TELNF - Telenor: Solid Fundamentals High Dividend Yield And Undervalued

2023-09-18 03:20:27 ET

Summary

- Telenor stock is undervalued and offers a high dividend yield with solid fundamentals and safety.

- The company's balance sheet is well-prepared for any downturns and it has a strong track record of profitability.

- Telenor's operational excellence and growth in emerging markets contribute to its potential for long-term ownership.

Dear readers/followers,

Part of the trickiness of the current environment has to do with what we pay for companies that are set either to not grow at all or that are showcasing potential for negative forward growth in terms of earnings - at least for the near-term foreseeable future. Such companies may still have very solid safeties and fundamentals. What's more, they may be extremely high yielders, with proven resilience and the sort of asset base which in some ways ensures their near-term to medium-term safety.

Such is the case with the company that I'm going to talk about here today - because I've covered it exceedingly often on Seeking Alpha. I will continue to cover it in the way that I have been doing for as long as the company remains undervalued.

And I still consider Telenor ( TELNY ) ( TELNF ) to be very undervalued here. The company combines appealing factors of fundamental infrastructure with a high dividend safety. While Telenor is unlikely to significantly appreciate in the short term, I see good potential for long-term ownership here.

Let's go through the potential here.

Telenor - Plenty to like even at a slightly recovered valuation

My last article on Telenor was over 2 months ago at this point, and I was positive. Since that article, we've seen company outperformance, even if only slightly. Since I loaded up back in the fall of 2022, we've seen double-digit appreciation inclusive of dividends - but that is still less than the market here. Telenor has yet to see a fundamental reversal, and I don't believe it is likely in the next 2-3 years under the current set of forecasts.

But that also does not matter to me.

Why?

Because I'm in this one for the long-term - and because Telenor is a close to 8% yielding telco with an extremely good dividend track record backed by some of the most solid assets and geographies around.

It's very similar to Verizon ( VZ ), a company in which I also own significant shares, at a yield of close to 7.8%. When I look at companies with what amounts to essentially zero growth, a minimum of 6% yield that's solid and likely to remain in the minimal of my demands for the company. I'm willing to wait years for reversal if need be - as long as what I buy is good enough to make me confident in the company.

That is the case here.

This is a significantly above-average Telco. By that I mean the company works with 74%+ gross margins, a very solid RoE, good RoA, and excellent profitability despite sub-par leverage and some other more fundamental issues. The company's business model not only works, it works very well.

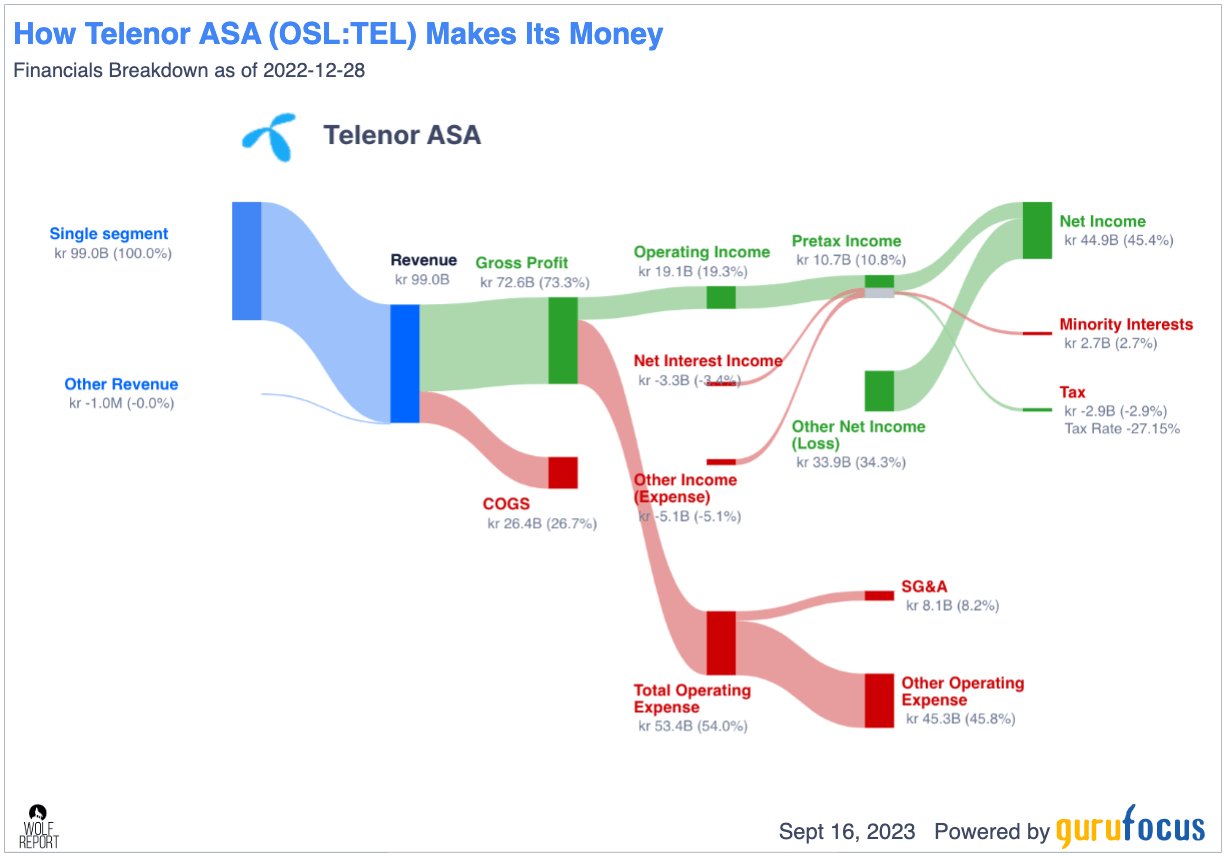

Telenor Fundamentals (GuruFocus)

{kind=link}

And despite what I said about fundamentals, the company's balance sheet is well-prepared for any sort of momentary downturn in the sector that may come the company's way. Company profitability has never been negative for the past 10+ years, and where other telcos have failed to capitalize on emerging market trends, Telenor has actually managed this quite well.

The latest set of results is a testament to Telenor's operational excellence. We see slight home market growth - meaning Nordic - and we see EBITDA and the ever-important expansion CapEx very much in line with projections. There's a sense of group-wide momentum in the results that belies the supposed instability or justified low valuation of the entire sector.

Telenor will never be "cheap" to run. Payments for spectrum, high continual investment needs, and other factors ensure that this will always be a company that needs to put much of its cash flow to work in its assets - but shareholders will, as I see it, continue to be well-rewarded for their patience.

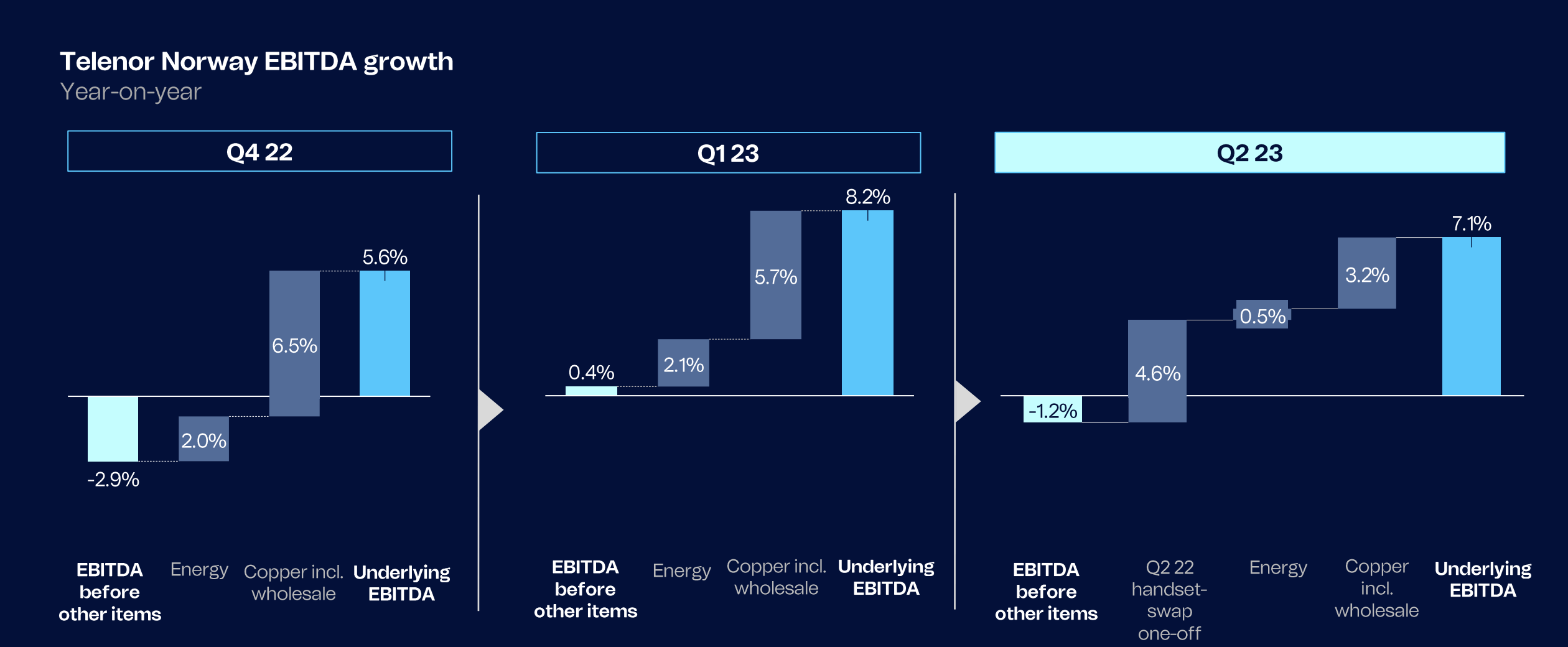

As an example, here we have a home-market Norwegian growth rate.

{kind=link}

And this trend is expected to be maintained. Preliminary targets and indications for 2H confirm a healthy subscriber and pricing environment, with really no significant headwinds in the home market for 2H. CapEx/Sales are still higher than some of the companies like Orange ( ORAN ) who were front-loaded with their initial CapEx for rollout, but Telenor is catching up - and this of course also includes WC optimization.

These overall Nordic optimizations are by the company expected to bring about OpEx reductions of 1-3% in a timeframe of 3 years from now which should be cause for at least some stabilization in the share price.

Meanwhile, the company's emerging markets continue to be a major factor for the business - and unlike many competitors, the company actually manages well here.

{kind=link}

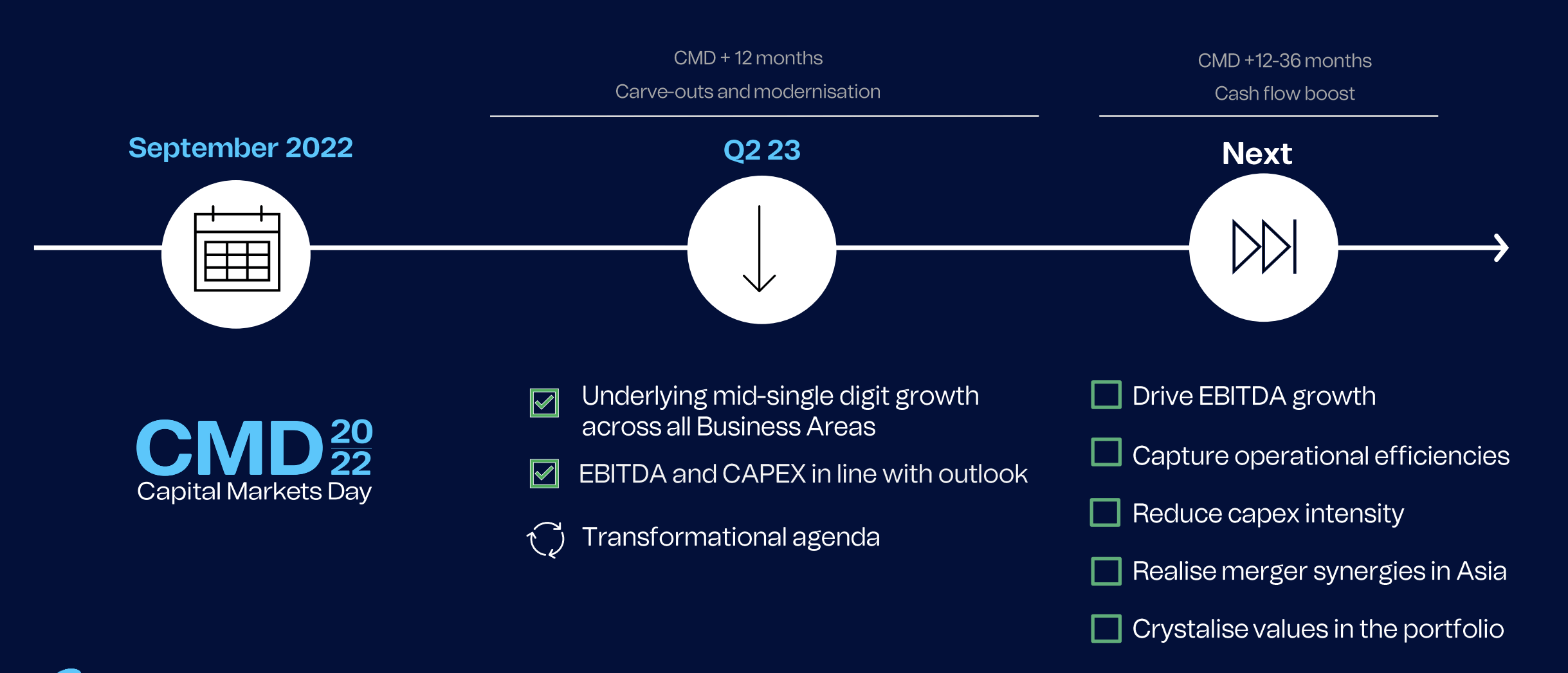

Telenor also, for those interested in such things, are fairly ahead in terms of ESG with things like Climate-based supplier targets, renewable exposure, green data centers, and other things. , I'm more focused on the economic and operational side of the business, and less on pushes such as this. The bottom line interests me, and thankfully Telenor does not disappoint here.

Its targets from 2020-2022 are starting to be realized, enabling Telenor to move into the next phases of its plans.

{kind=link}

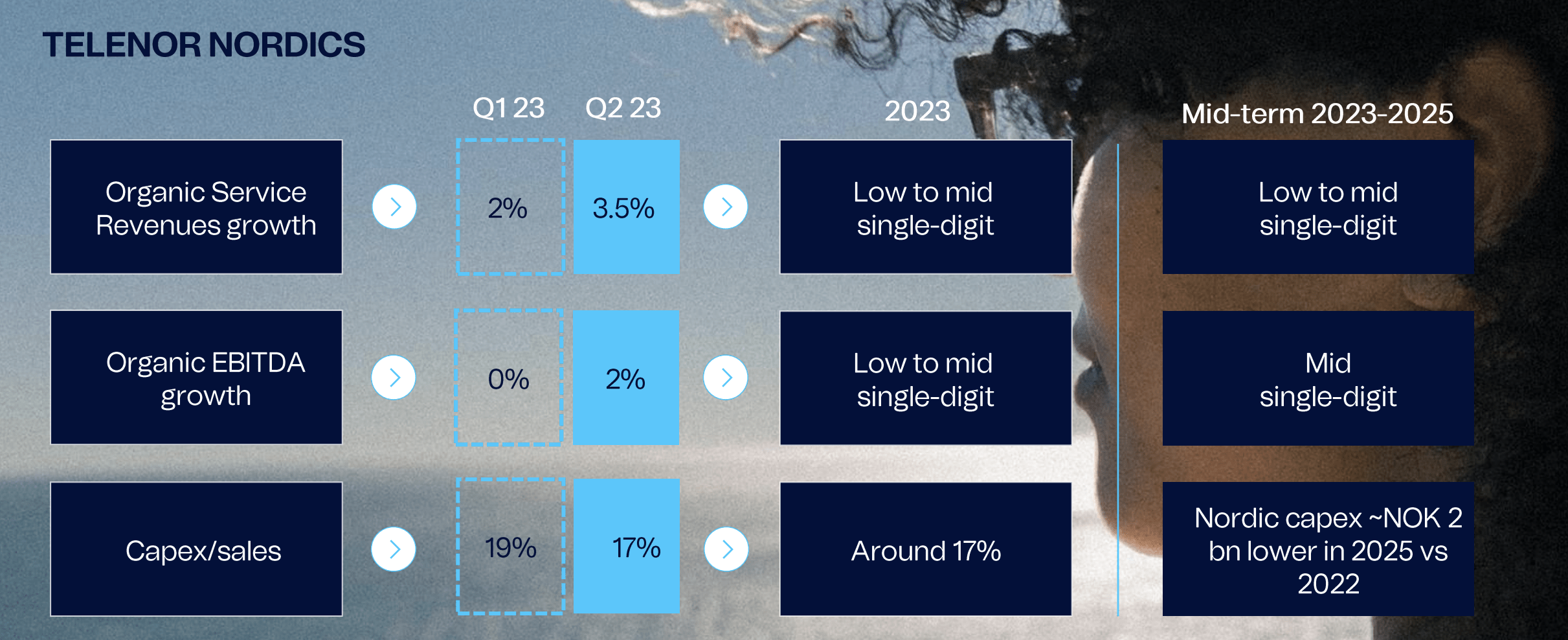

Some numbers. A 4.4% service revenue growth company-wide and 4.1% group-wide EBITDA growth means that Telenor is not beating inflation - but no telco in northern Europe I know of is actually doing that (Source: Telenor 2Q23 results /Telia/Tele2 results). 17% CapEx/sales means that Telenor is lagging some of its European peers, but not to a worrying degree. We're not talking 18-20% CapEx. FCF is still negative - but only on a pre-M&A basis. The overall picture I see is that the mature markets, meaning the Nordics, are growing in accordance with expectations. Churn is very low - this is the case for all operators, at least all major ones here.

Meanwhile, Asia is continuing to act as the growth motor for the company. With 5% service growth in revenues, all of it organic , there's room left to expand here. EBITDA is expanding even more, above 5% - again organic. The company's infrastructure arm is seeing even better growth, with a 16.2% increase in Organic EBITDA, now to over half a billion NOK on a quarterly basis after leases.

Telenor is a cash-minting machine - and at least 7.5% at the current price level of that cash is going straight into your pocket in the form of a dividend, paid bi-annually. Several telcos, such as Telia ( TLSNF ) have actually moved to a quarterly payment model as the markets grow more and more international, which is of course a welcome change. I don't think we'll see any Swedish company move to a monthly model - too much bookkeeping - but quarterly doesn't seem to be much of an issue.

Company OpEx is up - around the same as EBITDA - mostly from energy costs, SG&A, and personnel. Not much Telenor can do there except to continually optimize its assets, which they are in the process of doing.

Leverage for the company is actually up - on the basis if net interest-bearing debt/EBITDA (including dividends from JV's/associates), to a current 2.4x, which is slightly above its 2.3x max target. This is mostly due to adverse FX and some Asia non-recurring FCF though, so this is expected to actually drop down again within a few quarters. Telenor has been in the 2.1-2.2x range for a long time at this point. Its target is not to go below 1.8x.

What's more, Telenor also reaffirmed its outlook for the rest of 2023. The visibility for results here is very solid/high.

{kind=link}

Let's look at company valuation to see what sort of upside we have going for us here.

Telenor - Continued upside even with conservative estimates

My stance is that Telenor will continue to offer outsized potential returns even if the company growth rate is flat or slightly negative. The reason/s for this has to do with the sheer quality of assets we're talking about.

Telenor is A-rated, one of the very few Telcos that command an S&P Global A-rating, and this should tell you something of the business. Even if 2023 is likely to be an adjusted EPS decline year due to comparative/non-recurring items, we're back to growth next year, and more growth in 2025E as I see it. We've already moved from the lower trough levels of close to 80 NOK/share, but you don't need to expect outsized valuation trends to find nearly 20% per year in combined yield and potential capital appreciation here.

Telenor Upside (F.A.S.T graphs)

{kind=link}

That means that at 119, there's potential for a 50% total RoR that doesn't entail the company trading at above 155 NOK. That's a very good set of estimates, backed up by the fact that we're talking historical premiums, and nothing really beyond that.

The underlying trends here are actually extremely solid. Service revenue growth is solid across the board, with very specific and almost only 1-2 exceptions. Otherwise, it's all up. And debt? Nothing close to speaking about here - most of it is beyond 2028. The company is past the ROCE-trough of 2021 and is expected to normalize around 14-16% on a forward basis, at least according to the company's own estimates (Source: Telenor 2Q23 results )

S&P Global analysts still give this company a very wide target range, in this case as of September of 2023, 90 NOK to 160 NOK at this time, with an average that's down slightly to 130 NOK since my last article. 19 analysts still follow Telenor, and out of those, 9 give the company a "BUY" or equivalent - not the highest, but certainly not the lowest either. There are plenty of analysts on the fence here due to the company's likely negative 2023E year in terms of GAAP, but there is still close to a double-digit upside to the current average PT here. Don't get me wrong - I hope you bought the company at double digits when it yielded close to 9%. I know I filled up at the time, and that's why my overall yield on my position is over 8%.

I also won't change my PT here. I firmly believe that Telenor is well worth upwards of 150 NOK per share, and that argument is starting to be easily digestible when we're trading at around 120 NOK per share. I would start carving off some shares at a price of 155 or above - that's probably the biggest change in my stance. I no longer believe that Telenor will, or should trade above 185 NOK - so I'd start pruning at 155+.

Options are unfortunately usually not a good play here. The premiums and strikes are too unfavorable. You're better off owning the common. Buy-writes make little sense either to me because I believe the company will rise well beyond levels that would see profitability for me here.

Thesis

My thesis for Telenor is as follows:

- I view Telenor as one of the best telcos in all of Europe, based on its fundamentals and markets. Safer than Orange, and safer than Tele2/Telia. Perhaps Deutsche Telekom ( OTCQX:DTEGY ) might be as safe, but less than half the current yield.

- Based on this safety and this yield as well as this upside, I'm marking this company as a "BUY" and considering it with a PT of 150 NOK/share. I am still not lowering my PT here as of September of 2023.

- I believe the right way to invest in the business is native shares only, not ADRs. The native share trades on the Oslo Share exchange under the symbol TEL, and I would not invest in any Norwegian company except by buying the native share.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I call the company "cheap" here, and it fulfills every single one of my investment criteria.

For further details see:

Telenor: Solid Fundamentals, High Dividend Yield, And Undervalued