ORCL - TechTarget: No Upside Likely In The Near Future

2023-05-29 03:38:07 ET

Summary

- TechTarget combines sales and marketing data to help IT vendors identify potential buyers of IT products.

- The management has lowered its revenue guidance for the fiscal year 2023.

- TTGT's revenue growth has fallen behind the market's growth rate.

- I assign a sell rating to the stock until there are signs of revenue acceleration driven by management's execution on targets.

Investment Thesis

TechTarget, Inc. (TTGT) combines sales and marketing data to assist its clients, primarily large and rapidly growing IT vendors, in accurately identifying potential buyers of IT products. Over the course of 20 years, TTGT has built a valuable source of first-party intent data, leveraging more than 150 websites covering 5,000 IT-related topics. However, TTGT's historical and projected revenue growth appears to be lagging behind the market's growth rate, and the deterioration in the macroeconomic outlook has further posed challenges for the company's growth. Hence, I assign a sell rating to the stock until there are signs of revenue acceleration driven by management's execution on targets.

Q1 2023: Worsening Outlook

TechTarget released its first-quarter 2023 results and issued revised guidance due to the challenging macroeconomic environment. The management has lowered its revenue guidance for fiscal year 2023, now expecting a range of $225 million to $230 million compared to the previous midpoint estimate of $260 million. The new guidance indicates a 24% decline in revenue at the midpoint. The projected EBITDA margin for the fiscal year 2023 has also worsened, with management now anticipating a 30% margin for the year, down from the previous estimate of 35%, despite cost savings resulting from the previous round of job cuts. The company's profitability margin outlook is weaker, which may lead to another round of job cuts later this year. Like many other software companies, TechTarget emphasized in its shareholder letter the potential of leveraging artificial intelligence and its first-party intent data to enhance its prospects. Taking into account the updated guidance and a more pessimistic outlook, I remain bearish and assign a sell rating to the stock.

IT Industry Outlook

The increasing prominence of subscription-based models in technology purchases has created a more resilient revenue stream for global technology companies, which are important clients for TechTarget. Despite macroeconomic pressures and challenges in securing new deals, technology spending is expected to remain relatively stable due to the crucial role of technology transformation. As per Gartner, the global software spending is expected to grow 12.3% in 2023.

In the case of TechTarget, management has noted a shift in their customer base over the past decade, with a move from predominantly hardware-focused clients to a more balanced mix that includes a growing number of SaaS and cloud-based solution providers. The transition to the cloud is much more predictable and more difficult to put on hold, as it would potentially eliminate any hypothetical tech-based advantage that the enterprise was trying to achieve. However, the management believes that IT vendors may need to pause or reduce their sales and marketing spending as larger technology companies prioritize margin preservation and improvement in anticipation of a potential recession.

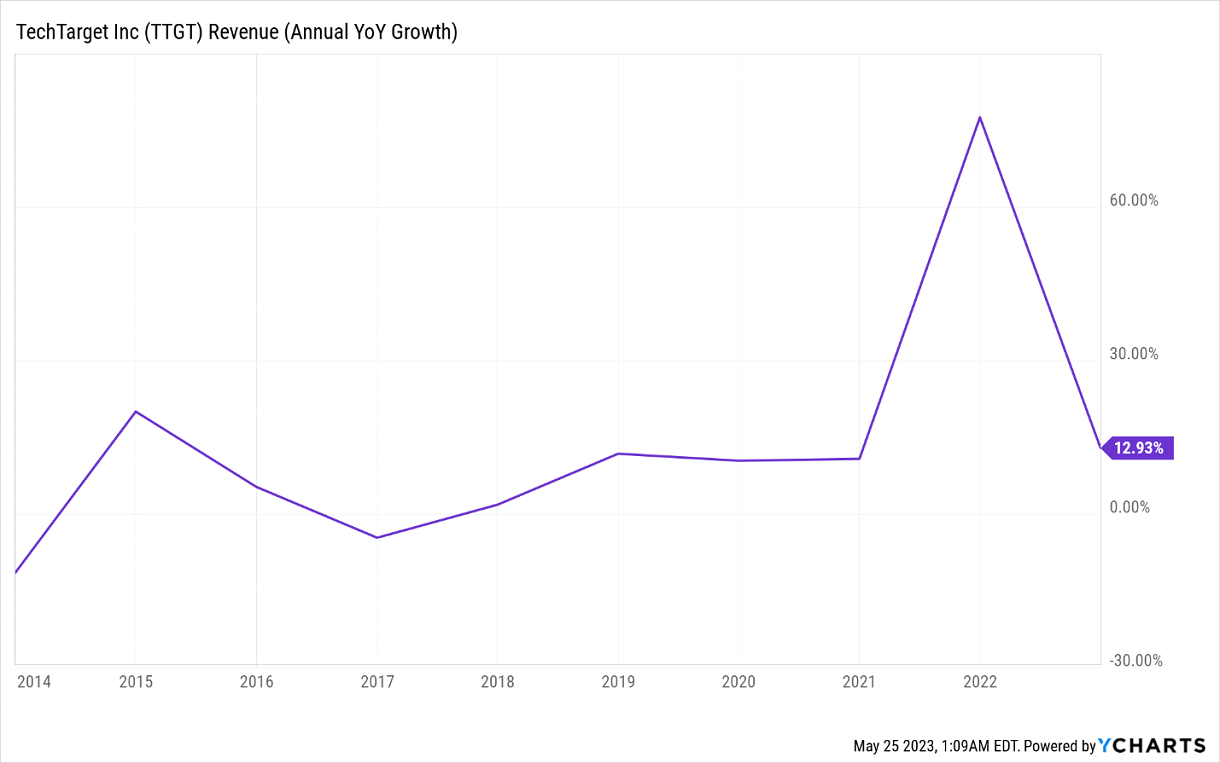

Lagging in a High-Growth Market

TechTarget's Priority Engine, a tool that offers purchase intent insights and integrates with sales and marketing platforms like Salesforce, is considered to be in competition with other account-based marketing ((ABM)) solutions. The ABM segment of the CRM market is expected to grow at a CAGR of 12% to $2.1 billion by 2030 from 750 million in 2021.

TechTarget does not seem to invest in next-generation sales and marketing software solutions that drive the growth of the ABM sector. The company also do not appear to be expanding into AI, ML, or automation solutions. For example, one competitor, 6sense, has integrated AI, big data and machine learning into its engagement platform, whereas priority engine still lacks those integrations.

Moreover, apart from Priority Engine and Content Enablement, TechTarget does not have other rapidly growing products. Over the past three years, TechTarget has allocated a small portion of its total sales to product development (R&D) and capitalizes on internal-use software and website development costs. The company's M&A strategy focuses on adding complementary products to enhance first-party intent data rather than on technology advancements.

YCharts

TechTarget faces competition from two main groups: large CRM software providers like Oracle Corporation ( ORCL ), Salesforce, Inc. (CRM), and Adobe Inc. ( ADBE ), who benefit from vendor consolidation, and niche players offering more technologically advanced solutions. Compared to these competitors, TechTarget's solutions are not seen as competitive and are perceived to be falling behind in terms of industry innovation.

{kind=link}

Valuation

TTGT currently trades at 3.9x 2024E EV/ Sales, which is broadly in line with median valuations for a group of profitable software application peers ([[ZI]], CRM, [[DNB]], [[ZD]]). I see the current valuation of TTGT as slightly overvalued given what I view as an unexciting revenue growth outlook, subsequent market share losses and low top-line visibility (considering that its share of long-contract-based revenues is relatively small compared to the broader software peer group average). My December price target of $26 is based on a forward EV/Sales multiple of 3x applied to the consensus revenue estimate of $244 million.

Seeking Alpha

Risks to Upside

TechTarget aims to accelerate the transition of its revenues to a subscription model, with a long-term goal of surpassing a 65% share of subscription revenue (compared to 41% in 2022). If the company successfully achieves this shift, it could enhance revenue visibility and improve the overall quality of its business, potentially leading to positive outcomes for financial forecasts. Additionally, TechTarget is expanding its total addressable market ((TAM)) beyond its traditional focus on marketing departments within large IT vendors. The development of first-party purchase intent insights with CRM and sales applications has opened up new revenue opportunities.

Conclusion

TechTarget offers free technical content through its extensive network of owned websites and webinars, serving to educate users about digital technology and assist technology buyers in their decision-making process. The management's long-term objective is to enhance revenue visibility by increasing the proportion of subscriptions and long-term contracts, aiming to surpass the 41% revenue share achieved in 2022. However, despite the profitability, TechTarget's historical and projected revenue growth appears to lag behind the market, indicating a lack of market share gain, informing my bearish stance on the stock. I view TTGT stock as a sell currently until there are signs of revenue acceleration.

For further details see:

TechTarget: No Upside Likely In The Near Future