TWODF - Taylor Wimpey: Price Uptick Due

Summary

- Taylor Wimpey, one of the UK's most prominent house builders, has seen a big price slump this year.

- Considering its strong financials over the last 10 years, this looks like a stock market overreaction, even considering an impending recession.

- Its P/E is way below the long-term average and its dividend yield is high making a buy case for it.

Investing in a property developer like Taylor Wimpey (TWODY) when we have a cost of living crisis at hand and a recession looms right in front of our eyes sounds as a contrarian idea as they come. But there are good reasons to buy its ADRs. Consider this.

The company is one of the most prominent house builders in the UK, whose stock price has fallen by half in 2022. It's now trading at near all-time lows. Now, a drop in price is understandable. It's a cyclical company and we are near the trough of the business cycle. But all-time-lows? That looks like a stock market overreaction. Moreover, it has a robust dividend yield of 9.2% and its dividend payout ratio isn't among the worst at 53% either.

Robust long-term financials

Taylor Wimpey looks even more attractive when its performance is considered. In the last decade, it has more than doubled its revenues and its net profits. Its revenues have grown in all years except 2020, the year of COVID-19, which was an atypical disruption that stopped both construction work and sent the economy into a recession. The company has also been consistently profitable over the past 10 years, though its profits did drop in 2020 and in 2017. In 2020 it was impacted by the pandemic and in 2017 by an exceptional charge. As far as the income statement goes then, Taylor Wimpey has been in good health.

Base effect impacts 2022 revenues

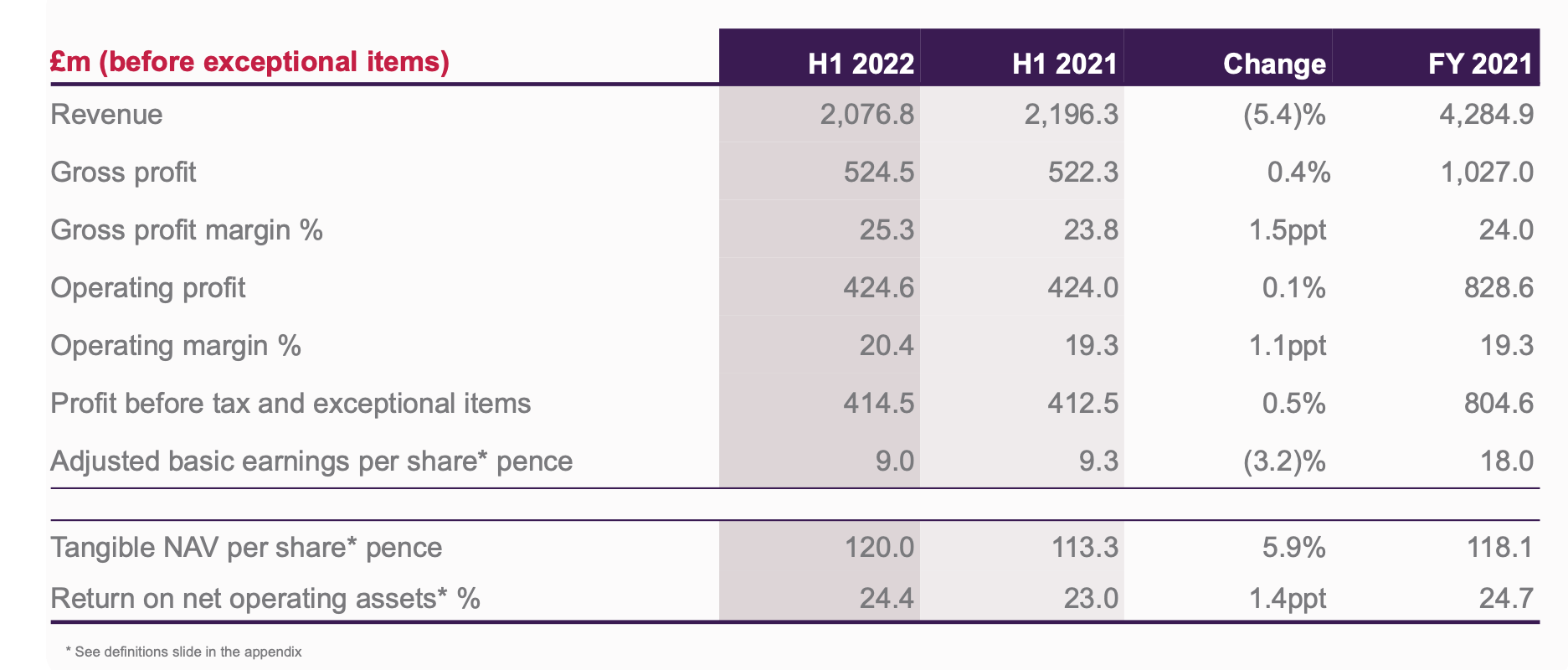

This brings me to the current year. Detailed numbers are available for only the first half of the year so far. Revenues declined by 5.4% year-on-year (YoY), which is disappointing on the face of it. But there's a good reason for this. Last year's comparable revenues were bumped up significantly by the much-needed sugar high of fiscal stimulus. The UK government slashed stamp duty on house purchases resulting in a dizzying rise in housing demand and house prices. Compared to the pre-pandemic comparable period in 2019, Taylor Wimpey's revenues are still up by 20%. Moreover, its net profits are up by 10.5% YoY despite the decline in revenues.

{kind=link}

However, the second half of the year might be worse considering that interest rates have been rising and inflation has stayed firm too. The effects of the rollback in stamp duty holiday will also continue to play their part. Indeed its trading update does continue to show a slowing down in sales from last year. The company says this is down to "customer response to heightened levels of economic uncertainty". It still reiterates though that it's "on track to deliver full-year operating profit in line with market expectations". The number for operating profit expected is a record £922 million and a healthy 13% YoY increase.

Undervalued right now

Just the robust earnings forecasts, in my view, make a case for an eventual uptick in its price from current numbers. That its earnings aren't adequately reflected in its price, is evident from the fact that its current price-to-earnings (P/E) ratio stands at 6.5x, which is far lower than the 11.5x median level for the last 13 years. Just to get to this median P/E, its earnings will have to drop by almost 44%, the likes of which haven't been seen in the past 10 years, save 2020 when the EPS dropped by 66%. And next year is likely to be a much smaller recession than seen during the pandemic, so it's unlikely that the fall in earnings will be quite as dramatic.

Why it can sustain earnings

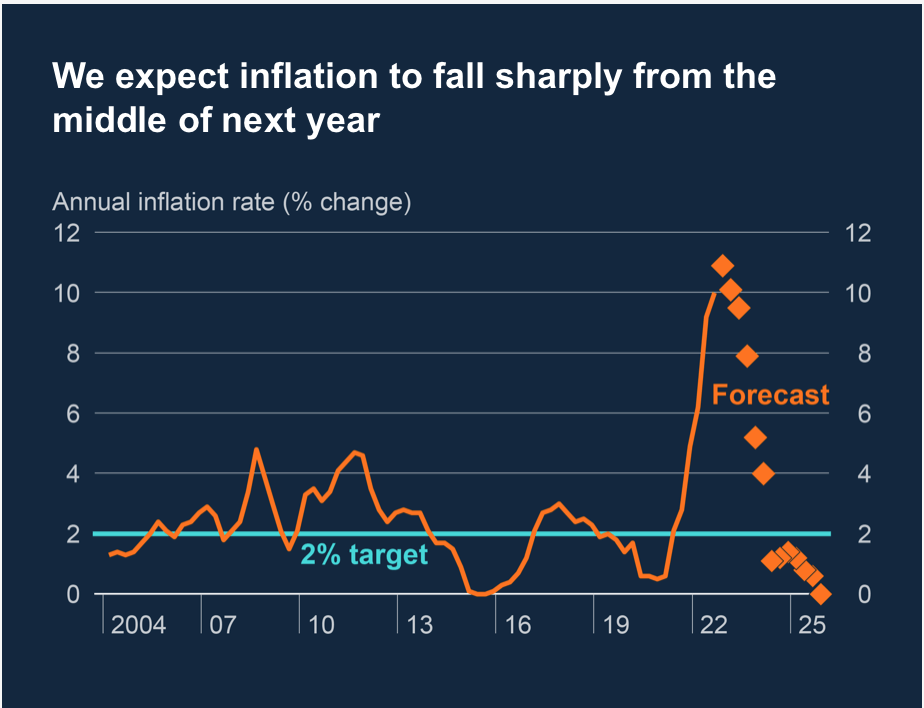

Another reason Taylor Wimpey could sustain its earnings is a come-off in inflation. The company has pointed to a rise in both material and labour costs. Its build cost inflation was in the 9-10% range when it reported its interim results. It's unlikely to have fallen, if anything, it's most likely higher going by the state of inflation. The key reason it has been able to do so this year is rising house prices. According to the Office of Budget Responsibility [OBR], 2022 will close with a 10.7% increase in house prices. This has more than made up for the cost inflation it currently faces.

However, the cushion of rising house prices is no longer expected to provide support in 2023, with an expectation of a small decline of 1.2%. This could impact revenues for another year. But inflation is also expected to come off. The OBR predicts that the UK's headline inflation is expected to fall to 7.4% in 2023. The Bank of England is hopeful of a fall in CPI inflation next year too.

{kind=link}

For context, at present, it stands at 10.7%. In other words, there could actually be a sharper decline in inflation compared to house prices. This could provide some relief on the cost inflation front, which more than makes up for the fall in house prices, making a case for sustained earnings. In any case, Taylor Wimpey's operating margins aren't too bad historically. On average, they have been at 17.5% over the last decade. While there have been fluctuations, they have never dropped below 10%.

The risks

Interest rates could still stay elevated, though. Rate increases are expected to halt by the first quarter of next year, with the Bank of England's policy rate at 4.5% according to Nomura, but will stay at these levels for the remainder of the year. Along with the expected recession next year, demand for housing could weaken. While the economy is expected to be down and out only for a relatively limited amount of time, how things actually play out remains to be seen.

What next?

All in all, there's a case to buy Taylor Wimpey now considering how much it has fallen. Even accounting for next year's recession, expected decline in house prices and high-interest rates. It has a history of strong financials and has consistently reported profits even at the worst of times. Considering that, its P/E is rather low and is likely to remain below its long-term average even if the company's earnings fall in 2023.

For further details see:

Taylor Wimpey: Price Uptick Due