ARE - Teleperformance And Alexandria Real Estate: 2 Companies With Potential Triple-Digit Upside

2023-09-12 00:15:32 ET

Summary

- Teleperformance and Alexandria Real Estate are undervalued companies, both investment-grade rated and with great upsides in yield and capital appreciation.

- The companies have proven history of hitting analyst targets and are estimated to experience double-digit earnings growth for the next 3 years.

- Despite recent drops in stock price, Teleperformance's fundamentals remain strong, with solid revenue growth and robust business development.

Dear subscribers,

Today's market is very volatile. This means we want to make sure that when we do invest, we invest in companies that combine capital appreciation with fundamental safety and good dividends. It is when you combine the qualities of "exhaustion", which is when investors seem to have "given up" on a stock or when the sell-off seems extreme or at least significant, but when the underlying stocks or companies are still very safe, or conservative.

There are plenty of such opportunities on the market today, and indeed choosing just two is a challenge for me. I could write several such articles, even articles like this involving every single sector or geography I cover. While the stock market when it comes to certain companies is still pretty richly traded, we can also see companies in virtually every segment that have this sort of upside.

Whether you're talking about finance, utilities, energy, consumer staples, consumer discretionaries, or real estate - whatever your "poison" is, there is plenty to invest in on the market today.

In this article, I'm giving you two of my companies I don't believe you should miss out on unless you have a very specific reason for doing so.

Let's get going.

1. Teleperformance ( OTCPK:TLPFY )

Yes, I know you've heard me talking about this company before. Like I do whenever there's a significant sale, I won't stop talking about the company until it actually recovers, or something fundamental in terms of risk actually materializes.

Teleperformance is the largest call center operator on the planet, and the company is very much in the "now" when it comes to things like AI and digitalization.

The company, as I see it, is the most undervalued company in the entire telecommunication sector - at least insofar as the companies I cover.

Let's go through the list:

- The company is BBB-rated.

- The company has a yield of over 3.2% at the current valuation, and that yield is covered at a payout ratio of 30% in terms of adjusted EPS.

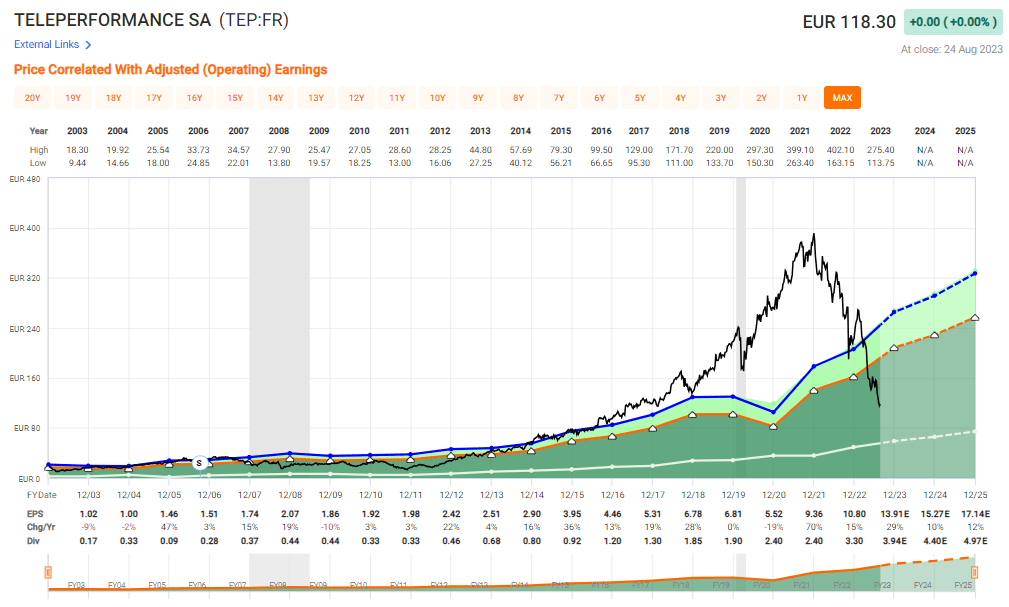

- The company typically trades at a 19x P/E. The current valuation is 9.24x.

- The company recently M&A'ed on of its significant competitors, Majorel

- The company has a proven history of hitting analyst targets, with a negative forecast failure of 8% of the time on a 2-year basis , the rest of the time the company either beat estimates or hit them (Source: FactSet)

- The company is estimated to experience earnings growth, double-digits every year for the next 3 years.

So why is Teleperformance out of favor?

Because it's coming from one of the largest, and longest overvaluation spikes for this sector in a long time.

{kind=link}

Most investors that invest in companies, or are on the stock market to any degree, have a woefully short attention span/patience. I've found that to invest effectively and profitably, you need to be able to act flexibly. At times, there will come developments that cause stocks to rise 100-150% in a very short timeframe. It's imperative at this point as I see it, that you have included in your strategy the ability to rotate such overvaluations when necessary. I have multiple examples, both local and international of such investments which would have resulted in far less positive outcomes had I not trimmed, rebalanced and sold my holdings.

At the same time, if a company is dropping as we see Teleperformance currently doing, you need to be able both mentally and financially to stay the course until either the upside or clarity regarding the downside materializes. And frankly, if there is a clear non-recoverable downside, you shouldn't even be investing in the first place.

What I mean is that I see investors often leaving investments behind far too early simply because the stock continues to drop.

My reaction to this is; "So what?"

If the thesis hasn't changed, if the upside hasn't changed, if the fundamentals haven't changed, why would you sell?

I find the company more attractive now, and my slight negative in my overall portfolio position is a non-issue to me. First, due to diversification. No company is more than 4% of my portfolio. Secondly, because I don't invest in anything, no matter what it is, lightly. Every one of my investments usually has multi-year timeframes and upsides.

If the company takes years to get there, I do not care. I've become better at this over the past few years, but it still surprises me that investors with over 25 years of market experience seem liable to fall into this trap.

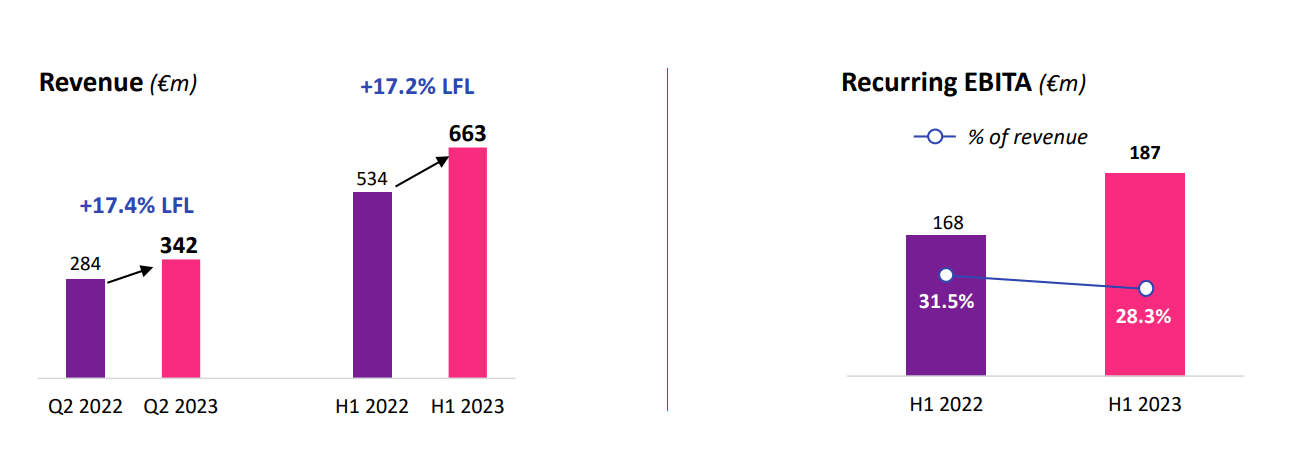

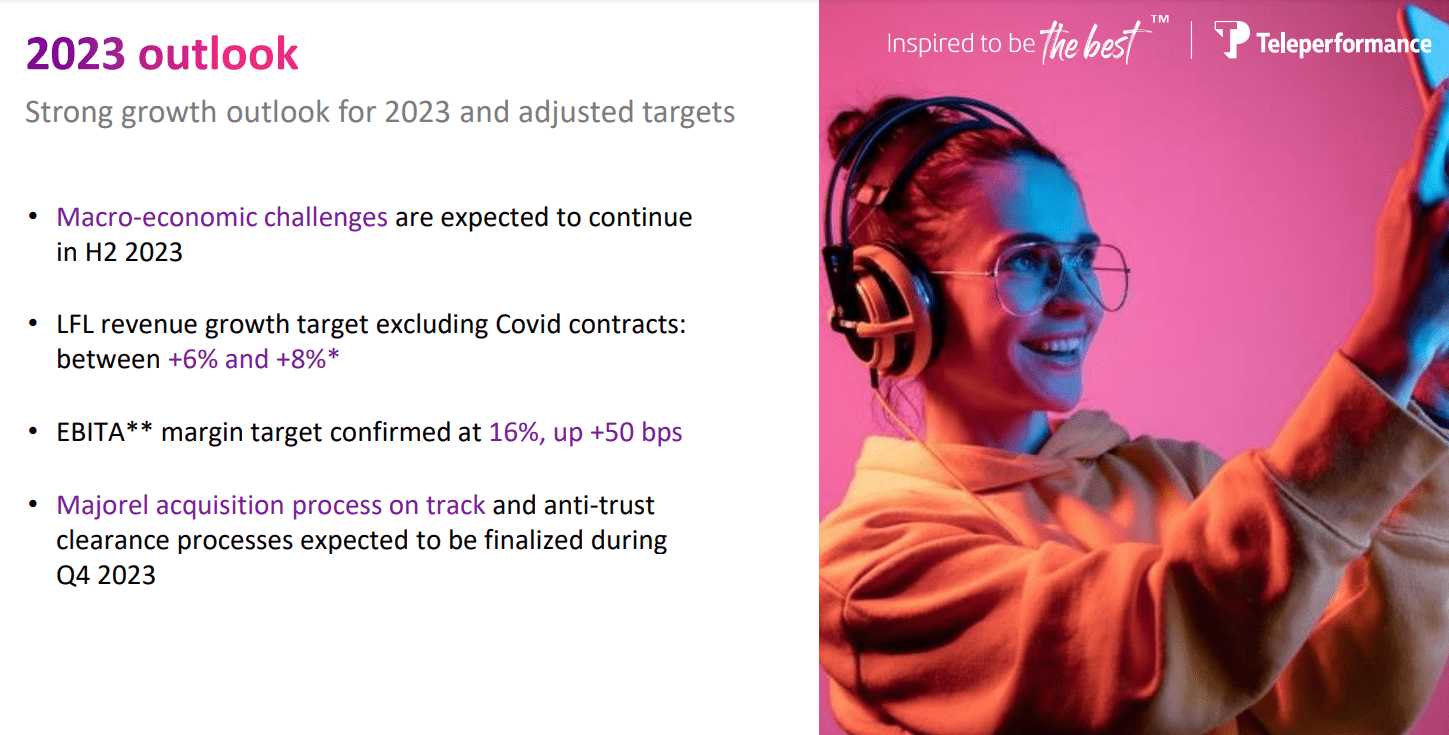

Teleperformance reported solid 2Q23 results less than a month ago.

LFL revenue growth of 7%, EBITDA margins are up 30 bps YoY and are now over 20.3%. The company's portfolio is absolutely stellar, and there is significant, robust business development across all of Europe.

{kind=link}

The company generated a half-year net profit of over a quarter of a billion euros, up to €271M. This is despite a massively negative currency effect due to declines in some emerging market currencies that the company has to work with, such as the Colombian Peso, the Egyptian Pound, and the Argentine Peso, all of these against the Euro. The same trends hounding the SEK are currently seen across the world, and this FX is surely part of the reason for some of the negative trends we're seeing here.

However, fundamentals? That they're at risk?

Don't make me laugh.

{kind=link}

Teleperformance has diversification , and despite what you see on the market in terms of valuation, there was not one significant segment in the company except LATAM which reported negative EBITDA YoY. And that EBITDA drop for LATAM was a measly €3M, which was still less comparatively than the slight revenue decline. LFL growth excluding COVID-19 in Europe was almost 11%, with strong growth in the UK and Germany in key segments.

And when it comes to the growth engines, such as specialized services, well those are up even more.

{kind=link}

The company's operating profitability has taken no sort of significant hit or impact here. The company's operating profit is up 1.8% YoY, to around €450M.

The company also gave us its 2023E guidance, and it's looking for continued growth, with even better margins.

{kind=link}

So, reasons for Teleperformance to actually be lower here? I view them as pretty few, and weak overall - especially once you start to look at valuation.

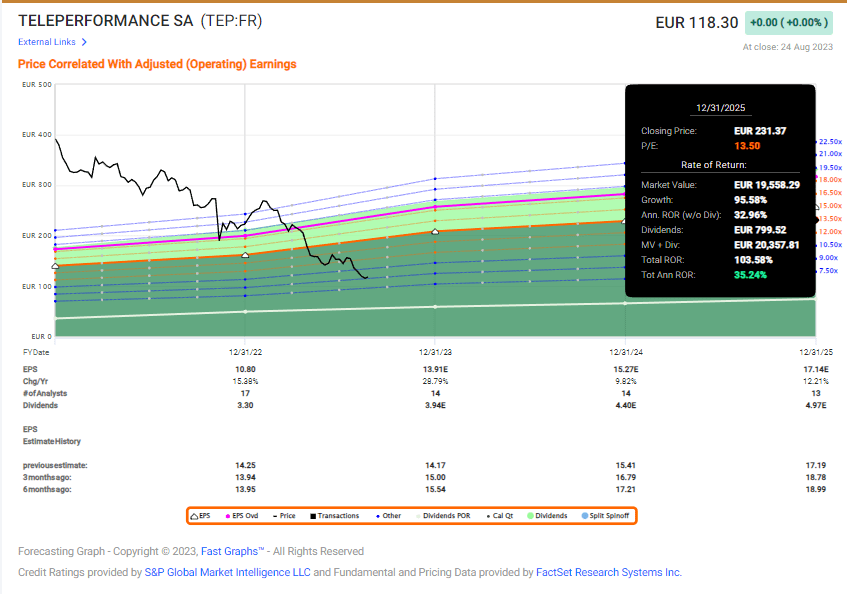

Because Teleperformance is currently trading at around half its overall premium, we can forecast it to be as low as 13.5x P/E and still get triple-digit returns.

That's 13.5x P/E for a company with 92%+ forecast accuracy, BBB rating, and a usual premium of 19x+ P/E with a 3.2% yield.

{kind=link}

That's where the conservative upside starts , as I see it. And it goes all the way up to 15-17x P/E, given that the company is set to grow on average 13.6% for 2023, 2024, and 2025. If the 15x P/E holds or sees reversal, that's 125% RoR or 41% per year.

If we look at the company's actual historical premium that's 200% RoR, and that's not even where GDF valuations have this company being justified. That justified upside goes to a P/E of almost 30x.

{kind=link}

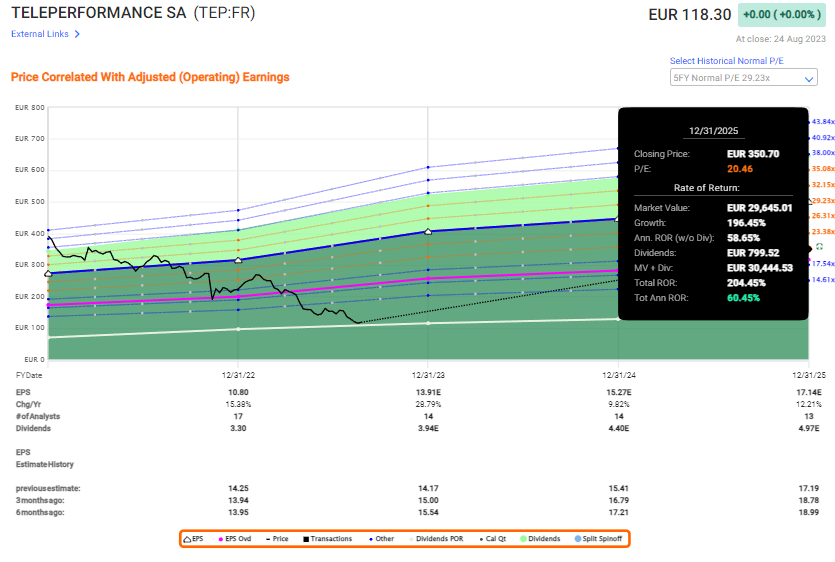

Now, to be clear, I don't consider 30x P/E likely. I also don't want you to think that 30x P/E is going to materialize. It's the sort of overvaluation I don't believe in in the communications sector.

Unless something fundamental changes, 20-25x P/E is where I would start considering rotation or trimming. But if the company reaches that, that means I've almost tripled my money.

And given the amount and percentage I've invested, over 3% of my total private and 4% of my total commercial portfolio, that's a fair bit of RoR at that time.

So, Teleperformance is #1.

2. Alexandria Real Estate ( ARE )

The pick for the second spot in this list is a tough call. Plenty of businesses could qualify for it because there is plenty of quality currently on sale. I've written before about companies like Lincoln National ( LNC ) or Intrum, but in the end, and for this time, I choose to go with Alexandria Real Estate as my second pick here.

Why?

ARE IR (ARE IR)

Alexandria is BBB+ rated, and unlike other Office REITs focuses on a subsection of properties and developments which by many investors are considered to be higher quality overall compared to what else is available.

I also think it incorrect to call Alexandria a traditional Office REIT. They do have offices technically, but these offices are so very different from your typical spaces, that they should be likened more to specialized research, production, or workspaces. Such spaces, used in things like pharma and healthcare, have different demands than a standard brick office building , and this means that the volume/availability is lower, and the rent terms are usually far longer.

As we see with Alexandria.

While Alexandria has seen a bit of recovery from trough levels - I bought some shares as low as $110/share - we're still at levels where the company is very attractive, yielding well over 4.2% with a BBB+ upside. But that's not the only reason I'm investing here.

No, as the title implies, Alexandria comes at what I consider to be a conservative triple-digit investment upside.

Alexandria Real estate typically trades at around 20-22x P/FFO - this is due to its high-quality assets, its low vacancies, no debt maturities to 2025, very low overall leverage for a REIT (close to 5x), and extremely high rates of fixed debt at very low-interest rates - below 3.7% on average, with terms of over 13 years.

Those are some of the best qualities in the entire space. That's also why Alexandria Real Estate is by far my largest office REIT position, despite it being the lowest-yielding by far. I go for quality above yield, and ARE is simply a higher quality than many of the other REITs I look at.

The historicals are definitely on ARE's side.

ARE IR (ARE IR)

And its portfolio is massively qualitative. Over 90% of the ABR is from IG-rated or above tenants, with an 80%+ retention rate. This speaks a very clear language. The company is a good landlord with quality assets where people want to stay. You might expect leasing activity to be low in 2022 or expected in 2023, but 2022 was the second-highest leasing activity in the company's history - more than twice the 4.4M of 2020 in terms of annual leasing revenues in square footage. Over the past 10 years, ARE has managed 1.3M RSF per quarter, and in 1Q23, that number is still at 2.0M, and for 2Q23, the number was very good as well.

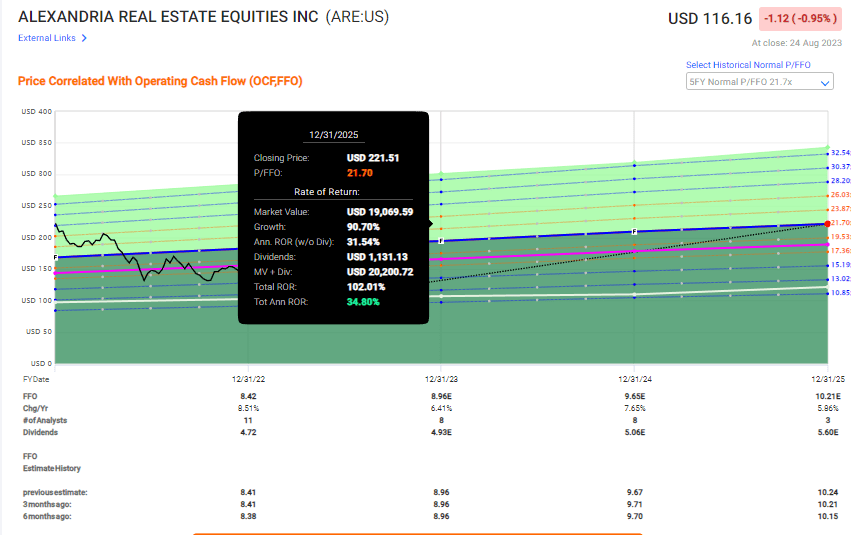

The company is still at a low valuation, despite the fact that I've written about it for a number of months at this point. It currently trades at a P/FFO of 13.25x, compared to a 5-year average of almost 22x. While not as ridiculously cheap as Teleperformance, in context it's still very cheap and worth looking at.

The upside to a reversal P/FFO is where we find the triple-digit RoR potential, and because the company seems very unlikely to underperform its current forecasts.

{kind=link}

Why do I say the company is unlikely to underperform its current forecasts?

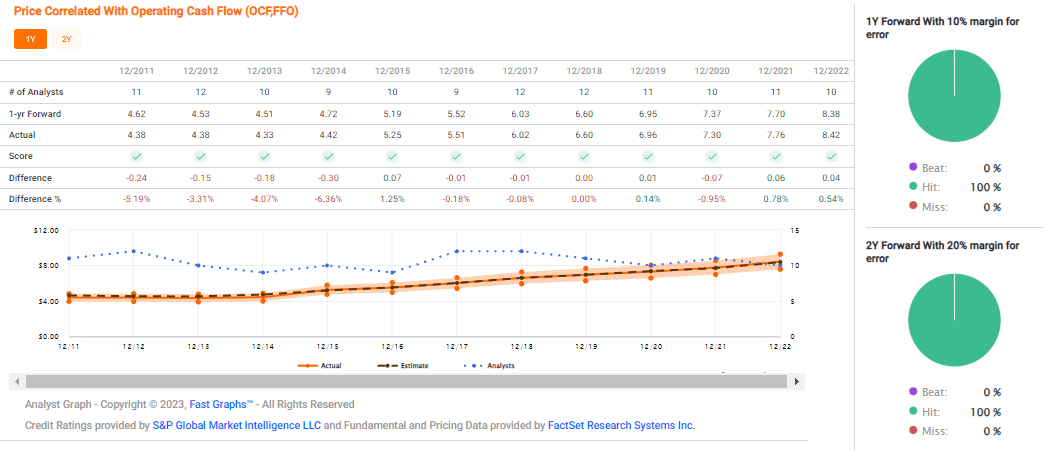

Because this company historically does not miss forecasts - ever - not with a small margin of error.

{kind=link}

So there are risks you can take - and risks you shouldn't really take.

Alexandria definitely comes to the sort of risk that I believe you should be comfortable taking if the company fits your risk and allocation profile. As the company meets my demands, I've invested heavily and pushed capital to work in this company. I intend to continue to allocate to this company over time for the combined upside I see here - meaning quality, dividends, and fundamentals with reversal.

I believe these two companies represent superb investment possibilities for the risk-conscious and valuation-aware investor who's looking for the sort of doubling of capital that I'm looking for.

Wrapping up

These is 2 companies that I consider to have a combination of undervaluation, quality, upside appeal, and likely growth to make them some of my strongest "BUYs" here.

They are far from the entirety of my "BUYs" at this time, but they are companies that I myself have been adding to over the past 2 weeks, and have frequently bought shares in as they have dropped/declined.

So when someone is asking me what he/she should be buying - I would say to take a look at these three companies and see if any of them meet your requirements or pique your interest.

Because if you're anything resembling a valuation-conscious investor, then they should at the very least interest you.

For further details see:

Teleperformance And Alexandria Real Estate: 2 Companies With Potential Triple-Digit Upside