JBI - Tecnoglass: 2023 Construction Spending Forecast Contributes To Rising Growth Prospects

Summary

- After a strong Q3 report that beat both earnings and revenue estimates, the outlook for FY22 was further increased.

- Strong construction spending is forecast to continue in 2023 and especially in Florida and the southeastern US where TGLS receives most of its revenues.

- The stock rose more than 60% since January 2022 despite a difficult macroeconomic environment and appears well positioned for 2023.

When I first wrote about Tecnoglass ( TGLS ) it was shortly after Hindenburg Research had issued a short report in December 2021, warning investors to avoid this high growth glass manufacturer from Colombia with the following title intended to drive down the share price to support the company’s short position:

Cocaine Cartel Connections, Undisclosed Family Deals, And Accounting Irregularities All In One Nasdaq SPAC

In that report the “research” stated that the company was improperly benefiting from cartel connections in Colombia and undisclosed third-party relationships that were somehow inappropriate or possibly even illegal. For example, one excerpt from the report stated:

In 2019, Tecnoglass’ filings make vague reference to a new “subsidiary” focused on metal façade fabrication, called ES Metals. Tecnoglass’ 2019 annual report briefly explained under a section titled “Formation of a subsidiary” that ES Metals is “a Colombian entity in which the Company has a 70% equity interest”.

At that time, I had suggested that TGLS was riding the Florida construction wave that was occurring in February 2022, and I rated the stock a Strong Buy, especially after the share price plummeted following the issuance of the short report. The company responded to the accusations in the report, and after a sudden and severe price drop the stock quickly recovered. Since then, the stock has soared by over 60% while the rest of the market declined in 2022.

Seeking Alpha

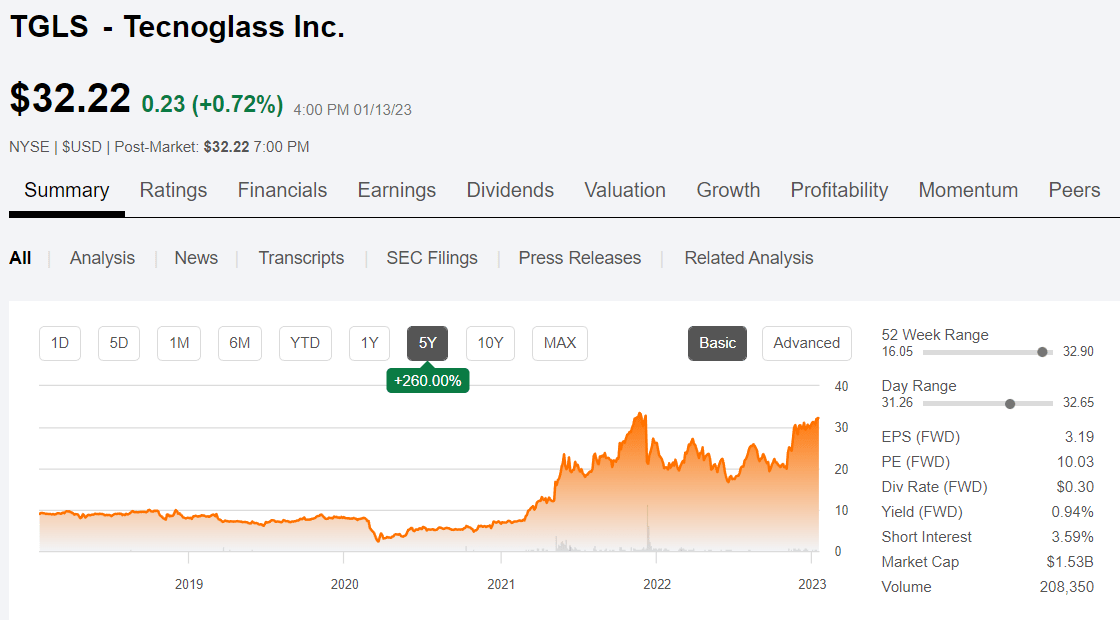

Then again in August 2022, I published an update on TGLS and again rated the stock a Strong Buy despite inflationary headwinds. At that time, the stock was trading for about $25 and has risen 27% since then, trading at a price of $32.22 as of market close on 1/13/23 and after having paid out a dividend of $0.075 and declaring another one in the same amount payable on 1/30/23. I summarized my review of the company at the time by stating:

With a strong balance sheet and good fiscal management, the company appears to be well positioned to take advantage of the low-cost, strategically located, vertically integrated operations, and reputation for quality that has grown for over 35 years to help them achieve the success they are seeing today.

Now it is a new year as we enter the second week of 2023 and two more quarters have passed with continued strong results since I wrote my latest update.

Q3 Earnings Results were Strong

On November 3, 2022 the company reported Q3 results and announced a beat on both the top and bottom lines and increased the outlook for FY22. The report included record quarterly revenues of $201.8M, a 53% YOY increase. Record gross margins of 52% resulted in record net income of $46.9M or $0.98 per diluted share.

In fact, the future looks even better as CEO Jose Manuel Daes commented in the press release:

"The strong efforts of our entire team led to another quarter of record results across nearly all metrics while operating through a complex macro environment. Demand for our high-performance architectural glass, window and aluminum products remains robust, with significant momentum in our single-family residential business, in addition to an acceleration in our commercial orders. We are set up to continue growing faster than the market as a result of our multi-year effort to diversify our business with new customers, products, end markets and geographies.”

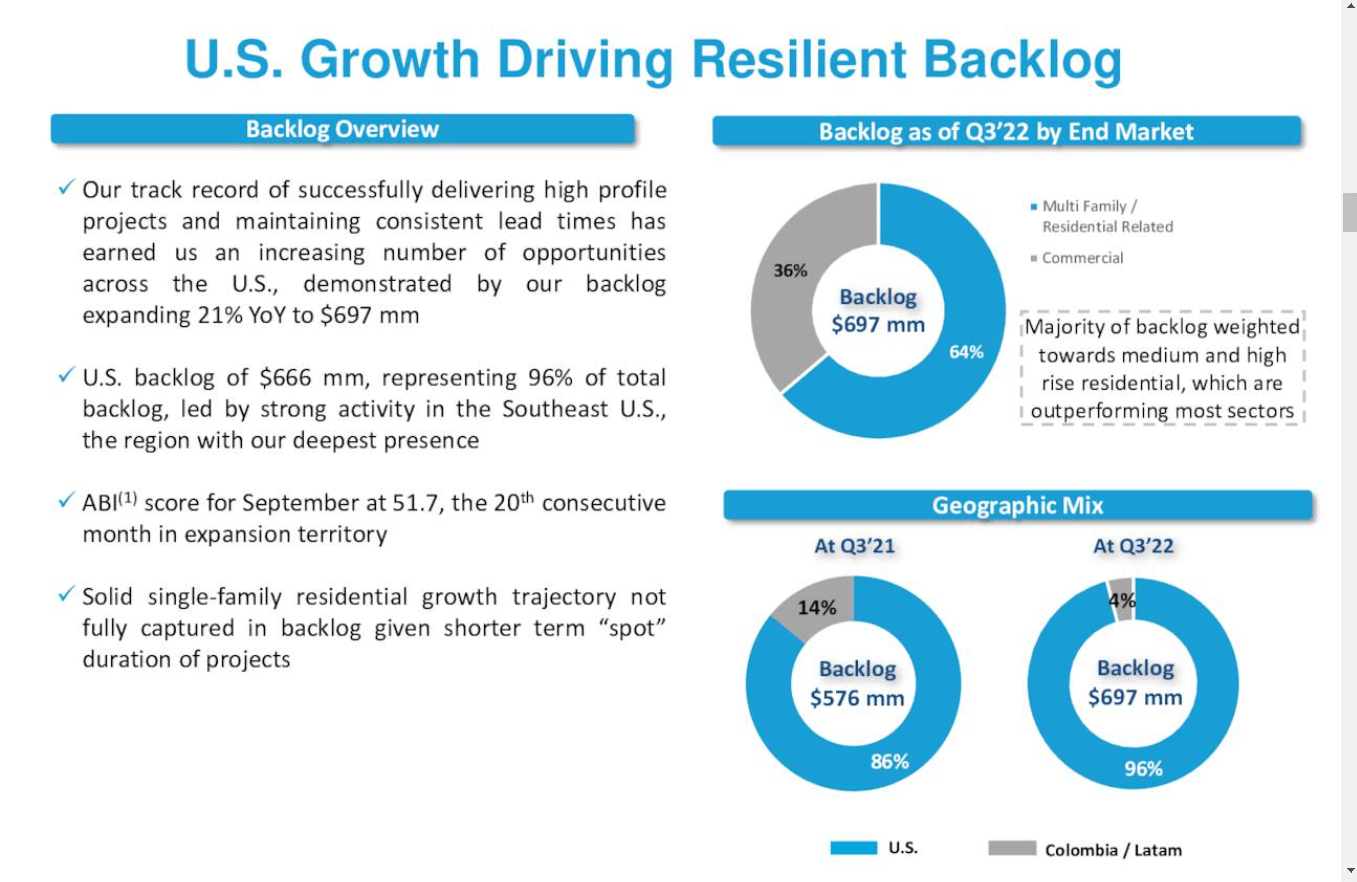

The backlog expanded by 21% YOY to $696.9 million. In addition, they updated the full year outlook:

- Increases Full Year 2022 Growth Outlook to Adjusted EBITDA of $240 Million to $255 Million on Total Revenues of $680 Million to $700 Million

The impacts of hurricane Ian are not expected to contribute to Q4 demand, however, there could be additional demand especially on the west coast of Florida later in 2023 as the rebuilding from the hurricane destruction begins to take shape, as explained by CEO Joe Manuel Daes on the Q3 earnings call transcript :

Well, when the hurricane passes, it takes a bit of time between the time that the government and insurance companies and the owners then together to how they're going to go about the replacement of the houses and the windows and whatever. We believe this quarter is not going to see any of that. We believe all that is for next year. So this quarter is already mostly sold. We believe for next year, we're going to see a lot of movement on the West Coast of Florida.

{kind=link}

Construction Forecast

The construction forecast for 2023 and the next several years looks strong and is likely to lead to continued strong growth for TGLS, who specialize in glass for high rise buildings such as condo towers and office or commercial buildings.

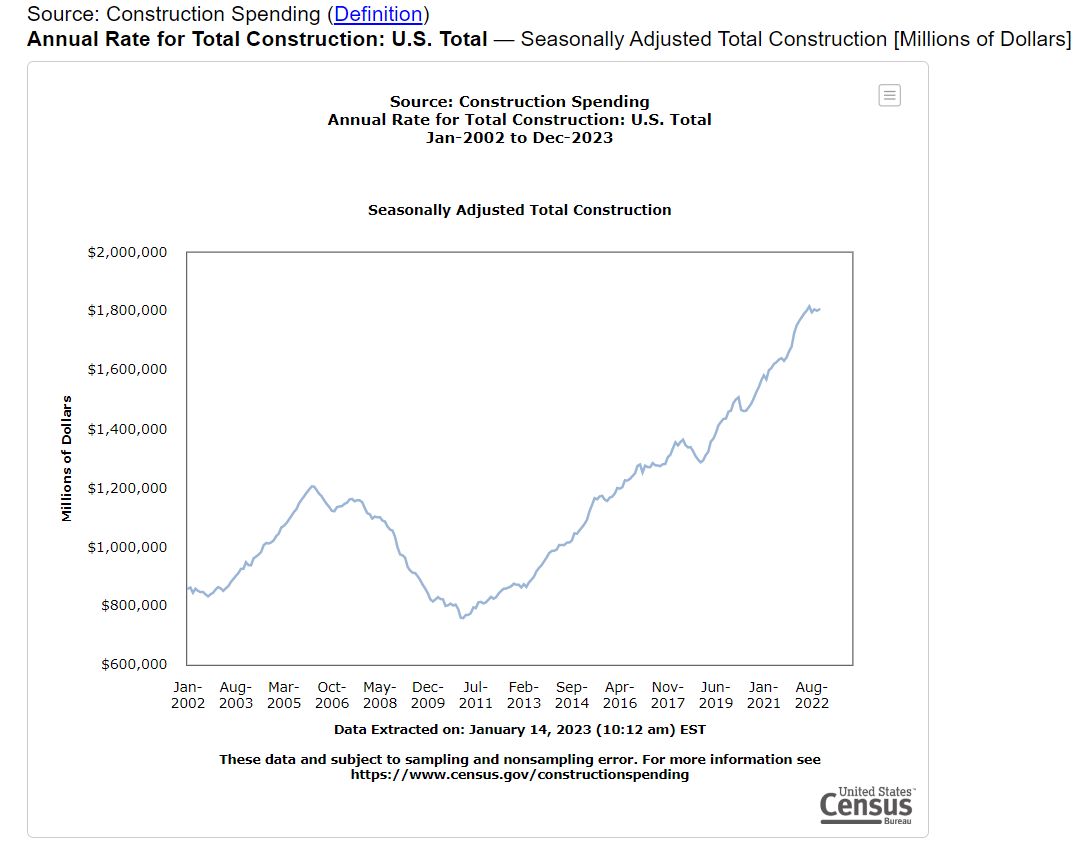

Annual construction spending in the US has been rising since 2011 and is expected to continue to rise even more over the next several years according to several forecasts. Data from the US Census Bureau shows the rise in total construction spending in the US through August 2022.

{kind=link}

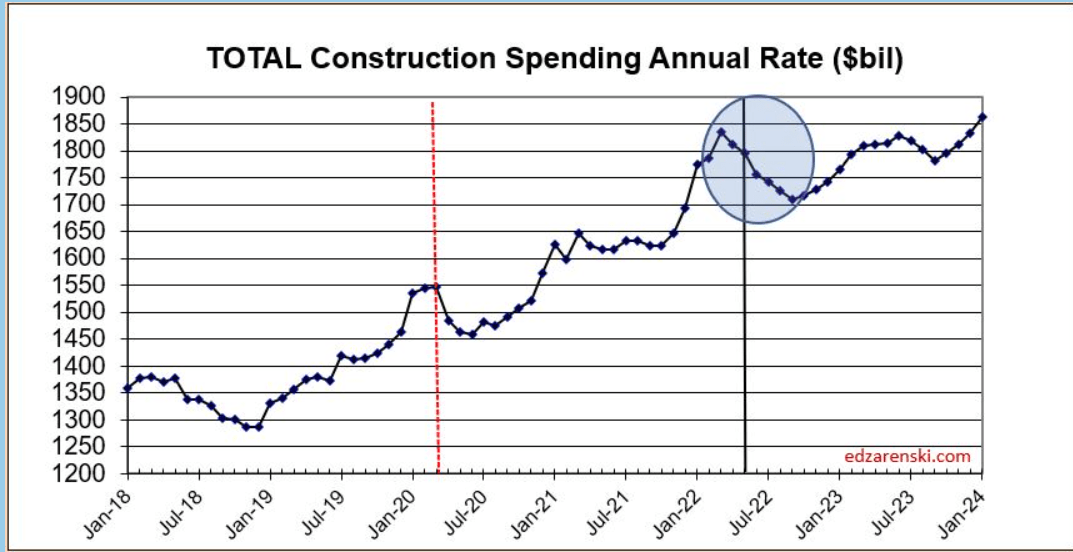

As of December 2022, based on a published forecast from Ed Zarenski, the construction spending for 2022 is still on track to increase over 2021 despite a pullback. Most of that growth is in non-residential construction.

Nonresidential Buildings Construction spending is on track to finish the year up 8% powered by a 23% increase in Manufacturing spending and a 17% increase in Commercial/Retail spending. Nonresidential Bldgs new starts are projected to finish up 22% in 2022.

{kind=link}

And despite Hurricane Ian and the impacts of rising inflation, higher interest rates, and ongoing fears of a recession in 2023 the outlook for Florida real estate, where TGLS earns the majority of its revenues, is still forecast to remain strong according to the Florida Realtors organization. Single family residential is a growing market for TGLS as well, and that end market could see additional demand increase once the housing market begins to recover later this year, as some predict.

Real estate professionals and economists say the Sunshine State will continue to be a powerful magnet for individuals, couples and families of all ages. That population growth, combined with a robust economy, puts Florida’s housing market in an excellent position for the new year.

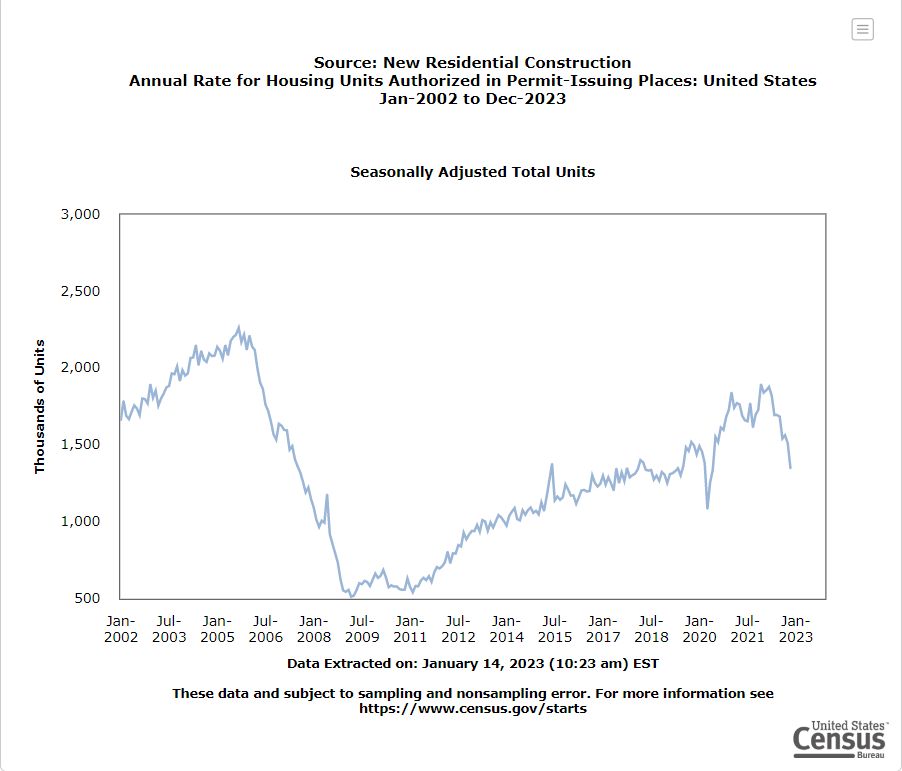

The general trend for new residential construction has been on the rise since 2011, with substantial pullbacks in 2020 and 2022. At some point, that trend is likely to reverse back to the upside as demand for new housing picks up again, whether that happens later this year or not until 2024.

{kind=link}

What’s Next for Tecnoglass?

On December 1, 2022, TGLS issued an updated growth outlook for the 2022 fiscal year. In that statement, the company increased the outlook to a range of $705 to $715 million in total revenues compared to the previous outlook that was expecting $680-$700 million. FY22 adjusted EBITDA is now expected to reach $255M to $260M.

“We look forward to delivering a fifth straight year of record Adjusted EBITDA, representing year-on-year organic growth of 72% at the midpoint, and exceptional cash flow," said CFO Santiago Giraldo.

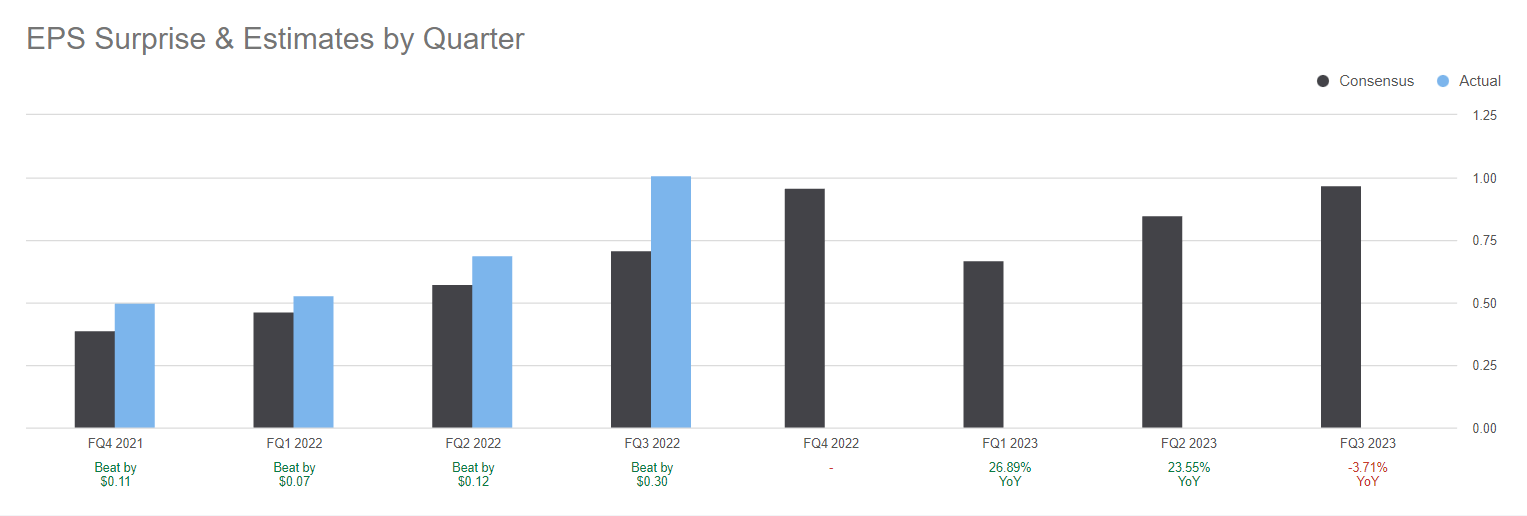

Revenues and earnings have been steadily increasing over the past 5 years and look to be continuing to rise as illustrated in this chart from SA on EPS Estimates and Surprises, which shows consistent EPS surprises over the past several quarters along with increasing revenues.

{kind=link}

All indications are that the fourth quarter 2022 is likely to exceed consensus estimates as well when the company next reports. The price of the stock has been steadily rising over the past year and a half after languishing for the previous several years and now appears to be poised for takeoff. Trading at a forward P/E of 10, TGLS has Strong Buy ratings from Wall Street, SA authors, and Quant ratings.

Seeking Alpha

Concerns over the company’s checkered past appear to be mostly in the rear-view mirror now as all indications are that the growth is likely to continue as margins improve and backlog increases even during a downturn in the economy. As the economy begins to recover and market sentiment appears to be turning more bullish in the early part of 2023, I expect that the stock price momentum will continue and shares will likely exceed the 52-week high of $32.90 before long. Looking at a 5-year price chart, it is obvious that the market is starting to reward the company for its solid growth and that the prospects for future capital appreciation are good, barring any unforeseen events.

{kind=link}

Risks to Consider

With the company being headquartered in Colombia there are some risks associated with possible geopolitical events, and potential currency risks depending on how the US dollar compares with the Colombian peso. According to CFO Giraldo, approximately 65% of costs are in US dollars and 35% in pesos. With about 96% of revenues coming in the form of USD any weakness in the peso is beneficial to the bottom line. If the dollar begins to weaken against the peso that could pose a potential risk to future margins. For now, the weaker peso is a tailwind for the company’s bottom line.

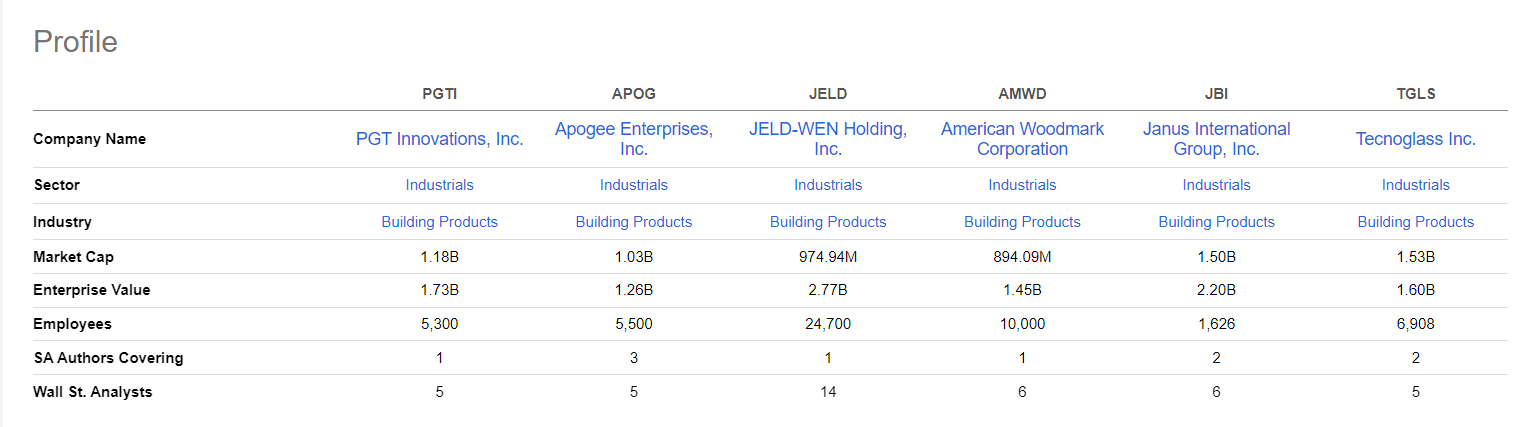

Competition in the industry is another factor to consider and I briefly mentioned that in my previous article. I discussed PGT Innovations ( PGTI ), as one possible competitor to consider. There are a couple other companies shown as peers on SA including Apogee Enterprises ( APOG ), JELD-WEN Holding ( JELD ), American Woodmark ( AMWD ), and Janus International ( JBI ).

{kind=link}

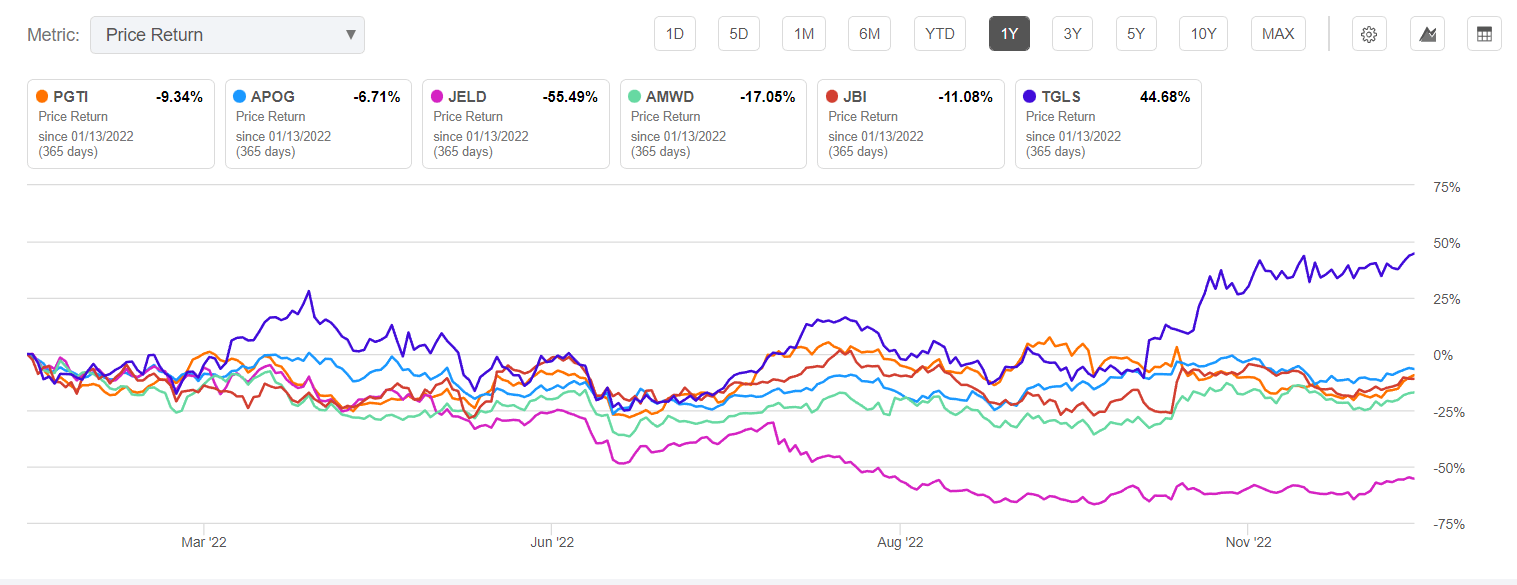

When I reviewed the Peer summary price chart TGLS clearly currently stands out above the rest based on performance in 2022.

{kind=link}

Concluding Thoughts

While TGLS has been growing revenues and paying down debt, they are also vertically integrated with relatively low costs for labor, transportation, and raw materials. These structural advantages offer shorter lead times than the industry standard and unlocks opportunities for continued market gains and expansion. The company has no significant debt maturities until 2026. The leverage has been improving and currently sits at less than 0.4x net debt to adjusted EBITDA. The company anticipates strong cash flow from operations and is growing capital expenditures to increase manufacturing capacity in order to accommodate the increasing demand.

I believe that TGLS is a Strong Buy at a price under $30 and based on a conservative multiple of 12x expected 2023 earnings of about $3.50 per share the price target by the end of 2023 could easily reach $42. If the earnings estimate for 2023 increases as I expect due to the rising demand and increased capacity a more optimistic price target might be closer to 12x earnings of $4, or as high as $48 by the end of the year, representing about 50% upside from the current price.

For further details see:

Tecnoglass: 2023 Construction Spending Forecast Contributes To Rising Growth Prospects