TWODF - Taylor Wimpey: Strong Dividend Yield And Price Growth Still Possible

2023-06-28 15:55:02 ET

Summary

- Taylor Wimpey's stock price has risen by 21.4% since December last year, despite economic uncertainties.

- The company's market valuations are attractive, with a TTM price-to-earnings (P/E) ratio of 6x, which is lower than its peers.

- Risks to consider include the potential for a UK recession and the impact of inflation on interest rates.

- Despite these risks, I retain a Buy rating due to its strong performance and attractive market multiples.

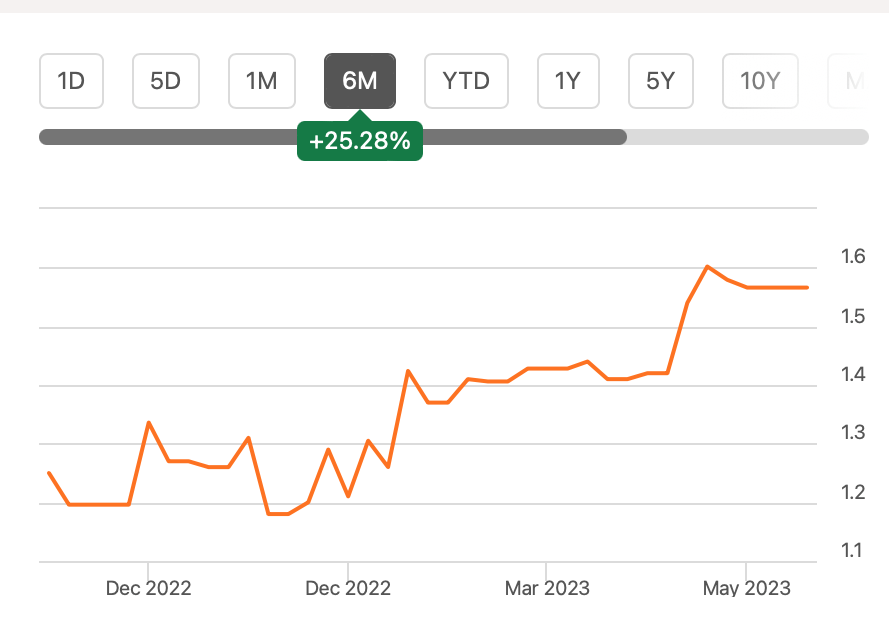

Sometimes a worthy stock's price falls so low, there is no way but up. And that is exactly what's happened with one of the UK's house builders Taylor Wimpey (TWODF). Since I last rated it a Buy in December last year, its price is up 21.4%. This is despite all the gloom and doom surrounding the economy. For context, the FTSE 100 of the London Stock Exchange, the home of its main listing, has gone nowhere during this time.

Price Returns (Source: Seeking Alpha)

{kind=link}

But an over 20% increase is a fair bit, prompting the next natural question. What is next for TWODF? Is it still a Buy or has it risen enough to prompt a Hold or even a Sell? Here I take a closer look at its fundamentals, its market valuations and the macroeconomic risks to figure out what's next for it.

Weakness visible, but still relatively strong

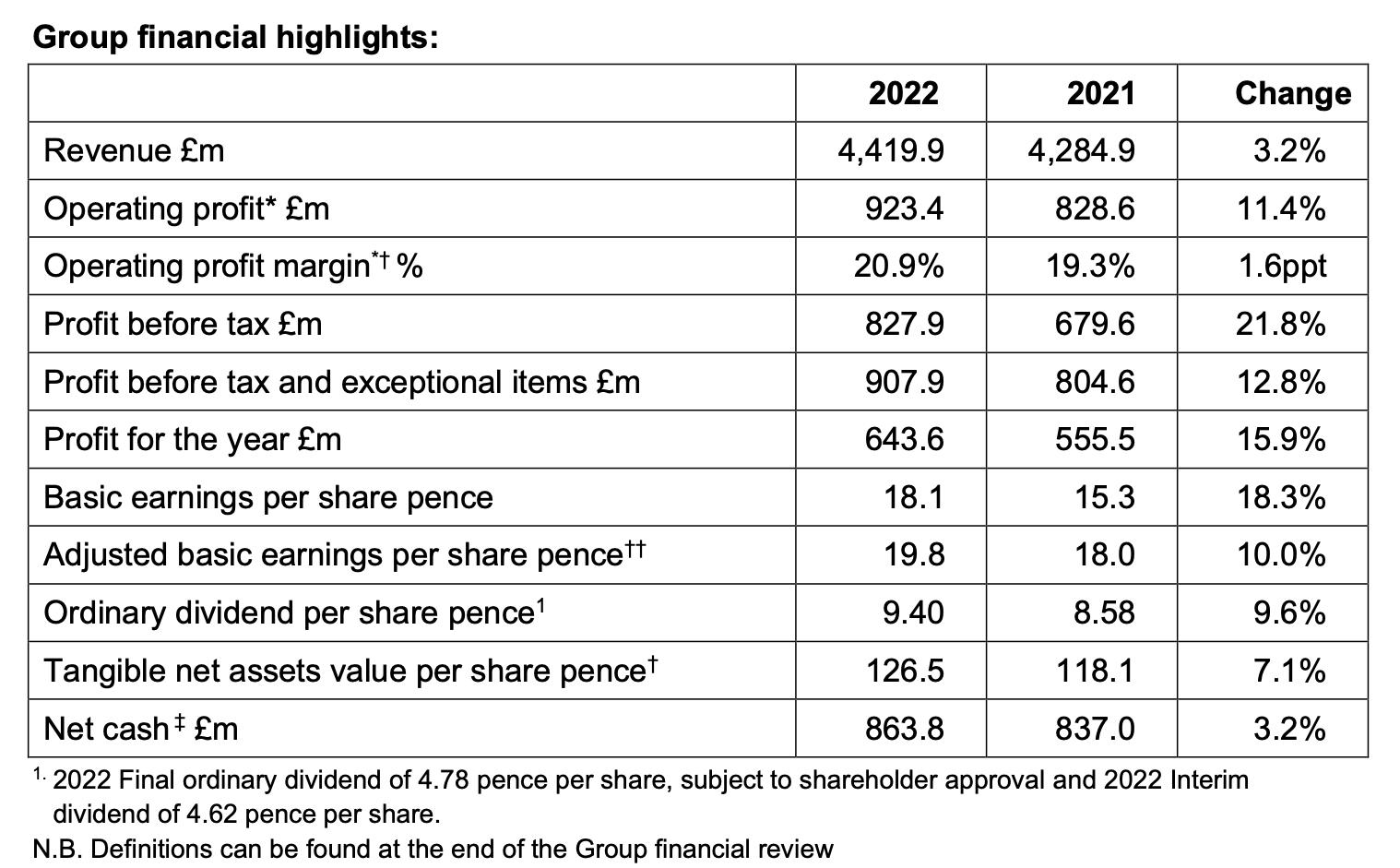

First, its fundamentals. Since December, the company has released two updates, which are its full year 2022 figures and its trading update for the period up to April 23, 2023. To start with, all things considered, its full year results weren't bad at all. The company managed to grow its revenues, by 3.2% year-on-year (YoY) and profit by 15.9%. It even managed to increase its gross margin to 25.6% in 2022 from 24% in 2021.

{kind=link}

Its trading update does show a slowing down in momentum, though. The company's net private net sales rate were at to 0.75 in 2023, up to April, which is down from 0.97 last year. There has also been a marginal increase in cancellation rates to 15% from 14% last year.

Interestingly, however, there are indications of a recent pickup too. It revealed the sales rate figures for up to the week ending February 26, 2023, when it announced its full year results. At the time, the number was at 0.62. This means, that the months of March and April actually showed an improvement in the housing market.

Encouragingly, it also reports signs of a come off in cost inflation from the 9-10% it saw up to March. Some improvements were to be expected going by some signs of cooling off in the UK's headline inflation as well as forecasts for a further decrease through 2023. It might also bode well for the company's profits despite the likely weakness in revenues this year.

That said, Taylor Wimpey is expectedly quite muted in its outlook for the year. It's working off the assumption that the sales rate range will be at 0.5 to 0.7 in 2023. In other words, it believes that the latest improvement in the rate will not last. In fact, a fair softening is to be expected.

Compelling valuations

TWODF's market valuations, however, still look attractive. Its trailing twelve-month price-to-earnings (P/E) ratio is at 6x, which compares rather favourably against its peers. Other UK house builders like Barratt Developments (BTDPF), Persimmon (PSMMF) and Berkeley Group Holdings (BKGFY), all have higher P/E ratios at 8.3x and 6.3x and 9.3x. Additionally, it is still trading way lower than its median P/E over the last 13 years of 11.05x . This alone suggests at least 30% upside to price and probably more.

This is not all. As a real estate company, a look at the tangible assets is instructive too. The company's tangible assets per share pence was at 126.5 in 2022. Compared to this, it was at a little over 100p at the last close on LSE, indicating an upside of 17.3%. The same, of course, applies, even when we consider its ADRs. In other words, however we slice it, a substantial price rise is indicated.

Dividends look good

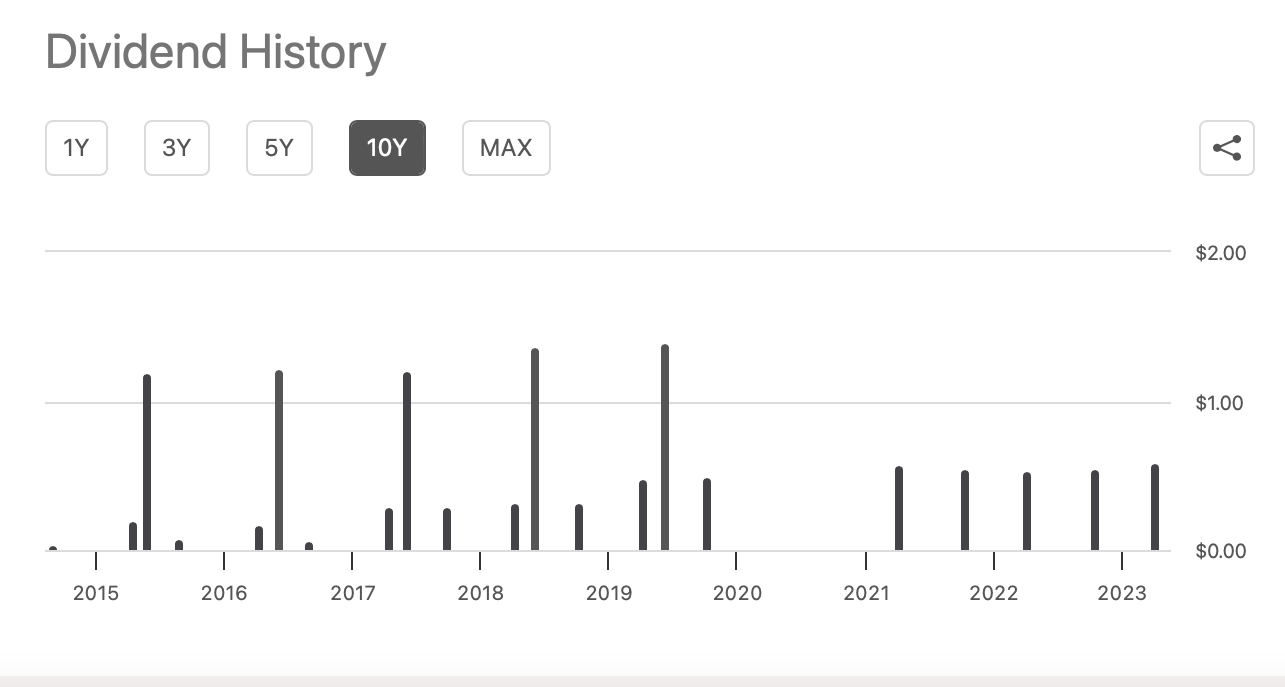

Additionally, there are dividends to consider too. Taylor Wimpey's TTM dividend yield is at a significant 8.6%. And while an inching up in its price will impact the yield, it is worth noting that the average dividend yield over the past is also quite nice at 6.2%.

For 2023 too, we can expect a healthy passive income from investing in it. The company has a policy of "paying out 7.5% of net assets, or at least £250 million, annually throughout the cycle". If we go with the net asset value for 2022, the expected dividend yield is a huge 9.3%. But even if it pays out £250 million as dividends, the yield is still a healthy 6.9%. In essence, with an at least 30% price rise and a 6.9% dividend yield, we are looking at total returns of around 37% on an investment in Taylor Wimpey over the next year.

Risks to consider

However, this will only play out if the forecasts for the macroeconomic situation turn out accurate. At present, the UK is expected to see a recession in 2023, before bouncing back the next year. Also, inflation is widely expected to come off, which in turn will slow down interest rate increases.

Things are not going entirely according to these forecasts however. On the plus side, the UK economy has avoided a recession so far. At the same time, inflation is slowing down, but still high and the Bank of England is left with little choice but to increase interest rates . This doesn't bode well for house prices, which have started coming off, and are even speculated to crash .

If things turn really sour for the housing sector, Taylor Wimpey can be impacted significantly. This of course isn't good news for either its price or its dividends. Despite what it says, it did suspend dividends during the pandemic. That was a particularly challenging time, but it is still something that I'd keep at the back of my mind.

{kind=link}

What next?

A more moderate perspective however, suggests that the UK economy will be in a much better place a year from now. Taylor Wimpey could see weakness in performance in the interim though. It is unlikely to be enough to stall either its price rise or from it paying out dividends, however. Its performance isn't the worst so far and its market multiples are pretty attractive. Not to mention its dividend yield, which looks good this year, no matter how we look at it. I am retaining my Buy rating on TWODF.

For further details see:

Taylor Wimpey: Strong Dividend Yield And Price Growth Still Possible