TELNF - Telenor: This Telco Is A 8.5%+ Yielding Income Play

2023-07-17 01:35:17 ET

Summary

- Telenor is viewed as a strong buy due to its consistent dividend payouts and potential for a reversal in the communications sector.

- The company's recent results and strategic objectives suggest promising 2Q23 results.

- Telenor's recent merger in Thailand and its focus on becoming a legacy-free operator are expected to significantly increase its overall EBITDA.

- The company is also targeting EBITDA growth driven by modernisation and reducing CapEx in the Nordics.

- Despite challenges in the telco industry, Telenor's profitability sets it apart. The company trades at close to 10-year lows.

Dear readers/followers,

The time has come, following a double-digit drop, to update my thesis for Telenor ( OTCPK:TELNF ) before the 2Q23 results. I argue that it's an excellent time to buy the Telco here specifically before results, because while the company may report below consensus, the recent results in 1Q23 including the execution of strategic objectives, give the high possibility of the company actually delivering some very good results.

I'm going to take this opportunity to show you why Telenor remains, with Tele2 ( OTCPK:TLTZF ) and Telia ( OTCPK:TLSNF ) my largest communication holdings. None of these businesses are currently flying very high. That's fine with me - the reason I own them is their consistent dividend payouts, coupled with the sheer magnitude of the reversal potential once things in the communications sector start turning around a bit. When exactly this is going to happen is a difficult question to look at - we're not clairvoyant after all.

But I can see a significant upside for the company here, and I continue to view Telenor as a "BUY".

Here is why.

Telenor - Plenty to like about Undervalued Telco

Telco's have been out of favor for a long time now, it seems like - and the reasons for it are not exactly secret, or hard to understand. The high interest rate environment we've entered means that their debt, which is usually rather substantial, is quite expensive. It also means that building is more expensive, and when we couple this with the competitiveness of the sector impacting overall pricing power, we get a picture where earnings growth , much like in some REITs, is going to be a very limited sort of possibility for the next couple of years.

Going into Telcos, this is something you most definitely should be aware of.

Does this make telcos uninvestable?

No, of course not.

I've hundreds of thousands of dollars invested in Telcos across my portfolios, with companies from different countries, and with different profiles. My favorite telco profile is one that doesn't rely on content, and instead focuses on mobile/fiber together with strong B2b, maybe with a burgeoning or potential TowerCo in the mix as well.

Couple this with a high yield - which we usually have here, and you get some impressive and interesting forward trends.

Enter Telenor - Norway's largest telco and their recent results.

{kind=link}

"Slow but steady" is a fair assessment of the company's recent set of results. The company finished its long-awaited merger in Thailand, creating a market-leading Telco with more than 6x of the Norwegian native market population, potential synergies of over $2B going forward, and a potential market cap that's likely to close to $10B in the foreseeable future. Telenor's share of this merged business is 30.3% , meaning this is likely to become an interesting holding going forward.

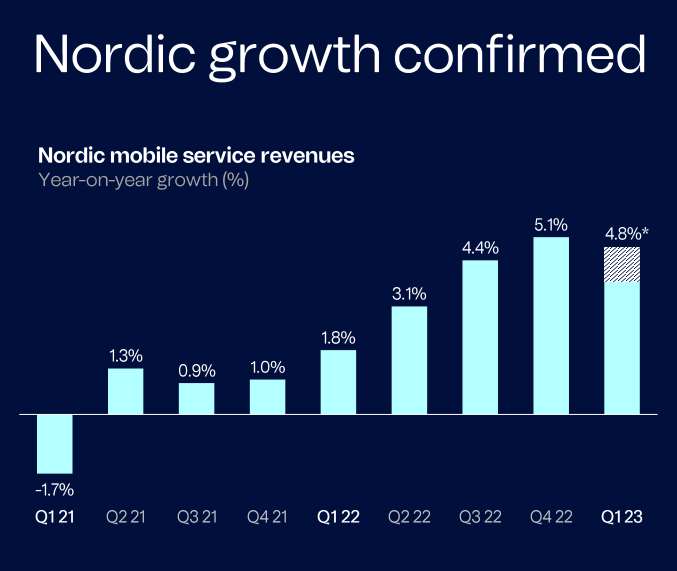

The notion that telcos aren't growing is demonstratively false. This is especially true for Telenor, which is actually growing more the past 2 years, not less.

{kind=link}

The problem is how those revenue growth rates translate into the bottom line because that's become significantly harder the past 5 years. However, Telenor has some advantages that other Scandinavian telcos are also playing at.

Namely, all of them are targeting to become legacy-free operators. Once these synergies hit home with no legacy networks to manage, the company will see significant increases in overall EBITDA. 1Q23 marks the completion of several corporate milestones, including but not limited to:

- Malaysia Merger now closed

- Closed Fiber transaction in Norway completed.

- Copper networks are being decommissioned.

- Thailand merger completed

Going forward, the company will target EBITDA growth driven by modernization, reducing the amount of CapEx needed in the Nordics, which will boost Nordic earnings, see some of those Asian synergies pay off, and work to increase value in infrastructure. But the way the market is punishing Telenor, you'd think that 1Q23 including 2% EBITDA growth year-over-year from a 3% rev growth did not happen - nor that Telenor managed to generate 6 billion NOK worth of EBITDA , despite an 18% CapEx/sales ratio. This is significantly above some European peers, but Telenor is not as far along as some of the companies that have already started lowering CapEx to the 14-16% range, such as Orange ( ORAN ).

The big question with Telenor is when we'll start to see real value from Asia - given the amount of "goals" the company has hit over the past few quarters, I say that we're close to starting to see some real upside here. The company actually received its first dividend from CelcomDigi, almost 275M NOK for a single quarter, with full contribution expected from 3Q and forward.

Also, the market keeps underestimating the infrastructure segment. There is so much dormant value here that's slowly improving - revenues and organic EBITDA are already growing for the segment.

Telenor IR (Telenor IR)

The stance that Telenor's earnings growth will be somewhat muted going forward is nothing to discuss. The entire telco industry is feeling the pain, with giants like AT&T ( T ) and Verizon ( VZ ), both of which I also own stock in by the way, continue to be pressured by the market.

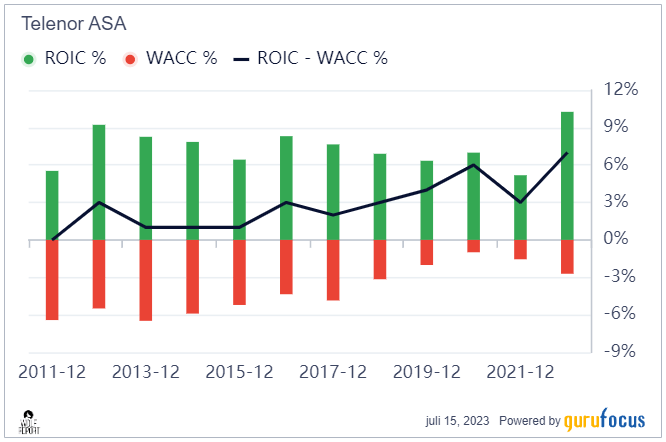

Where Telenor actually differs is the profitability. With a 70%+ gross margin, a near-20% operating margin, and solid net margins, this company is one of the market-leading businesses in the entire telco sector. Looking at RoE, RoA, and ROIC, Telenor manages to be in the 95th-98th percentile in the entire sector (Source: GuruFocus) - and that includes some of the large peers I recently mentioned.

The negatives for Telenor are the same as for most telcos. Increased interest rate pressure and macro are working against the company's operating margin, which is declining. The revenue per share, barring small growth, is also relatively flat. But the company trades at close to 10-year lows both in terms of earnings and assets, and it's an incumbent telco that isn't going anywhere in a geography that doesn't have room for any new entrants to even start trying to "get in" here - I'm referring here to Scandinavia. It also adds to this with its growth projects, many of which have already started paying dividends, both figuratively and literally.

The company is chronically profitable and sees increasing profitability on a 10-year basis in the form of increased ROIC.

{kind=link}

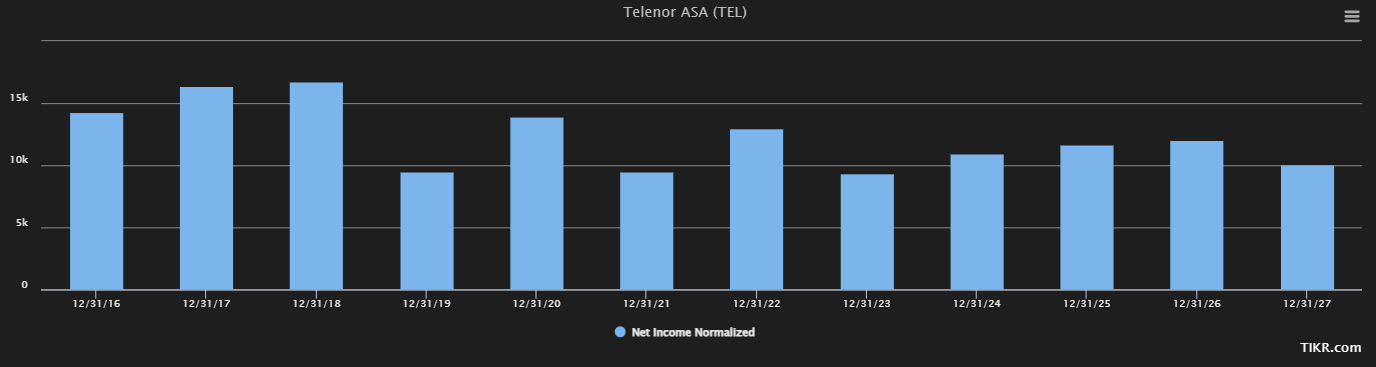

Current estimates are for the revenue to trail down in 2023, troughing this year, before picking back up again and climbing back until 2027E and beyond, as fundamentals and the operating environment improves. Company net income is expected during this time to remain at levels where the company can still comfortably execute on its strategy and investments as well as pay out the dividend.

{kind=link}

Overall, this is a company I view as an extremely attractive income investment with a great upside. Expenses and costs are increasing - as are they for most companies, really - but Telenor is also seeing increased revenues and earnings, despite energy costs still being a significant overall impact on the company.

The company recently reiterated its 2023 outlook, calling for low-to-mid single-digit growth in revenues, and similar growth in company EBITDA, with a CapEx to sales ratio that's likely to drop to around 17%.

Overall, I believe there is enough reason to be positive about the company here and to view the valuation for Telenor as a significant positive - and I present to you the following case for Telenor.

Valuation for Telenor - a good upside

Telenor remains an attractively-valued Telco. We had a short period during the past few months when the company climbed to the 130+ NOK level, only to decline back down south over the past month.

However, Telenor's yield remains at a very attractive level over 8% considering the company's current dividend. The current valuation also means the company is trading at less than 15x P/E - it's above some of its massively undervalued peers like AT&T and Verizon, but it's below some of its European peers.

What's more, I believe Telenor actually warrants some of the premium the company is currently assigned. The company is conservatively leveraged to some of its peers at 45%, it's A-rated from S&P Global, it has a market cap of almost 150B NOK despite the drop we've been seeing here.

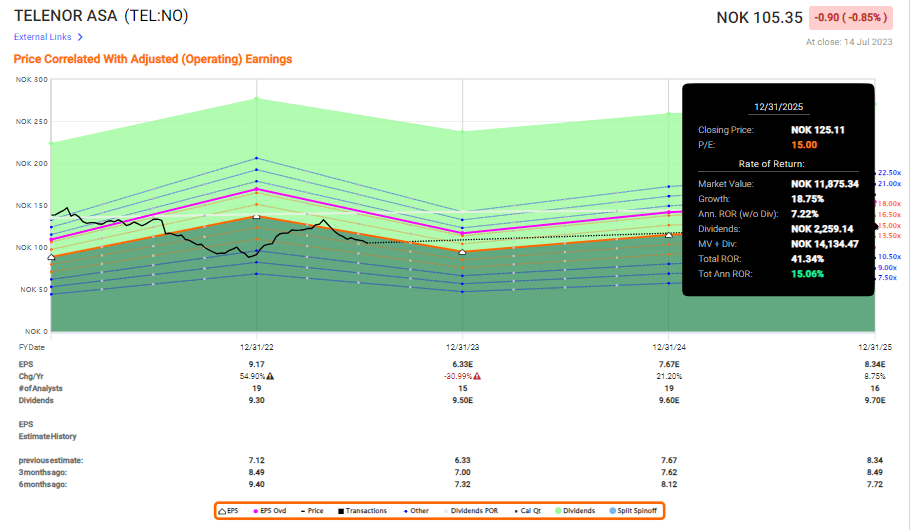

Even on a 15x forward P/E, which is the lowest I can see myself forecasting Telenor at for the long term, I expect a 40%+ 3-year RoR, given the current forecasts. That's over 15% per year.

{kind=link}

Now, this is with dividends - naturally - but this is what I consider to be valid for the company, and because it's an income investment, I don't expect much more than this. It's the safety and the income I want - and the company provides this in spades.

S&P Global analysts give this company a target range from 90 NOK to 155 NOK at this time, with an average that's up to 135 NOK since my last article. 19 analysts still follow Telenor, and out of those, 9 give the company a "BUY" or equivalent - not the highest, but certainly not the lowest either. There are plenty of analysts on the fence here due to the company's likely-negative 2023E year in terms of GAAP, but the upside to that target is still more than 25% at the current share price.

My last price target for Telenor was 150 NOK/share - and I'm not changing that. I see no reason to - my long-term thesis for the company always included a shift in interest rates, and the fact that it might be more than previously assumed isn't a reason for me to change anything here - it's not significant enough for that, as I see it.

Like VZ and T, I view Telenor as a very solid income investment. There might be some shorter-term pain before these companies revert - maybe it'll take until we see a revision in interest rates - but that makes them excellent investments, and I believe investors may regret in 5 years not buying them here.

Because of this, I view Telenor as a "BUY" here. I also believe specifically that it can be bought before they report 2Q23 because if 1Q is any indication, things might go up.

My thesis for Telenor is now as follows.

Thesis

My thesis for Telenor is as follows:

- I view Telenor as one of the best telcos in all of Europe, based on its fundamentals and markets. Safer than Orange, and safer than Tele2/Telia. Perhaps Deutsche Telekom ( OTCQX:DTEGY ) might be as safe, but less than half the current yield.

- Based on this safety and this yield as well as this upside, I'm marking this company as a "BUY" and considering it with a PT of 150 NOK/share. I am still not lowering my PT here as of July of 2023.

- I believe the right way to invest in the business is native shares only, not ADRs. The native share trades on the Oslo Share exchange under the symbol TEL, and I would not invest in any Norwegian company except by buying the native share.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I call the company "cheap" here, and it fulfills every single one of my investment criteria.

For further details see:

Telenor: This Telco Is A 8.5%+ Yielding Income Play