TK - Teekay Corp.: Discounted Price Leaves Appealing Investment Opportunity

2023-11-15 19:51:33 ET

Summary

- Teekay Corporation's stock has been steadily climbing and outperforming the broader markets, with a return of over 60%.

- The company's value is discounted compared to its equity, with a potential upside of $18.6 per share.

- Teekay is experiencing growth and generating robust free cash flow, allowing for share buybacks and increasing shareholder value.

Investment Rundown

The share price of Teekay Corporation ( TK ) has been on a steady climb upwards and heavily outperformed the broader markets at a return of over 60%. The quite recent results that the company posted were strengthened by the consolidation of Teekay tankers ( TNK ). It's important to mention that TK still has control over TNK through its supervoting class B shares. The stock has showcased some volatility over the past few months but I think the upward trend will continue as the market for fleets has been volatile. Rates seem to have peaked during the supply chain issue period some time ago. The spot rates are down nearly 50% for some but I think most investors didn't see those levels as something that could be sustainable for a long period.

Where I see the value in TK comes a lot from the fact it seems still quite discounted compared to the amount of equity it has, over $1.6 billion in total using the last 12 months' results. Just from an equity per share valuation, we get $18.6, indicating a significant upside potential from here. I am rating the company a buy despite the run-up the last couple of weeks.

Company Segments

TK is involved in global crude oil and marine transportation services on an international scale. The company possesses and manages a fleet of crude oil and refined product tankers, offering ship-to-ship support services, tanker commercial management, technical management operation services, and various operational and maintenance marine services. With approximately 54 owned and chartered-in vessels as of March 1, 2023, TK plays a significant role in the maritime industry, catering to the transportation needs of crude oil and related products worldwide.

{kind=link}

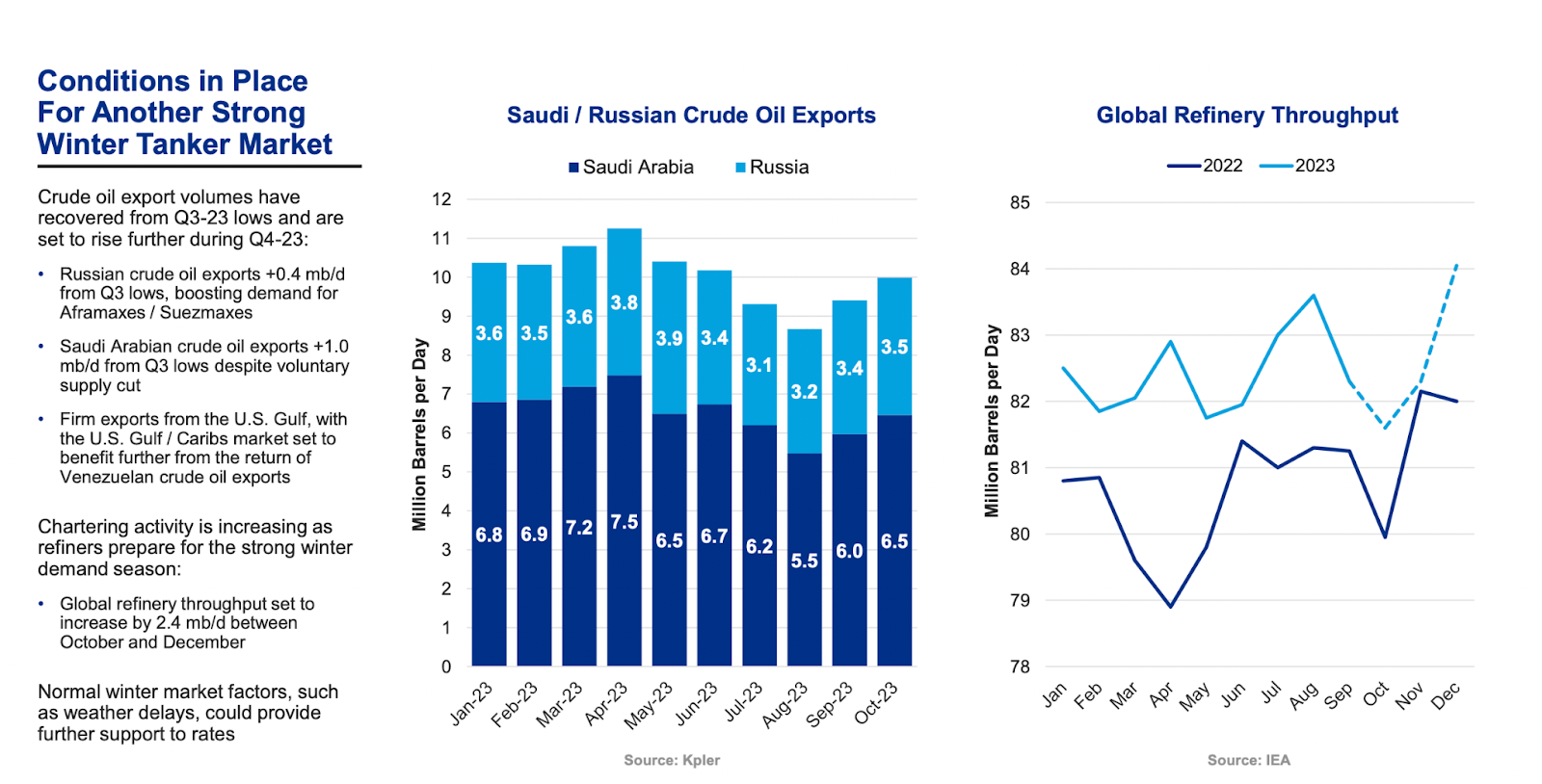

Market Conditions (TNK Presentation)

Right now there are strong fundamentals supporting another solid 6 months or so for the tanker market and that may be why shares of TK have soared over the last 12 months. Exports are seemingly on the rise again and that will drive higher utilization and demand for tankers. We will dive deeper into the last quarter's results for TK below, but one trend that was spotted is higher revenues despite softer spot rates. Revenues climbed decently at 2.6% YoY and even more during the last 9 months, up 41%.

{kind=link}

Cash Flows (Earnings Report)

Where TK has been appealing to investors as well is the amount of buybacks they are doing. Earlier this year they announced an additional $25 million of capital has been authorized to use for share buybacks. The last program has roughly $5 million remaining and since August 2022 the company has managed to reduce the outstanding share by over 10%.

Shares Outstanding (Seeking Alpha)

TK is experiencing substantial growth, with its value increasing by an estimated $0.15 to $0.20 per share monthly. This growth is attributed to the robust free cash flow generated by TK's stake in TNK. The net cash position of TNK serves as a stabilizing factor, mitigating potential management risks and contributing positively to TK's overall financial health and shareholder value. This FCF generation has been a key reason why TK has been able to buy back as many shares as they have done. Despite there being some consolidation of their stake in the company, I do expect there to be strong FCF generated going forward that will aid further buyback plans and bring shareholder value.

Earnings Highlights

{kind=link}

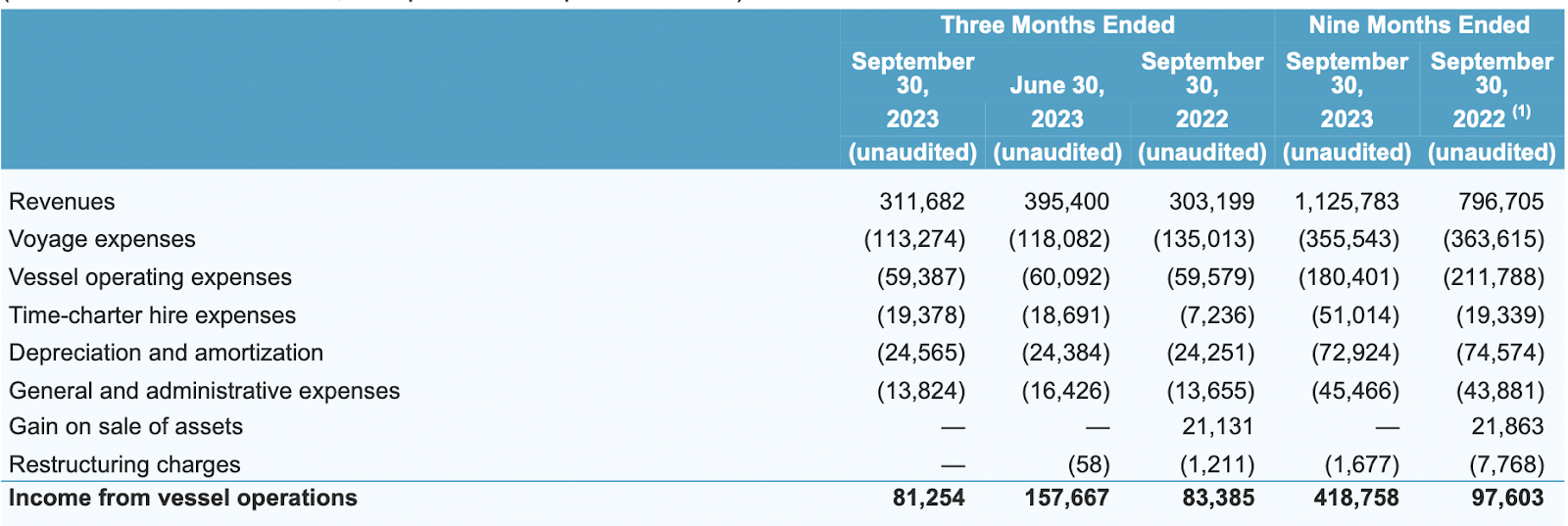

Income Statement (Earnings Report)

The last quarterly report that TK provided showed strength in my opinion as the revenues climbed YoY and the voyage expenses continued to decline further. This did not generate a YoY increase in the bottom line since the last quarter the company had a gain on sales of assets of $21 million which pushed incomes higher. When we don't account for that one-time gain, we instead see a YoY increase in income from vessel operations by nearly 30%. This is impressive and I think a key reason has been the flexibility the company has in terms of its contracts.

Spot Rates (Earnings Report)

The company does not have a majority of its rates fixed. This lends some more flexibility to the company and they can benefit from quick rises in spot rates and ultimately yield higher results as seen in the Q3 report. Going into the coming few reports I do think that TK can deliver a consistent increase in the top line. TNK did more in the last quarter did repurchase more vessels and YTD has bought back 19 vessels previously held under sale-leaseback arrangements. Furthermore, in the first quarter of 2024, it can buy back an additional 8, which I believe they will be doing too. This fleet expansion is something that has me bullish on the coming reports from the business.

Risks

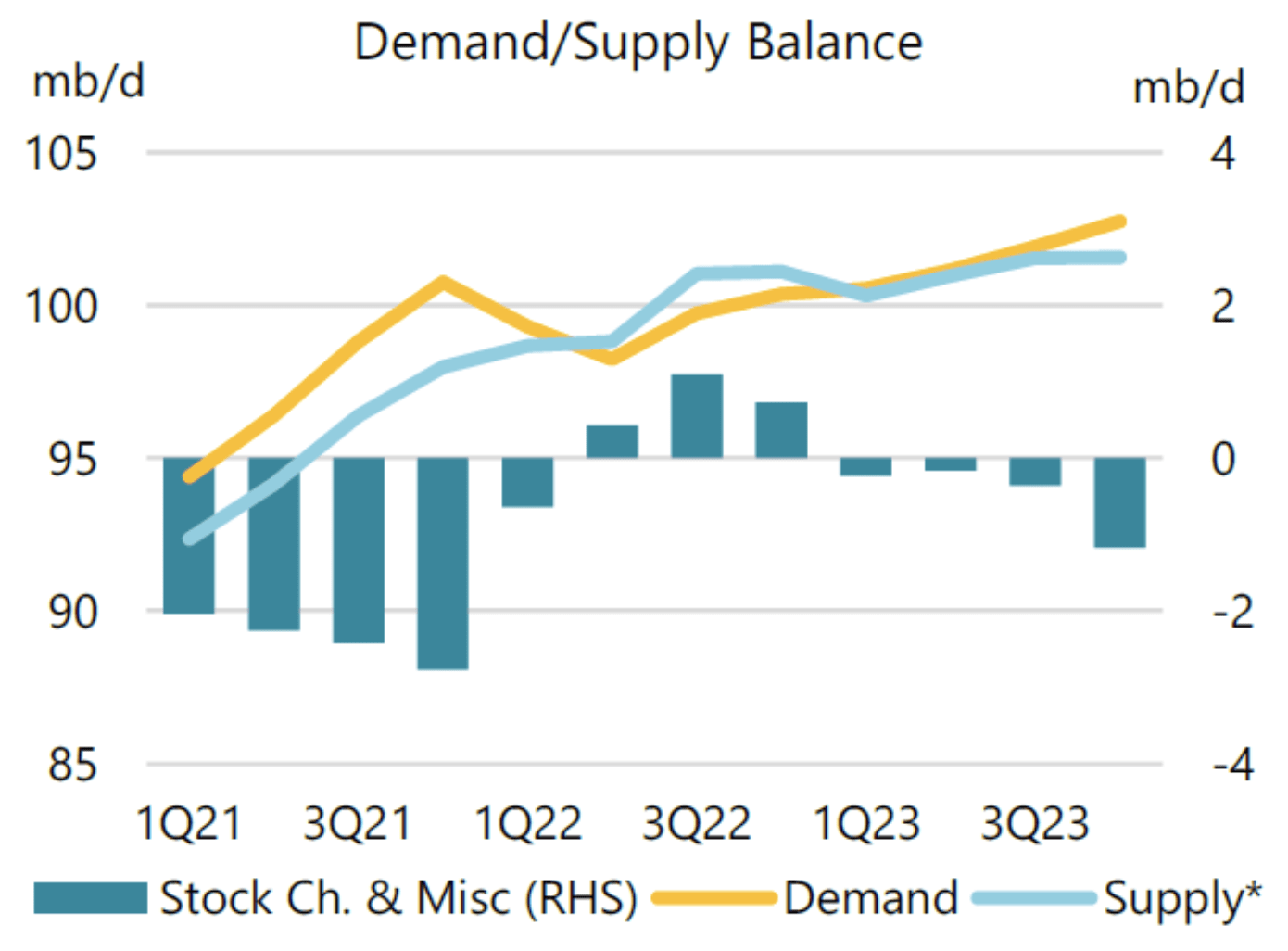

Traditionally, tanker stocks exhibit an upward trend alongside increased crude oil prices . However, the current market dynamics introduce a level of uncertainty, with swirling rumors suggesting that Saudi Arabia might implement supply cuts to elevate prices. If such cuts materialize, the demand for tankers could diminish. Compounding this, the industry is currently in its slowest season, and rates have experienced a significant decline in the latter part of Q3. In the event of additional supply cuts, there is a possibility that the market might perceive Teekay Corporation ( TK ) at a lower valuation due to uncertainties surrounding short-term demand.

{kind=link}

Demand And Supply (TNK Presentation)

Despite these short-term challenges, it's crucial to recognize TK's robust asset base, which positions the company favorably in the long run. While short-term fluctuations may impact the stock's performance, the underlying strength of TK's assets suggests that any downturn is likely temporary, and the company remains well-positioned for sustained success over the extended horizon.

Financials

{kind=link}

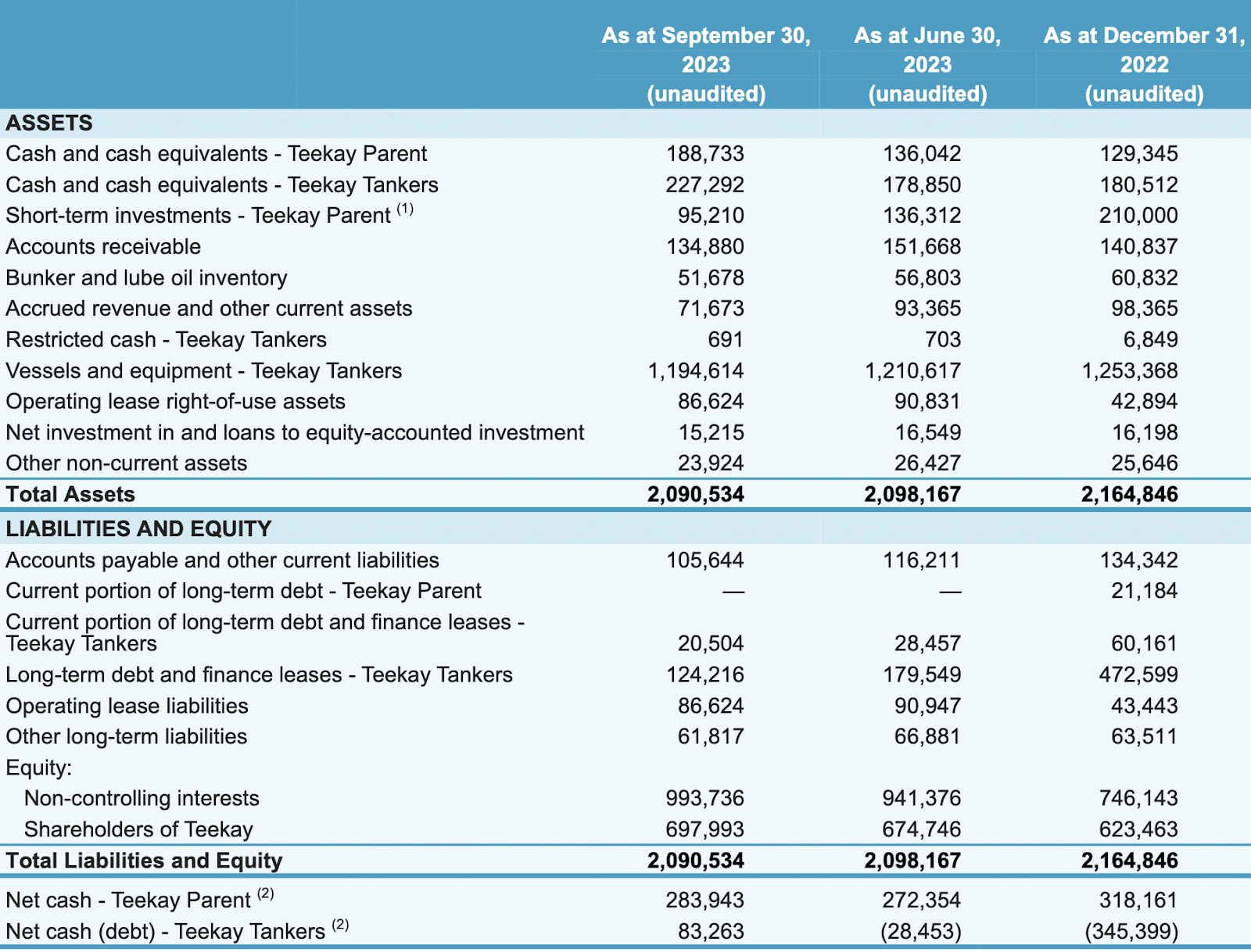

Balance Sheet (Earnings Report)

When we look at the balance sheet of the business I do think it poses a lot of quality right now as several improvements have been made. The consolidation of some of its stake in TNK has yielded a steadily climbing cash position for example, one that right now sits at $188 million, up from $129 million at the end of 2022. When accounting for the cash in TNK it reaches above $400 million right now. Since December 2022 there has been a decline in total assets though of about $100 million, partly because of the reduced short-term investments the company has on the books. I don't see this as something significant to worry about as the equity per share is still at $18.3 right now, indicating a pretty strong discount rate.

Valuation

Perhaps where I have been the most impressed is the debt the company has. The parent company, that being TK, has no current debts, but rather just $61 million in other long-term liabilities. With the cash position that has been highlighted, this seems easily managed. For TNK the long-term debt and finance leases have gone from $472 million at the end of 2022 to under $130 million, mostly due to the repurchase of vessels which has reduced finance lease costs. At the end of it, the equity for TK is at $1.6 billion right now, and with a market cap of under $700 million that is significantly under the current equity for the business, and investing based on a discount to actual equity value leaves a good opportunity here. I don't think TK exhibits any risks that would discount it by over 50% against equity value. Based on the current price this is an upside of 150% at least should it reach the $18 mark. The $1.6 billion in total equity together with negative net debt of over $200 million leaves a total value of $1.8 billion and with 100 million outstanding I arrive at the $18 target price mark. To balance this out a little bit, since I don't think we will see such a high jump in price unless there are rapid increases in spot rates that would catapult net income further, then we can look at the NAV instead. With $283 million in cash and cash equivalents and a $428 million stake in TNK, the net asset value reaches $711 million right now. With shares outstanding of 92 million as of the last report, we get an NAV per share of $7.72, or an upside of 7.7% in the immediate term. This is sufficient enough to justify a buy here in my opinion.

Final Words

The share price of TK has been on a very steady climb for the last 12 months and beating out the broader markets by a fair bit. Trends seem to indicate higher export levels and activity in the crude market and this could bring about higher spot rates for TK and result in even better net income results. I think the share price is discounted right now to a point where a buy case can be made. It's discounted based on NAV and equity per share to a degree where the upside is too good to pass up on. I think having some exposure to this market is beneficial to a diversified portfolio and will be rating TK as a buy as a cover the stock here for the first time, and look forward to following it further.

For further details see:

Teekay Corp.: Discounted Price Leaves Appealing Investment Opportunity