TLTZF - Tele2: If You Want A Nice Steady ~8% Yield This Is The Company

2023-10-16 04:27:48 ET

Summary

- I have been investing in a diverse range of investment potentials, including low-yield companies with high potential and debt instruments.

- I am happy with the investments but missed the opportunity to trim their position in Tele2 during overvaluation.

- Tele2 offers plenty of upside potential and a high yield, making it a good investment option.

Dear readers/followers,

We've been looking at a variety of different investment potentials over the past few months as things have been going down. I have been investing in companies with low yields, and massive upsides. I've been investing in high yield with flat EPS forecasts, and I've been investing in debt instruments, prefs and bonds, and the like. In short, it's been a veritable smorgasbord of attractive potential investments, and looking back on my mix, I'm very happy about what I've been buying.

I haven't been overexposed to any one investment here - and I'm still unusually cash-heavy with over 13% cash at the current time and as I am writing this article - but I still buy on almost a weekly basis.

One of the investments that I'm so-so happy with is Tele2 ( OTCPK:TLTZF ). The reason that I am so-so-happy is that I "missed out" on actually trimming/rotating my position during overvaluation back in 2022. I completely overestimated where the company was going, though part of the reason was also that I really didn't have anywhere to go with the massive amounts of capital that I had invested here.

So, the company has fallen back closer to the levels of my cost basis, which means that I'm generally happy because I can buy more, but also a bit annoyed because I "missed out". No excuses from me in these cases - because I do actively manage my investments. My last article was back in February. You can find it here.

The reason for this update is a material drop in the company's valuation - meaning more than 10%, despite the market being up. However, while the macro may be different, the company's fundamentals and long-term income potential have not worsened but improved. This warrants an update from me here.

So, let's see why you should "BUY" tele2 here.

Tele2 - Plenty of upside, and a juicy yield to boot.

So, Tele2 at around 125-130 SEK isn't a buyable stock. That's something I can be fairly clear about. I can also be fairly clear about my stance that in order to invest in a stock I want at least a 7-9% almost guaranteed longer-term sort of yield or RoR.

Why?

Because 7-8% is where we can get certain investment-grade bonds at this time, which is a completely different risk profile. Ideally, and this is perhaps even more accurate, I would want 15%+ per year from a stock at a very high likelihood in order to invest here. If it doesn't give me that, then there are better opportunities out there.

I have for some time been so-so positive on Tele2. As with most telcos, the investment thesis for this one hinges on a very high attractive dividend supplemented by single-digit EPS growth and an incumbent position in an attractive market.

Tele2 gives us all of this. The company is an investment-graded BBB Telco that has been trading rather unimpressively for over 20 years. By that, I mean that you have gotten that 7-8% long-term annualized RoR in a combination of dividends and capital appreciation, but you haven't gotten more than that.

That's something to know. In order to really get those high returns, you need to know when to buy and when to sell. Because this is not a buy-and-hold business, not forever at least (then again, few are).

After the coupling with Swedish Com Hem, the company has become a digital communication and infrastructure powerhouse. It represents my own broadband account and internet connectivity.

Tele2, as of the last quarter, continues its topline growth momentum, with solid 1H23 cash generation, and the company has been very clear about its attractive shareholder remuneration, and that these trends support exactly that. The company's rollout of 5G isn't as fast as Orange ( ORAN ), but then again, very few companies are.

The company has, as of the latest quarter, updated its 2023E guidance and its mid-term forward ambitions.

{kind=link}

Tele2 IR (Tele2 IR)

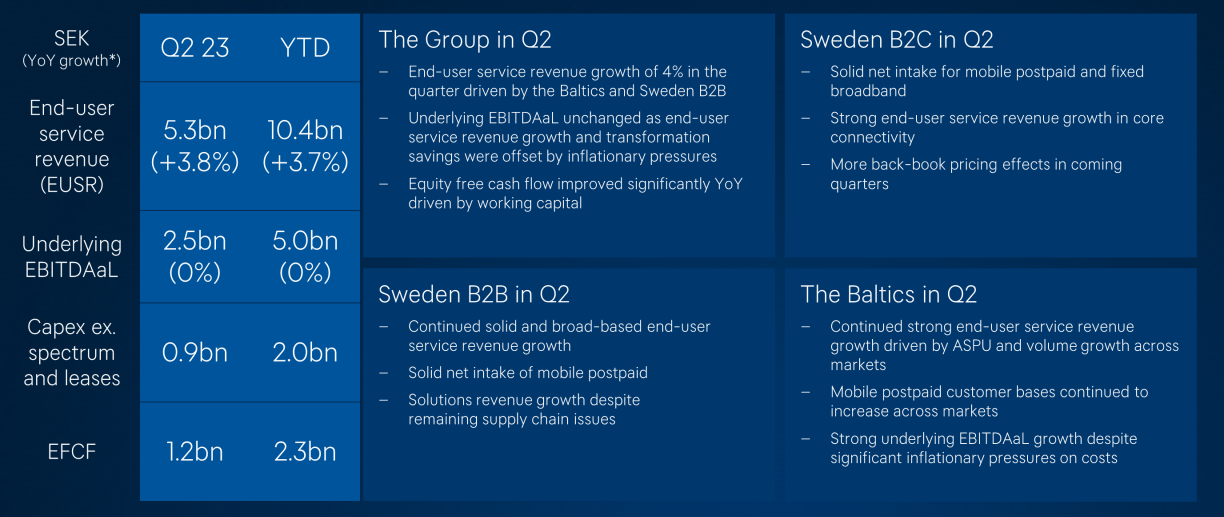

Tele2 remains a play on Sweden and the Baltics - and you can see that as a whole, the company is growing more than your average Telco. This is based on attractive postpaid and broadband trends, and thanks to the addition of Com Hem, also based on digital TV Cable/Fiber trends. All of these growth trends are either flat or up, and not a single segment in the core Swedish consumer segment is declining. We're seeing a strong mobile postpaid intake of 25,000 with good switching to attractive family plans and propositions.

The B2B sector, meanwhile, is also reporting attractive overall trends. The company's topline growth is sustained here with a Mobile ASPU YoY growth of 1% in 2Q23, and almost 5.5% in end-user service revenue for the business segment - 11,000+ new RGUs, in the segment.

And all of this was despite ongoing supply chain issues.

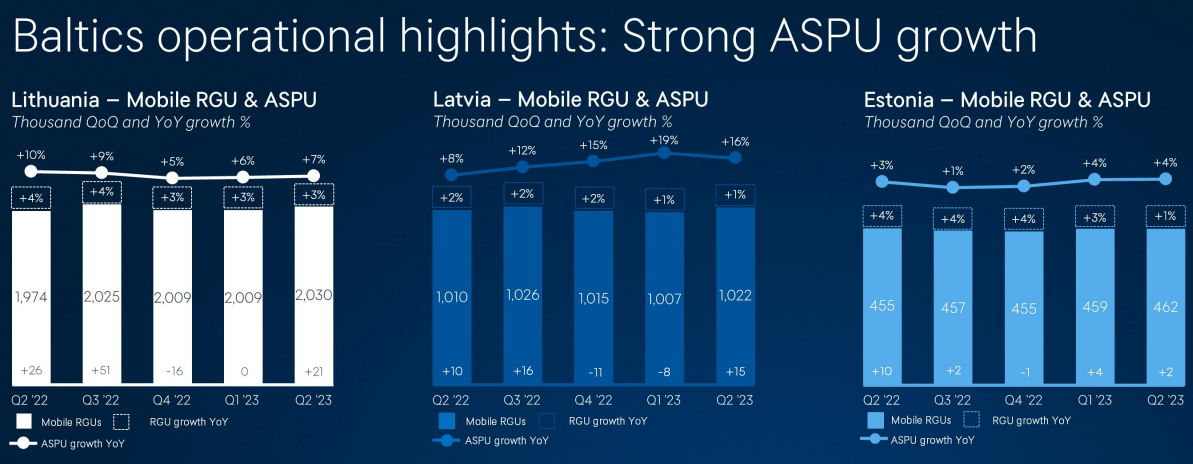

The Baltics continue to be attractive growth vectors, with Latvia currently at the peak with 16% YoY ASPU growth.

{kind=link}

Tele2 IR (Tele2 IR)

Even the underlying bottom-line financials in the Baltics are very attractive, with a 40%+ EBITDA margin, which you typically only find in home markets. This is up from 35% as late as 2022A for the 2Q. The company also maintains 70%+ cash conversion ratios here. So the company's growth vectors are working extremely well here.

This is part of the reason why I believe Tele2 to actually be somewhat mispriced here, and why it could represent a very core sort of growth potential.

Leverage continues to be at a very attractive level, around 2.6x to underlying EBITDA, slightly up due to the dividend, but still at the lower comfortable range of 2.5-3x target.

As a reminder, this company pays dividends two times per year, so it's not a single dividend payor, as some European companies are. Like many businesses, Tele2 is in the midst of a transformation program for its business, expecting 1B SEK worth of savings for the full program at an annualized run rate, with nearly a quarter billion realized for 2Q23.

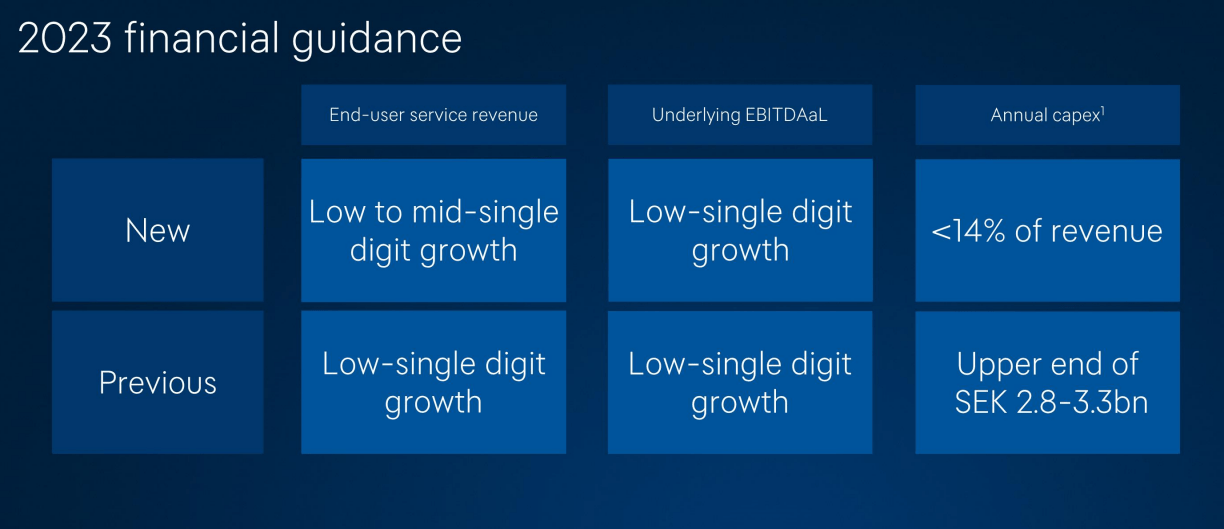

The guidance for the company is currently as follows.

{kind=link}

Tele2 IR (Tele2 IR)

This means that the dividend levels are likely to be maintained here, and we can expect a continued, 8% dividend yield at this particular valuation and price point. The company's long-term plans concern mostly CapEx as a difference to how things are today. Currently, 14% or slightly below is going to CapEx. Long-term has a target of 10-14%, which would obviously free up more cash for returns.

Your expectation going into this investment should be slight increases in the dividend from the 6.75 level (ordinary) we saw during 2022A. Tele2 has, over the past 10 years, often been able to offer extraordinary and high dividends. Some years this was close to 10 SEK per share. This has been part of muddling valuations and company earnings somewhat. Going forward, with everything concerning Com Hem and the company's growth strategy now done, I believe the company to be a more stable dividend payor, as most telcos are. For 2023E, I don't believe a more than 0.05 SEK dividend increase, which is also where the current FactSet analysts end up (Source: FactSet), or as S&P Global believes, a 0.06 increase. In any case, this is likely to only be a token increase for the year.

But the current dividend is already good enough. At 8%, you're getting a Swedish telco incumbent at a very attractive price, with a valuation-related upside.

What sort of upside?

Tele2 - The valuation implies an upside of at least 15% here.

My last article on Tele2 was in February. Since then, the company has dropped. I could see 10-15% annualized RoR as likely back then, and I can see the same thing now. The company does still, in fact, fulfill every investment criterion I hold, and the only literal reason that I am not buying more is that I am already fully invested at this particular time.

Tele2 typically trades at a decent premium due to its company structure and assets (among other things). Over the past few years, a valuation of 24-29x P/E has been the norm for this business. The high dividends also play a role here.

I forecast it at 14-17x P/E , which at the mid-point gives us around 14% annualized RoR, and the high point implies an upside of that 15% I talked about - and this is, as I see it, conservative for this business because it tends to beat those estimates at least 40% of the time on a 1-year basis with a 10% margin of error. (Source: S&P Global).

The fact is that at 85 SEK or thereabouts, you're investing in Tele2 at vastly lower multiples and targets than we've been seeing. While some discounting is in order, because we're no longer in ZIRP when a 5% yield was "good", this discounting is too high for what the company may offer on a forward basis.

For analysts, we're looking at an average PT of 105 SEK, from a low of 83 SEK and a high of 130 SEK. That high was by the way 179 SEK less than a year ago, which shows you how much the company has already been impaired due to macro. At this valuation, 12 out of 19 analysts are at a "BUY", with the remainder at "HOLD". (Source: S&P Global)

My last PT was that the company was attractive at anything below a 105 SEK PT - and this was in February. Note that this is where the PT has actually ended up.

I specified a 120+ SEK trim level for the company in my last article, and I'm maintaining this here.

That means the following thesis is relevant going into 3Q23 for Tele2.

Thesis

- Tele2 is one of the 3 large telcos in Sweden and Scandinavia, and it's probably my second-preferred telco investment here in this geography, behind Telenor. It combines appealing mobile services with cable TV infrastructure, generating both an attractive dividend (albeit with some volatility) as well as impressive infrastructure safety.

- At anything below 105 SEK, this one becomes an appealing "BUY", and at over 120, I would say it becomes time to look at trimming positions in the company.

- Due to this, the current rating for Tele2 stock is a "BUY" with a double-digit upside, and I double down on this thesis as of October 2023.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

Currently, Tele2 fulfills every single one of my investment criteria. I rate the company as a "BUY".

For further details see:

Tele2: If You Want A Nice, Steady ~8% Yield, This Is The Company