TEAF - TEAF: Attractive Distribution Yield And Deep Discount

2023-06-09 13:33:06 ET

Summary

- Ecofin Sustainable and Social Impact Term Fund offers a unique blend of fossil fuels and renewables, with a focus on transitional energy investments plus other social infrastructure investments.

- The fund has a deep discount of around 20%, providing a potential opportunity for investors to initiate a position.

- TEAF's portfolio includes a mix of public and private investments in energy and social infrastructure projects, making it an attractive proposition for long-term investors seeking further diversification in their portfolio.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on May 26th, 2023

Ecofin Sustainable and Social Impact Term Fund ( TEAF ) is Tortoise's foray into the more transitional energy investment space. Tortoise was traditionally investing in the fossil fuel industries with their older closed-end funds. However, TEAF provides a blend of both fossil fuels and renewables. They also take a more unique approach than other infrastructure funds as they are split between public and private investments in material amounts.

Solar investments are expected to pass oil production investments in 2023 . So this is one investment that can play the transition while still being hedged to more traditional oil and gas energy players too.

Private investments can be both a good and a bad thing, as they can sometimes provide outsized returns, but valuations can always become a question. These private investments include plays outside of energy alone too. With a deep discount of nearly 20%, it would seem that some skepticism is priced into the fund. These types of discounts can provide an opportunity for investors to pick up a position while it's cheap.

It's also a term fund. While that term is a fair bit out, it should eventually mean that the discount is ultimately realized. The only question would be if it's at a higher price now as the share price rises to meet its NAV or if it'll be the NAV that falls to meet the share price.

Since our last update earlier in the year, returns have been essentially flat, with a total return of around 1%. The fund's discount has widened out just slightly since that update as well, which would have been pushing against the upward performance.

{kind=link}

The debt ceiling and the banking crisis have all generally caused weakness in the broader market. The exception to that is if you are a mega-cap tech stock, which those types of positions can't seem to get anything wrong and only go up.

This portfolio probably isn't for everyone. The private exposure and cyclical energy investments, on top of some leverage on the fund, can make it more speculative. Still, I believe with the fund's attractive discount and monthly distribution that can slowly return an investor's capital back over time, it's an attractive proposition.

The Basics

- 1-Year Z-score: -1.12

- Discount: -19.31%

- Distribution Yield: 8.61%

- Expense Ratio: 1.89%

- Leverage: 12%

- Managed Assets: $254.9 million

- Structure: Term (anticipated liquidation date around March 27th, 2031)

Tortoise launched TEAF with the goal of "attractive total return potential with emphasis on current income and uncorrelated assets." Additionally, "access to differentiated direct investments in essential assets" and "investments intangible, long-lived assets and services." TEAF is also targeting a "positive social and economic impact."

The fund's expense ratio is quite high at 1.89%. However, that isn't unusual for a fund that incorporates private investments. They utilize a mild amount of leverage, which increases costs and risks nonetheless. The total expense ratio comes to 2.17% when including the leverage expense.

The leverage the fund implements is very light, but with a more cyclical investment space, that's probably a positive. Of course, any leverage means that moves either up or down are amplified, and that means more volatility on top of the discount/premium in CEFs.

Additionally, the fund's borrowings are based on 1-month LIBOR plus 0.80%. As interest rates have been rising, so too have their borrowing costs. Having only a mild amount of leverage means that the increased burden is also relatively reduced in terms of rising borrowing costs. When including the leverage expenses, the fund's total expense ratio comes to 2.17% in its last fiscal year .

The sizeable 1.35% management fee largely drives the fund's expenses. Carrying so many private investments and flexibility in both equity and fixed-income investments often come with these larger management fees.

Performance - Deep Discount

Aside from the unique positioning of the fund, I believe the main selling point for the fund is currently the quite large discount. The fund launched in early 2019, so it really isn't considered to be such a new fund anymore. At the same time, while the discount was being reduced briefly through 2021 and even 2022, it has more recently started dropping back to some of the levels we saw in 2020.

Ycharts

In 2020, we also saw the spike lower as the pandemic caused many CEF discounts to spike similarly. At this time, the fund's discount is trading materially below its longer-term average - which is quite substantial on its own.

The fund's performance since inception is probably a driving factor in keeping the fund relatively uninteresting to investors. However, not all the standard timeframes of performance have been as ugly. The 3-year annualized results are quite impressive, which is getting a boost of being the post-pandemic bounce. Plus, this fund held up relatively well in 2022, when the broader market was hitting bear market territory.

{kind=link}

Distribution - 8.61% Distribution Yield Paid Monthly

The fund's current distribution yield is meaningfully higher than what the underlying fund has to earn. This comes about when a fund's discount is as deep as it is for TEAF. The NAV distribution rate comes to 6.95% based on the $0.09 paid per month. The fund's distribution policy is to pay a managed distribution in the target range of 6-8% on a trailing average NAV.

The fund was cut during Covid but has bumped up twice since then. It isn't back at the high watermark of its inception distribution. However, the NAV per share now is lower than at inception too. Since the fund's inception, they've paid (or will pay with the inclusion of the next distribution already announced) a total of $4.3505.

{kind=link}

The fund will require plenty of capital gains to fund this distribution. It isn't covered by net investment income alone, and that isn't that uncommon for a fund that invests in a more multi-asset approach with equities and debt investments.

That being said, when looking at the fund's net distributable income, which includes the return of capital distributions from MLP holdings, coverage is fairly strong compared to other infrastructure fund peers at nearly 75%. For example, Reaves Utility Income ( UTG ) has NII coverage of 22.47%, and Cohen & Steers Infrastructure Fund ( UTF ) showed NII coverage of 27.07%. That would primarily be thanks to the fund's exposure to various fixed-income investments.

Overall, TEAF is substantially different than UTG and UTF. So this isn't to say that either of those funds aren't worthwhile. I own both, I just wanted to provide some context of other infrastructure funds.

Since our last update, there hasn't been a new report, so the coverage numbers that we have available now are the same as we had previously.

That being said, we see that NII coverage comes to 41.8%, which is fairly strong for a fund with a high allocation to equities. Even further, the fund carries MLPs and other energy investments that traditionally distribute out return of capital. These ROC distributions can be added to the NII to come up with the distributable cash flow or net distributable income.

For TEAF, in their last fiscal year, ROC distributions were $4,599,443. When including that with the NII, we see that NDI jumps to 74.27%. That makes me more confident that they will keep the distribution where it is currently - though never guaranteed.

{kind=link}

TEAF's Portfolio

At the end of April 2023, the portfolio is currently split between 59% being allocated to public investments and 41% being allocated to private investments. This was a fairly material shift from earlier this year when it was 52% public and 48% private.

TEAF Portfolio Breakdown End of April 2023 (Tortoise)

This shift happened at some period through April because, at the end of March 2023, they had listed a split of 47% private and 53% public in their quarterly commentary .

TEAF Portfolio Breakdown End of March 2023 (Tortoise)

So a reason for this shift could be something to look out for in their next quarterly commentary or to see if it shifts back to the more normal range closer to a 50/50 split.

Back to looking at the fund's positioning at the end of April 2023, they list that sustainable infrastructure is the fund's largest weighting. This is then followed by social impact at 20% and energy infrastructure at 16%. The social impact is the allocation that adds a bit more oddity to the fund. It isn't just a pure-play energy infrastructure fund, but an infrastructure fund in a more broader sense that can include schools, healthcare facilities and other infrastructure investments.

TEAF Asset Breakdown (Tortoise)

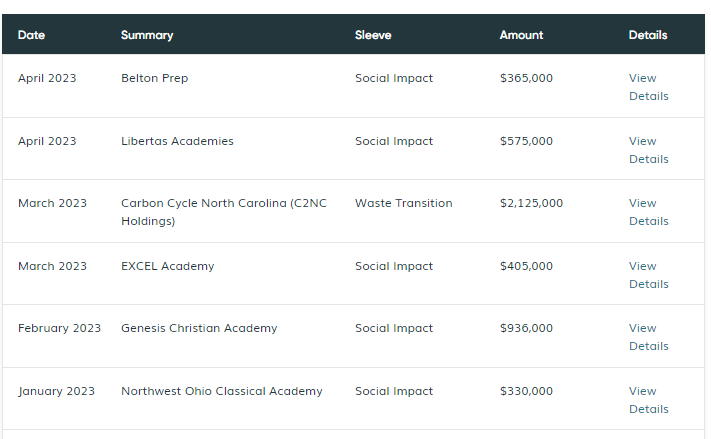

The managers have continued to be busy in 2023 , putting together private investments. In this case, this year included plenty of the social impact investments that set it apart from other infrastructure funds.

{kind=link}

Outside of the social impact category, we saw another investment in C2NC, the "waste transition" company. This wasn't their first investment in this project either. They previously invested $10.715 billion in 2020 subordinated bonds with a 13% yield.

This latest deal was another $2.125 million in subordinated secured taxable green bonds. The cash yield on this one comes to 14.5%, so we can see the impact of higher interest rates leading to higher yields playing out here too.

Now, at double-digit yields, this brings up a great point on highlighting the risks of some of TEAF's underlying holdings. Rock-solid companies with solid financials aren't issuing double-digit bonds just yet.

So, therefore, we can already presume that C2NC is going to be quite a risky play. And that assumption would be correct. This is actually not an operating project yet; it's still being built and "in the process of completing construction and commissioning a biomethane-producing waste-to-energy anaerobic digester plant in North Carolina." At this point, it has no cash flows but a lot of "ifs" and "potential."

Helping to support this operation is the fact that North Carolina has mandated energy companies have to have a certain portion of their fuel from animal sources. They also mention that there are only a fairly "limited number of participants." Meaning that this facility could see high demand. They also mention that the project "has contracts to sell all of the RNG to a regional utility company via direct injection into a pipeline that has an access point on the company's property."

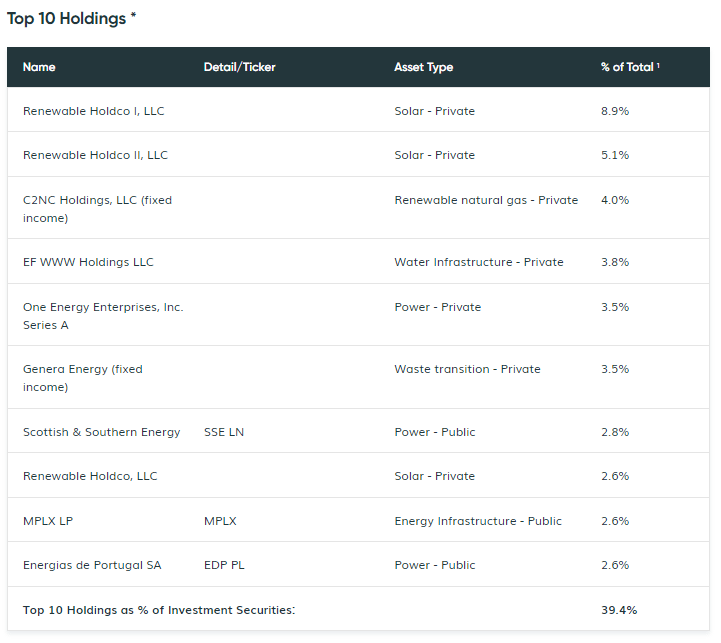

These are also the types of private investments that are classified as level 3 securities or can be restricted investments. At the end of their last fiscal year, they listed 24.5% of the portfolio as level 3 securities. Level 3 securities get valued on assumptions, as there isn't a liquid market to value the readily available securities. That leads to skepticism about the valuation of said investments and often leads to a fund being discounted - as we see with TEAF and plenty of other CEFs that invest in private investments.

The largest of these level 3 securities are TEAF's largest holdings. These are the affiliated Renewable Holdco LLC investments that are listed as their first, second and eighth largest holdings. These Renewable Holdco positions are held wholly or majority owned through the wholly-owned TEAF Solar Holdco LLC.

{kind=link}

They noted in their last commentary that they expect the last solar project that's under construction to "come online in summer 2023, after experiencing interconnection delays by the utility."

The EF WWW Holdings LLC is also partially owned by TEAF, where that position has provided a commitment of up to $15 million in debt funding to World Water Works Inc. On this construction note, the company pays monthly interest at an annual rate of 10.50%.

Conclusion

TEAF owns a unique mixture of securities that goes across both public and private investments. While exposure to energy investments in renewable and traditional are the primary weighting of the fund, other social infrastructure projects are also included. That sets this fund apart from most other infrastructure funds. They also invest across equities and various debt investments.

The fixed-income sleeve can generally provide more stability in terms of cash flow to the fund and, therefore, more predictable streams of income to pay the distribution. At the same time, these are riskier investments on their own, as a good portion of these are only projects or ideas and not currently generating cash flows.

Overall, TEAF has dropped to a substantial discount, and while there are plenty of risks to be aware of, the discount helps compensate for some of these risks. For a longer-term investor that can handle a riskier holding, TEAF is rather uniquely positioned to provide potentially opportunistic exposure.

For further details see:

TEAF: Attractive Distribution Yield And Deep Discount