TGNA - TEGNA: Large Buyback Should Begin To Lift Shares In 2024

2024-01-08 21:27:53 ET

Summary

- TEGNA stock has underperformed due to failed acquisition and concerns about the future of television.

- TEGNA's geographic mix and political advertising revenue make it a likely beneficiary of the 2024 election cycle.

- TEGNA's strong cash flow, share buybacks, and potential for political advertising tailwind make its shares a buy.

TEGNA stock ( TGNA ) has been a terrible performer over the past year, given its failed acquisition and concerns about the future of television. Shares are also 10% lower than they were on September 14, 2021, the final day before rumors began circulating over TEGNA’s sale to Standard General for $24. After the deal was called off earlier this year, TEGNA launched a $300 million accelerated buyback alongside a $136 million termination fee paid in stock, though this has not done much for shares. It also increased its dividend by 20%. Given its strong cash flow and the fact that TEGNA should be a significant beneficiary of the election cycle, I view shares as a buy.

{kind=link}

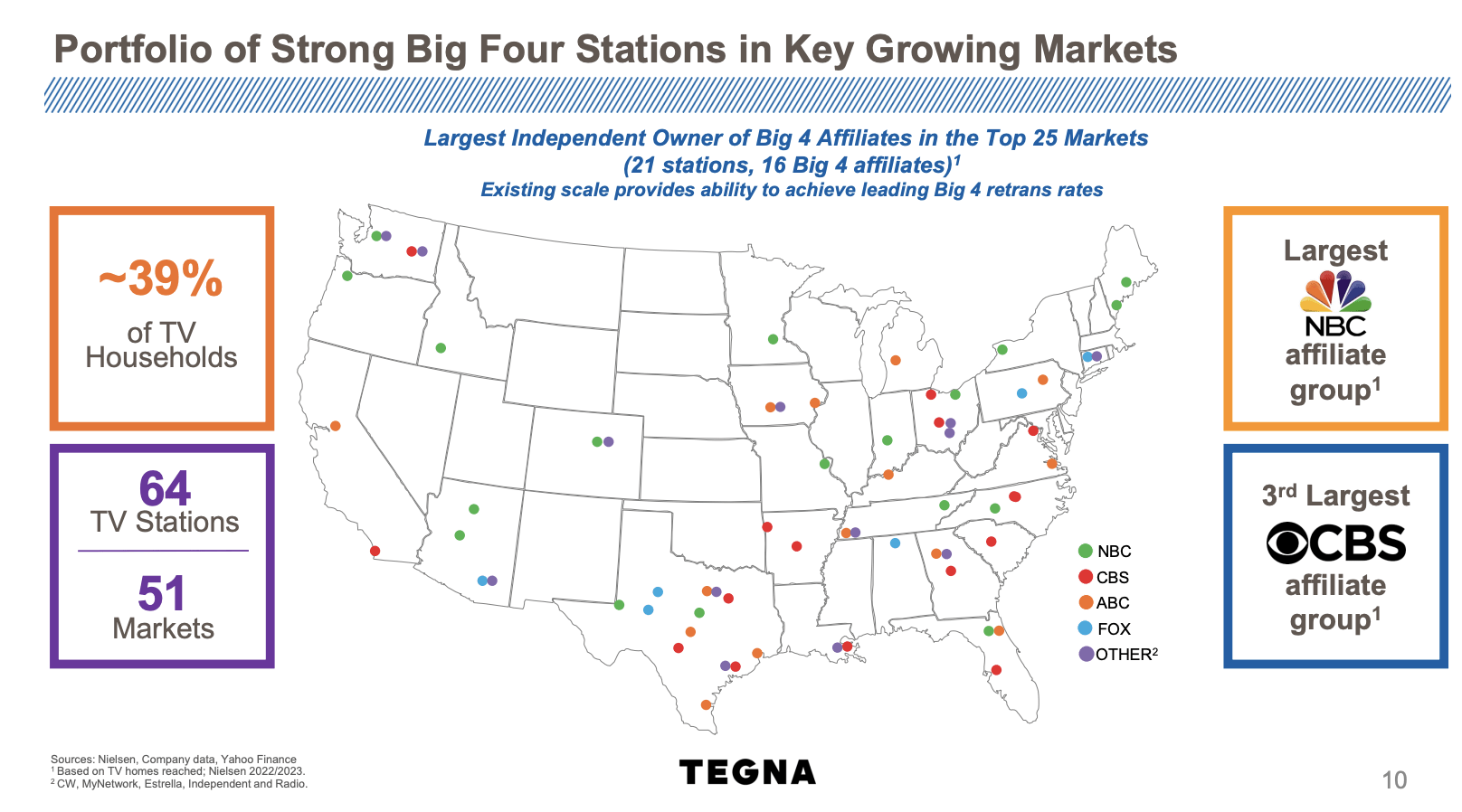

TEGNA is an owner of broadcast network affiliates. It owns 64 television stations, reaching 39% of television households. As you can see, it is spread across the country; however as I will discuss further below, I see its geographic mix as a material positive for the company in 2024 as the political campaigns begin ramping up spending.

{kind=link}

Because political campaigns spend substantial sums on local networks, TEGNA’s revenue and profits are quite volatile year to year. This was evident in the company’s third quarter , revenue fell by 11% to $711 million, primarily due to the absence of political revenue. Political revenue was down by $81 million. Excluding this, revenue was down by about 1.5%. Cost of revenue rose by 2% due to higher programming expenses while TEGNA kept G&A roughly flat.

Subscription revenue rose slightly to $378 million as price increases offset subscriber declines while non-political advertising was down by 3% to $312 million. Advertising is showing some sequential improvement, and Morgan Stanley ( MS ) has forecast a 10% increase in 2024 ad spending, which should help flip this metric positively.

Given lower political advertising, which flows largely to the bottom line, quarterly free cash flow was $60 million with EBITDA down by 38% to $166 million. Based on guidance, Q4 revenue is expected to fall mid-to-high teens as political revenue is down substantially as we will be comparing vs the midterm elections last year. Still, excluding its termination fee, TEGNA should earn about $1.90 this year, aided by the fact its share count is down by 10.5% to 201 million. That gives shares less than a 9x multiple, and TEGNA is also highly cash generative with $370 million of free cash flow so far this year, or $320 million excluding working capital.

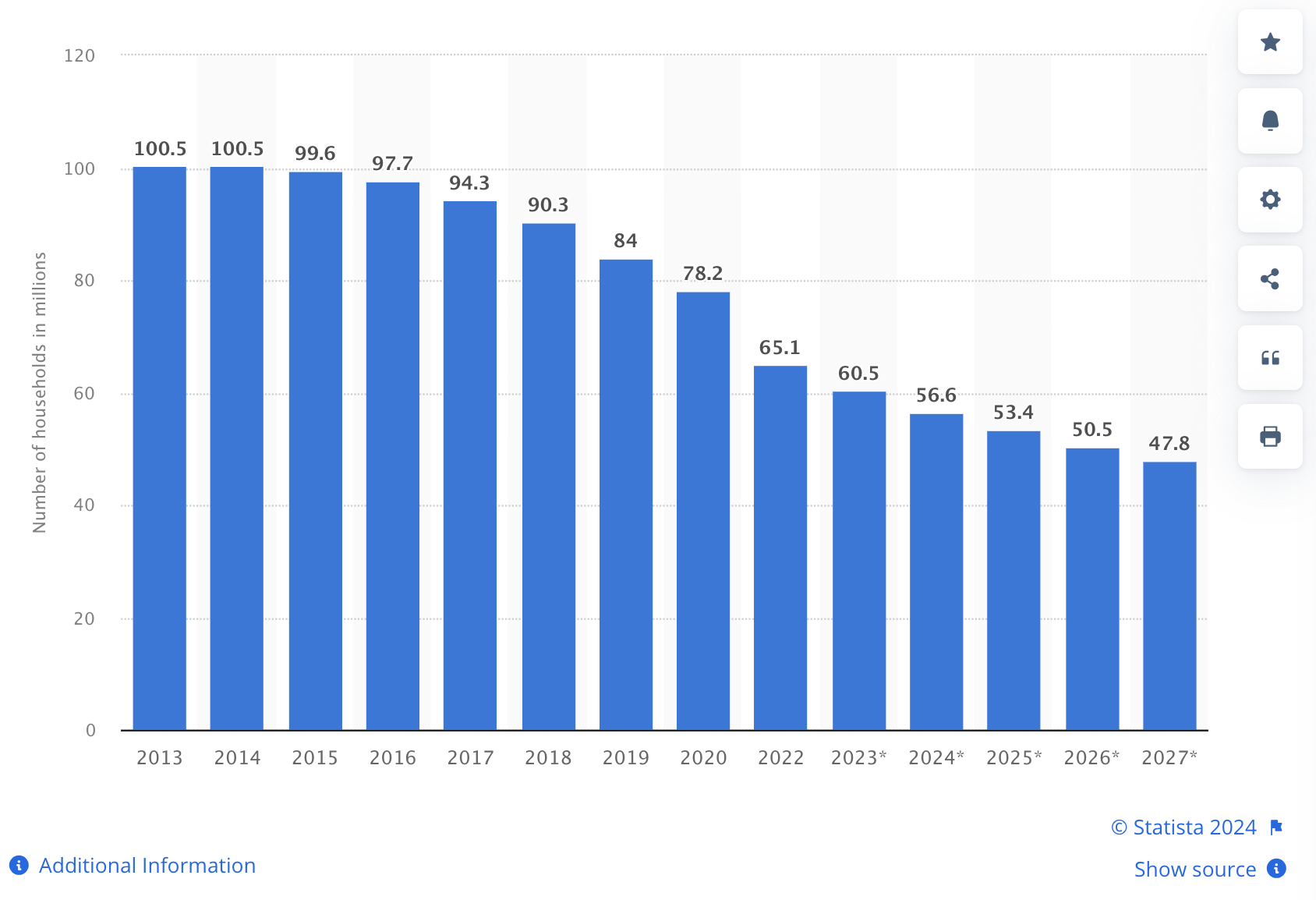

A reason TEGNA trades at such a low multiple is that fewer and fewer Americans watch television. The number of pay TV households has steadily fallen with a significant drop after COVID. Those losses are expected to continue, based on forecasts. Increasingly, sports are one of the lone things keeping consumers watching linear television. Of the top 100 primetime TV broadcasts in 2023, 56 were sports with 45 being NFL games. The first scripted program came in at 43 rd place (Fire Country on CBS, which aired after the AFC championship game, the year’s second-highest broadcast). Increasingly, scripted content is a streaming-first media form.

{kind=link}

Now, broadcast television has held in better than cable. It still reaches 76% of households vs 54% for cable. Like sports, news is still largely consumed in real-time. Moreover, it is harder to see the streamers, like Netflix ( NFLX ) make a play into local news as you would need different offerings in each local market. TEGNA undoubtedly faces subscriber headwinds, but its base should prove stickier than a scripted cable channel, which can more readily be replaced by over-the-top offerings. Even with lower subscribers, subscription revenue is at an all-time high. And with valuation where it is, markets are pricing in a long-term decline for the business.

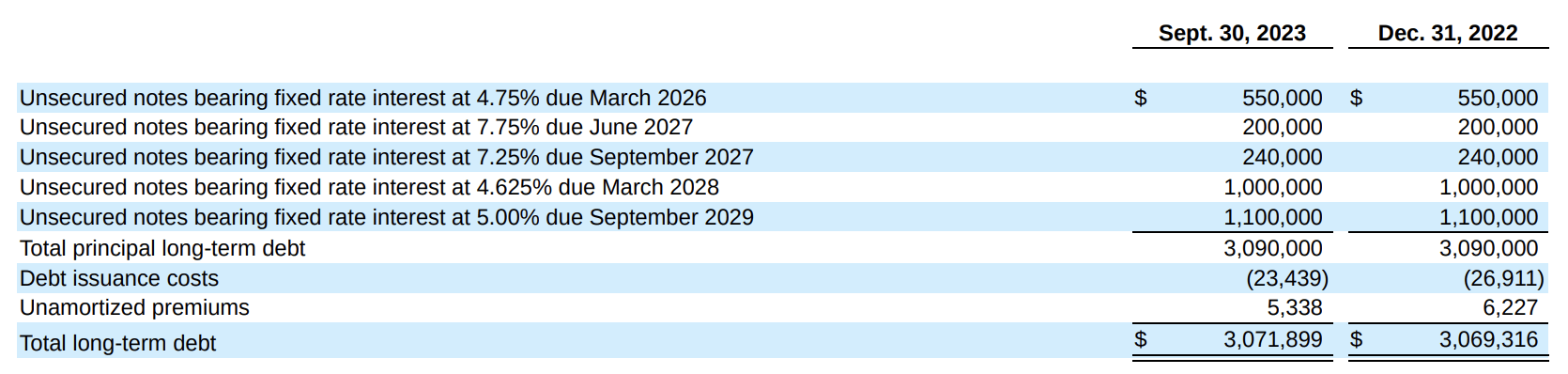

In the meantime, TGNA is buying back shares at depressed levels. On top of its $436 million in repurchases announced earlier this after, after Q3 results, it launched a $325 million accelerated share repurchase. By March 2024, it will have repurchased $800 million of stock. TEGNA can fund this repurchase out of its $553 million of cash on hand, which is why its $3.1 billion of debt will stay flat in 2023, leaving leverage a bit below 3x.

Importantly, TEGNA has no maturities until 2026, meaning it will not need to roll over debt at higher rates. As such, I expect it to continue to devote free cash flow to dividends, or possibly M&A if it can add stations at discounted levels.

{kind=link}

As investors move beyond its disappointing 2023, I expect there to be increased optimism when a closer look is given to likely 2024 results because of the Presidential election. In 2020 , political spending was a $446 million tailwind. The 2022 midterms drove $341 million, up nearly 50% from the prior midterm’s $234 million. In 2024, I would expect at least a $500 million tailwind, given the growth of political spending. Moreover, its networks are positioned quite well for the 2024 landscape. There are critical Senate races in Texas, Florida, Arizona, Ohio, Michigan, and Pennsylvania as well as a competitive gubernatorial election in North Carolina. While it is not a swing state, its jungle-primary system is likely to mean substantial political spending in California’s open Senate race. Georgia, Arizona, Michigan, and Pennsylvania will also likely be the focal point of Presidential spending in 2024. These states that are the focal point of the 2024 elections are the backbone of TEGNA’s affiliate ownership, meaning it should see significant demand for airtime by campaigns and affiliated groups,

Even assuming some decline in its legacy business from higher programming costs, TEGNA should do over $700 million in free cash flow in 2024 thanks to this political advertising tailwind. Including its already announced $325 million program, TEGNA can conservatively buy back over $700 million of stock by the end of next year without borrowing. That will reduce its share count by over 20%. That is on top of its 3% dividend payment.

Because TEGNA’s cash flow moves so much with the political calendar, we can average how it does over a 4-year cycle. In the 2 off years, TEGNA has $350 million of free cash flow, in a midterm $500 million, and in a Presidential year, $700 million, for an average of $475 million. With the share count likely to be below 165 million by the end of 2024, at 10x free cash flow, TEGNA would be worth over $28. A 12% free cash flow yield (to generate a 10% return, assuming a 2% annual decline rate) yields a fair value of $24. That $24 is the same price TEGNA was going to sell itself for, though its share count is likely to end 2024 25% lower due to its buybacks.

With TEGNA buying back so much stock, its depressed share price can actually help to enhance longer-term returns as more of the share count is retired. Coming into an election year when cash flow is particularly high, this is an opportune time for dramatic share count reduction. Thus far, TEGNA has weathered the loss of subscribers well, and so I view a 2% annualized decline as conservative, particularly given the growth in political spending over time and the potential for broadcast affiliates to pair with streamers, like YouTube TV, in a streaming-first bundle. Still, given the pessimism around the sector, a discounted valuation is likely. Nonetheless, I arrive at a $24 fair value, or 50% upside from here. I would be a buyer, and as we see political spending begin to boost results and share buybacks reduce the float, I expect the stock to re-rate higher over 2024.

For further details see:

TEGNA: Large Buyback Should Begin To Lift Shares In 2024