TELNF - Telenor's Long-Term Upside Remains Intact

2023-04-22 05:57:23 ET

Summary

- Telenor is a solid company with a significant long-term upside. Since my last article, published at significant undervaluation, the company has recovered somewhat.

- My cost basis is around this level - but I believe the value of the company is quite a bit above what we see here.

- In a bit over 1.5 weeks, we'll have the 1Q23 results - and I believe we're in for a good year of Telenor. Here is why.

Dear readers/subscribers,

Since my last article on Telenor (TELNF), the company has seen outperformance in terms of the S&P500 and other indexes. I've seen my position appreciate by double digits, while other indexes are flat or down. I tend to focus on cheap companies or businesses that I believe to be cheap. Sometimes I go in too early - but other times, I manage to pick companies at more of the right price - the bottom price before reversal.

But in either case, I try to only pick qualitative companies, so that even if we do end up owning something that goes down, we needn't be worried because what we've bought is a qualitative business that could trade "down" for many years without really impacting the long-term viability of our investment.

I've been buying Telenor for as long as it's been undervalued. And this is what the company has done since November.

Telenor Article (Seeking Alpha)

Telenor - The upside is smaller, but still there

So, if you didn't buy Telenor when it was at double digits, you shouldn't be surprised that the upside is now far smaller. While my entire position wasn't established below 100 NOK, I managed to lower my cost basis well below 140 NOK/share, to where I am now seeing a Yield on cost on my position of more than 7%. That is why I invest in telecommunication companies. The high, safe yield, backed by solid, recurring cash flows, and with the slight chance of capital appreciation and outperformance, similar to what we saw from Tele2 (TLTZF) when I last sold part of my position at a high profit.

That is, how I believe, we should handle Telcos. Buy them cheap, enjoy the yields, then trim them when expensive. Telenor's expensive valuation is closer to above 155-160 NOK, as I see it - we've seen the company reach those levels a few times in the past 10 years.

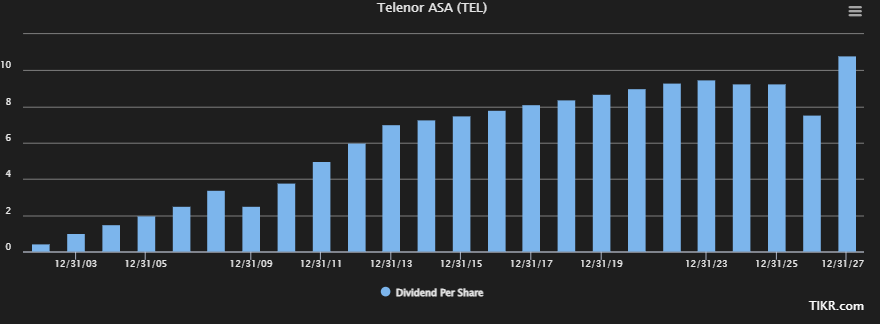

Telenor is one of the best telecommunications companies. The company's gross, operating, net margins, and return metrics are well above the 85th percentile in the telco industry. In the industry, Telenor plays with peers such as T-Mobile ( TMUS ), Comcast ( CMCSA ), Verizon ( VZ ), AT&T ( T ), Deutsche ( OTCQX:DTEGY ), Vodafone ( VOD ) and many others. Out of these mentioned, Telenor is comparatively small at around $17B in market cap, with TMUS being the largest at around $175B. But Telenor still has plenty of things going for it - and that is beyond the high dividend yield of over 7% even here - and that yield is well-covered here with a very long tradition. And it's not expected to go down either.

{kind=link}

So, in investing in Telenor, you're betting on a 7% yield that's bound to grow or stay around at this level, while the stock might have potential upside - more on that valuation-related upside later.

The past few quarters, including this latest one of 4Q22, have clarified the picture of the overall ebb and flow of the company's business. And while the overall mobile performance for the company is an unerring, stable business over time, and the company's investments are paying off, the company is experiencing some instability.

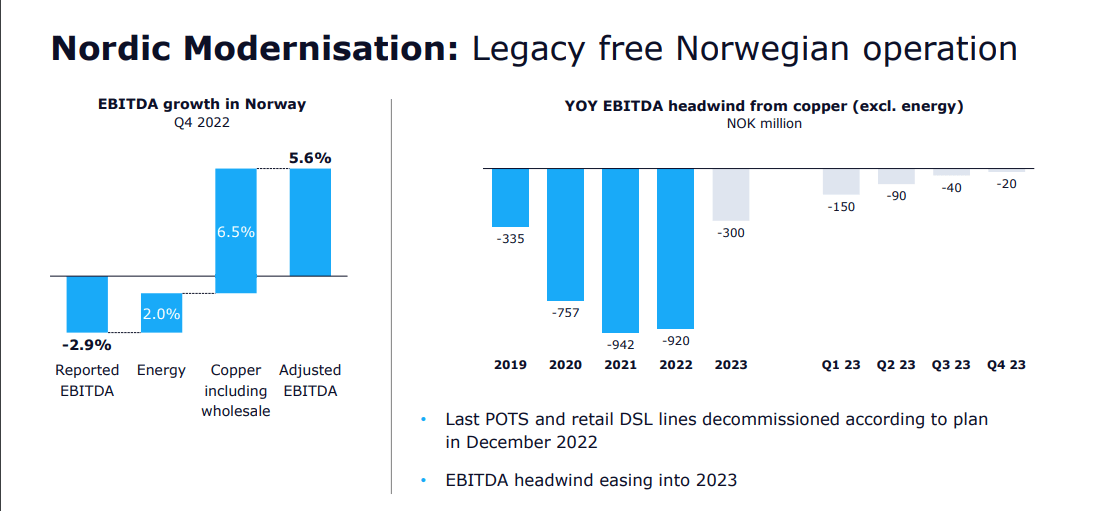

Remember, Telenor is a combination of stable home markets - Scandinavia. For several years, there hasn't been any home-market trend breaking that could have justified what has happened here in terms of the share price. The company can really do very little "better" in those geographies, given how mature these markets are. 0.5% organic growth is really some of the best results which can be expected here. Its growth comes from its investments in emerging markets. Legacy operations are focused on winding down copper networks, and maintaining its market leadership where possible, while gaining market leadership or share in Malaysia, Thailand, and other areas.

{kind=link}

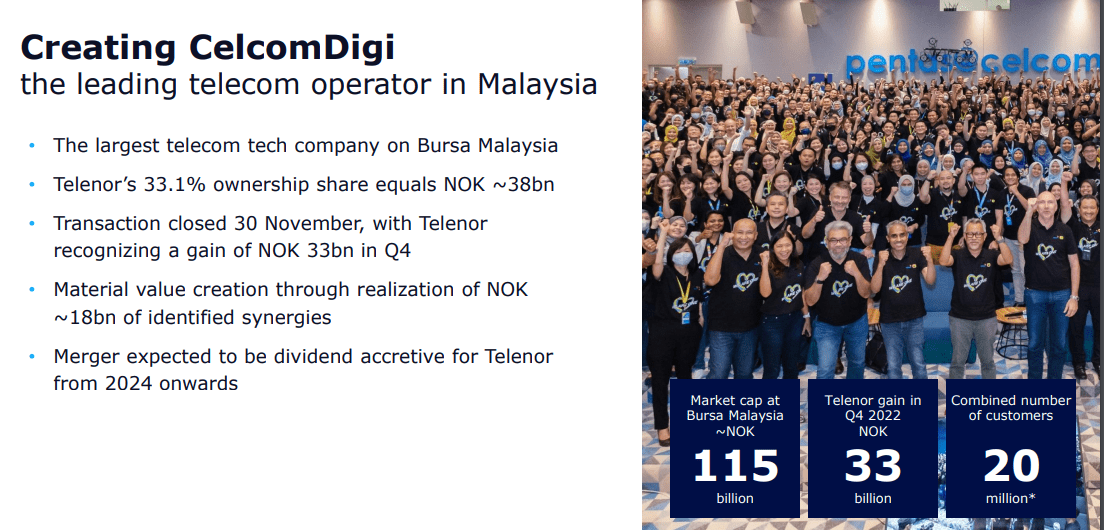

The completion of the merger in Thailand in the last quarter marks the final phase, and we'll get an update on this merger in a week or two, where the company is expected to create the #1 Thailand telco with a combined number of customers of 55M, where Telenor has a 30% ownership.

The company is also rationalizing its legacy operations. Telenor has sold 30% of its legacy fiber business to KKR and Norwegian pension funds at over $1B. It's more of a partnership than a sale, given that the transaction concerns over 130 000 km of cable connecting large parts of the Norwegian population, while Telenor retains a solid 70% ownership stake, enabling monetization of another 19% if the company so desires. proceeds. Legacy ARPU has been growing, and Telenor is moving ever closer to a copper-free operating profile.

{kind=link}

While the past few years have meant plenty of pain for Telenor investors in terms of their returns on the capital appreciation side, this is easing, at least insofar as EBITDA for home regions go. Much like with other European telcos, Telenor has been front-loading its CapEx for several years with 5G rollouts. The past few years have been strategy - including these carve-outs and mergers we're seeing now, to make the company stronger for the future.

The company's goal is legacy Scandinavian leadership combined with Asian telco expansion, which has realized many of the company's growth targets - such as low single-digit revenue growth, and a 16-17% CapEx in terms of sales. 2022 came in without surprises for Telenor.

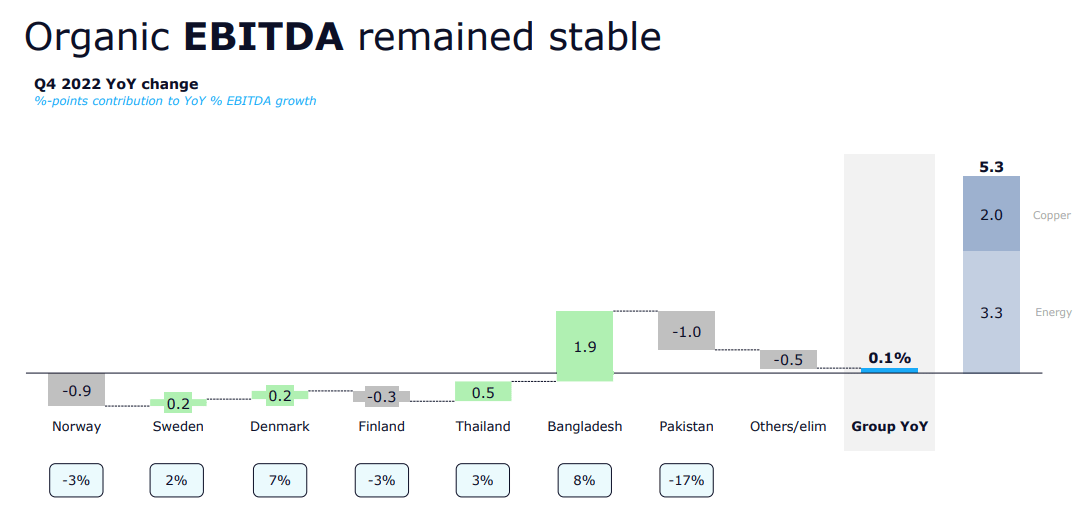

And you know what - 2023E is, at this time, expected to be much the same for this business. Yes, operating expenses are increasing. Energy is a factor, and even without energy costs, OpEx was up 5% from a combination of salaries, sales, maintenance, and other OpEx. However, energy costs were actually lower than expected for the year, and the company's organic EBITDA trends remained quite good. Despite immense pressure, the company was flat here during this year.

{kind=link}

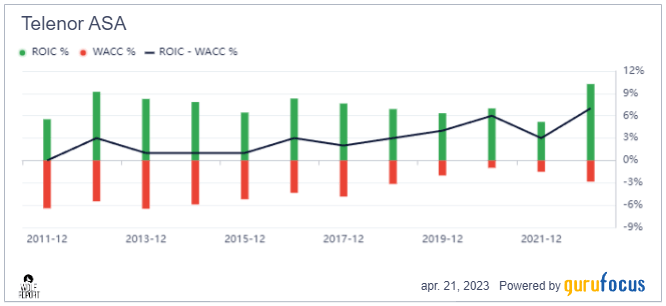

Telenor remains a very profitable operating, and its profitability and debt have gone down as we've seen improvements. You can see the stability and improvements in things like the company's ROIC compared to its WACC.

{kind=link}

There are risks. We're looking at things like operating margins somewhat declining, rev/share in very slight decline, but that's really as far as negatives go. Some would say that in terms of valuation, Telenor isn't cheap here. I would say Telenor isn't as cheap as it has been, but to say that it's unattractive here is to do the company a disservice, as I see it.

Let me show you what I mean.

Telenor - The valuation is higher, but the upside is still there.

I miss the time when the company was trading at a double-digit share price. That upside and nearly 9% yield was no joke - but even at 120-130 NOK/share, Telenor is still attractive enough. The reason for owning Telenor is two-fold.

A company like Telenor provides me with a very good yield, throwing off thousands of dollars every year, and also have given me very good capital appreciation at times, and now the potential for it.

The capital appreciation has been so-so for a few years now - but I believe that it's coming back, and with the tens of thousands I've made in dividends, my eventual RoR will significantly outperform the overall average. The company might be more volatile than your typical telco because of its Asian projects, but the fundamental substance of the company is beyond stable.

Now, most analysts haven't "corrected" their overall assumptions. 18 S&P Global analysts follow Telenor, and they still consider the company at an 86 NOK low to a 170 NOK high, with a current average of 130 NOK. that's around the current price. But a year ago, the company was at around 152 NOK in target share price - and very little has changed in company fundamentals since then. This is why I don't give too much credence, and why 8 out of 18 analysts at a "BUY" or equivalent doesn't really faze me.

Remember also, Telenor is an A-rated business - many investors tend to forget this. While some analysts do consider the company at a fair value here, I believe those analysts are not giving the eventual upside once many of the company's strategies are done, enough credence.

Much of what the company could deliver over the next 5 years is still percolating, and investors should view an investment into Telenor as a mid-term investment at the very least - if not very long-term. That is how I view it.

From my current cost basis, I expect an upside of no less than 60-70%, far more with dividends. None of the current valuation assumptions take into account the full growth potential in the Asian market, and Thailand and Malaysia specifically. Good materialization here would put the fair value for the company well above 200 NOK/share.

Current averages are 125-145 NOK per share - and this is also where most current analysts land - somewhere in the middle. I was at 150 NOK for my PT in my last article, and as things stand, I am not lowering that price target. If you recall when I beat the drum for Norsk Hydro ( OTCQX:NHYDY ), I view this as a similar play,

If you want a good yield at a good price, with plenty of upside potential, still say that investing in Telenor is a good way to get it. My trimming will start once we hit above 170 NOK/share, and this is still ways off.

This leads me to my current thesis.

Thesis

My thesis for Telenor is as follows:

- I view Telenor as one of the safest telcos in all of Europe, based on its fundamentals and markets. Safer than Orange, and safer than Tele2/Telia. Perhaps Deutsche Telekom (DTEGY) might be as safe, but less than half the current yield, and isn't as undervalued as of April of 2023.

- Based on this safety and this yield as well as this upside, I'm marking this company as a "BUY" and considering it with a PT of 150 NOK/share. I am not lowering my PT here.

- I believe the right way to invest in the business is native shares only, not ADRs. The native share trades on the Oslo Share exchange under the symbol TEL, and I would not invest in any Norwegian company except by buying the native share.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized) .

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Telenor still fulfills almost every one of my criteria, despite not being able to exactly call it "cheap" any longer.

Thank you for reading.

For further details see:

Telenor's Long-Term Upside Remains Intact