TRP - TC Energy: Deleveraging Is Needed To Bring Shares Back Into Favor

Summary

- TC Energy Corporation’s recent operational problems and overspending have caused its stock to underperform.

- The overspending is concerning given its implications for the company’s leverage.

- In light of TC Energy Corporation’s recent results and management’s plans to address leverage, we have lowered our price target for TC Energy shares.

Over the recent months, TC Energy Corporation ( TRP ) shares have sold off far more than its major Canadian midstream peers. Whereas Enbridge ( ENB ) shares declined by 6.3% from their high in June and Pembina ( PBA ) fell by 9.7%, TRP shares have fallen by 25.0%. Such an ugly relative performance begs the question of whether its shares have fallen into bargain territory and should be bought.

HFI Research

We recently downgraded our TC Energy Corporation valuation, and in light of recent events, we believe there was good reason for the selloff in its shares.

For one, the selloff puts TRP shares in line with their historical average and their long-term relationship with ENB and PBA. When TRP's shares traded at their 2022 highs above $75, they sported an EV/Adj. EBITDA multiple of more than 14-times, which was far above their historical averages and also above the historic trends relative to ENB and PBA.

The decline over recent months has brought TRP's EV/Adj. EBITDA multiple back to 11.6-times, versus 13.2-times for ENB and 10.5-times for PBA. The multiple now approximates its prior years' standing between ENB and PBA.

{kind=link}

The decline has also brought TRP's 6.2% dividend yield in line with ENB's 6.4% yield. It remains higher than PBA's 5.6% yield.

Reasons Behind TRP’s Selloff

TC Energy Corporation's selloff came in response to two developments. First, the company's recent operational issues and the risk that they imply wider problems; and second, TC Energy Corporation's weaker financial position relative to its peers.

On the operational front, TRP was forced to declare force majeure in two separate incidents. The first was on its Keystone Pipeline, and the second was on its Texas Eastern system. While it's too early to tell if these incidents signal a pattern of operational deficiencies, additional issues could be problematic, both for management's reputation and TRP's share price. The first rule of the midstream business is to maintain safe and high-integrity operations, and persistent operational difficulties are a sign of wider problems in the organization.

TC Energy Corporation’s operational issues may have brought it bad press, but as of yet we don’t view them as material to its long-term cash flow generation. However, if they continue, they could cause legal and regulatory issues while serving as an obstacle to the company’s ability to execute on its capital planning.

The second—and more problematic—issue that has hampered TRP's share performance is the company's constant outspending of its organic cash flow.

Outspending cash flow is not necessarily a problem, for instance when building long-lived, high-return assets. However, when the spending is aimed at long-lived assets that generate sub-par returns on capital over their lifespan, it becomes a growing problem over time.

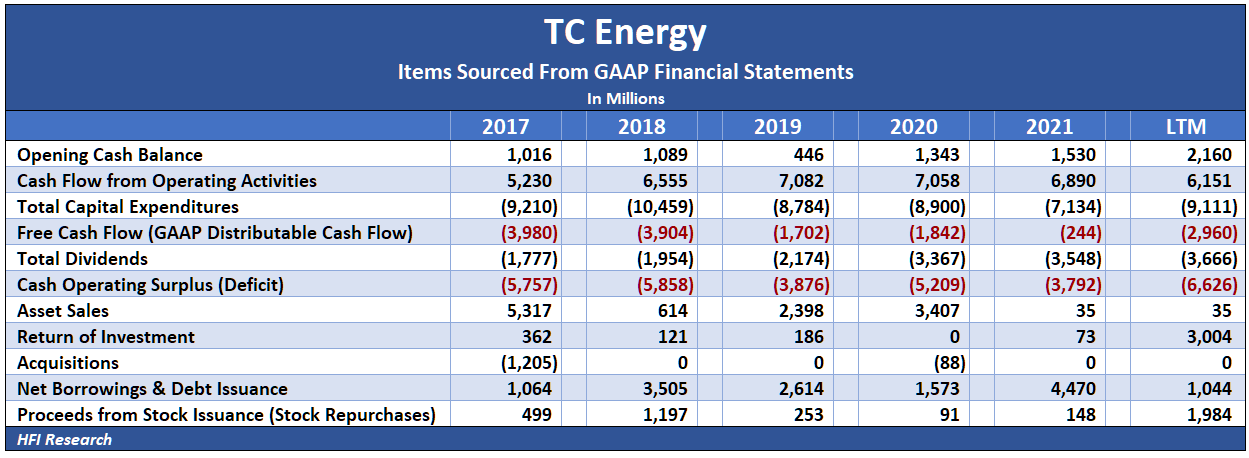

For years, TC Energy Corporation’s spending on growth projects has drowned out its free cash flow. After capex and dividends, it has run a massive cash flow deficit. It funded the deficit by selling assets, increasing debt, and issuing equity. The table below shows the longer-term cash flow picture.

{kind=link}

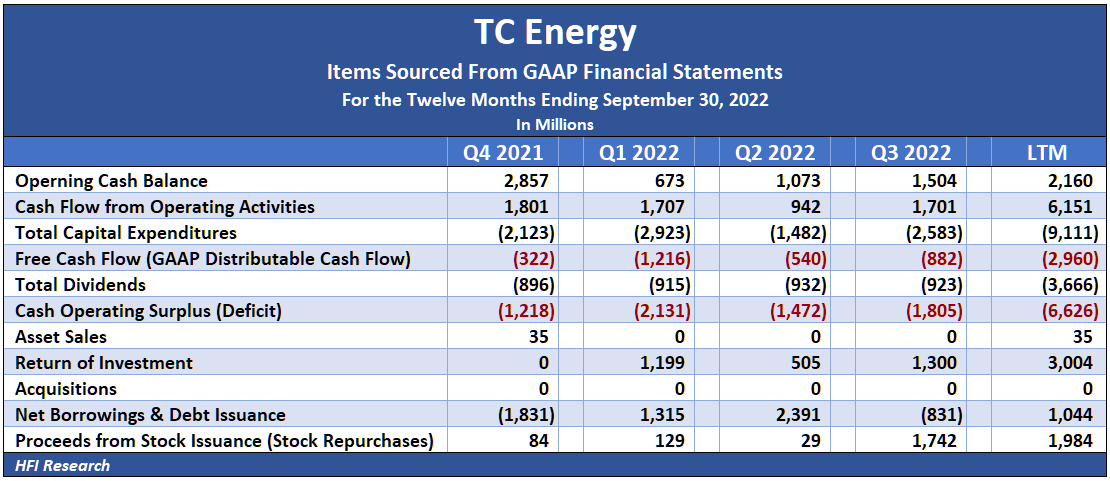

TRP's long-term cash flow trend remained intact over the last four quarters, as it outspent its $6.2 billion of operating cash flow by $6.6 billion. Over that timeframe, its total capex was a whopping $9.1 billion.

TC Energy Corporation funded its cash flow deficit through return-of-capital distributions from its equity investments, by taking on additional debt, and by issuing common equity.

{kind=link}

All this spending hasn’t increased TC Energy Corporation’s returns on capital. The following table shows the company’s long-term returns, which have declined in recent quarters and now hover around the average of its large midstream peers.

{kind=link}

TC Energy Corporation’s return on capital is now only slightly higher than its cost of capital. The company’s cost of long-term debt has been in the mid-4% range while its return on capital is consistently in the mid-single-digits. Management targets a 7-9% long-term after-tax internal rate of return on new projects, so we don't expect much of an upswing from current returns. Unless it can boost its returns, the company is at risk of higher interest expense eating into its returns for shareholders. This could be a growing problem as TC Energy Corporation refinances its debt at higher rates over the coming years.

The Consequences of Overspending

TRP has the luxury of operating primarily in natural gas and power generation, which are more stable than other energy sub-sectors. The underlying stability allows the company to take on a larger debt load than peers in more volatile operations.

But the stability doesn’t mean that leverage won’t become a problem if left unchecked. In recent years, increasing debt without a commensurate increase in Adjusted EBITDA has resulted in TRP’s debt-to-Adjusted EBITDA leverage ratio rising from 4.7-times in 2019 to an uncomfortably high 5.3-times over the past four quarters. Clearly, its years of overspending on projects that offer a middling return on capital are now catching up with it.

TRP's uncomfortable leverage position has increased the urgency among shareholders and management to rein in long-term debt. To this end, management recently pledged a divestiture program in which it plans to sell $5 billion of “non-core” assets. Given TRP's vast trove of assets—which span North America and include natural gas, crude oil, and power generation facilities—it shouldn’t have a problem identifying assets to sell. Management hopes to capitalize on high public market EBITDA sale multiples on its assets and the comparatively low cost of constructing new assets at a higher EBITDA yield.

At the same time, however, TRP’s spending will continue at high rates. Over the next few years, the company plans to sanction $5 billion in new growth projects. No doubt, the growth capex will consume a significant amount of proceeds from asset sales. When combined with maintenance capex requirements, total capex is likely to remain significantly in excess of cash inflows.

We’re not convinced this asset sale strategy amid continued outspending of organic cash flow is the best one for reducing leverage, lowering the risk to shareholders, and, ultimately, boosting the share price. While management believes it can build new assets at a mid-single-digit EBITDA multiple, its return on capital history suggests it has failed to do so in the past. Of course, this raises questions about the company's ability to arbitrage public and private midstream asset markets as management intends with its planned assets sales.

Slashing capex also won't be sufficient for deleveraging. In order to generate a cash flow surplus that can be allocated toward paying down debt, TRP would have to bring its capex and total dividends below the level of operating cash flow. But reducing capex to the level of cash flow after dividends would only leave $2.5 billion for total capex. Consider that over the past four quarters, TRP reported maintenance capex of $2.7 billion. Clearly, deleveraging will require more than slashing capex alone.

Given these challenges for deleveraging, we'll wait to see evidence of success before we consider rating TRP as a Buy.

A better path for TC Energy Corporation would be to bring down capex and sell assets in tandem. By doing so, TRP would be following many of its U.S. peers that have successfully rehabilitated their balance sheets over the past two years. Pursuing only spending reduction or asset sales would not be enough to convince the market that the company is serious about reducing leverage.

Valuing TRP Shares

Going forward, TC Energy Corporation's management is guiding for 5% to 7% Adjusted EBITDA growth in 2023. If it can refrain from issuing debt, the Adjusted EBITDA growth should marginally reduce leverage, though not enough to bring its leverage ratio below 5-times. Until it is in the mid-4-times range, leverage will remain too high.

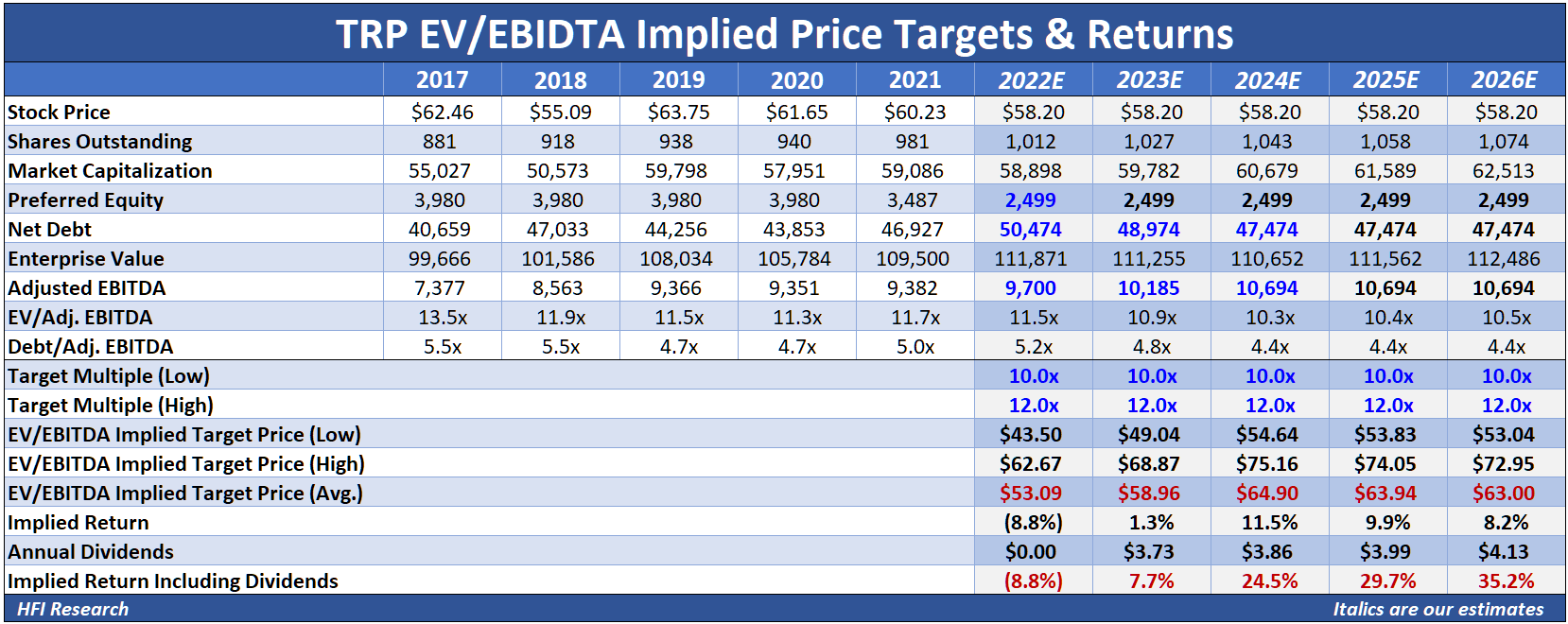

Our EV/EBITDA valuation assumes TRP’s Adjusted EBITDA increases by 5% over the next two years, which is the low end of management's guidance and accounts for the $5 billion of planned asset sales. We also assume the company pays down $1.5 billion of debt in both 2023 and 2024. We expect the amount of debt paydown to be less than the $5 billion of asset sales because part of the asset sale proceeds will be needed to fund growth capex. We also assume dividends increase by 3.5% annually.

{kind=link}

Our valuation shows the company achieving management’s 4.75-times debt to Adjusted EBITDA goal in 2024. It implies that the shares have 31.8% total return upside through 2026.

TRP's shares currently trade in our range of intrinsic value of $56 to $61, and close to our price target of $58.50. We’re therefore reiterating our Hold rating.

Conclusion

If TC Energy Corporation's management follows through on its deleveraging initiatives, the company's dividend will remain safe, and its shares offer upside over the next few years. If all goes well and TRP's leverage ratio falls to management's target below 4.75-times, its trading multiple may undergo a re-rating to a higher multiple, which would imply upside to our valuation.

For now, however, we reiterate our $58.50 price target and Hold rating for TC Energy Corporation until all is clear on the operations front and until we see evidence that management can deleverage the company.

For further details see:

TC Energy: Deleveraging Is Needed To Bring Shares Back Into Favor