TEAF - TEAF: A Unique Approach To Infrastructure And Attractively Discounted

2023-09-23 02:15:36 ET

Summary

- Ecofin Sustainable and Social Impact Term Fund offers a unique portfolio with a comprehensive infrastructure approach, including social infrastructure investments.

- TEAF has traded at a deep discount since its launch, presenting a potential long-term opportunity for investors.

- The fund pays an attractive monthly distribution, with a distribution yield of 8.61%, providing income for investors while they wait for the discount to narrow.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Ecofin Sustainable and Social Impact Term Fund (TEAF) offers investors a unique portfolio that offers an unusual comprehensive infrastructure approach. The majority of infrastructure closed-end funds are going to be loaded generally with utilities and energy investments. Some offer exposure to renewable energy sources, but with today's environmental regulations, most utility companies are naturally putting more CAPEX to work in that direction anyway.

They have certain levels of emissions targets they need to achieve, so even your traditional utility will often have a renewable tilt. Thus, the funds that invest in energy or utilities are going to have some renewable exposure naturally. Where TEAF offers investors a bit of a different approach is that they also incorporate "social" infrastructure. That can include private schools and senior living buildings, which are different but are just as critical as power generation and transmission.

Additionally, TEAF has continued to trade at a deep discount, which adds its own opportunity over the longer term as a term structured fund. However, it should be noted that TEAF has seen its discount narrow a touch since our prior update. Additionally, the fact that the fund is involved significantly with private investments can also mean a discount persists for longer than usual.

The Basics

- 1-Year Z-score: -0.13

- Discount: -18.46%

- Distribution Yield: 8.73%

- Expense Ratio: 1.85%

- Leverage: 12.80%

- Managed Assets: $239.7 million

- Structure: Term (anticipated liquidation date around March 27, 2031)

Tortoise launched TEAF with the goal of "attractive total return potential with emphasis on current income and uncorrelated assets." Additionally, "access to differentiated direct investments in essential assets" and "investments intangible, long-lived assets and services." TEAF is also targeting a "positive social and economic impact."

Funds that offer unique exposure, particularly with a focus on private investments, often have higher expense ratios. For TEAF, they aren't an exception, as the fund's expense ratio comes to 1.85%. When we include the leverage expenses of the fund, it ticks up to 2.66%.

They've had to deal with higher interest rates in the form of increased borrowing costs on the fund, as the fund had previously reported in their fiscal 2022 total expenses of 2.17%. Fortunately, TEAF is only modestly leveraged, which I view as a positive. That being said, any leverage is going to make an investment more volatile and expose investors to greater risks, which should be considered before investing.

The small size of this fund is also something that investors should consider before investing. It often leads to a fairly low average daily volume, making buying and selling a position more difficult. In particular, larger investors would have a more difficult time accumulating a meaningful position if they wanted to do it all at once.

The Deep Discount Opportunity

TEAF has sported a deep discount just about since the fund launched, and the Covid crash really pushed the discount to some unusually wide levels. At this point, the fund is carrying a deeper discount than it has averaged since it launched.

A deep discount isn't that unusual, as we've seen discounts widen out through 2022 and into 2023. Two thousand twenty-one discounts were historically narrow across the board, so this widening out has probably felt even worse for investors with heavy exposure to CEFs. It was also a newer fund, so we generally expect the discount to appear shortly after launch.

Still, for the longer-term investor, this could present an opportunity, being that it is a term fund. The termination date doesn't come up until 2031, so we certainly have some time before we'd expect an uptick resulting in that anticipated event.

We covered the termination structure in our initial coverage of the fund more in-depth. However, there are two things that should be reiterated:

- The term may be extended by approval of the Board only. Once for up to a year and then again for an additional one year. That could end up pushing the termination date into 2033.

- The fund may also end up going perpetual if they trigger a tender offer for 100% of the outstanding shares at 100% of the NAV. If the fund would have at least $100 million in net assets after the tender offer, then the Board can remove the term date.

A large risk beyond extending a term would be that the fund is carrying around 50% of its managed assets in more illiquid private investments. As of their last semi-annual report, the fund had 31.56% of its portfolio in level 3 securities. These are investments that don't have a market and are valued on the "fund's own beliefs about the assumptions that market participants would use in pricing the asset or liability." Meaning that it is a genuine and good faith estimate based on models, but it's largely a guess nonetheless, which adds some ambiguity.

Finally, it is worth noting that Saba Capital Management owns around 6.59% of the outstanding shares. However, that was a reduction as they sold off some shares on June 30, 2023.

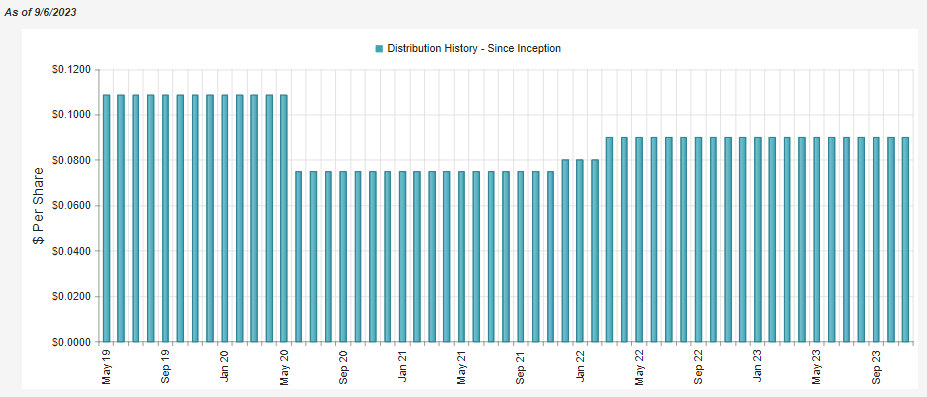

Attractive Distribution

While an investor waits for the underlying portfolio to pay off or the potential for the discount to narrow, the fund pays an attractive monthly distribution. Thanks to the large discount, the fund's share price has a distribution yield of 8.73%, while the underlying portfolio has to earn 7.12% to achieve that.

The fund did cut its payout during Covid but has since boosted it back up a couple of times. Though it remains under the pre-Covid level.

{kind=link}

When looking at distribution coverage, one of the first places we would look is at the net investment income.

{kind=link}

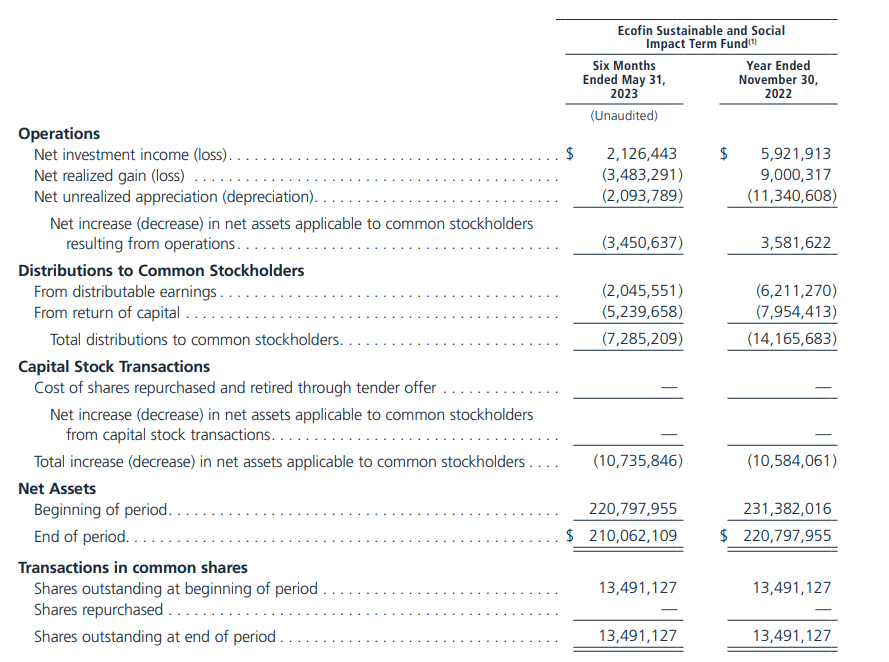

In this case, we'd see NII coverage come to 29.19%, which is fairly attractive for an equity fund. We would anticipate that capital gains would fund any shortfalls, at least as long as they are investing successfully. However, for a fund that holds energy investments, NII really isn't enough to look at.

Some of the underlying portfolio companies will pay distributions classified as return of capital. These cash flows are subtracted from the NII figure. In the case of TEAF, in the first six months of the fiscal year, they had ROC distributions of $1,217,856. When we include that in the NII, we would get the distributable cash flow ("DCF"), and that provides higher coverage of nearly 46%. Again, that's not bad for an equity CEF, as most coverage isn't even that high.

To help produce more potential capital gains, the fund also writes options. That wasn't an overly large contributor to the fund for the first six months of the year at only $46,486. Although that did help negate some of the losses in the underlying portfolio, it wouldn't have really been a meaningful amount as total net assets were down around $3.451 million in the six-month period.

In a previous update earlier this year, we touched on the tax classifications of the distribution. Here is the recap:

With return of capital distributions it receives, it's only natural that some of the distributions that TEAF pays will also be classified as return of capital. This means that not all of the ROC we see in TEAF would necessarily be considered "destructive" ROC.

TEAF Distribution Tax Classifications (Tortoise (highlights from author))

{kind=link}

TEAF's Portfolio

TEAF has been fairly active in the first half of its fiscal year, with a turnover rate of 16.51%. Compared to last year, the entire fiscal year saw a turnover rate of only 18.08%. However, that had moderated out from fiscal 2021's turnover rate of 68.31% and 2020's turnover rate of 73.22%. So, it seems they have become more settled in how they want to be positioned.

The fund also hadn't invested in any new private deals since April 2023 , when they invested in Belton Preparatory Academy and Libertas Academies. Both of those belong to the social impact category as they are schools. They were also fairly small debt investments but paid off some high cash yields of 11% each.

The weighting of private vs. public has also shifted quite a bit since the end of April 2023. At that time, the weighting came to 59% public and 41% private.

TEAF Private Vs. Public (Tortoise)

That being said, this 50/50% is actually closer to what we've seen in our previous updates, and the difference in the last update was more of an anomaly.

In the semi-annual report, they noted that they had two realizations in the first half of their fiscal 2023. The first was a debt investment to St. James Christian Academy that was originally invested in October 2019. They received more favorable financing as this debt was at a rate of 12% to TEAF. It was a fairly small investment, but the investment was called at par.

The second investment was a sizeable debt investment of $8.11 million they participated in April 2021 to Dynamic BC Holding LLC. This is a waste-to-energy facility, and the cash yield on this debt was 13.5%.

This was not callable until 2026, but "the team negotiated a $108 price in exchange for the ability to retire this debt." The team not only pulled in an attractive yield, but they also saw some capital gains on this debt investment as they would have received $8,758,800 back.

Dynamic BC Holding could have also contributed to the temporary shift in the fund's public/private weightings at the end of April, explaining why we saw a shift in the weightings.

Now that the portfolio is getting a bit older, it'll be interesting to watch how these deals start to change or come to a conclusion. So far, the team is off to a fairly strong start.

Overall, the fund remains invested heaviest in sustainable infrastructure, with the social impact category and energy infrastructure still at meaningful weightings. These weightings were fairly consistent with what we've seen previously - despite what was a shift in the public/private weightings since our last update.

TEAF Asset Type Weighting (Tortoise)

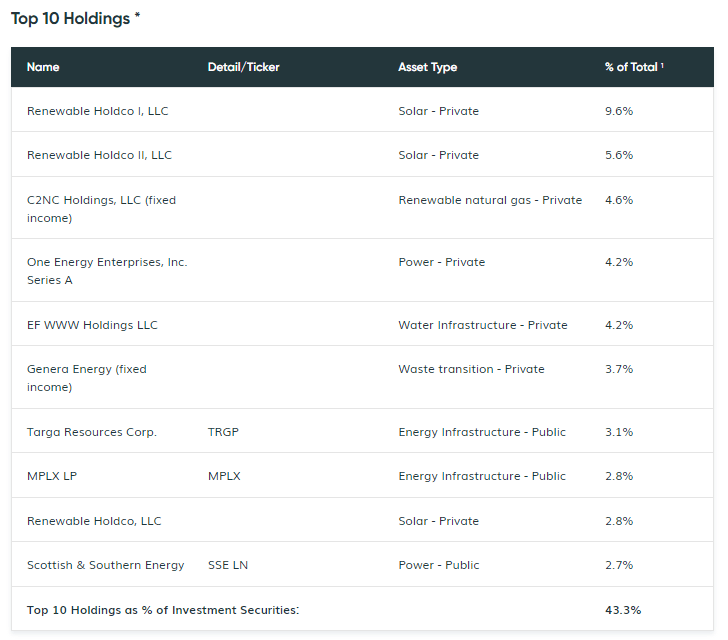

In looking at the top holdings, we see very little change. The portfolio is still quite top-heavy and concentrated in their "Renewable Holdco" positions.

{kind=link}

As a reminder, these are the largest contributors to the level 3 securities; they are also affiliated investments as they are wholly or majority-owned investments of TEAF.

As of May 31, 2023, TEAF has committed $63,739,819 to TEAF Solar Holdco, LLC, a wholly-owned investment of TEAF. TEAF Solar Holdco, LLC wholly owns each of Renewable Holdco, LLC and Renewable Holdco I, LLC, which owns and operates renewable energy assets. TEAF Solar Holdco, LLC owns a majority partnership interest in Renewable Holdco II, LLC. Renewable Holdco, LLC and Renewable Holdco II, LLC's acquisition of the commercial and industrial solar portfolio is ongoing. Renewable Holdco I, LLC acquired the commercial and industrial solar portfolio in September 2019.

Conclusion

TEAF continues to trade at a deep discount. I don't suspect that the discount will disappear anytime soon, and there are even valid reasons for the discount. This investment is more unique than most other infrastructure closed-end funds, and it likely isn't going to be appealing to most. Despite that being the case, I believe the discount still represents a long-term opportunity for investors willing to take the risks. Being paid the distributions along the way certainly makes it more appealing to stay with the investment.

For further details see:

TEAF: A Unique Approach To Infrastructure And Attractively Discounted