TRP - TC Energy: High Yield And Exposure To The Energy Transition

2023-06-26 12:16:56 ET

Summary

- TC Energy Corporation is one of the largest midstream corporations in North America, boasting operations stretching from Canada to Mexico.

- The company makes the majority of its income from transporting and storing natural gas, which differentiates it from liquids-focused peers.

- The company promotes itself as a "sustainable energy" firm, but the majority of its growth spending is on natural gas pipelines.

- The company's debt level is a lot higher than we really want to see and is quite a bit higher than other Canadian midstream companies.

- The current 6.89% yield appears to be quite sustainable going forward.

TC Energy Corporation ( TRP ) is a Canadian midstream company that primarily transports natural gas throughout Canada and the United States. The company has also begun to get involved in the emerging renewable energy space, which is likely an attempt to please regulators and other Canadian government officials. Regardless, the company has long been one of the most well-known and followed companies for those investors that are seeking a high level of income from their portfolios. After all, the company yields an impressive 6.89% at the current stock price. This is very close to the kind of company that we normally discuss here at Energy Profits in Dividends.

As is usually the case with midstream companies, TC Energy Corporation has remarkably stable cash flows over time. This should position the company pretty well to provide a secure return in the currently bifurcated market . The company's focus on natural gas is also rather appealing considering that the fundamentals of this commodity are somewhat better than the fundamentals of crude oil. The company might, therefore, be worth investigating further.

About TC Energy Corporation

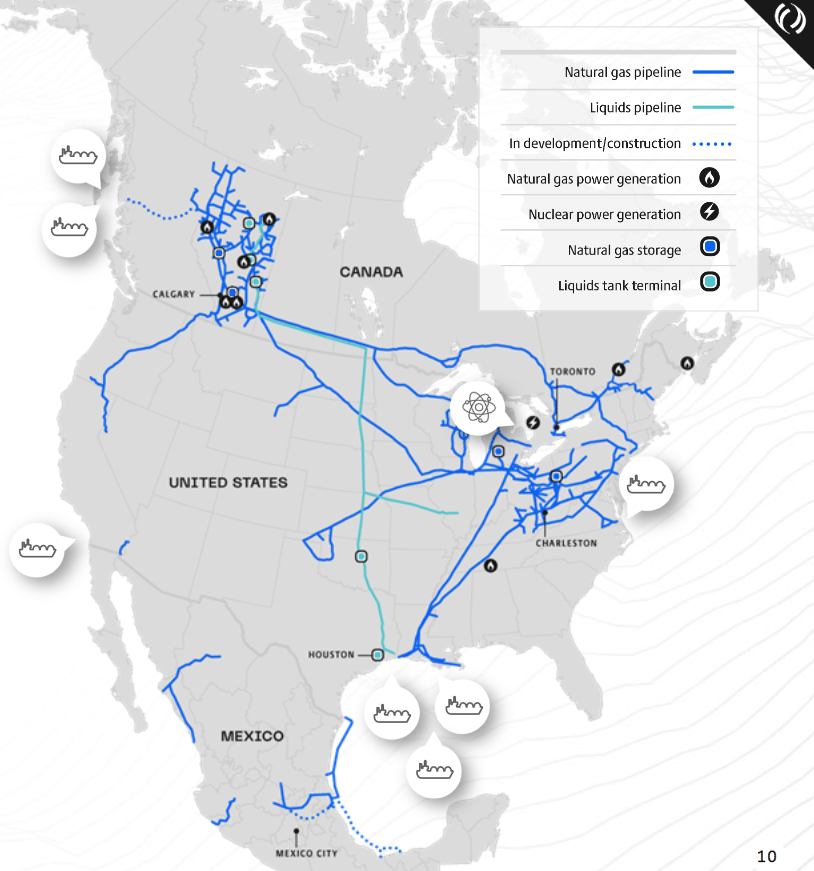

As stated in the introduction, TC Energy Corporation is a Canadian midstream company that primarily transports natural gas throughout Canada and the United States. The company is one of the largest midstream companies on the continent, as its pipelines cover the breadth of Canada, the United States, and even Mexico:

{kind=link}

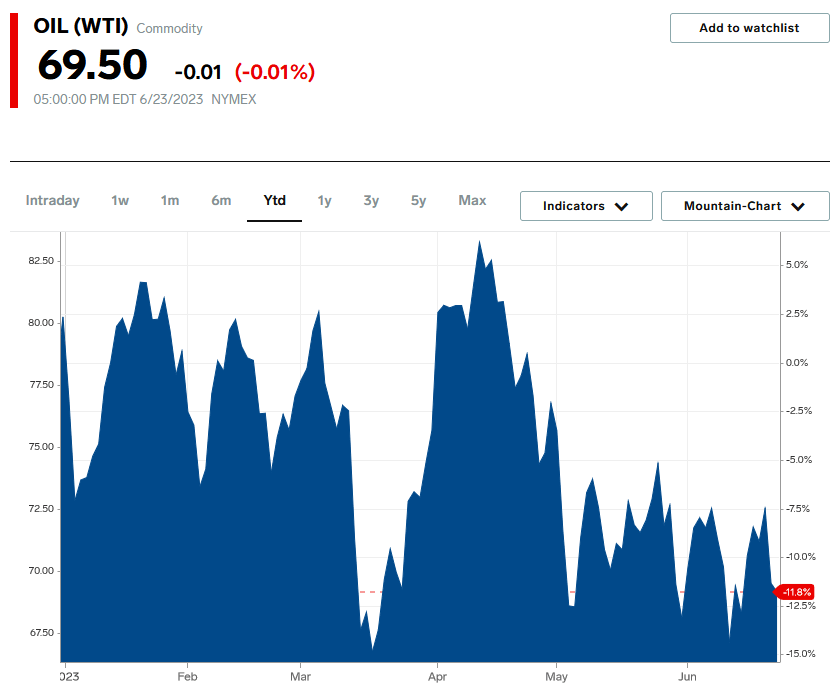

This is clearly much larger than its American peers, as very few companies have operations that extend the whole way down to Mexico. However, despite its size, the company's overall business model is very similar to that of its American peers. In short, TC Energy enters into long-term (usually five to ten years in length) contracts with its customers under which the company transports and stores hydrocarbon products owned by the customers using its network of pipelines and other midstream infrastructure. In exchange, the company's customers compensate it by paying a fee that is based on the volume of resources handled, not on their value. This provides TC Energy Partners with a great deal of insulation against changes in energy prices. That is a very good thing today, as the price of West Texas Intermediate crude oil is down 11.80% year-to-date:

{kind=link}

Natural gas prices have certainly not fared any better. The price of natural gas at Henry Hub is down 40.13% year-to-date. Unfortunately, this works both ways, as the company does not benefit when energy prices are very high. We can see this quite clearly by looking at its cash flows. Here are TC Energy's operating cash flows during each of the past ten years:

{kind=link}

(All figures in millions of Canadian dollars)

As we can clearly see, the company's operating cash flow generally was very stable over the period despite the fact that crude oil prices were all over the place. For example, we saw very low prices in both 2015 and 2020 yet the company's operating cash flow appears to have been completely unaffected by this, just like it did not see big year-over-year surges in 2021 and 2022 despite the strength in energy prices that we saw during those years.

The fact that TC Energy enjoys very stable cash flows over time should be appealing to income-focused investors, however. This is because it provides a great deal of support to the dividend that the company pays out. After all, it is much easier for a company to pay out a substantial portion of its cash flow to the investors if it can be reasonably certain that it will receive a similar amount of money in the next period. This is similar to the way that a salaried employee typically has an easier time carrying a mortgage than a person that works on commission or is self-employed (it is also much easier for the salaried person to qualify for a mortgage). As many income investors want to use the dividends to support themselves, the fact that the company can pay out a large proportion of its cash flow sustainably should be appealing. As is always the case, we will discuss the sustainability of TC Energy's dividend later in this article.

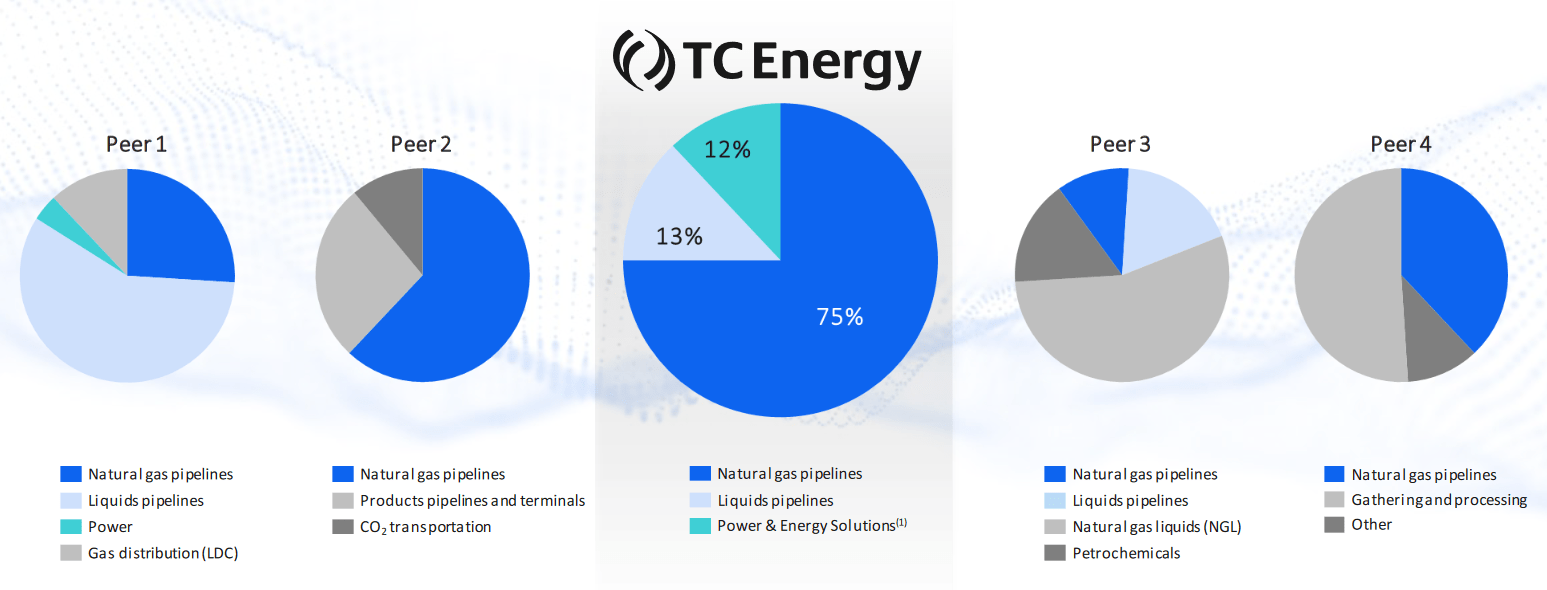

Despite this stability, TC Energy does have an indirect exposure to the fundamentals of the energy sector over the long term. This is because its business model is based on the volume of resources that are transported. Logically, when the demand for a given resource increases, the company's volumes will increase as upstream producers seek to satisfy that demand. The most important resource for this company is natural gas as 75% of the company's adjusted EBITDA (a proxy for pre-tax cash flow) comes from natural gas:

{kind=link}

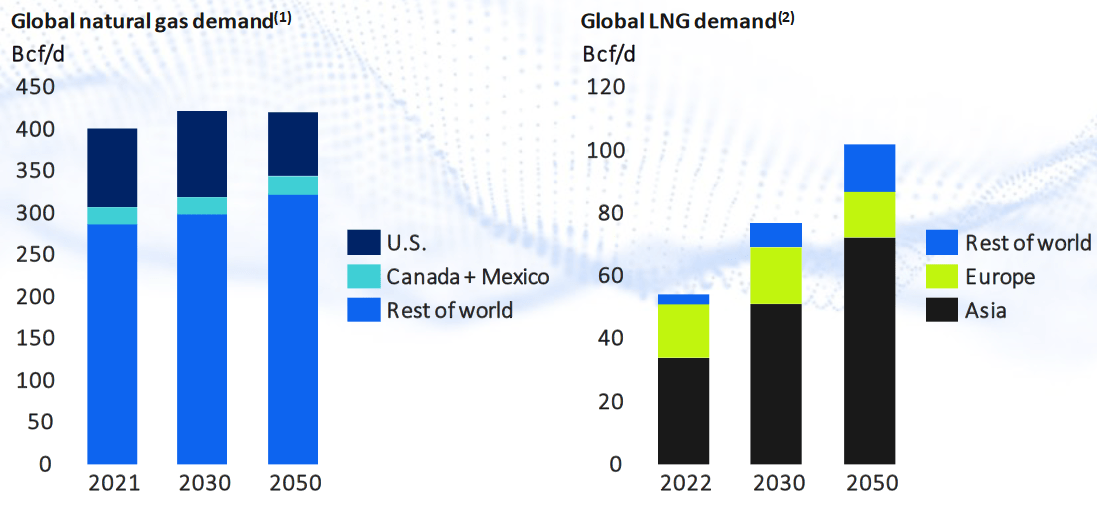

As I have discussed in numerous previous articles, the fundamentals for natural gas are quite positive. This is because of its use as a supplement for renewable energy generation. After all, wind and solar are intermittent and do not produce power 24/7 but a modern electrical grid requires 24/7 reliability. While batteries have been offered as a solution, the truth is that no battery technology that humans currently have is anywhere close to capable enough to fix this problem. Thus, the usual solution is to supplement the renewable generation with natural gas turbines as natural gas is capable of reliably producing power to the degree necessary to sustain a modern grid. We can see this in the fact that the International Energy Agency projects that the global demand for natural gas will increase through 2030 and will be well above current levels in 2050:

{kind=link}

As I have noted in the past , the International Energy Agency has recently come under fire from critics for making incredibly optimistic predictions about the success that the world will have in reducing energy consumption. There are numerous reasons to believe that the actual demand for natural gas will be quite a bit higher than the agency is projecting. We can still see though that the demand for natural gas will grow regardless of whether you believe the International Energy Agency's projections about the success of electrification in weaning the world off of fossil fuels or not. This is important for our purposes because North America is one of the only places in the world that is capable of significantly increasing its production of natural gas to meet this demand growth. This is due to the incredible mineral wealth of areas like Appalachia, which TC Energy serves with its infrastructure network as noted in the map above.

Thus, the company would be a logical choice for an upstream producer in that region that is seeking to get its natural gas out of the area and to the market where it can be sold. As TC Energy's cash flows are directly correlated to its volume of transported resources, we can expect this to grow the company's cash flows going forward.

Growth Opportunities

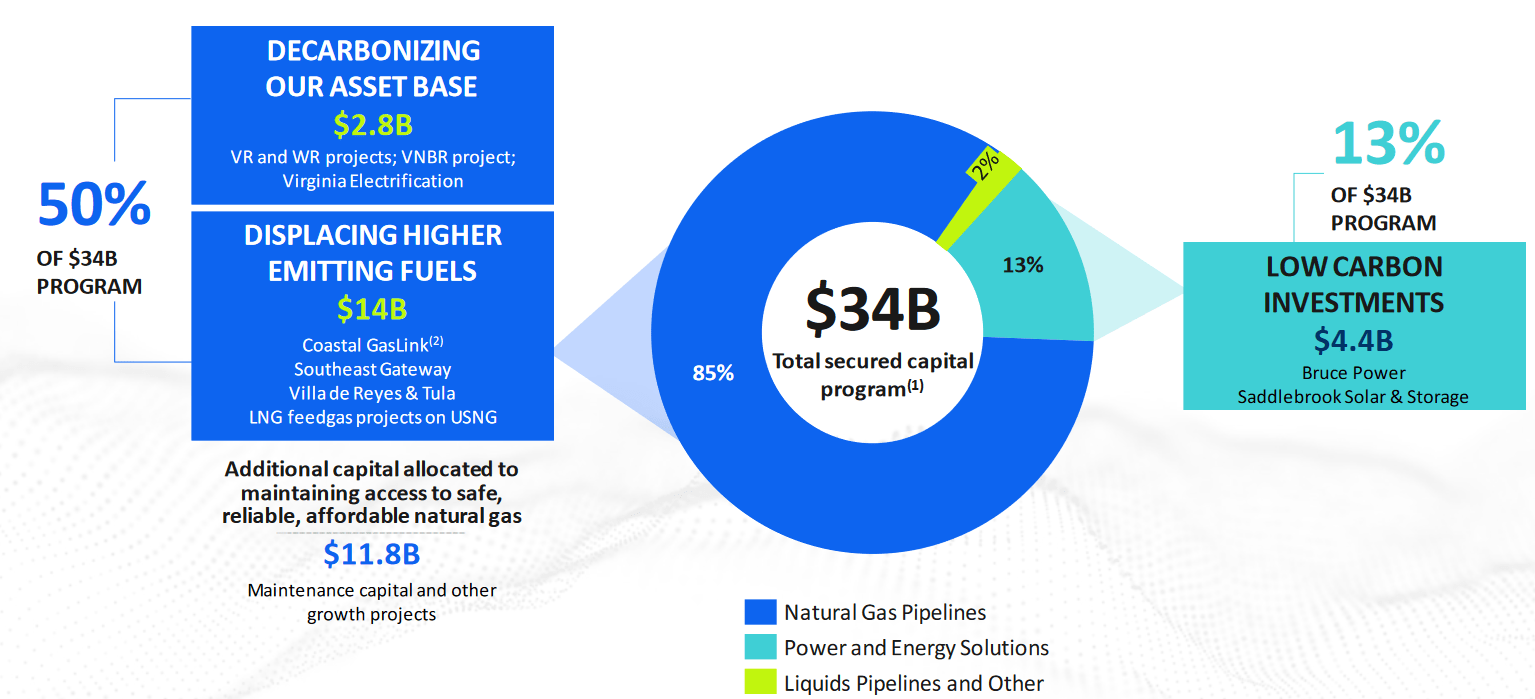

As we can clearly see, TC Energy has some growth potential due to the rising demand for natural gas. However, that is not the company's only growth opportunity. In fact, TC Energy Corporation has approximately C$34 billion worth of projects under various stages of development that are intended to generate growth:

{kind=link}

We can clearly see that the overwhelming majority of these are natural gas pipelines. This is unsurprising considering that pipelines are the largest source of both revenue and cash flow for the company despite the constant promotion of its "green credentials." This is likely to be the case for a considerable period of time given that renewable energy does not work without natural gas supporting it to ensure reliability. The company has also almost assuredly noticed that major European energy companies like Shell ( SHEL ) and Equinor ( EQNR ) are struggling to earn any profits from their renewable energy divisions. It makes sense for TC Energy to focus its investments in traditional pipelines, as these are actually profitable and thus provide value to investors despite some people screaming about the problems with fossil fuels.

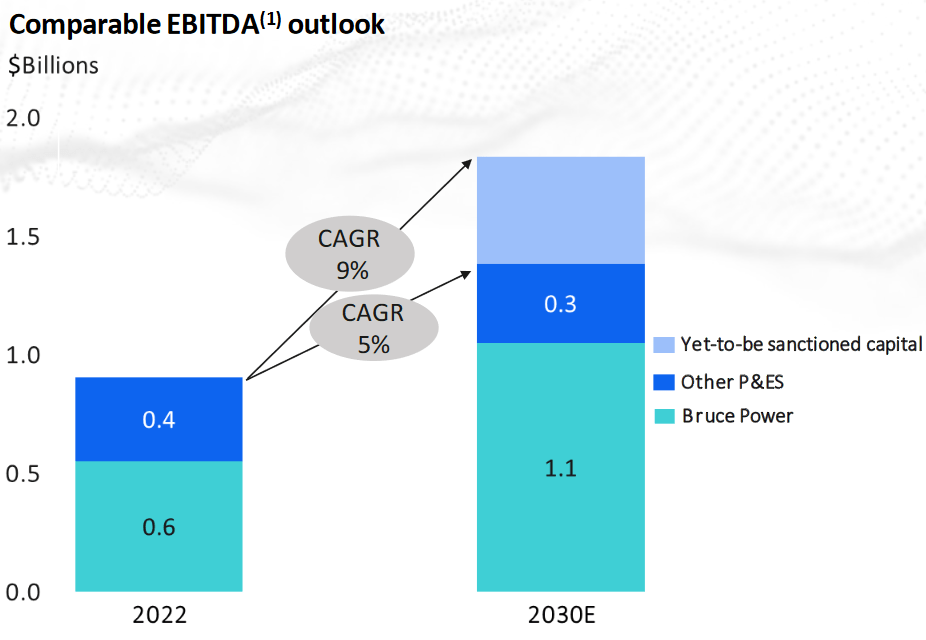

The nicest thing about the company's pipeline projects is that TC Energy has already secured contracts from its customers for the use of the new infrastructure. This ensures that the company is not spending a great deal of money to construct new infrastructure that nobody wants to use. In addition, TC Energy knows in advance how profitable each project will be prior to beginning construction of it. Thus, the company knows in advance that it will earn a sufficient return to justify the investment. The company has stated that it expects that its current projects will generate a 10% internal rate of return once they begin operating. It has also provided guidance pointing to a 5% compound annual growth rate of its EBITDA through 2030 just from the projects that it has under construction:

{kind=link}

The company's guidance is for a 9% compound annual growth rate of its EBITDA over the period, but that higher figure is being driven by potential future projects that it has not secured commitments from customers yet. Thus, there is no guarantee that the projects driving the higher figure will ever be started. The 5% growth rate is simply from the projects that the company currently has under construction and since it already has commitments from its customers to utilize the new projects, that figure should be considered guaranteed. Thus, the company's actual EBITDA growth will likely be somewhere between 5% and 9% annually, which is not too bad for a company like this. That is especially true considering that TC Energy has a high enough dividend yield that the company should still provide an adequate return on investment even if it does not manage to achieve any growth.

Financial Considerations

It is always important to analyze the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt and using the proceeds to repay the existing debt. After all, most companies do not have the ability to completely repay their debt with cash as it matures. As new debt is issued with an interest rate that corresponds to the market interest rate at the time of issuance, this process can cause a company's interest expenses to increase following the rollover in certain market conditions. In both the United States and Canada, interest rates are at the highest rate that we have seen in over a decade, so this is a very real concern today.

In addition to interest-rate risk, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company's cash flows to decline could push it into financial distress if it has too much debt. While TC Energy has remarkably stable cash flows, this is still a concern that we should never ignore.

The usual metric that we use to evaluate a midstream company's ability to carry its debt is the leverage ratio, which is also known as the net debt-to-EBITDA ratio. This ratio tells us how many years it would take the company to completely pay off all of its debt if it were to devote all of its pre-tax cash flow to that task. In the first quarter of 2023, TC Energy reported an EBITDA of C$2.775 billion, which works out to C$11.1 billion on an annualized basis. The company's net debt as of March 31, 2023 was C$59.283 billion. This gives the company a leverage ratio of 5.34x today. That is a bit high for a company like this. As I have pointed out in numerous previous articles, Wall Street analysts generally consider anything under 5.0x to be acceptable. However, ever since the pandemic-related lockdowns, most midstream companies have been aggressively reducing their debt, and the best companies in the industry now have ratios under 4.0x. TC Energy thus appears to be excessively reliant on debt to finance itself, and this could pose a higher risk to investors than peers such as Enbridge ( ENB ) and Pembina Pipeline ( PBA ), which have much lower debt levels.

Dividend Analysis

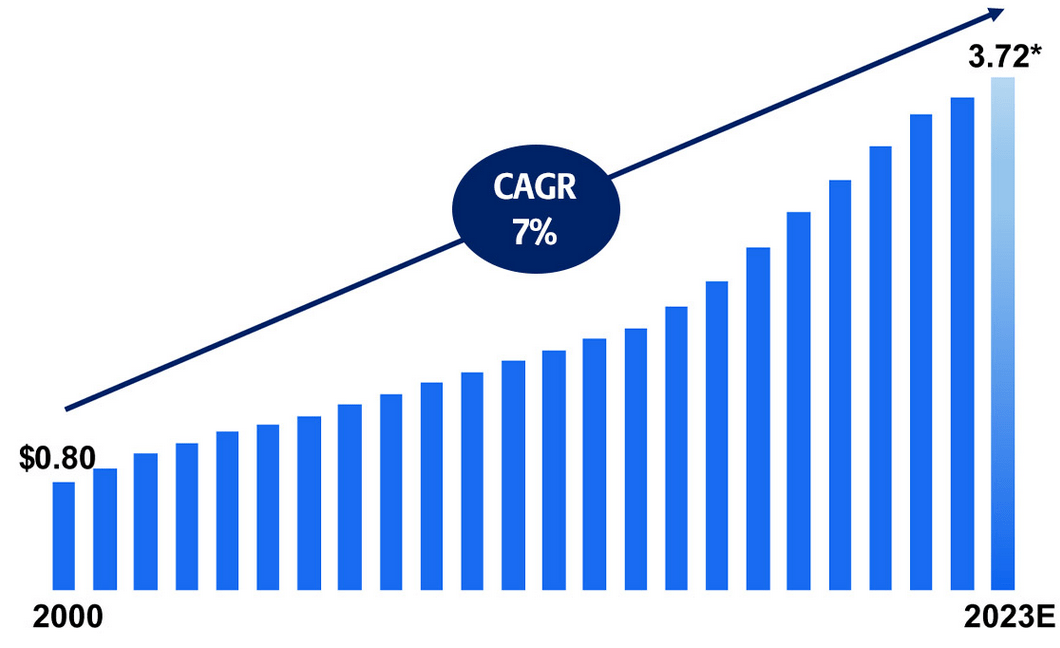

One of the biggest reasons why investors purchase shares in midstream companies like TC Energy is because of the incredibly high yield that most of these companies possess. TC Energy is certainly no exception to this as the shares yield 6.89% at the current price. The company also has a long history of raising its dividend on an annual basis. In fact, TC Energy has grown its dividend at a 7% compound annual growth rate over the past 23 years:

{kind=link}

It is important to keep in mind that TC Energy declares and pays its dividends in Canadian dollars. However, the shares that trade on the New York Stock Exchange pay a dividend in U.S. dollars. The dividend by these shares will vary based on the exchange rate between the two currencies at the date of issuance. Thus, while American investors will still generally see the dividend grow over time, it will occasionally go down from quarter to quarter if the U.S. dollar strengthens against the Canadian currency.

The fact that the company increases its dividend annually is something that is very nice to see during inflationary periods such as the one that we are in today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividends that the company pays out. This can make it feel as though we are getting poorer and poorer with the passage of time. This is especially a problem for those investors that are depending on the income from their portfolios to pay their bills or finance their lifestyles. The fact that the company increases its dividend annually helps to offset this effect and maintains the purchasing power of the dividend over time.

As is always the case, it is critical that we ensure that the company can actually afford the dividends that it pays out. After all, we do not want to be the victims of a dividend cut since that would both reduce our incomes and almost certainly cause the company's stock price to decline.

The usual way that we judge a company's ability to pay its dividend is by looking at its free cash flow. The free cash flow is the amount of cash that was generated by a company's ordinary operations and is left over after it pays all its bills and makes all necessary capital expenditures. This is the amount that is available to benefit the shareholders through things such as debt reduction, buying back stock, or paying a dividend. In the twelve-month period that ended on March 31, 2023, TC Energy had a negative levered free cash flow of C$1.2303 billion. That is obviously not enough to pay any dividends, yet the company still paid out C$3.087 billion in dividends over the period. At first glance, this will almost certainly be concerning as the company is apparently unable to cover its dividends out of free cash flow.

However, it is not uncommon for companies like TC Energy to act much like utilities. This is because the inherent stability provided by its contract-driven business model is similar to the cash flow stability that utilities enjoy by virtue of their status as providers of a basic necessity. A utility will commonly finance its capital expenditures through the issuance of equity and debt while paying its dividends out of operating cash flow. TC Energy generally does the same thing. In the twelve-month period that ended on March 31, 2023, TC Energy reported an operating cash flow of C$6.742 billion. That was easily enough to cover the company's C$3.087 dividend with a substantial amount of money left over for other purposes. Thus, it does appear that the company can afford to sustain its dividend at the current level.

Conclusion

In conclusion, TC Energy is a Canadian midstream giant that offers a lot to income-seeking investors. In particular, the company's focus on natural gas has provided it with very strong growth prospects that will almost certainly result in dividend growth. Thus, anyone buying the company will probably have a higher yield-on-cost in just a few years. The only real problem here is that the company's debt is a bit higher than we want to see. Overall, it might be worth considering, particularly for those that want natural gas exposure.

For further details see:

TC Energy: High Yield And Exposure To The Energy Transition