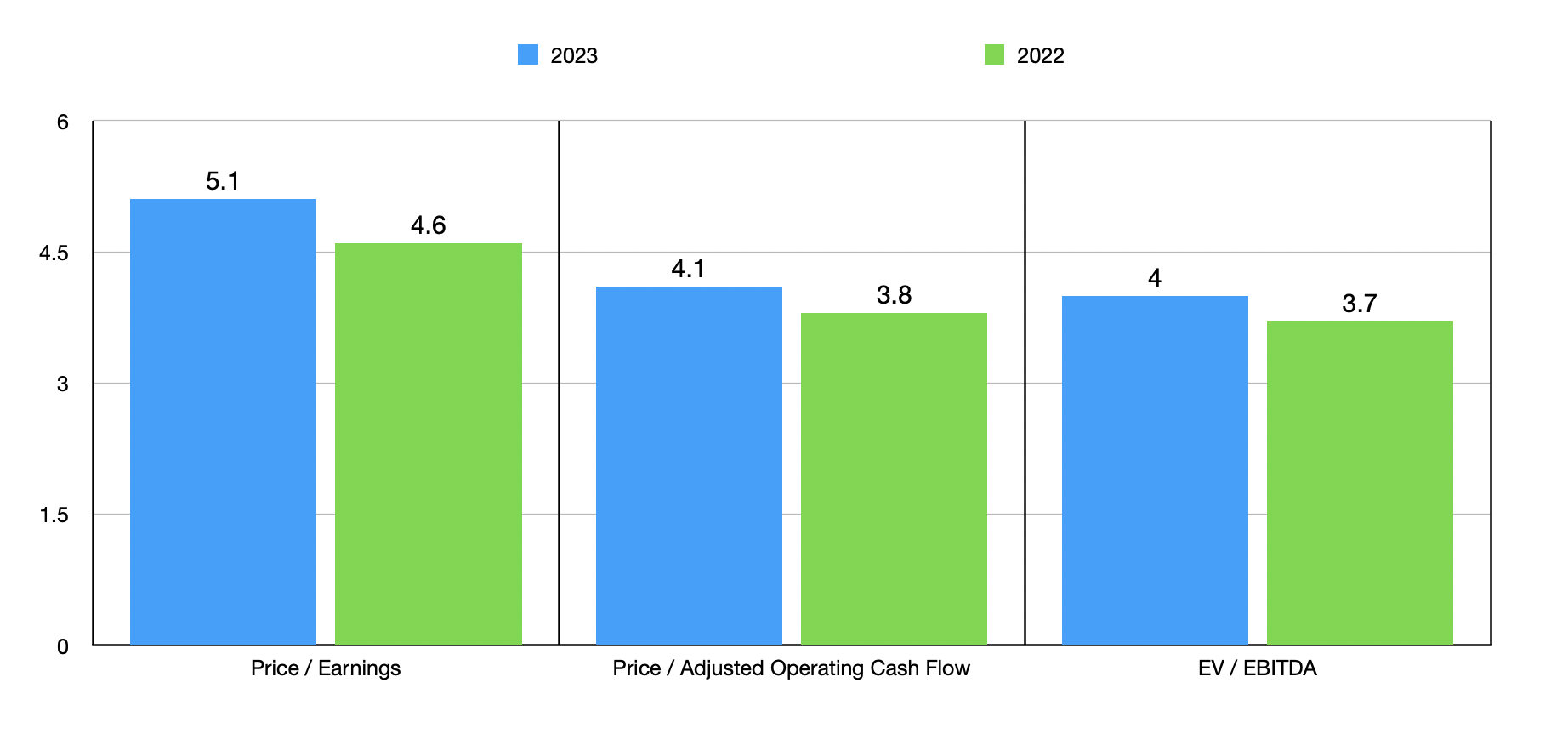

In the chart above, I took these figures and valued the company on a forward basis. I also valued it using data from 2022. On an absolute basis, the stock looks cheap either way. Then, in the table below, I compared our prospects against five similar firms. On a price to earnings basis, only one of the firms was cheaper than it. On a price to operating cash flow basis, two of the five were cheaper. And when it comes to the EV to EBITDA approach, I saw that Taylor Morrison ended up being the cheapest of the group.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Taylor Morrison |

| 5.1 |

| 4.1 |

| 4.0 |

| Legacy Housing Corporation ( LEGH ) |

| 8.0 |

| 44.3 |

| 6.2 |

| Meritage Homes ( MTH ) |

| 5.9 |

| 5.1 |

| 4.4 |

| Century Communities ( CCS ) |

| 7.5 |

| 4.2 |

| 7.5 |

| Beazer Homes USA ( BZH ) |

| 4.5 |

| 2.5 |

| 6.6 |

| KB Home ( KBH ) |

| 5.5 |

| 3.7 |

| 4.9 |

Takeaway

At this moment, we seem to be at something of an inflection point. The market still has some pain ahead for it. However, shares of Taylor Morrison look incredibly cheap, both on an absolute basis and relative to similar firms. Add on top of this the recent strength in net new orders, and I would make the case that additional upside for shareholders is not out of the question at this time. Because of all of this, I do still believe that a 'buy' rating is appropriate at this time.

For further details see:

Taylor Morrison: Signs Of Improvement Are Emerging