TELDY - Telefonica Vs. Telefonica Deutschland: German Subsidiary More Appealing Than Spanish Parent

Summary

- Telefonica Deutschland is less well known than its parent Telefonica SA and consequently also less well covered.

- Both companies have the same high 6.25% dividend yield but also have a history of dividend cuts.

- At first glance, Spanish Telefonica looks preferable, but German Telefonica Deutschland is more suitable for dividend investors.

- More important, Telefonica revenue has been on a decline, whereas Telefonica Deutschland has grown it over the last years.

- Not only does the dividend seem more safe, but the distributions of Telefonica Deutschland also are not subject to a dividend withholding tax.

Telefonica Deutschland (TELDF) (TELDY) is less well known than its parent Telefonica S.A. ( TEF ) but does have some merits compared to its Spanish parent. Currently both companies deliver a decent dividend yield, but the Spanish parent has been losing momentum whereas the German subsidiary is growing both revenue and operating income. This article details the merits of an investment in Telefonica Deutschland compared to Telefonica.

Telefonica S.A.

Telefonica S.A. is a Spanish multinational telecommunications company. The operations are focused on Latin America and Europe, with the latter continent being the main contributor to turnover. This is not surprising given the company started in Spain nearly a century ago.

Nevertheless the focus of the company is equally distributed between both continents as the Spanish and German segments are only slightly larger than the Brazil and Hispam segments. But more important, revenue margins are superior in Brazil which explains why the company spends most of its Capex in this country.

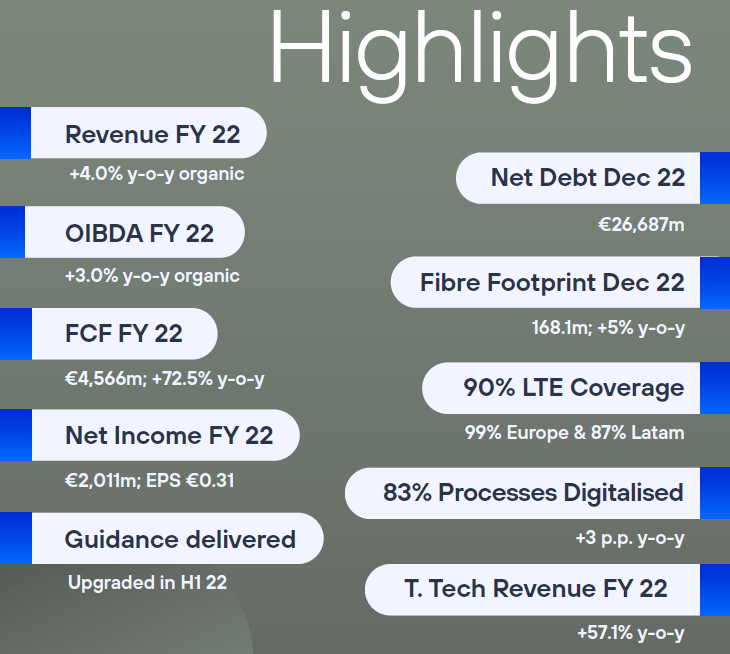

The results presented for FY2022 looked quite reasonable, see figure 1. Revenue was up, and the same holds for operational income before depreciation and taxes (OIBDA) and free cashflow.

Figure 1 - Telefonica FY22 results (telefonica.com)

{kind=link}

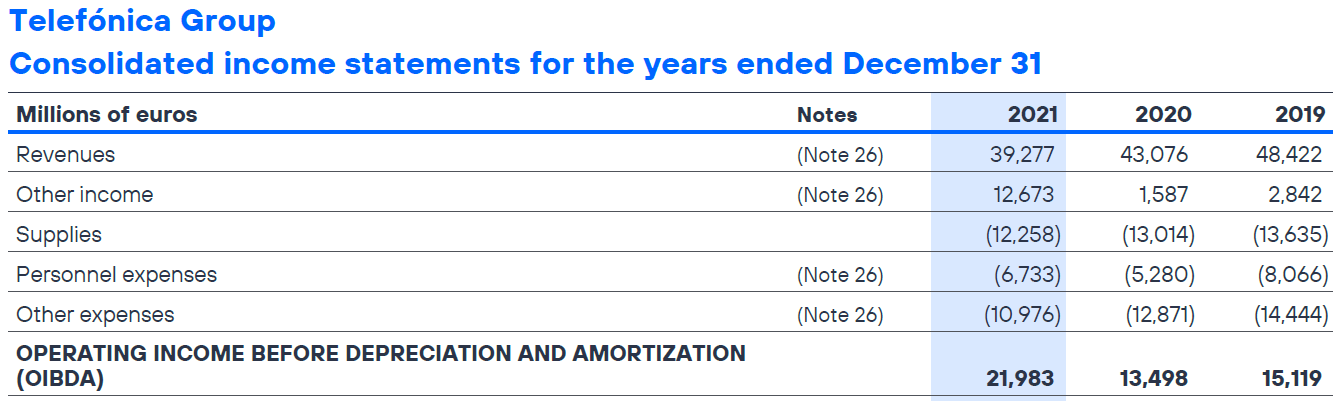

Delving somewhat further into the numbers, revenues and operating income for the group have been fluctuating however, see figure 2. Clearly revenue has been declining substantially prior to 2022 and the operating income has shown a similar decline.

One could argue this was not the case in 2021, but delving further into the annual report of said year, it appears €11Bn of the 'Other income' was obtained from selling parts of the business. Correcting for this number the operating income has actually been declining, just like revenue.

On the upside, the decline of both revenue and OIBDA was halted in 2022. Yet, in spite of the high (trailing) dividend yield, one can understand why Seeking Alpha's quant system assigns the lowest score for dividend safety and actually warns of a potential dividend cut.

Figure 2 - Excerpt of consolidated statement of income Telefonica AR 2021 (telefonica.com)

{kind=link}

In addition to the listing of Telefonica S.A., the segments with the second and third largest revenues, Telefonica Deutschland and Telefonica Brasil ( VIV ), have their own listings in their respective countries. Both of these entities distribute dividends of which only Telefonica Deutschland is able to come close to the yield of the parent company.

Telefonica Deutschland

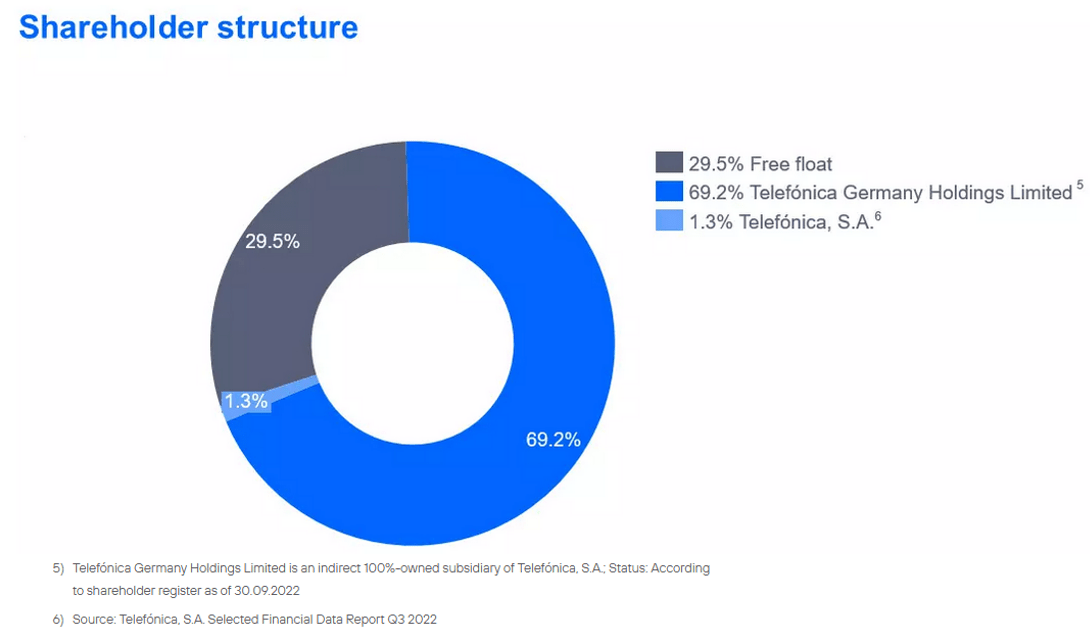

Telefonica Deutschland is less well known than its parent Telefonica SA, and consequently also less well covered. This creates an opportunity as it is a sizeable company that manages the business well and focuses on shareholder returns. Although TELDF is a separate entity, Telefonica SA has a sizeable stake in the company, see figure 3.

Figure 3 - Shareholder structure Telefonica Deutschland (telefonica.de)

{kind=link}

As the name indicates, Telefonica Deutschland focuses exclusively in Germany. The company operates in the largest economy of Europe, which is home to a population of nearly 84 million persons compared to 43 million inhabitants of Spain.

This number of inhabitants combined with a strong economy mean there are other competitors on the German market of which Deutsche Telekom ( DTEGY ) and Vodafone ( VOD ) are the main players. Deutsche Telekom obviously is well-known due to its presence in the US market through T-Mobile US (TMUS).

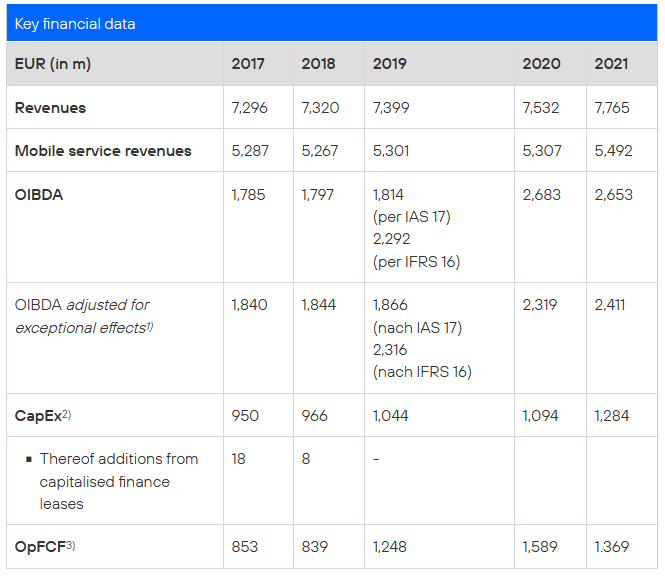

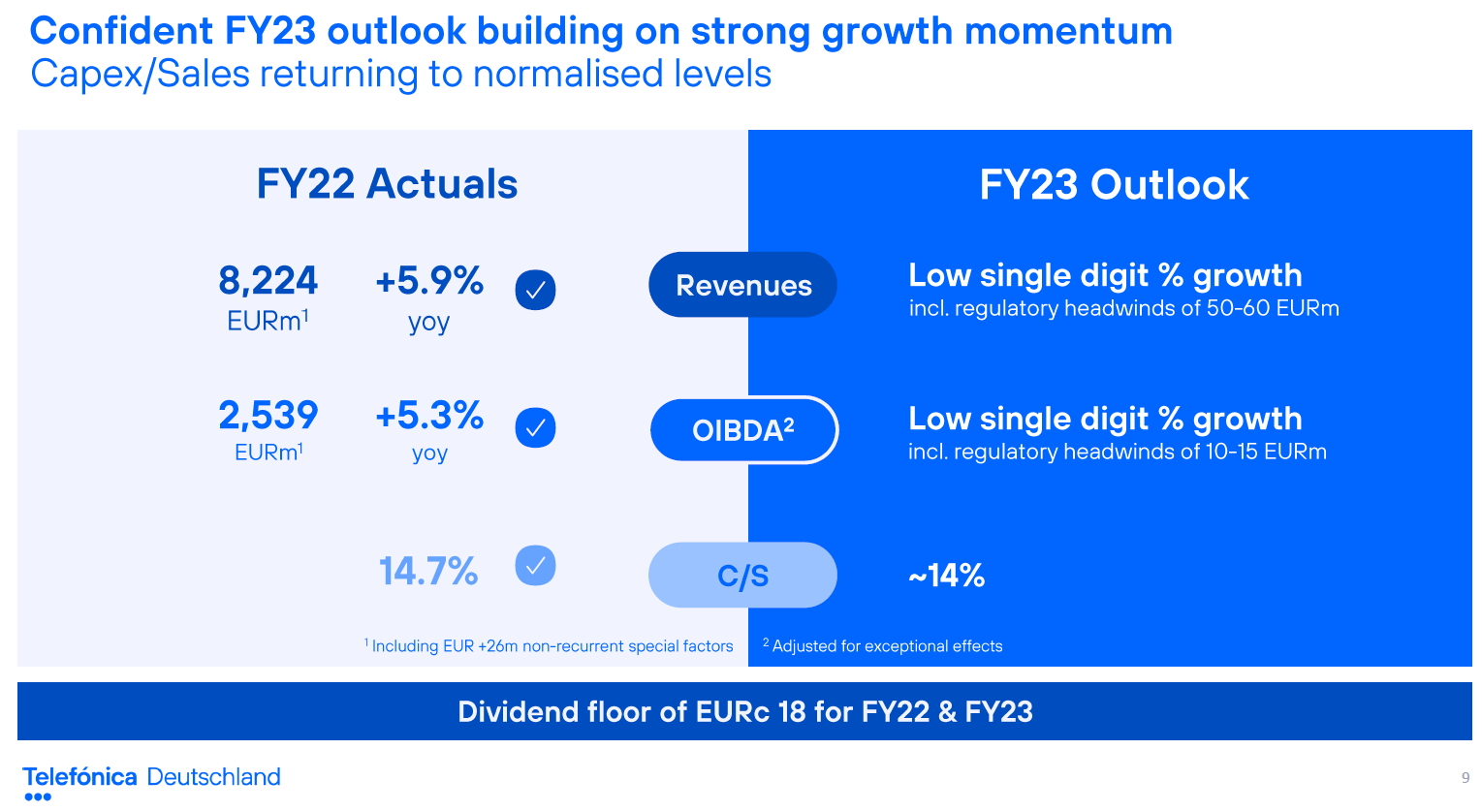

An overview of the key financial metrics is given in figure 4. The numbers show the company has been growing revenues and income steadily, without sacrificing investments given the continued increase in CapEx.

Figure 4 - Telefonica Deutschland key financial data (telefonica.de)

{kind=link}

At the 4Q22 presentation , the company showed revenues grew further and actually surpassed the €8Bn mark for the first time. The OIBDA however declined slightly as can be seen in figure 5.

Figure 5 - Telefonica Deutschland FY22 results (telefonica.de)

{kind=link}

Stock price comparison

Firstly, the share price development since 2015 is shown in figure 6. This year has been chosen as a start date as it was the first full year after Telefonica Deutschland finalized the acquisition of E-Plus to become more competitive against rivals Deutsche Telekom and Vodafone.

Figure 6 - Normalized stock price development since 2015 (seekingalpha.com, finance.yahoo.com; chart by author)

{kind=link}

Clearly, an investment in either company destroyed more wealth than it created. Whereas Telefonica stock is currently worth 65% of the value relative to 2015, a 35% decline, the stock of Telefonica Deutschland actually declined by nearly 70%. Both stocks have clearly shown a downtrend, which came to an end in 2020. Since then, both stocks performed relatively steady and have been moving sideways.

The superior performance of Spanish Telefonica could be attributed to the cancellation of shares in 2021 and 2022, but the magnitude has been small and does not explain the differences in stock price. Moreover, Telefonica has occasionally opted for a scrip dividend which increases the amount of shares outstanding. In that sense the cancellation of shares must be seen as a remedial action to mitigate the dilution.

Even given the paltry performance of both stocks, the dividend yield is quite alluring at present. Therefore one can understand why investors may be willing to make an investment in either of the Telefonica stocks. But which to choose?

Dividend comparison

Going by the stock price development of the last years, it would be understandable if an investor steers clear of Telefonica Deutschland. After all, an investment in TELDF would have created a loss twice that of the same investment in TEF.

Being a DGI however, and acknowledging the stock price appeared to have found a lower bound, my attention goes out to the potential of the dividend of both companies.

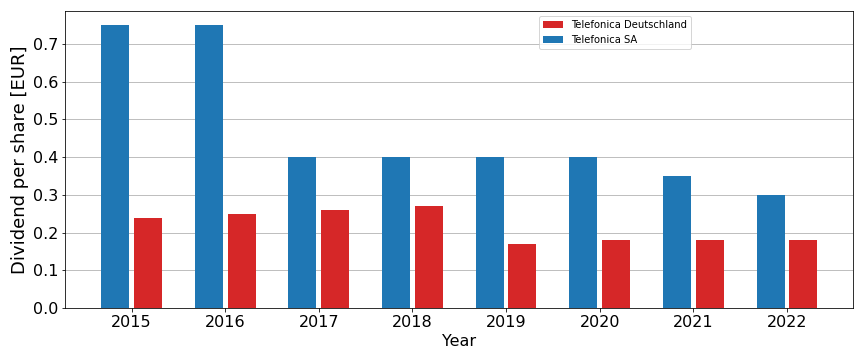

In spite of Telefonica looking better at first glance, the development of dividends per share, as shown in figure 7, tells a different story. The dividend paid by Telefonica has been cut substantially in 2017 and lately it has been cut two years in a row. On top of this, the company alternates between paying dividend in cash or stock. Now, a stock dividend can be a good option, but not if the stock trends downwards as shown in figure 6.

Figure 7 - Dividend per share (ARs from telefonica.com and telefonica.de; chart by author)

{kind=link}

The dividend paid by the T. Deutschland is not free of cuts either, but the trend displayed in figure 7 is different. Although it falls outside the timespan of the chart in figure 7, to be complete it must be mentioned the dividend per share was cut following the E-Plus acquisition in 2014. After that the dividend was increased only to be cut again in 2019.

The 2014 cut was done to fund an acquisition and the 2019 one to fund a growth strategy. In between the cuts Telefonica Deutschland made an effort to increase the dividends and always paid in cash. This gives a slightly more positive signal than only lowering the payout and opting for stock dividends.

More important however, the presented data on revenue development (figures 2 and 4), shows the biggest distinction. Telefonica Deutschland has reduced dividend payouts to fund growth and achieved an 11% increase in revenue between 2019 and 2022. This stands in stark contrast to the 15% decline in revenue Telefonica achieved over the same period.

In spite of the essentially down trending dividend for both companies, Telefonica Deutschland appears to have better cards to maintain the dividend and potentially grow it.

Taxation

This section covers taxation which may vary from person to person as it depends on many factors. However, for the comparison in this article the withholding tax of the respective countries where the companies are based is used.

Possibly the biggest differences between both companies concerns the withholding tax. Generally speaking the withholding tax for companies domiciled in Spain, such as Telefonica, amounts to 19%. Holders of the ADR are advised to account for this tax rate as the website of Citi gives no additional information on the actual tax withheld at the source.

Investors disliking the Spanish withholding tax will definitely be repelled by the German withholding tax of 26%. However, before discarding an investment in Telefonica Deutschland, one should be aware the dividend is actually exempt from a withholding tax, to wit :

The dividend for FY21 was paid in full from the tax contribution account within the meaning of section 27 of the German Corporation Tax Act (KStG) (contributions not made to the nominal capital). The payment is made without deduction of capital gains tax and solidarity surcharge. In the case of domestic shareholders, the dividend is generally not subject to taxation. The dividend is not subject to any tax refund or tax credit. Out of today's perspective, the dividend payment (subject to change) will continue to be made from the tax contribution account in the coming years.

Although the dividend is not subject to a withholding tax, this will not be the case indefinitely. Yet, as it currently stands the company distributes €0.18 in dividend per share translating into a 6.25% after-tax yield. Telefonica's €0.30 dividend generates the same after-tax yield at the time of writing. All in all, the superior yield of Telefonica vanishes if the withholding tax is accounted for.

Conclusion

Without a doubt both Telefonica and Telefonica Deutschland have shown appalling stock price development over the last years. Spanish Telefonica comes out as a clear winner when the stock price development is assessed, but a 35% loss will hardly feel as winning for many investors.

When it comes to Telefonica, the Spanish holding is better known, but the German subsidiary shows more appealing prospect in terms of growth. Both companies have a history of dividend cuts, but Telefonica Deutschland has grown the dividend in between and distributes a cash dividend, whereas its parent opts to differentiate between cash and scrip dividends.

Remarkably the dividend is currently the same, but only when the after-tax amount is considered. Nevertheless taxes affect net income and as such should be accounted for. Therefore, investors looking to build a stake in Telefonica are advised to consider the possibility to invest in the German subsidiary rather than the Spanish parent.

For further details see:

Telefonica Vs. Telefonica Deutschland: German Subsidiary More Appealing Than Spanish Parent