TEL - TE Connectivity: Patience Rewarded One For The Very Long-Term Investor

2023-11-22 20:33:48 ET

Summary

- TE Connectivity's stock price has begun to reflect a period of better business ahead despite mixed annual numbers.

- The company's strong cash flow and dividend history make it attractive for long-term investors, 5-years+ horizon.

- But the company's low-growth prospects and higher multiples make it a hold for short to mid-term investors (1–4 years).

Investment update

Since reporting Q4 and FY'23 results earlier this month, markets have begun to price in a period of better business for TE Connectivity Ltd. ( TEL ). Which is strange given the mixed performance dotted throughout the company's annual numbers. Or, is it simply correcting a previously wild forecast of TEL's value?

In my last report , I noted that TEL "is a company that offers multiple inflection points for potential investment. Cash flows, dividends + buybacks, economic earnings, high returns on capital, they are all there". What I also noted, is (1) no sales, earnings or FCF/share growth, and (2) pricey multiples for this kind of company. I rated the company a hold for investors with a short to mid term horizon.

Following the company's FY'23 numbers, we now have the following investment facts pattern:

- TEL now sells at 17-18x forward earnings, slightly below 5-year averages. At the same time, TEL's growth percentages at the bottom line for FY'23 were flat at best.

- What are the standouts— first is dividends . Rated an A on safety and growth by Seeking Alpha. Current yield gets you 1.8% with a $2.32/share trailing payment. The company has been paying dividends for 9 consecutive years.

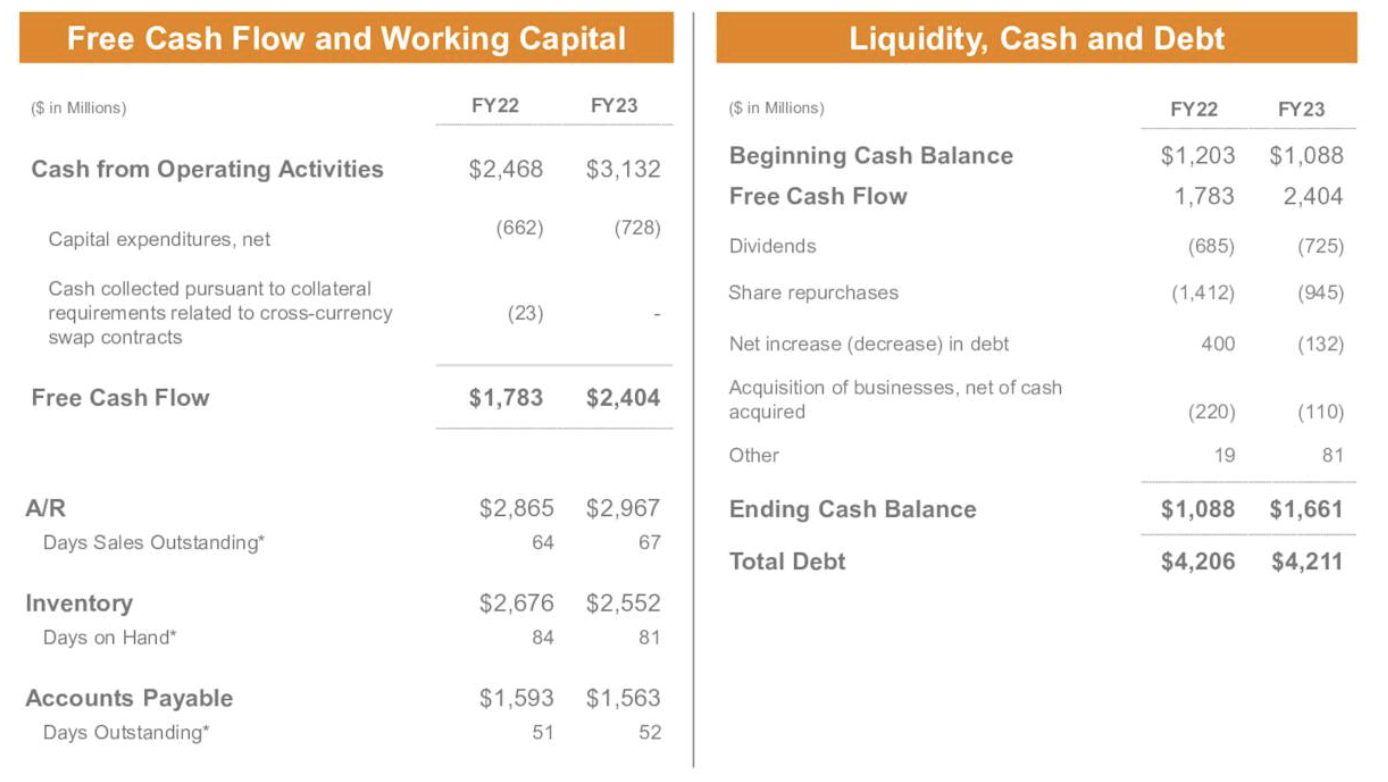

- Second is the strong year of ramping up cash, producing $3.1Bn in operating cash flow and ~$2Bn in FCF.

- This is a highly profitable enterprise that is compounding wealth for its shareholders over the very long-term.

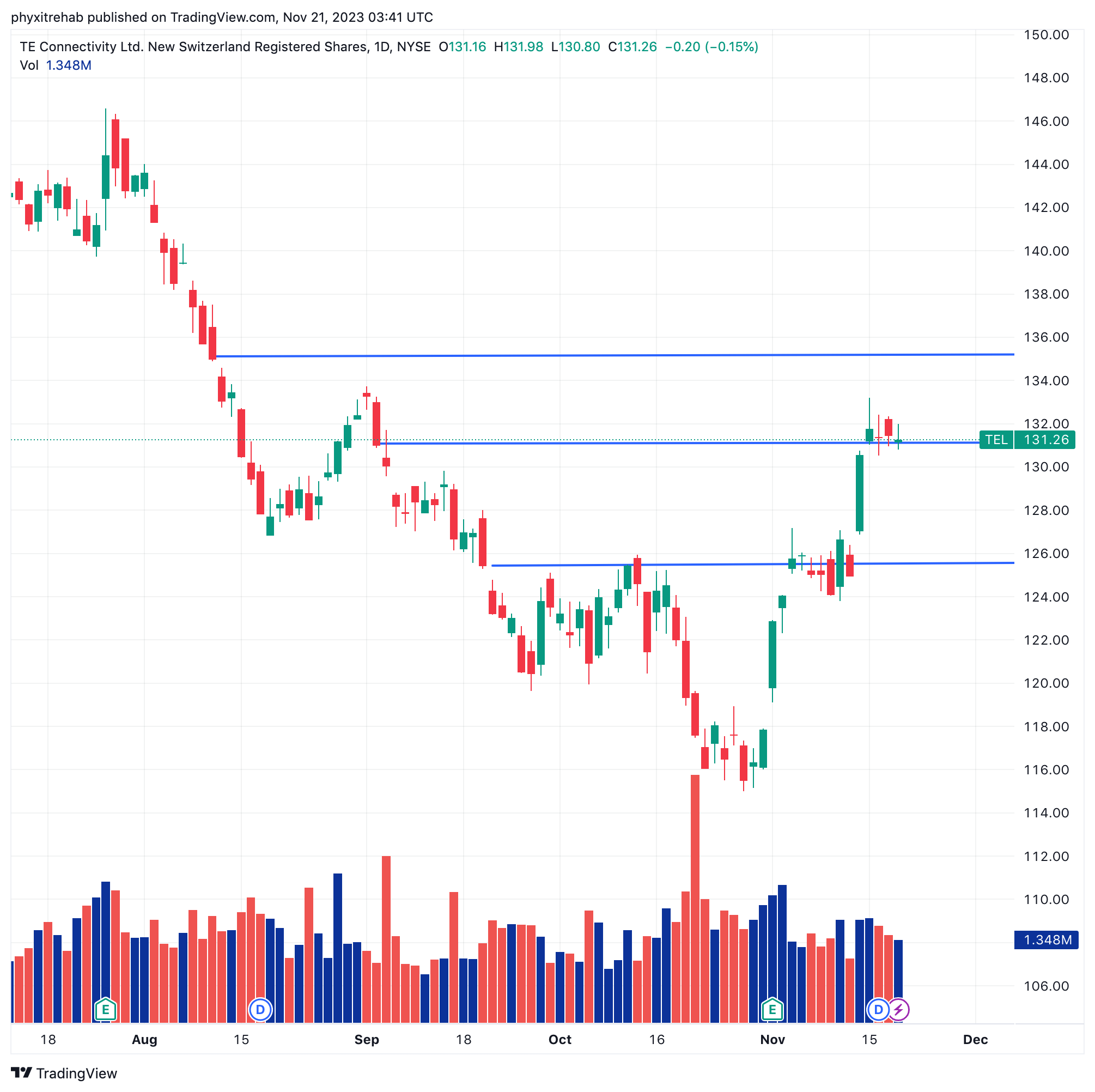

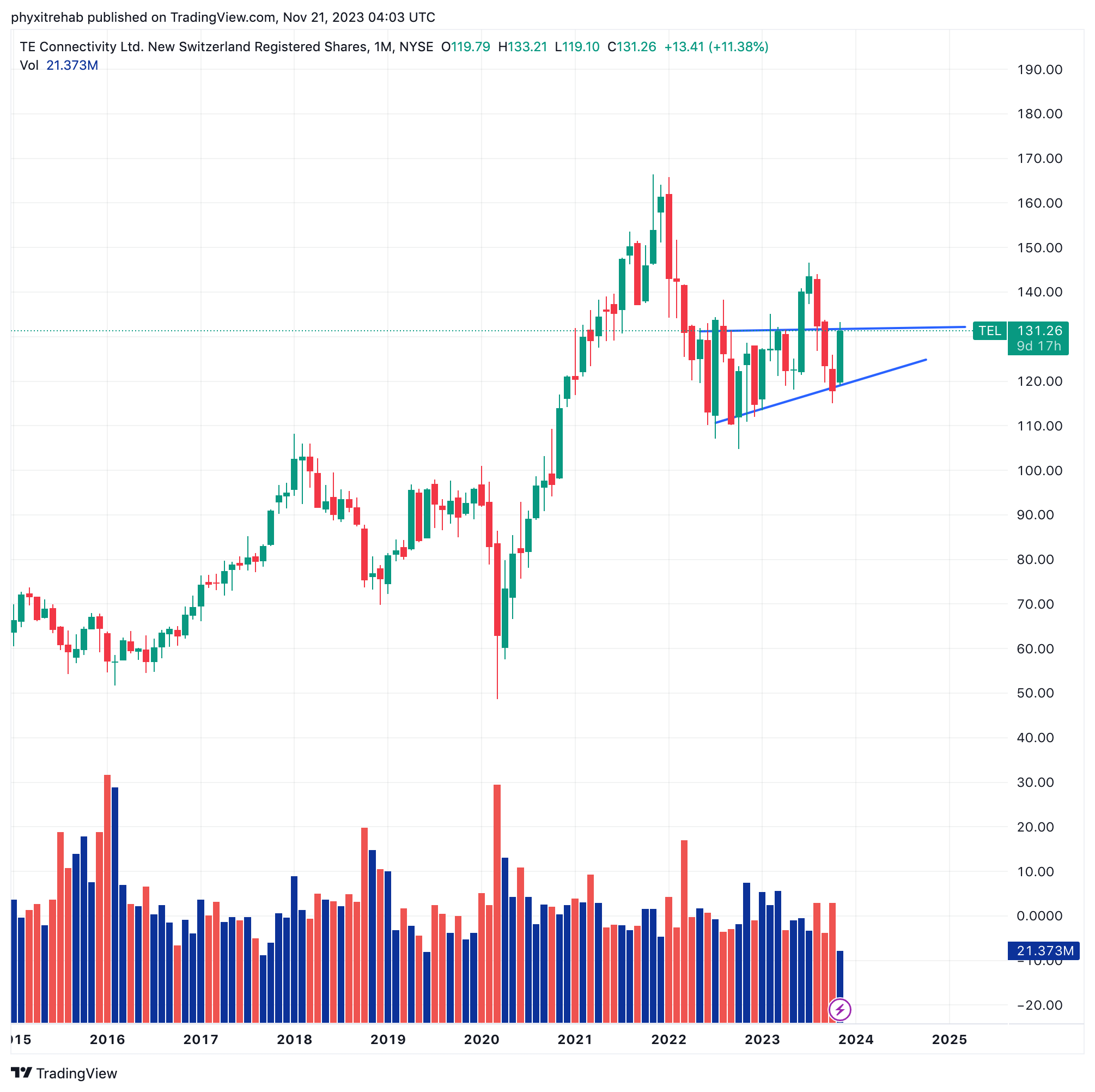

Like most markets + industries, the company's stock price found buyers at its October low (Figure 1). TEL's buying thrusts since then have been particularly strong. The 2x ledges of price competition in November have formed at the 2x gaps down from Sep–Oct, now retaken. Next region we have similar to this is to $136, so keep this price in mind as a signal. Meanwhile, the stock found liquidity in the $110s after the '22 selloff. It has held this range with higher lows (Figure 2).

Each of these factors tell of a low-growth, stable cash flow company that suits a very long-term orientated investor. Aim: to compound and avoid excessive drawdown. In that scenario, I could see value for TEL. For my portfolios, they more aggressively positioned and so keep a shorter-time frame in mind (1 to 3 years). So I rate TEL a hold for that reason.

Figure 1.

{kind=link}

Source: Tradingview

Figure 2.

{kind=link}

Source: Tradingview

Review of TEL's FY'23 numbers

As a reminder, TEL reported its Q4 / full year results for its fiscal year 2023, coinciding with Q3 CY 2023.

- Insights into financial performance

TEL booked $16Bn in FY'23 net sales , flat YoY, holding strong against a $430mm in FX headwind. It also clipped 3% organic growth with all adjustments. Finished the year with a book to bill of 0.97 vs. 0.99 last quarter, could be a sign of productive business. It collected a record $3.1Bn in operating cash flow and $2.4Bn in FCF for the year. It returned $1.7Bn to shareholders as well, a total of $4.1Bn in cash for usage in its FY'23.

As to the segmental analysis, note the following takeouts:

Transportation Segment:

- Management's view on transportation markets remains solid, with global auto production staying steady. I found this compelling language. Certainly one to keep an eye on in next earnings to see if the ends match up.

- Booked $2.4Bn in Q4 sales in transportation, up 4% YoY, on 23.5% operating margin, a clear step above averages.

- The major drivers of growth were automotive sales, up 10%, and ~300bps of contribution from sensors.

Industrial Segment:

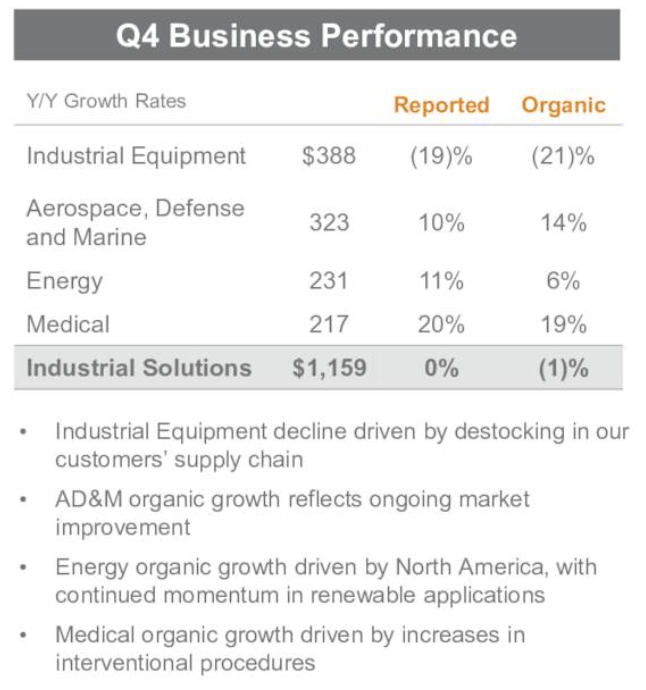

- Mixed year– 75% of businesses in the industrial segment grew, but industrial equipment was down 19%, so segment was flat YoY (Figure 3).

- It continues to eye the play in renewable energy, especially in wind and solar applications. It has reported development in its North America market.

- Management also report that commercial air sales are bouncing back as the market recovers, and the medical business is floating higher on growth in interventional procedures.

Figure 3. Industrial Segment Revenues

{kind=link}

Source: TEL Q4 / FY'23 Investor Presentation

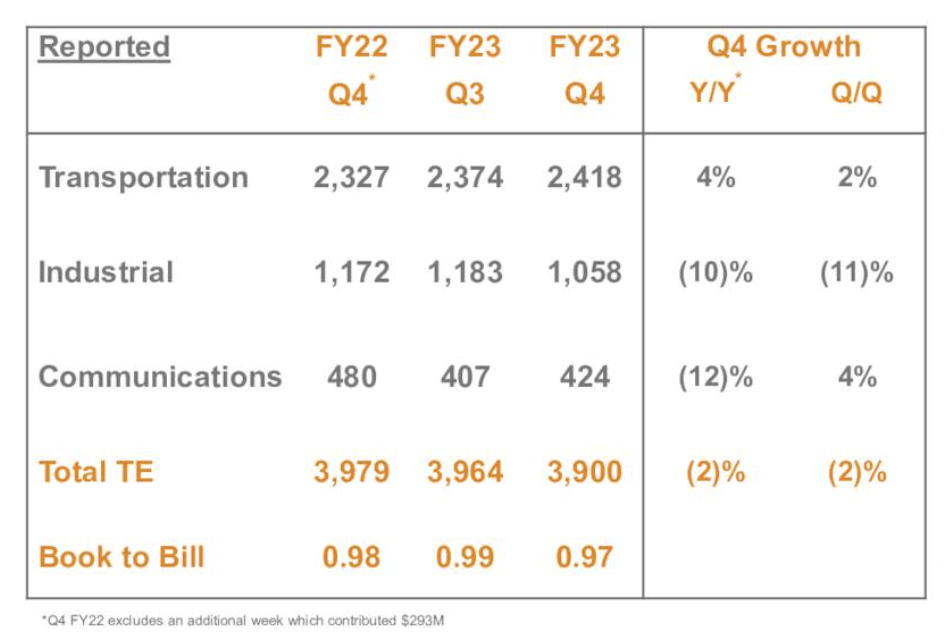

Communications

- Sales peaked last year, and were down 26% in FY'23 to $463mm.

- The major reason is an inventory destocking across TEL's supply chain, its customers supply chain, and, its supply chain customers.

- Management did report that it booked sequential growth in orders in Q4. So I would advocate to pay close attention to the communications business from here. It looks as if management are piping the capital cake batter onto the segment, and there's been momentum.

Figure 4.

{kind=link}

Source: TEL Q4 / FY'23 Investor Presentation

- Well positioned for growth in '24

Looking ahead to Q1 of fiscal '24, management anticipates net sales of approximately $3.85Bn, flat YoY. It is eyeing 27% YoY growth in earnings on this to ~$1.60/share. It also increased its cash on hand by ~$600mm along with the record $2.4Bn FCF. Large in part with the operating margin growth to 17.3%. Crucially, most of the margin upside was seen in H2 FY'23, providing momentum into the new fiscal year.

I also believe the market has digested the hurdles imposed by the inventory destocking by TEL's distributors. This is likely to continue over the next few quarter, based on recent trends. Management were clear about this on the call, and no major reactions followed, so it is likely the market has discounted this already. Keep in mind, we sold off to 6-month lows in October.

The company's reported figures were also impacted by USD strength. The stronger USD negatively impacted sales by ~$430mm compared to FY'22. That's something to keep in mind. When this begins to roll off, TEL's underlying fundamentals are well positioned against this.

Figure 5.

{kind=link}

Source: TEL Q4 / FY'23 Investor Presentation

Long-term economics show TEL's competitive position

TEL is not compounding its intrinsic value through profit margins or business expansion.

For example, the compounding 5 year rate of sales growth is 2.7%, on asset growth of 4% for the last 3 years. The company is, however, compounding its intrinsic value through robust business returns, earnings growth, and FCF per share.

(1). Business returns

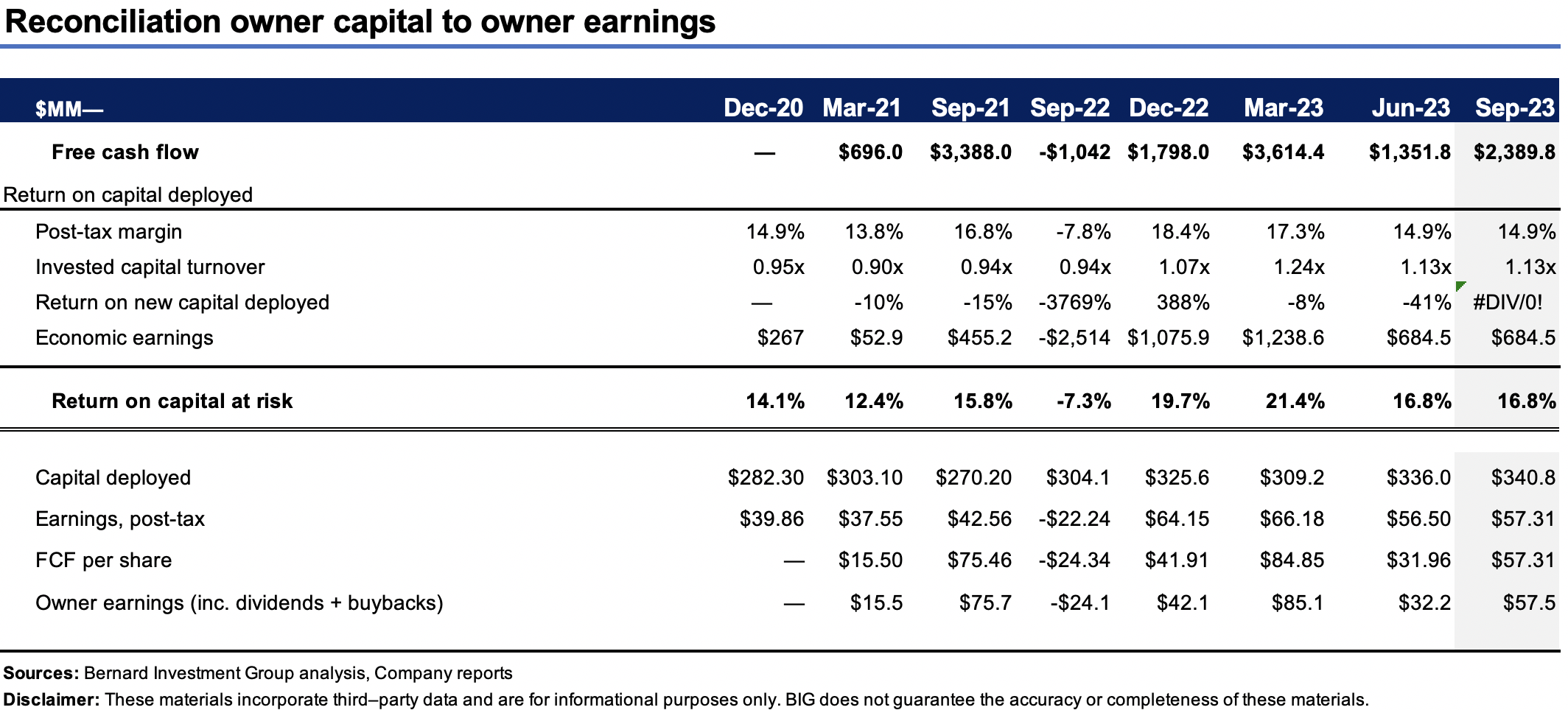

It had $340 per share of capital invested into the business end of Q3, which returned $57/share in TTM NOPAT last quarter, producing a 16.8% return on investment—better than most investment managers. It has averaged a 15-16% earnings rate on capital since 2020.

The drivers of this are 1) high capital turnover of 1.13x sales, and 2) modest post-tax margins of 15% on sales. The first means TEL's assets are producing income at a reasonable pace (daily pace for instance); the second, that these assets are profitable to run, meaning utilization should be as often as possible.

For the long-term investor (5 years+), this is compelling. A firm will create substantial long-term value for its shareholders generating profits on its investments at a persistent rate above 12-13%.

Figure 6.

{kind=link}

BIG Insights

(2). Earnings growth

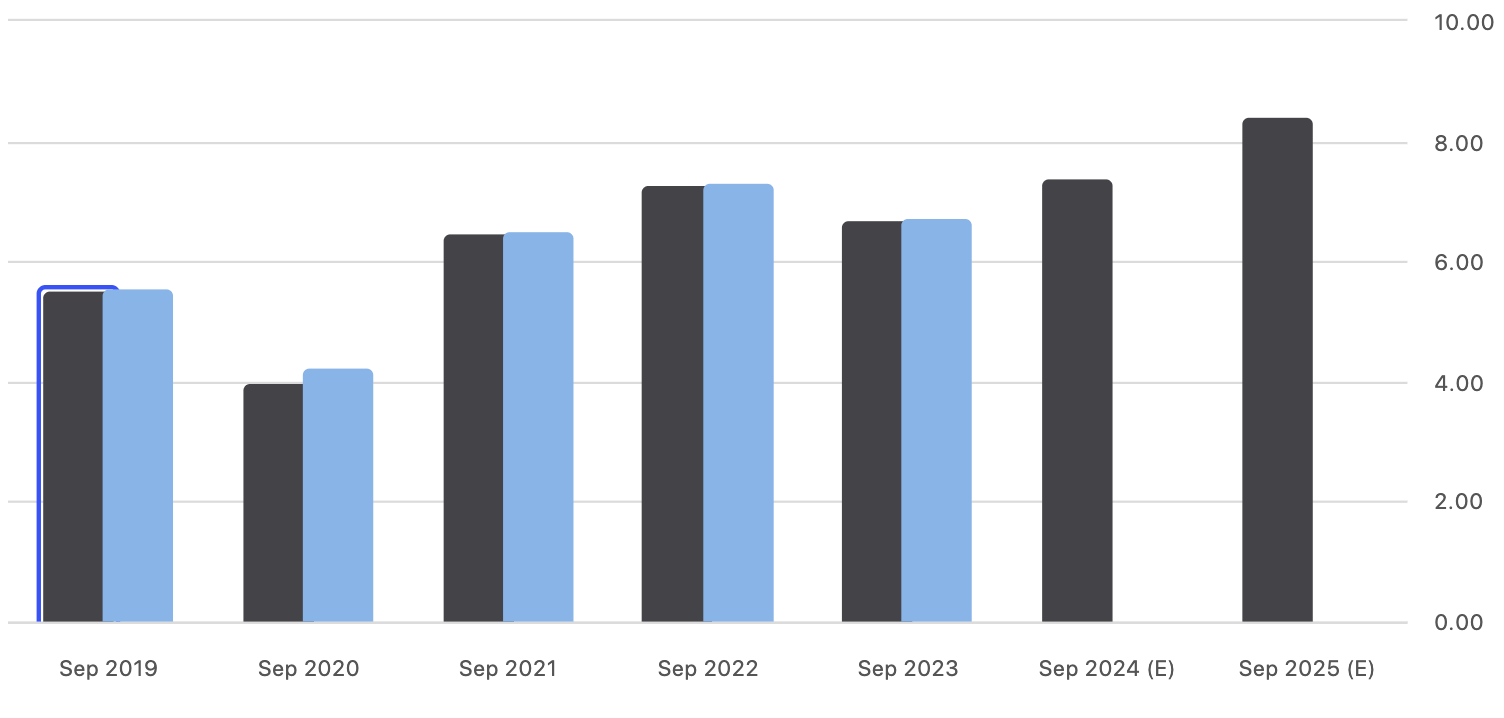

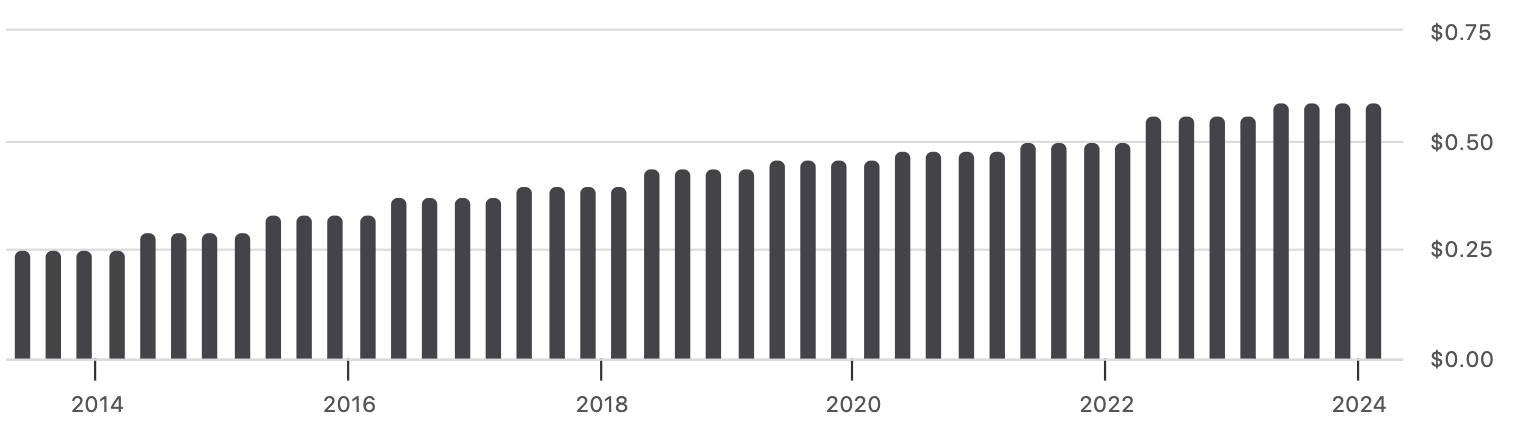

I will also sneak in here, dividend growth. Both have been commendable for the company over the last 5 years. Earnings have been lumpy, but grown from $5.55/share in 2019 to $6.74 in the TTM. The company's dividend growth, seen in Figure 8, is to be commended. The power of compounding in income is clearly observable here as well.

Consensus is eyeing in 9-10% earnings growth this year in FY'24, stretching up to 13% growth in FY'25. Investors are paying 17.7x and 15.6x forward earnings to buy this growth at the current market price, respectively. This bodes in well for returns over the next 1-3 years, both on the valuation and growth front. Should it keep up this rate of earnings growth, it is well positioned.

Figure 7. TEL Earnings Growth 2019–date

{kind=link}

Source: Seeking Alpha

Figure 8. TEL Dividend growth 2014–date

{kind=link}

Source: Seeking Alpha

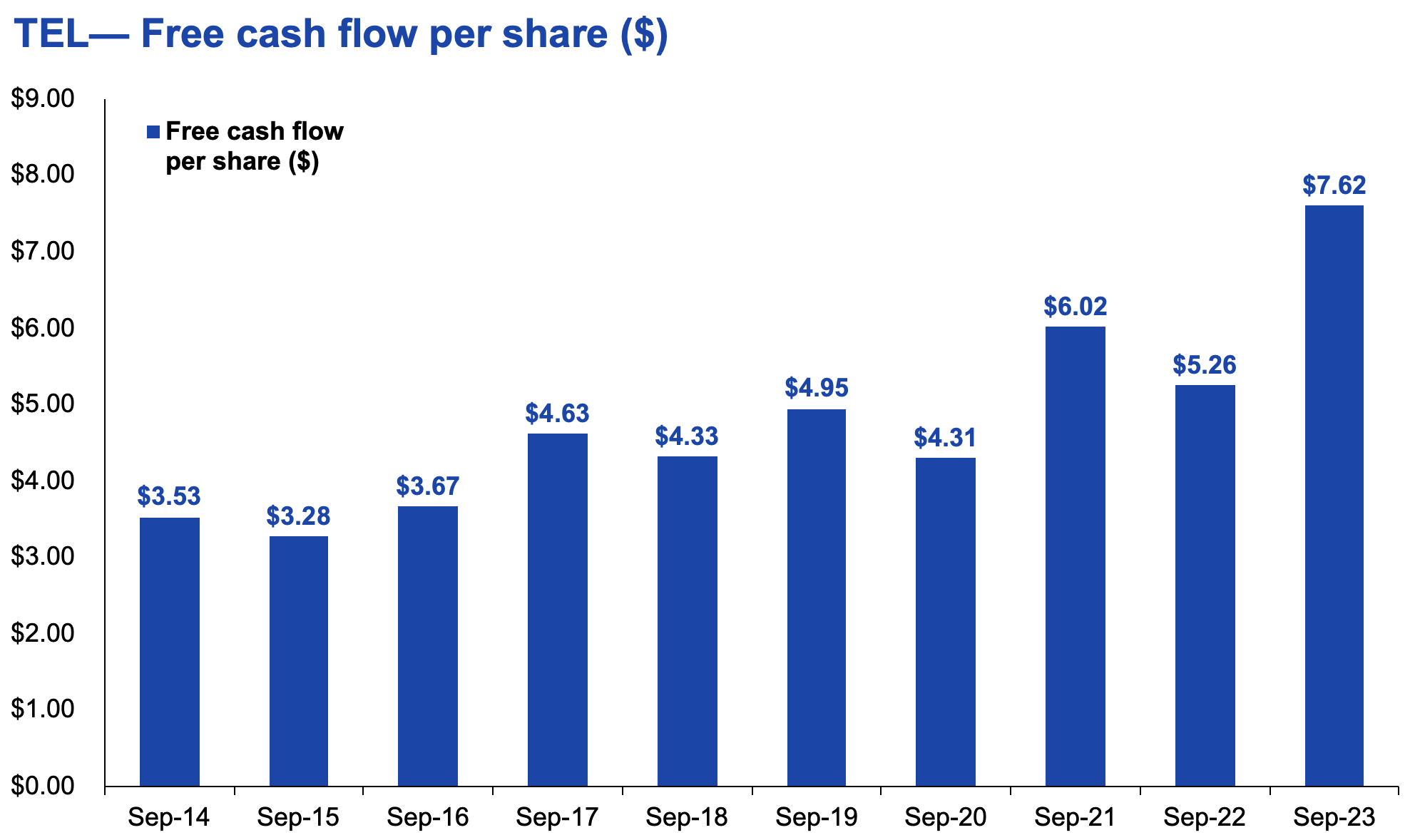

(3). Free cash flow per share

The long-term TEL investor has obtained remarkable results for his or her patience. In terms of economic characteristics, the proof is in the data for TEL. The critical facts are:

- The FCF per share increased from $3.53 in 2014 to $7.62 last year, having averaged above $5 since 2021 (Figure 9).

- It has produced $47.60 in cumulative FCF per share since 2014, back when its share price was around $60. On top of this, it has returned a total of $16.22/share by way of dividends over this time. Collectively, therefore, the company has created $63.44 per share of direct intrinsic value for its shareholders—in FCF and dividends, since 2014. Its stock price has compounded by $71.25 (118.7%) over the same time. This sets a critical long-term trend in motion, and by all measures looks set to continue going forward.

These facts cannot be overlooked and illustrate a firm with potential to create wealth over a long-term horizon, more than 5 years. For those seeking to own the company, this holding period is ideal to maximise the compounding effects combined with dividends in my opinion.

Figure 9.

{kind=link}

Source: BIG Insights, Company reports

Valuation and conclusion

The stock is not offensively priced at 17.7x forward earnings and 15x forward EBIT. The company's 17% ROE is noted, but chopped down to 4.85% for the investor if paying the 3.5x book multiple. At an EV of $43.9Bn, this is >3x the business capital required to operate, so the stock is in buy no means cheap either.

You are also receiving a 7.3% cash flow yield if buying TEL today, with 1.77% in dividends. The 17x forward also seems pricey with the forward PEG ratio at 1.8x indicating the growth is well captured at 17x multiple. Moreover, at 17x FY'25 consensus earnings estimates of $8.42/share, this gets you to $143/share in implied market value, 9% value gap from today's market price. This margin does not support a buy rating in my estimation. I should note, the quant system supports this rating of a hold, using a blended composite of factors at different weightings. This adds further support to the thesis.

Figure 10.

{kind=link}

Source: Seeking Alpha

In that regard, what you are receiving is crystal clear, but the price is high to get on board for TEL in my view. For those looking over the mid term (1 to 3 years), my thoughts from last time echo " [v]Valuations are unsupportive and today's prices may not be the correct entry, as asymmetrical risk/reward does not come out from my modeling here ".

As I've stated multiple times now, this is a holding to be considered for the very long term, more than 5 years in my view. It has exceptional economics to compound wealth. But these situations need time for the arithmetic to manifest. In that vein, reiterate hold for my horizon (1-3 years).

For further details see:

TE Connectivity: Patience Rewarded, One For The Very Long-Term Investor