TEF - Telefonica: Don't Let An 8% Dividend Yield Fool You

2023-11-22 23:44:48 ET

Summary

- Telefonica S.A. offers an 8% forward dividend yield, but dividend growth is unlikely due to revenue challenges and high leverage.

- The company's financial performance has been declining, and its weak balance sheet limits room for investment in growth initiatives.

- My valuation analysis suggests the stock has almost no upside potential.

Investment thesis

Telefonica, S.A. ( TEF ) currently offers an attractive 8% forward dividend yield, which might be tempting for dividend investors. On the other hand, dividend growth is also important for value investors as it suggests the sustainable ability of a company to deliver solid operating leverage and ensure the safety of the dividend over the long term. My analysis suggests that it is very unlikely to expect dividend growth from TEF in the foreseeable future as the company struggles to drive revenue growth given industry-specific challenges and its highly leveraged balance sheet. Historical trends in dividend history suggest that the management is likely to prioritize balance sheet improvement over dividend growth. Moreover, my valuation analysis suggests almost no upside potential for the stock. All in all, I assign TEF a "Hold" rating.

Company information

Telefonica S.A. is a Spanish multinational telecom company that mostly operates in Europe and Latin America. The company provides a range of telecommunication services, including fixed-line and mobile telephony, broadband, and digital television.

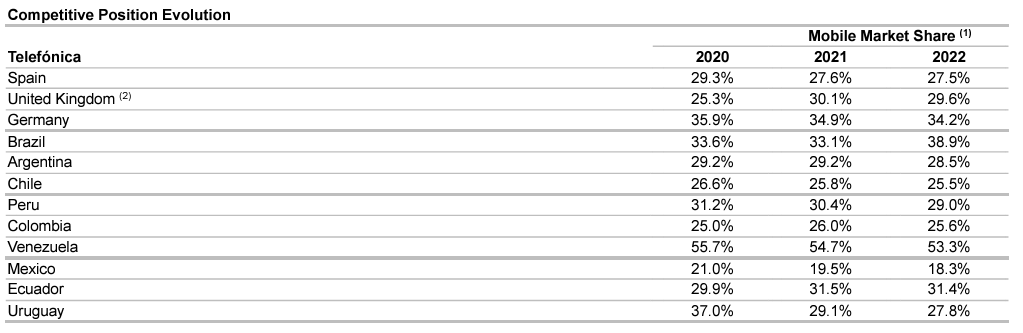

The company's fiscal year ends on December 31. According to the latest annual SEC filing , TEF has solid market shares across some of the largest European and Latin American economies.

{kind=link}

Financials

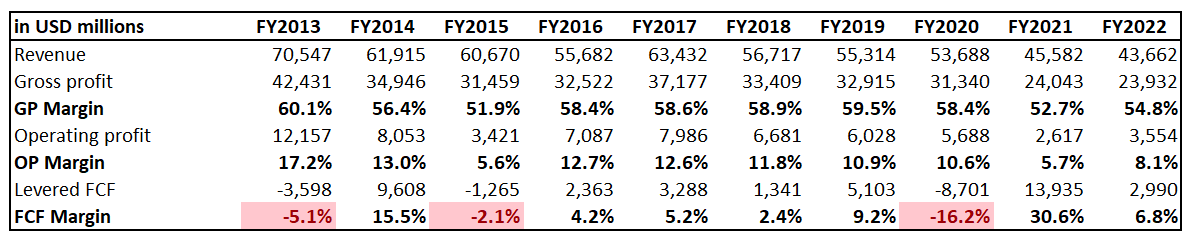

The company's financial performance over the last decade does not look optimistic. The decline in revenue occurred due to several notable divestitures over the last decade. Divesting multiple business units means the unfavorable trend of losing strength as a market player. I could have said that divestitures are good if they help the company improve operational efficiency, but secular trends in profitability metrics also do not add optimism to me.

{kind=link}

Positive outliers in free cash flow [FCF] margin, like in FY 2021, should not mislead readers as they were substantial cash inflows from business divestitures. Overall, the FCF margin was low in recent years, mostly due to substantial investments related to a 5G buildout. To invest in new technology, TEF raised substantial debt financing, and the company is currently highly leveraged. Despite most of the debt being long-term, I consider high indebtedness a substantial risk for the business as profitability metrics are shrinking and the covered ratio is just slightly above 2.

Author's calculations

The company's weak balance sheet does not give many options to invest in strategic initiatives to fuel revenue growth or sustainable profitability expansion. The current financial position, together with the secular decline in profitability metrics, also makes aggressive dividend hikes unrealistic. That said, the current forward 8% dividend yield looks like a peak for the foreseeable future.

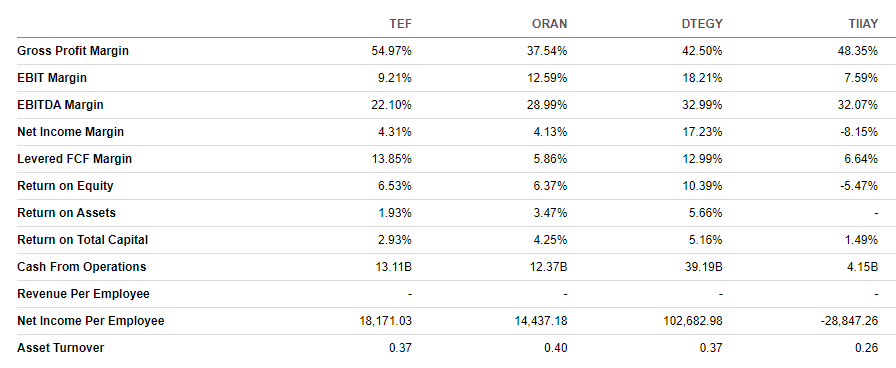

On the positive side, despite experiencing a steady decline in profitability, TEF's profitability metrics look solid compared to the ones demonstrated by its European peers. Robust profitability metrics compared to peers suggest that the management is efficient in managing costs despite revenue experiencing a decline over the long term.

{kind=link}

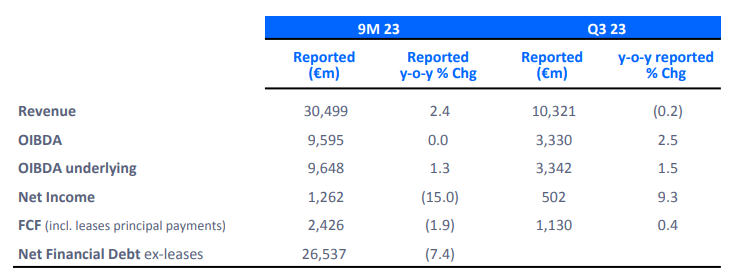

The latest quarterly earnings were released on November 8, when the company topped consensus estimates . Quarterly revenue declined by 2.1% on a YoY basis. However, despite revenue softness, TEF delivered a notable 9% growth in net income. While strong Q3 profit might be good news, I would like to highlight that the net income for the first nine months of 2023 tumbled by 15%. That said, there are still apparent challenges for the company to sustain its profitability.

{kind=link}

The good part is the FCF, which surpassed one billion euros in Q3, meaning the company has the opportunity to improve the balance sheet. On the other hand, given the massive indebtedness, it would be a long road even if TEF sustains a billion-per-quarter FCF.

It is also crucial to highlight that the management also shared its vision of financial goals for 2023-2026. The target annual dividend for the given period is 0.3 euros per share, meaning that dividend growth is unlikely to happen in the next 2-3 years. The management's projected 1% revenue CAGR, which is below inflation, for the next three years, is also solid evidence that the company has no options to drive revenue growth. The management's very conservative projections for the next three years look very honest to me as the company operates in an industry where almost 100% penetration is achieved. The business also requires substantial investments in infrastructure, which requires raising debt finance. The management's goal to improve profitability does not look impossible, but I do not expect a substantial improvement in profitability given almost no expected revenue growth and a harsh macro environment with substantial inflationary pressure across Europe and Latin America.

Valuation

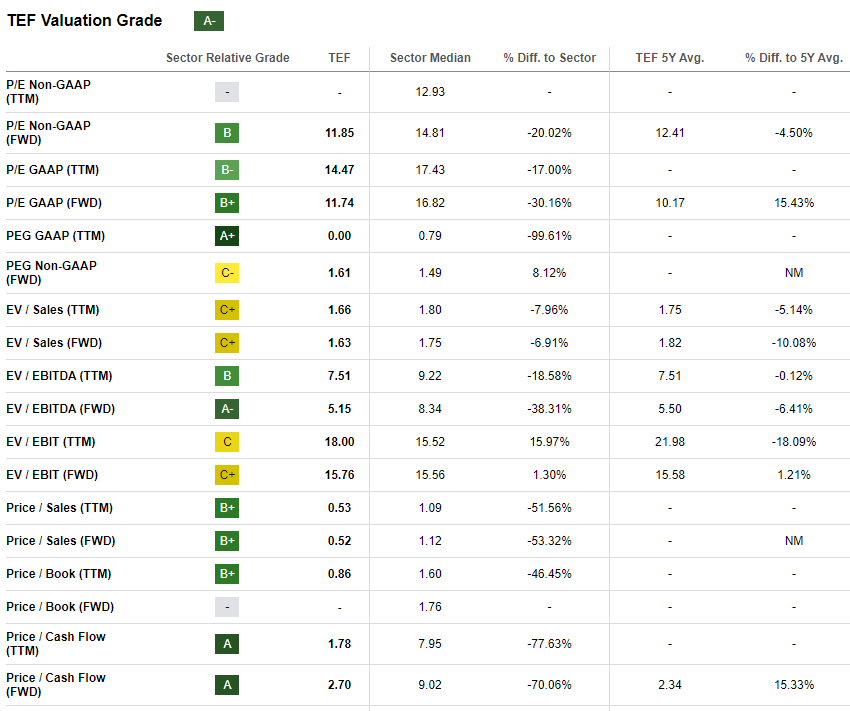

The stock rallied by 13.5% year-to-date, notably underperforming the broader U.S. market. On the other hand, the stock demonstrated stellar performance compared to the U.S. telecom giants like Verizon and AT&T, whose shares plunged this year. Seeking Alpha Quant assigns TEF a high "A-" valuation grade because the company's valuation ratios are substantially lower than the sector median. On the other hand, the current valuation multiples are very close to historical averages, which might indicate the stock is fairly valued.

{kind=link}

I want to proceed with the dividend discount model [DDM] simulation. I use an 8% WACC for discounting, as suggested by Gurufocus . Dividend consensus estimates forecast FY 2024 payout at $0.33, which I also incorporate into my DDM formula. Telefonica historically had struggles with increasing dividends , so I use a shallow 0.5% dividend CAGR.

Author's calculations

According to my DDM valuation, the stock's fair price is $4.40. This indicates a very limited upside potential even if TEF sustains its dividend yield. It is also crucial to keep in mind that the DDM ignores TEF's massive indebtedness. That said, I cannot say that the stock is attractively valued despite a solid 8% dividend yield.

Risks to my cautious thesis

Positive breaking headlines tend to be strong positive catalysts for stock prices, which might lead to sudden spikes. For example, Saudi Arabia's STC Group is one of the company's investors. Any news regarding this investor from an oil-rich country increasing its stake in TEF might become a strong catalyst for the stock price.

While I do not expect dividend growth based on the management's goals up to FY 2026, I cannot say that dividend hikes are impossible for TEF in the foreseeable future. The FCF is still strong, and there is a small possibility that a sudden dividend hike might occur. This can also be a positive catalyst for the stock price in the short term.

Bottom line

To conclude, TEF is a "Hold". Despite an attractive forward dividend yield, it is unlikely that we will see dividend hikes in the next couple of years. The valuation does not look attractive either. Industry specifics, together with the balance sheet indebtedness, make it quite unlikely that the management will prioritize dividend hikes or substantial stock buybacks.

For further details see:

Telefonica: Don't Let An 8% Dividend Yield Fool You