TELNF - Telenor: Compelling Norwegian Telco Yielding 8%+ Going Into 2023

Summary

- Telenor remains one of the largest telco positions in my entire portfolio. The company very recently reported 4Q22 and delivered its outlook and dividends.

- The yield is now confirmed at 8.1%+, and this is well-covered. The company's non-native operations are also moving forward, and things are looking better.

- If I wasn't already at maximum exposure, I would "BUY" more. Telenor is a "BUY", and here is why.

Dear readers/followers,

I've followed Telenor (TELNF) ( TELNY ) for a couple of years at this point, and have written a number of articles detailing my bullish stance for what I view as being one of Scandinavia's better telcos. Now, granted, the company is currently on a downward trajectory. However, I view this as unjustified, and I'm prepared to show you exactly why that is.

Telenor is now, after 4Q22, yielding over 8% covered - it did very well during the last year, hence the outperformance during the day of reporting, and while some risks remain, I do believe that the valuation here is compelling.

Here is why.

The bullish case for Telenor very much remains

Telenor has underperformed - no doubt about that. The reason for this underperformance is some of the uncertainty in Asia, as well as the growth potential - or lack of it - in its legacy markets. Like most developed western markets, the Scandinavian market where Telenor operates is essentially an oligopoly, managed by 3-4 incumbent massive Telco businesses that operate the absolute majority of the available infrastructure.

While they can occasionally poach customers from one another - I've switched back and forth a few times, finding actual growth here in legacy is tricky - especially once you look at inflation numbers and the telco challenges to actually boost prices. In nominal terms, I paid more for my cell phone and internet in 1998 than I do today - though it's obviously structured very differently.

Still, some investors take what I am saying here and equate this to Telenor not being able to be profitable or grow.

That is wrong.

As the company proved in the latest quarter of 4Q22, and as they have been proving, they're perfectly capable of growing revenues even in home markets. In the last quarter, Telenor pushed revenue growth in legacy Nordic regions by 5%. They also recorded record results, coming in at a net income of 45B NOK in 2022.

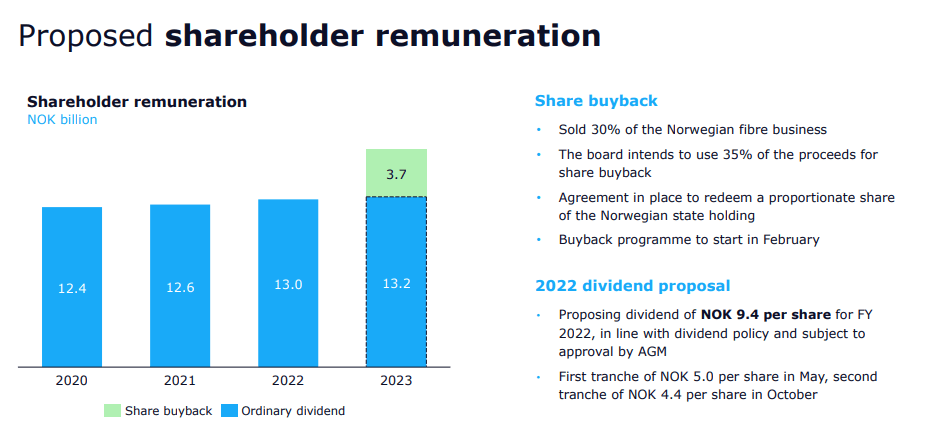

This has also led to a record dividend of 9.4 NOK/share, split into two payments, which turns this company's yield to the coveted 8%+. And that yield, dear readers, is very much safe.

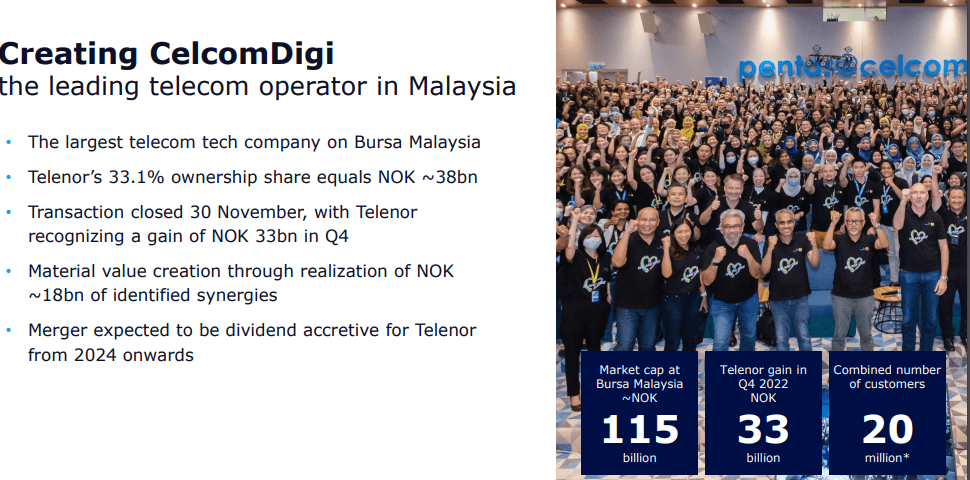

Now, the company also delivered some impressive emerging market growth, when they closed the merger and created CelcomDigi.

{kind=link}

As you can see, this will deliver accretive growth not only in earnings but in dividends for fiscal 2024, which means we'll see impacts in 2 years or so. Because of how Telenor operates, I'll likely still hold onto my 5%+ position in the company in terms of my portfolio.

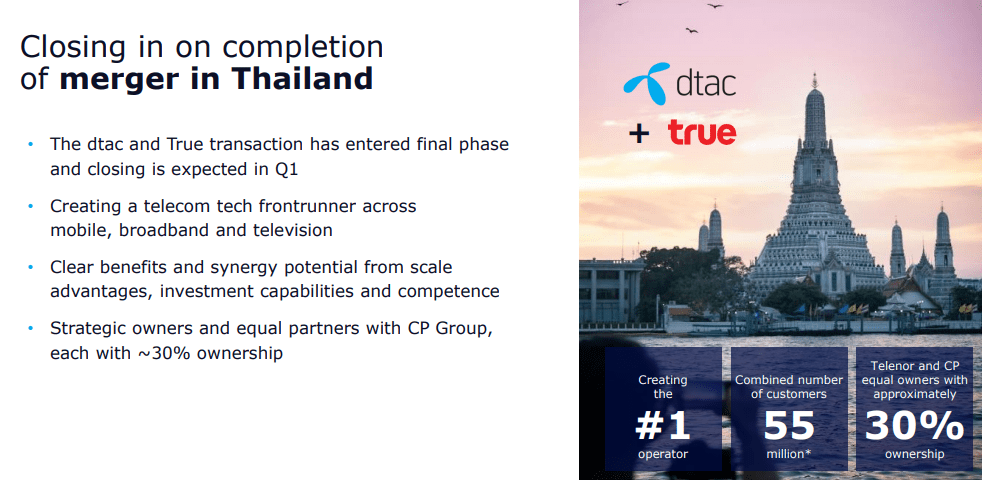

What's more, the company isn't just pushing for success in Malaysia, but in Thailand as well.

{kind=link}

Where Telia (TLSNF) not only failed with its emerging market pushes but actually suffered because of them, Telenor after a long time seems to have found working recipes not only for one but two major geographies that will deliver value to shareholders within the next few years and decades to come, as I see it. It will also more than ten-fold the company's customer base in markets where growth isn't just "easy" to come by, it's likely to continue for some time.

In legacy, things are calmer but no less exciting. The company sold 30% of its Norwegian fibre business to a combination of KKR and the Oslo Pension insurance fund at an EV of 36BNOK, which contains around 560,000 homes, and total proceeds of almost 11BNOK. The company retains financial and operational control , but this transaction will allow for further value creation with continued investments. It's a transaction in the legacy that I like quite a bit.

Numbers for the quarter, and the year are not only good - they're actually amazing - take a look at overall Nordic growth.

{kind=link}

The company also was able to showcase EBITDA growth in its Norwegian segment, as well as a 1% organic EBITDA growth for the full year of 2022. This is, given the cost increases, energy costs, and inflation, quite amazing. The one thing I don't exactly like about Telenor is that in terms of Capex/Sales %, the company is lagging behind some of its southern European countries, including Orange (ORAN) and Deutsche Telekom (DTEGY). However, the company makes up for this with somewhat more stable legacy operations, which to me makes it fine.

The share price instability is something I didn't expect to the degree that we've been seeing, but the fact that the company climbed double digits on reporting day showcases how much negativity was baked into that valuation estimate.

This, by the way, is not saying that the company did not see an OpEx increase - but it was lower than the 6-7% I modeled for, at 5% ex-energy and lower energy costs than expected.

Most importantly, organic free cash flow remained at surprisingly stable numbers. On a group level, it's at 0.1% positive, with the most major negative impacts from Norway due to costs, and Bangladesh was up nearly 2%. Not one of the company's operating geographies is showcasing significant instability or volatility to a degree that would worry me.

The company also continues to operate at very low leverage ratios - less than 2.3x net debt/EBITDA.

Oh - the dividend is one part of returning cash - but Telenor is also using this low valuation to buy back shares, almost 10B NOK worth.

{kind=link}

The short of it is this. I foresee it being a very profitable few years, being a Telenor shareholder. Part of my position was bought at above 135 NOK, but part was bought at below 95 NOK. I'm still down, but I expect the investment to become profitable, even without dividends (with dividends, I'm firmly in the black) by year-end this year or next at the latest.

At that point, it will be too late to invest in Telenor at an 8%+ yield, and a potential double-digit RoR.

The company has also given us a 2023E outlook. For the time being, Telenor expects CapEx to stay at that 17% level, but it should go down by billions in 2025E at the latest. Organic EBITDA growth is expected to be a low-single-digit (mid at post), with ongoing single-digit organic revenue growth.

All are within my target and estimate range, which means my valuation case for Telenor is as follows.

Telenor's Continued Undervaluation

The fact is, since my last article, found here , Telenor has firmly outperformed the market, more than five-folding the results we've seen. However, I've been positive on Telenor for so long, that this sort of outperformance at this point really doesn't lend me credit here - at least not yet.

Seeking Alpha Telenor article (Seeking Alpha)

As I've said though, I actually expect this to continue not just for now, but in the future as well. The buybacks coupled with continued slight organic growth, added onto by emerging market earnings , will in the end catapult Telenor to the top of the Nordic telco food chain. I don't mind saying that - I believe Telenor has more potential than Telia and Tele2 ( TLTZF ) both. Telia is a classic bond-type telco play. It's a 6-10% annual RoR, with dividends. That's fine. Tele2 is the same, but with the added spice of extraordinary dividends, and it also owns one of the largest cable infrastructures in the nation.

Telenor though, that's the player that can really grow long-term, as I see it. Telenor is A-rated but has used its cash to drive accretive M&As over the past few years. Much of what the company could deliver over the next 5 years is still percolating - we're just now starting to see the implications, as of this quarter , so you really need to bide your time here. That is how I view it.

I expect my Telenor investment to double in the long term. The yield is now over 8% - and it's well-covered - though. That puts it on par with Orange, which is amazing to me, given what this company actually delivers. S&P Global analysts have gone down in their targets from 160 NOK about a year back, to where they currently stand at 125 NOK. That's about a 10% upside from today's level. However, as I've said before, I view this to be entirely too negative for what the company offers.

My previous PT is 150 NOK/share. That's the one I held in my last article. Because I see zero reasons to shift from this target here, I'm not going to shift it. The cost increases were already calculated in that target, but so were the successes in M&As and the company's emerging market pushes.

I want to once again call attention to one of my Norwegian drum-beatings for an undervalued Scandinavian company . Many of you took my stance, some of you elected to ignore it.

The results?

Seeking Alpha Norsk Hydro (Seeking Alpha)

In the end, I invested nearly 4.5% of my entire portfolio into Hydro, which then ballooned to almost 8% of my holdings before I started trimming. Different sectors, but the same logic, and the same country/geography. I do not want my readers to miss out on undervaluation opportunities, so even if you get tired of my beating the drum here, I'll keep doing it to hammer the point home.

Telenor is a real good potential "BUY" here, and I'd like for you to at least take a look at it to see if it might fit your investment criteria - because it fits mine like a glove.

Thesis

My thesis for Telenor is as follows:

- I view Telenor as one of the safest telcos in all of Europe, based on its fundamentals and markets. Safer than Orange, and safer than Tele2/Telia. Perhaps Deutsche Telekom might be as safe, but less than half the current yield - and Telenor also mixes this with growth potential.

- Based on this safety and this yield as well as this upside, I'm marking this company as a "BUY" and considering it with a PT of 150 NOK/share. I am not changing my PT here.

- I believe the right way to invest in the business is native shares only, not ADRs. The native share trades on the Oslo Share exchange under the symbol TEL, and at the time of writing trade hands for about 110 NOK.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company still fulfills every single one of my valuation criteria - this one remains a "BUY", and a more attractive one now that the dividend is clarified.

For further details see:

Telenor: Compelling Norwegian Telco Yielding 8%+ Going Into 2023