THNPY - Technip Energies: Long-Term Value Drivers Overcome Current Challenges (Rating Upgrade)

2023-09-01 14:58:37 ET

Summary

- Technip Energies' outlook has brightened primarily due to its involvement in LNG expansion projects in Qatar.

- The company's TPS segment has become the primary value driver, with a strong backlog and growth in pre-FEED and FEED work.

- Despite weaknesses in project delivery and negative free cash flow, the LNG market's growth opportunities make the stock reasonably valued. Investors should "hold" the stock.

Technip To Hold Its Ground

I have been discussing Technip Energies N.V. ( THNPY ) in the past, and you can read the latest article here . The company’s outlook has brightened following the continued involvement in the second phase of Qatar NFE’s LNG expansion project. It is also involved in similar projects in the Americas and Africa. This has strengthened its TPS segment and created a healthy book-to-bill ratio for enhanced revenue generation. Currently, the company focuses on offering integrated post-combustion solutions in carbon capturing.

Despite some weaknesses in the project delivery segment, its EBIT margin improved in 1H 2023 due to higher volumes and the increased share of higher-margin products. However, its free cash flow remained negative, which muddles the balance sheet strength. Nonetheless, the LNG market’s growth opportunities should dispel the near-term worries. The stock is reasonably valued versus its peers. I would suggest investors “hold” the stock.

Strategy And Backlog

THNPY's H1 2023 Results Presentation

{kind=link}

THNPY plans to expand its lab network and digital capabilities through technology developments and product launches. Some of its primary target markets are carbon capture and ethylene decarbonization. In carbon capture, it has recently launched integrated post-combustion solutions - Canopy. This, combined with Cansolv, will be helpful for smaller industrial emitters to minimize operational downtime, de-risk project execution, and improve schedule. Cansolv is Shell’s (SHEL) CO2 capture system technology. Technip and Shell are collaborating on carbon capture projects. The emission reduction for small emitters is the largest contributor, representing 80% of all emissions in the U.S. and Europe.

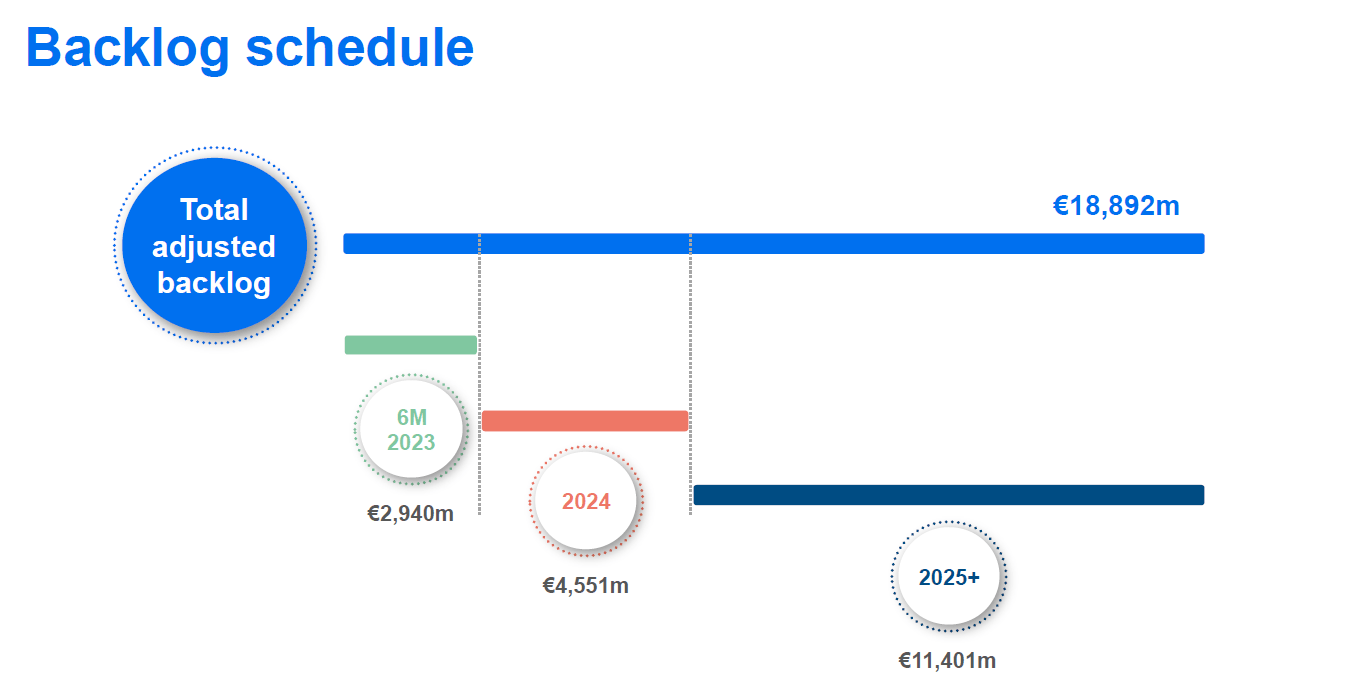

In 1H 2023, THNPY’s year-over-year backlog increased by 37% to EUR 16.8 billion, led by Qatar NFS. NFS represents the second phase of Qatar's LNG expansion project. The project involves a contract for two mega trains of 8 million tons per annum. According to the company’s estimates , the contract will result in THNPY participating in 35% of global LNG capacity under construction. It is also involved in similar projects in the Americas, Africa, and some parts of the Middle East. Its current backlog is ~3x FY2022 segment revenues, with a trailing 12-month book-to-bill ratio of 1.5x. This gives solid visibility into its future revenues.

TPS Segment Capability Builds

THNPY’s Technology, Products & Services (or TPS) segment has recently become the primary value driver. The company follows a hybrid model, combining a long-cycle project delivery business with a short-cycle solution. Its integrated post-combustion solutions – ‘Capture.Now’ would span across energy cycles. Also, it witnessed growth in pre-FEED and FEED work in various energy transition domains.

Starting in 2022, the segment has benefited from increased order backlog, especially large orders in renewable fuels. So, the year-over-year backlog in this segment has gone up by 80%. The company’s management appears confident it can double its FY2020 revenues from this segment to EUR 2 billion.

Natural Gas Market Outlook

{kind=link}

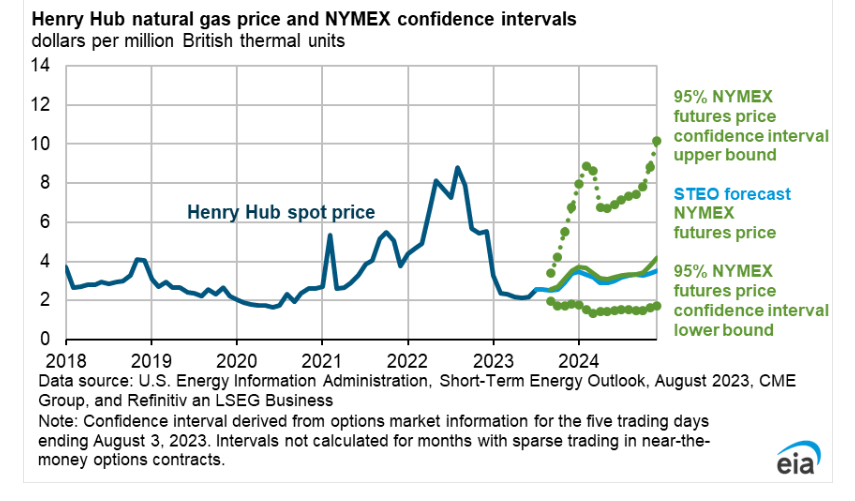

In the past year, the US natural gas price has decreased by 74% until the last week of August. Despite that, relatively steady crude oil prices supported higher dry natural gas production in 2023. Although natural gas-directed drilling fell, associated production increased. In 2024, the EIA expects natural gas production to remain steady.

1H Performance: A Segment Analysis

THNPY's 1H 2023 Results Presentation

{kind=link}

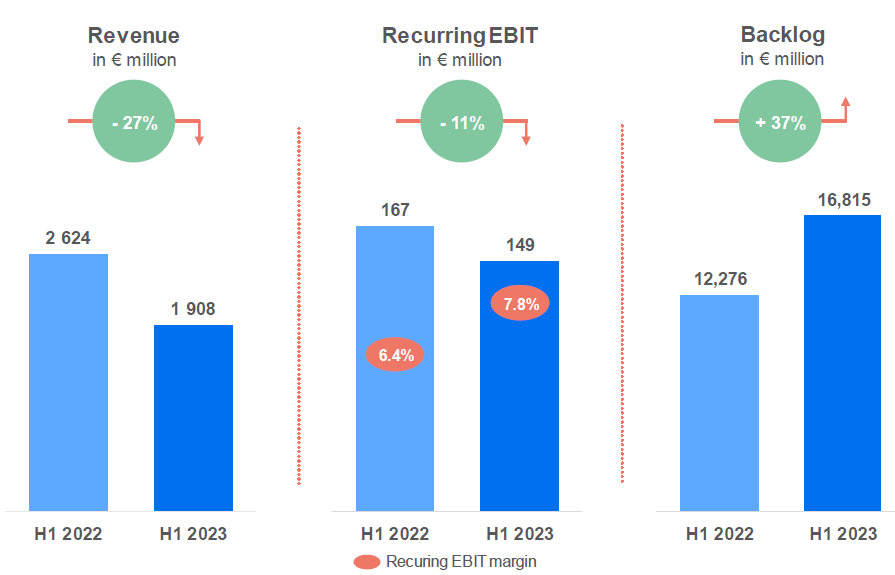

Technip Energies' revenues from the Project Delivery segment decreased by 27% from 1H 2022 to 1H 2023. However, the segment EBIT margin improved in 1H 2023. Revenues from the Technology, Products, & Services segment increased by 45% in 1H 2023 versus the year ago. Its EBIT margin remained resilient in 1H 2023.

Investors may note that the company’s revenues from project delivery slowed after its exit from the Arctic LNG 2 contract. However, the activity ramp-up in Qatar NFE and robust performance in the TPS performance. The year-over-year EBIT improved due to higher volumes and the increased share of higher-margin products in the TPS segment. I expect the rise in project backlog will lead to further margin improvement in 2H 2023.

Cash Flows and Balance Sheet

Technip Energies' cash flow from operations deteriorated sharply and turned negative in 1H 2023 compared to a year ago. Lower revenues and adverse changes in working capital led to a steep fall. Capex increased, too, during this period. So, free cash flow turned negative in 1H 2023 compared to a positive FCF a year ago.

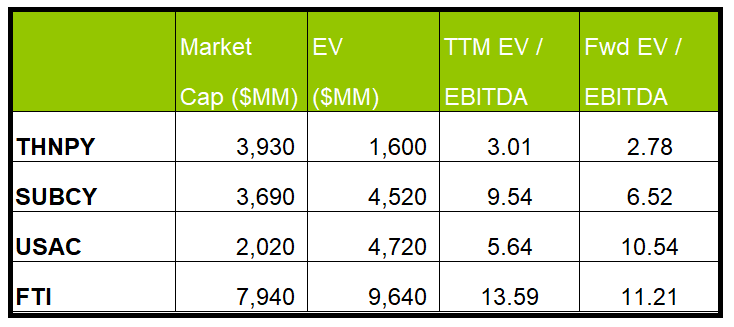

THNPY's debt-to-equity ratio (0.34x) is much lower than its peers' (SUBCY, USAC, FTI) average of 3x. As of June 30, 2023, its liquidity was €4.2 billion. So, robust liquidity ensures little financial risks. The company’s net debt was negative because of a significant cash & equivalents balance (€3.4 billion).

Relative Valuation

Author created and Seeking Alpha

{kind=link}

THNPY's current EV/EBITDA is expected to contract versus the forward EV/EBITDA multiple. This, however, is in contrast to some of its peers. This typically results in a steeply lower EV/EBITDA multiple. The company's EV/EBITDA multiple (3.0x) is much lower than its peers' (SUBCY, USAC, and FTI) average (9.6x). So, the stock appears to be reasonably valued compared to its peers.

{kind=link}

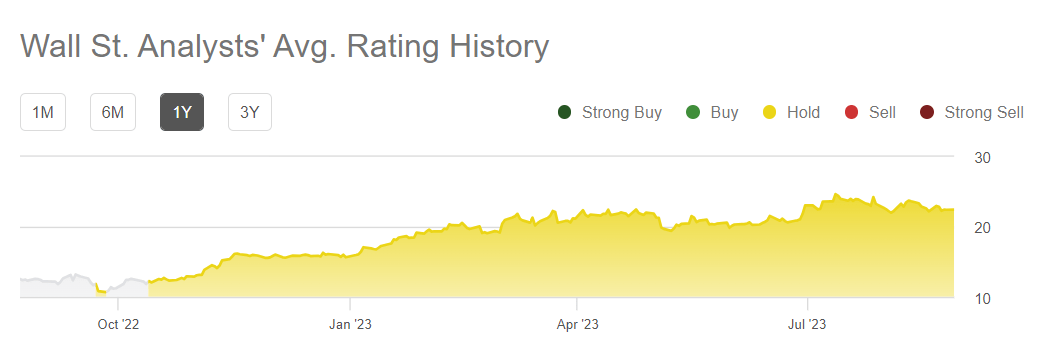

In the past 90 days, one sell-side analyst rated THNPY a "buy." None of the analysts rated it a "hold," while one rated it a "sell." The consensus target price is $20.7, suggesting a 9.5% downside at the current price.

Why Do I Change My Call?

I was relatively bearish about THNPY’s near-term outlook in my previous article. Its backlog had declined, and natural gas had suddenly turned south. Cash flows presented a concern to the investors. Its stock price climbed sharply. These negative factors mitigated the positive transformations impacted by carbon-capturing and modularized mid-scale energy construction resources. I wrote :

The company's backlog took a hit in FY2022 following the loss of the Arctic LNG 2 project and can get even lower in FY2023. Free cash flow dipped severely in FY2022, although working capital may improve in FY2023. Given the short-term headwinds, I expect the stock to turn slightly bearish in the near term.

After 1H 2023, THNPY’s year-over-year backlog increased significantly, especially following Qatar's LNG expansion project. It also witnessed growth in pre-FEED and FEED work in various energy transition domains. It has robust liquidity, which should offset the cash flow risks. Given the relative valuation, I upgraded it to a “hold.”

What’s The Take On THNPY?

{kind=link}

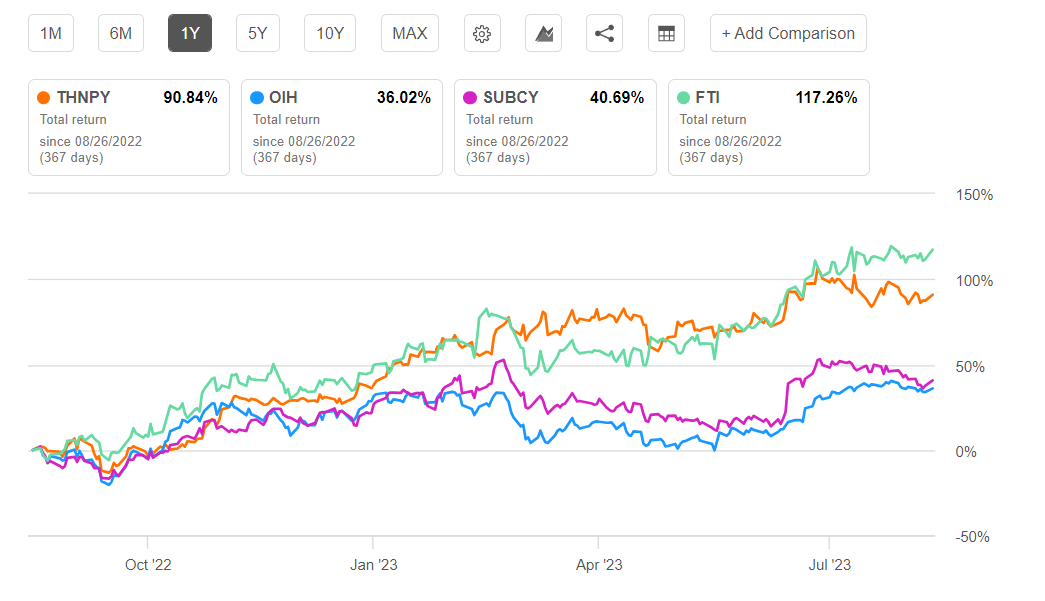

After 1H 2023, THNPY’s TPS segment has recently become the primary value driver. It has made investments in carbon capture and ethylene decarbonization. Its integrated post-combustion solutions span energy cycles in the LNG market. Higher LNG production and export capabilities in the Middle East led to pre-FEED and FEED work growth. So, the stock outperformed the VanEck Vectors Oil Services ETF ( OIH ) in the past year.

In 1H 2023, the company’s Project Delivery segment weakened. The natural gas price has decreased by 74% in the past year, raising doubts over the sector's near-term outlook. Its free cash flow remained negative, which muddles the balance sheet strength. Given the stock is reasonably valued and the industry provides the necessary momentum, investors should “hold” for an upside in the medium to long term.

For further details see:

Technip Energies: Long-Term Value Drivers Overcome Current Challenges (Rating Upgrade)