TWODF - Taylor Wimpey: Analysis Of The U.K. Housing Market

2023-10-03 23:49:18 ET

Summary

- Taylor Wimpey is one of the leading homebuilders in the UK with a large portfolio of land ready for development.

- The UK government's support for building due to supply and demand disparity is expected to drive long-term demand for homes.

- Taylor Wimpey is currently facing challenges with high interest rates and a decline in home sales, making it vulnerable compared to its peers.

- The UK is less a less attractive investment proposition, and the lasting impact of the current economic conditions remain uncertain, but we maintain a bullish view.

- We suggest investors remain patient, monitoring the performance of the peer group for early signs of an improvement in performance.

Investment thesis

Our current investment thesis is:

- TW is one of the leading homebuilders in the UK, with a large portfolio of land across the UK, primed to be built on in the coming years.

- The UK Government is very encouraging of building, owing to the supply and demand disparity in the market. We expect demand to outstrip supply over an extended period long term.

- TW is facing significant headwinds currently, however, with high interest rates in the UK and the threat of further hikes contributing to a rapid deterioration in home sales.

- TW looks overly exposed to this relative to peers, implying investors would do well to be patient until conditions improve.

Company description

Taylor Wimpey ( TWODF ) is a UK-based residential property developer and homebuilder. With a rich history dating back to 1880, the company is one of the largest homebuilders in the UK, operating across England, Scotland, and Wales. Taylor Wimpey primarily focuses on building houses, apartments, and other residential properties for various customer segments.

Share price

TW's share price has lost value in the decade, primarily due to the decline since 2021, with strong distributions offsetting this. TW's dividend payments are a reflection of its cash-earning potential and business model.

Financial analysis

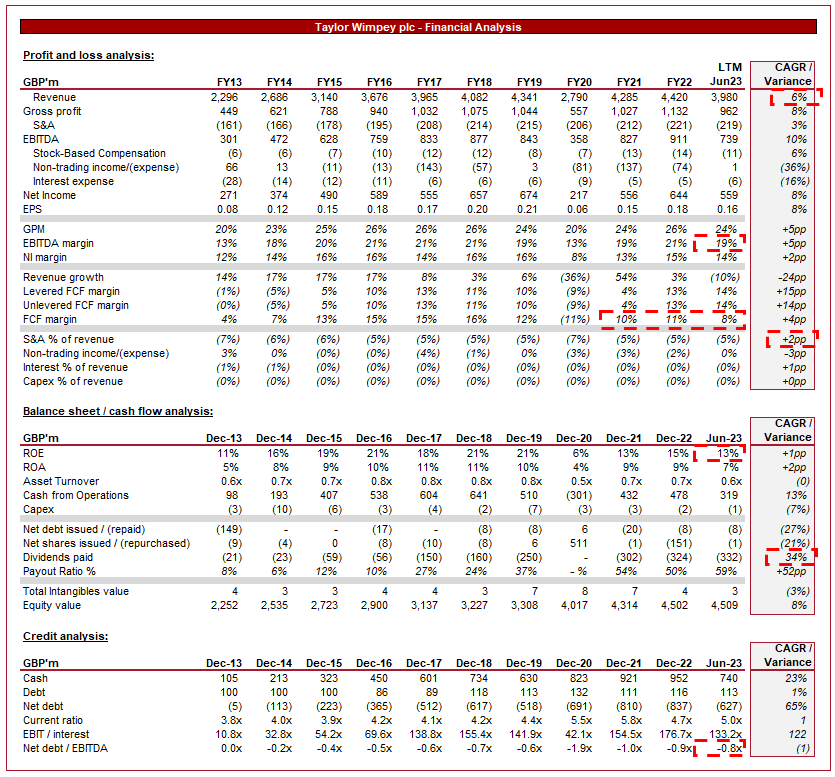

Taylor Wimpey financials (Capital IQ)

{kind=link}

Presented above is TW's financial performance in the last decade.

Revenue & Commercial Factors

TW has achieved healthy revenue growth in the last 10 years, with a CAGR of 6% despite the recent decline. During this period, TW has consistently achieved good growth YoY, reflecting the quality of its business model.

Business Model

TW's business model revolves around the acquisition of land, planning, and development of residential properties. The company sells these properties to homebuyers, both private and affordable housing. TW's revenue is primarily generated through the sale of completed residential units.

For this reason, the identification and acquisition of land for residential development is critical. This involves assessing potential sites, obtaining planning permissions, and managing the legal and regulatory aspects of land acquisition. Within the UK, there are strict planning rules in place to protect heritage sites, areas of nature, and other culturally important locations. Overarchingly, however, the dynamics of the UK housing market (which we will discuss later) means the UK Government is highly encouraging of Homebuilding.

TW designs and constructs a wide range of homes, including apartments, townhouses, and detached houses. This allows the business to reach a broad range of consumers, maximizing its selling potential and reducing exposure to any single segment.

TW has a long-standing presence in the UK property market, which gives it brand recognition and customer trust. Based on its size, it is only rivaled by a small number of other firms, most of whom have a similar reputation.

TW emphasizes high-quality construction and energy-efficient features to meet modern living standards. The company generally scores well for quality , although lags behind some of its similarly sized peers. There has been an undertone of criticism for UK builders, primarily because they have been unable to match the quality of those pre-70s. A quick google search will have you convinced a property built in 1900 is superior in quality today than a new build (and they are likely correct). This said, new builds are improving following this criticism, and offer consumers convenience, a smooth buying process, a long warranty, and are ready to live in.

The company operates across various regions in the UK, strategically selecting locations with high demand and growth potential for residential properties. This approach supports a reduction in exposure to any single region, allowing reducing the risk of a decline in demand or inability to sell homes. Unlike many of its peers, however, the business also builds in Spain (Tourist hotspots for Brits), marginally softening its reliance on the UK.

The company aims to secure a significant portion of its sales before construction is completed, which provides more predictable revenue streams and reduces financial risks. For this reason, the business is somewhat "hedged" against downturns, as its costs are already covered by past earnings.

Economic conditions

The UK, similar to most of the Western world, has seen a rapid increase in inflation during 2021-2022, followed by a steady increase in interest rates to combat this. While the US has brought inflation down to below 5%, the UK and much of Europe have been less successful, primarily due to a greater reliance on importing Energy and Food.

Our expectation is for the current trend to continue, with inflation slowly declining MoM, but requiring further rate hikes to ensure this decline is sustainable. We are now expecting rates to peak at 5.5-6% in 2024, before beginning a decline quicker decline from there.

The impact on the housing market is substantial and we are already seeing the effects. UK house prices have declined at the sharpest rate in 14 years .

Tighter lending conditions during periods of high interest rates will limit the availability of mortgages for potential buyers. Further, high inflation and interest rates are reducing consumers' purchasing power, making it more challenging for potential homebuyers to be in a position to afford an acquisition.

This is a major issue for TW, with projects currently under construction facing a softening of demand. This will encourage greater negotiation by those seeking to purchase, forcing TW to accept a reduced amount.

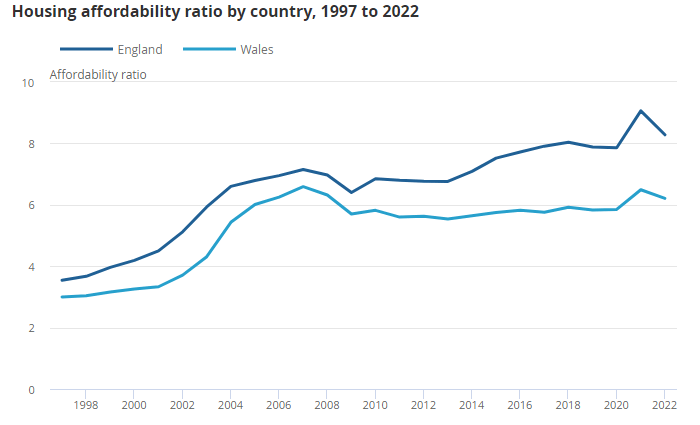

As the following illustrates, UK housing affordability has declined over time (increase in affordability ratio), with a significant bump during the GFC, and likely another which we are currently experiencing. This will act to price more consumers out of the housing market and into the rental industry.

Affordability ratio (Office of National Statistics)

{kind=link}

This begs the question of what the wider impact will be in the coming years. Consumers are facing an unprecedented deterioration of their finances, with no clear route to reprieve. Many individuals will see a permanent decline in financial standing, essentially pricing them out of a new build purchase and setting them back years. UK Consumer Confidence illustrates this, currently at pandemic low levels.

During times of high inflation, the costs of raw materials, labor, and other inputs for construction can increase significantly. TW faces challenges in managing rising construction costs in the medium term, likely impacting profit margins unless the increased costs can be passed on to buyers through higher property prices. This is usually what occurs during periods of inflation, however, the degree to which consumers are struggling means prices are unlikely to offset this.

Longer term outlook

The UK housing industry is unique in that it has performed modesty well for centuries. Most recently, the industry bounced back well from the GFC, especially impressive given the rapid rise it experienced (fueled by foreign money). Countries like Italy and Spain are still struggling with house prices over a decade later.

This inherent strength in the housing market is a reflection of two key factors. Firstly, and most simply, the UK is an incredibly attractive place to invest. Foreigners have been buying up properties, businesses, and anything they can get their hands on, with the promise of healthy returns and economic/legal safety. With Brexit, this has certainly softened but remains the case.

Secondly, the UK has a demand and supply imbalance. The UK is smaller than New Zealand in size (km2) while having a population of over 67 million (NZ has 5m). This naturally means the demand for housing is high, exacerbated by an aspirational culture of home ownership.

Given these two factors, we believe the housing industry is inherently safe. The current conditions are highly concerning, and will likely take an extended period to correct. This said, we are not bearish on the UK housing industry as the fundamentals are not going away.

TW faces competition from other UK-based residential property developers (which are listed later in this report). This somewhat restricts the earnings potential of the cohort, as they compete for land and development opportunities.

Margins

TW'S margins have been incredibly consistent over the historical period, and impressively so in the LTM, owing to the factor mentioned previously. TW will only invest in locations that are neutral or accretive for the wider business and competition means it is unlikely to materially outperform this (and thus see margin appreciation over time).

There is scope for technological development making the build process significantly quicker and cheaper, but it remains unclear when this will be possible at a mass market level.

We expect margins to contract in the near term, as inflationary cost pressures and a lack of demand force the business to conceding in negotiations.

H1 results

The key takeaways from the H1 results are:

- Revenue growth is down (21.2)% and OPM is down (6.0)ppts.

- Land acquisitions continue, although the business is far more selective. This is a positive development in our view, suggesting Management is not spooked by conditions.

- The average selling price of affordable housing is already down YoY, while Private is still up at 8.6%. Private completions are down (27.1)% while Affordable is down (23.4)%.

- Margins have declined due to build cost inflation exceeding house price inflation, increased marketing spending required, and reduced land prices.

- Expectations are for headwinds to continue.

These results are in line with our expectations. We forecast the business to end the year down (20)-(27)%, owing to the likelihood of a larger decline in H2 following further rate hikes in the UK.

Balance sheet & Cash Flows

TW's balance sheet remains robust, with a ND/EBITDA ratio of (0.8)x and a sufficiently large cash position to fund operations in the coming year assuming no sales.

Outlook

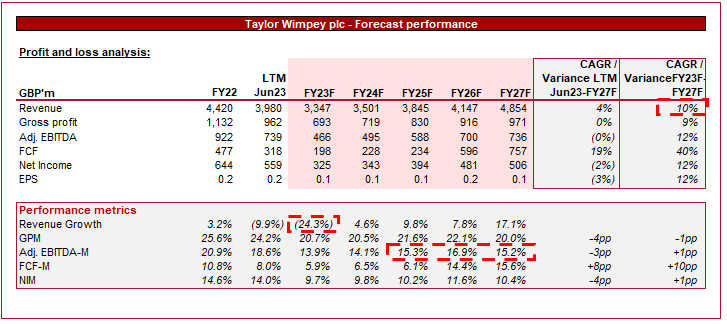

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a (24)% decline in FY23, followed by a 10% growth rate into FY27F. Margins are expected to materially decline, with a permanently lower level subsequently.

We broadly agree with these forecasts, although we believe MSD growth into FY27 is more reasonable.

Peer analysis

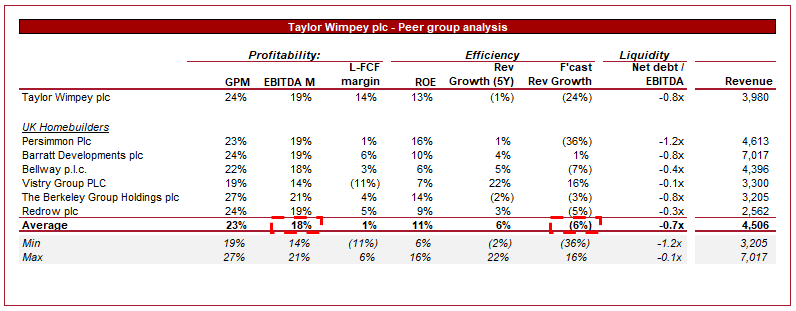

Peer analysis of Homebuilders (Capital IQ)

{kind=link}

Presented above is a comparison of TW to a cohort of its directly comparable peers, namely Persimmon ( PSMMY ), Barratt Developments ( BTDPF ), Bellway ( BLWYF ), Vistry ( BVHMF ), Berkeley ( BKGFY ), and Redrow ( RDWWF ).

Margins are relatively standardized across the peer group, with no material difference between the group. The movement in FCF is volatile, reflecting differing approaches to current conditions (TW has continued to invest in inventory).

Forecast growth suggests a strong weakness with TW, owing to its significant scale and core demographic. Declining earnings is the biggest obstacle currently, and TW is overly exposed.

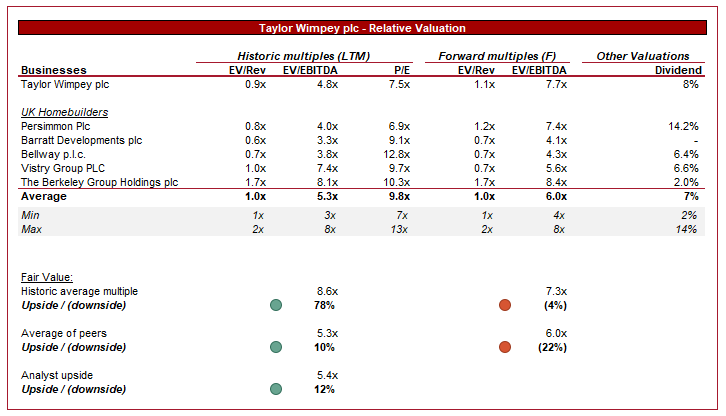

Valuation

{kind=link}

TW is currently trading at 5x LTM EBITDA and 7x NTM EBITDA.

On an LTM basis, TW looks incredibly attractive. The stock is trading at a discount while being positioned well relative to the group and has a good portfolio of land.

This view changes on a NTM basis. Given the decline the company is facing, the risk is that it quickly becomes overvalued. At a 4% discount to its peer group, but more importantly, facing a large decline in sales with an uncertain impact on margins, it is difficult to suggest there is upside at the current share price.

Final thoughts

The UK housing market is a modest investment choice in our view, particularly over an extended period of time. TW, among a cohort of a few leading developers, provides investors the ability to gain exposure to this industry.

We expect a difficult period in the coming 12-18 months and TW is highly exposed. We see sales declining further and margins tightening.

The performance beyond this should be good, however, to invest today feels premature.

For further details see:

Taylor Wimpey: Analysis Of The U.K. Housing Market