TLPFF - Teleperformance: Don't Underestimate The Negative Qualitative Aspects

2023-10-28 06:50:26 ET

Summary

- The stock is rated as a hold due to factors beyond the numbers that may compromise the sustainability of the business model.

- Looking at the company's metrics, Teleperformance seems to have solid competitive advantages and a strong market position.

- The stock price decline may be influenced by concerns about AI disruption and the acquisition of Majorel, but potential issues with working conditions might be the most important factor.

We rate the stock as a hold as there are some factors beyond the numbers that might compromise the sustainability of its business model for the long term. Some investors are focusing only on the numbers but overlooking entirely subtle qualitative aspects that are causing the stock price to remain low, creating uncertainty. The fall of the stock price started even before the reduction of the guidance from around 9% to 7% for 2023. One of the first things to explore in a company before considering investing in it is the qualitative aspects, so we will explore these factors to understand how they are affecting the stock price and how they might create uncertainty about the long-term sustainability of the business model.

Business model

Teleperformance ( TLPFF ) is divided into two different business lines : i) core services and digital integrated business services ((DIBS)); and ii) specialized services. These services offered by TP are outsourcing services hired by multinationals and small and medium-sized companies that enable them to focus on their core businesses.

Exploring a little bit further each segment, the core services and DIBS include customer relationship operations, technical assistance and customer acquisitions, management processes, back office, and digital platform services. These services are recognized as a function of time spent by phone, chat, or email, of volumes processed, such as the number of calls or sales made, or even of personnel allocated to the engagement.

TP tracks these services through internal and external tools, as certain contracts reward or punish with penalties based on achieving or missing contractual ratios related to operations. We will come back to this interesting topic later.

Related to the second business line, the specialized services include interpreting, visa application management services, debt collection, and process management services in the healthcare sector or for government departments that provide services to citizens. Revenues in interpreting are recognized based on the work done; revenues associated with visa application management are recognized based on the number of application processes.

Those revenues related to Health Advocate are collected monthly based on subscriptions, while those revenues associated with recruitment and related services are billed monthly based on the number of employees allocated to each engagement.

{kind=link}

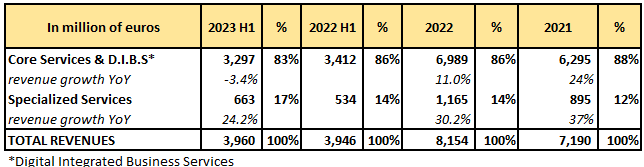

In the table above, I can see the revenue breakdown and how important each business segment is for TP. We may see how the segment Core Services & DIBS represents more than 80% of the total revenues and how its revenue growth is decelerating.

Author, Annual Report

With respect to the margins, we may see that the specialized services are the business segment that contributes the most to the bottom line, but it only represents 17% of total revenues according to the first half results of 2023, so that contribution is diluted; furthermore, the margins in both business lines have been declining since 2021, which is a result of the lower demand for those services as the macro headwinds are influencing the client's decisions to spend less on these services.

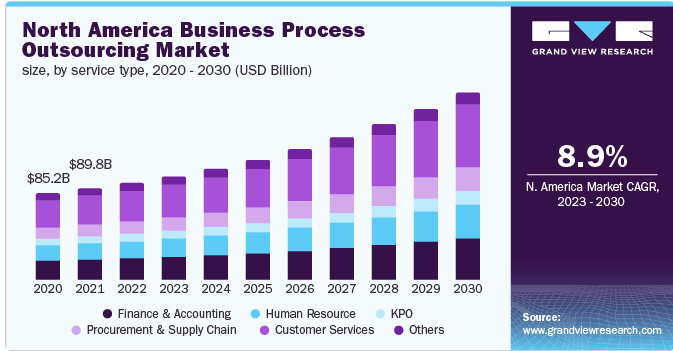

Of course, once the economy shows some positive signs, companies might recover confidence in their businesses and demand more of these kinds of services, as business process outsourcing has good long-term growth prospects, as shown in the following chart:

{kind=link}

In addition, TP has a presence in more than 90 countries, surpassing any other player in the industry, while showing a client retention rate of 95% , reflecting an average client relationship with TP of 13 years. Also, TP's portfolio of clients is well diversified through different sectors such as healthcare, financial services, retail, and e-commerce, among others.

{kind=link}

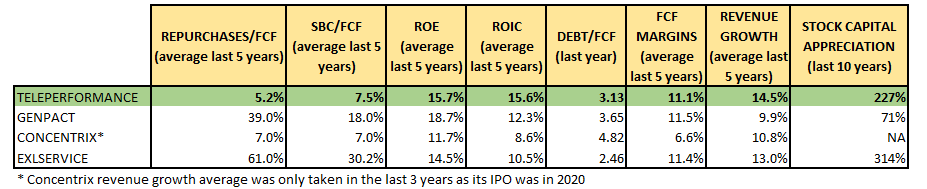

In the table above, we can see how TP delivers good returns on capital, adequate financial leverage, good free cash flow margins, and good revenue growth, even compared to some players in its industry.

So, we are talking about a resilient business model and, apparently, a very interesting opportunity; however, we need to examine deeply which are the factors that are impacting the stock price right now to understand what are the risks that we are assuming with this company.

From all the factors pushing down the stock price, only one might make sense

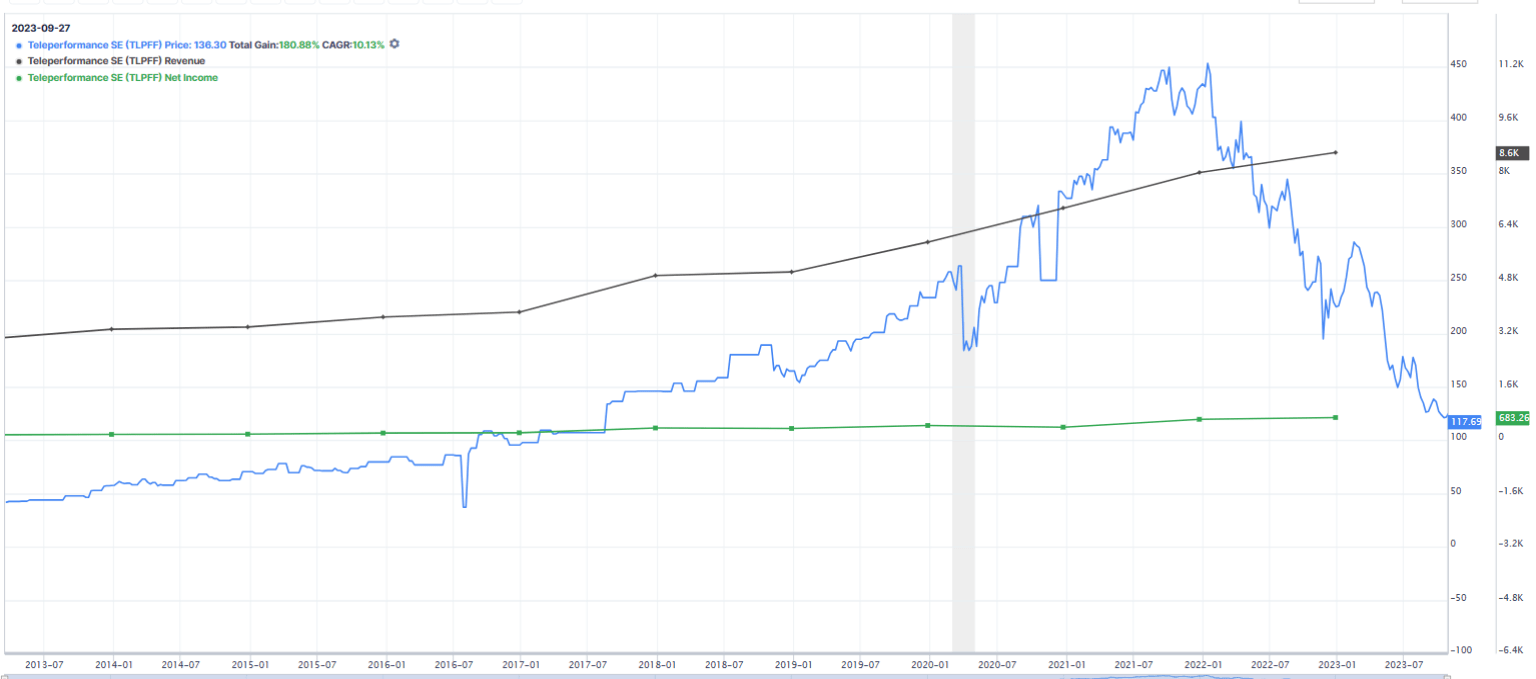

In the next chart, we may see the evolution of the stock price in the last 10 years, and it's clear that there is no justification for a 74% drop from its peak in 2021. The company is still growing, though showing signs of deceleration.

{kind=link}

The first factor that might be causing uncertainty is the possibility that AI ends up disrupting TP's business model. In 2023, the company said that in the next 3 years, between 20 and 30% of the volumes could be handled by AI, and apparently that was information that was taken as a bad sign. Nevertheless, this factor is ill-founded, as to disrupt a business model like that of TP, any disruptor would need to collect data on many interactions.

Here, TP is the company with the highest presence worldwide to take advantage of AI given its huge data related to different interactions. Taking advantage of this data, TP has been working in generative AI for the last few years. For instance, 72% of TP's 200 clients have at least one of TP's top five products embedded with AI; the most common is CX automation.

On the other hand, TP already has projects with GPT similar to the type of ChatGPT in Europe and Latin America. Therefore, TP has the advantage of holding the data to disrupt its own business model in the long term to benefit itself. It is very unlikely that any other company could disrupt TP's business model, as it does not store all the data necessary to do so.

We consider that AI is not a key factor behind the pessimism of the market related to the stock. Another factor that might be affecting the stock price is the acquisition of Majorel. We think that Majorel is a good acquisition, as it will enable TP to expand its markets and reinforce its market position. TP has agreed to pay 3 billion euros for a company whose revenues were 2.1 billion euros in 2022, so TP is paying 1.4 times sales, which is a very good price where we see lots of acquisitions above 20 times sales in other companies.

Probably, you might be thinking of the way to pay for that acquisition; let's explore it. The transaction is made through cash and shares, but TP has set a limit on the number of shares issued. Indeed, a maximum of 4,608,295 shares are available for issue in Majorel's transaction. In August 2023, TP launches a share buyback program of 500 million euros, which will enable it to pick up most of the new shares issued in the transaction. If TP repurchases at a price of 114 euros, it would pick up 4,385,965 shares from the market; if TP repurchases at a price lower than 114 euros, it would pick up even more shares from the market. Thus, the dilution is not a relevant factor impacting the stock right now.

The reduction of the guidance from around 9% to 7% might be a good explanation, but even with that reduction, it's hard to explain a 74% decline in the stock price since 2021. We know that the interest rate hikes caused many stocks, particularly those named "growth stocks," to be affected the most since 2021; however, there is a pessimism with respect to this company that is beyond the guidance of AI or the recent acquisition of Majorel.

The working conditions might be the factor behind the pessimism

This factor is well overlooked, not only by many analysts but also by European fund managers. In the call for 2022's results, CEO Daniel Yulien said the following:

I'm not going to make use a gift not to come back on the unfair, unsubstantiated, crazy storm in a glass of water politic that has been started and amplified in some places. We got a negative noise in media, social media in late '22 with regard to our content moderation practice. And the working conditions at Teleperformance in Colombia.

There was two articles in three months from two different -- one from a journal, one from another one, and one tweet from a Vice Minister of Labor.

Then when I was in a roadshow in the U.S. at three in the morning, somebody called me and told me, Daniel, wake up. It is a disaster, there is a massive fail of and the stock is down 38%, November 10, Black Thursday. If an atomic bomb comes on the European city in the future, we will be more prepared to that than ours to listen to this hallucinating story.

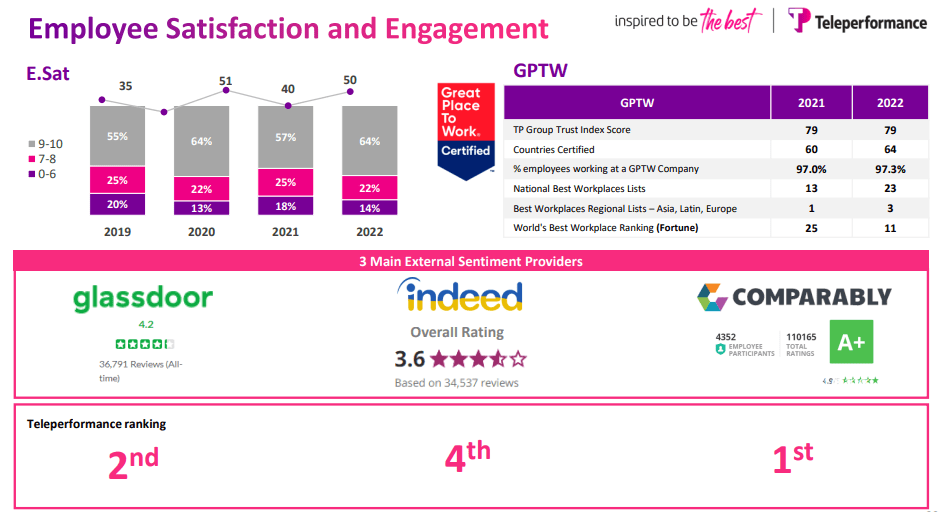

The CEO does not acknowledge that there is a problem related to the working conditions, as he backs up his assertions that those allegations are unsubstantiated, mentioning the TP's achievement of being among the World’s 25 Best Workplaces (ranked 11th out of over 10,000 companies) in the list drawn up by Fortune magazine in partnership with Great Place to Work (GPTW).

The company has taken other steps, such as independent assurance from Bureau Veritas ((BV)) in February 2023 regarding the use and inclusion of Standard ISO 26000 guidelines in six countries: Greece, India, Indonesia, Malaysia, Portugal, and the United States, where the country has substantial trust and safety operations. Colombia also received a similar assurance from BV.

{kind=link}

However, even with all the aforementioned steps taken by the company, there are certain things that are not clear; for instance, we explored the website for job searching, Indeed, mentioned in the chart above, to know more about the employee's opinion about the company; according to the chart above in Indeed, TP has received a rating of 3.6/5 over 39,230 reviews, which is not bad.

If we go to Indeed , we will find these results:

Indeed

This rating assigned by Indeed seems to be good, but if we check out each opinion one by one with a rating of 1 and 2, you will discover that most of those opinions belong to workers that are part of the call center departments, in other words, those who deal directly with the daily interactions.

Thus, that rating of 3.5 is biased as most of the good opinions come from employees with upper positions within the company being the majority who made a review in Indeed, whereas employees who are part of the call centers represent a minority in these reviews but are the great majority in number within TP. These complaints not only come from employees in Colombia but also from other countries and were made on Indeed very recently—lots of them were made in October 2023.

We've found one experience through an article written in 2021, just to picture the situation. The article was written on Voragine News , a website about local news in Colombia. In the article, it's mentioned that the maximum time given for employees in a workday is only two breaks of 17 minutes each, while each employee has a clock on his computer counting the time. One employee said that in just 3 days, 60 employees out of 142 who started working at TP decided to quit as they felt pressure was hard to handle.

As investors, we find that something is not right here, as we notice that the CEO just denies these bad experiences, saying that TP's good working conditions are supported by GPTW ratings and Bureau Veritas; nevertheless, the facts say another completely different story. The information on Indeed is public; anybody can find that information, and we're sure that several fund managers have seen the same information.

We can think of several scenarios, like how TP is managing the surveys for the GPTW or if the high employee turnover might be influencing a different picture from reality. For instance, it might be possible that only the new employees in the call centers received the GPTW's surveys, and they were satisfied in their first weeks in the company, whereas the other ones who worked for a longer time are not receiving that survey as they are quitting.

We are not assuring anything, just contrasting the evidence of what the CEO is saying with the facts. These situations do not give us confidence to hold the stock for the long term, as a CEO who does not acknowledge that the company is carrying a serious problem is dangerous. Something that we would expect is that a CEO recognizes the problem and takes action to solve it.

Qualitative aspects are a priority for a long-term investor

When we assess a stock, we like to explore it fully, understanding its business model through reading about the products and services it offers, the quality of the management, competitive advantages, comparison with competitors, growth prospects, etc. We take all these steps before calculating the intrinsic value; if we find some qualitative aspects that make us feel uncomfortable, we stop the assessment.

Here, we've identified that the CEO is not fully transparent since a problem that is not recognized might grow as a snowball over time, bursting out at some point in the future, and we do not like that. Anyway, we will provide an intrinsic value in case you are not planning to hold this stock for the long term but, maybe, for the middle term, or, at least, for a scenario where the stock recovers its intrinsic value pushed by other market forces or some new actions taken by the management. Of course, all of these aforementioned scenarios are not guaranteed.

Valuation

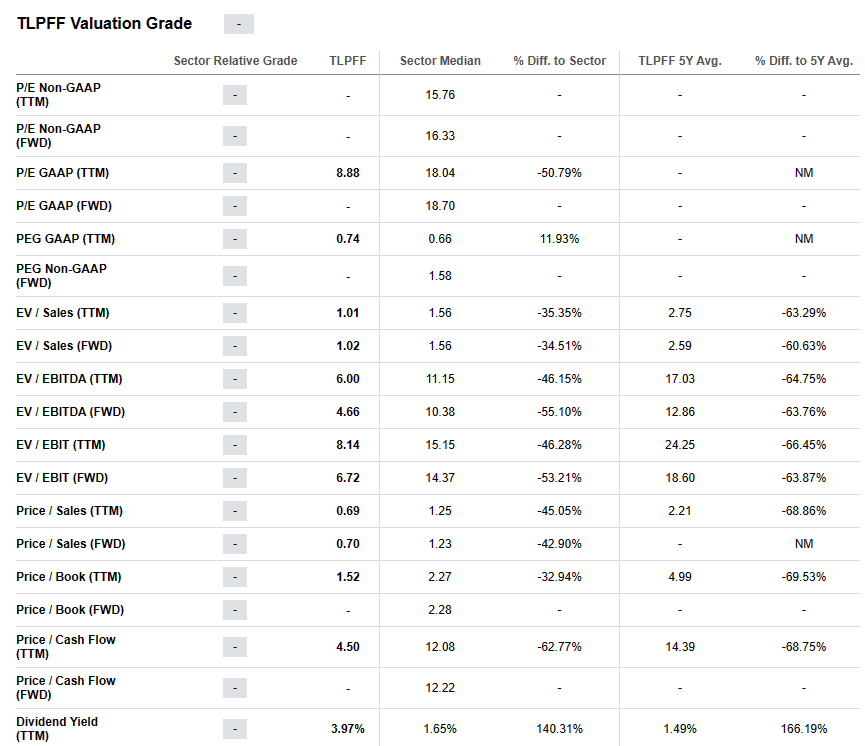

According to SA, TP is cheap in all the valuation ratios compared with those of its peers:

{kind=link}

As usual, we will calculate the intrinsic using our discounted free cash flow model, making certain assumptions:

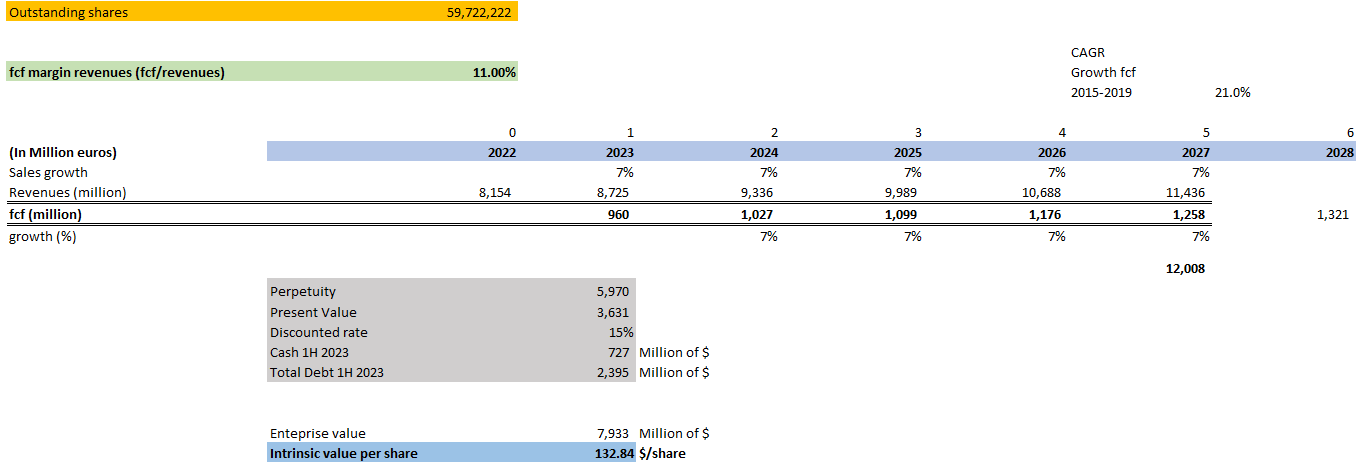

- Outstanding number of shares: 59,722,222 shares

- FCF margins: 11% (average of the last 5 years)

- Revenue growth: 7% (According to the last guidance, we are not considering the acquisition of Majorel to project future revenues.)

- Cash as of July 2023: 727 million euros

- Total debt as of July 2023: 2,395 million euros

- Discounted rate: 15%

- FCF growth perpetuity: 4% annual (21% CAGR from 2015 to 2019 before COVID-19).

{kind=link}

To find the perpetuity, we used the formula:

Perpetuity = FCF 2027/(discounted rate - g)

where g = FCF growth perpetuity, which was assumed to be 4% annual

With perpetuity, we calculate the present value of all the FCFs beyond 2027. Then, we calculate the enterprise value using the following:

Enterprise Value = Present Value of FCF (from 2023 to 2027) + Perpetuity + Cash - Total Debt

Finally, the intrinsic value is calculated by taking the enterprise value and dividing it by the outstanding number of shares. In this way, we could get $132.84 per share under the assumptions presented.

Here, we need to say that we are making very conservative assumptions; for instance, we are not incorporating the growth associated with Majorel's acquisition; we assumed that the growth of FCF perpetuity is only 4% when TP's FCF growth was more than 20% annual in the last 5 years. On the other hand, we are assuming a discounted rate of 15%, which is usually assumed for a Chinese company.

However, as we said previously, we will not buy this stock as the company lacks an important qualitative aspect, such as the quality of the management. In addition, our DCF model assumes that the company will be able to handle problems related to working conditions over the long term while avoiding any future punishment by regulators or governments.

We've seen several analysts and fund managers overlook this important factor. In our view, transparency is an important component of the quality of management, aside from his or her skills to deploy capital or manage the company's resources to deliver value. In this sense, in our assessment, the qualitative aspect always comes first to decide whether to buy or not a certain stock.

Risks

A risk of our thesis is that the market ends up overlooking the qualitative aspects in the long haul and the stock price recovers its peak reached in 2021 at some point in the future. Another risk is that the management identifies that it's important to take important steps to improve the working conditions of its employees in the call centers.

However, there are many fund managers who focus on these kinds of qualitative aspects, and they will not support these policies in a company. On the other hand, it's not that easy for the CEO to recognize this problem of the working conditions right now, as that might compromise the name of GPTW and Veritas, adding to the fact that could add more fuel to the fire, triggering more articles by the press and pushing down even more the stock price.

Final Thoughts

TP is apparently cheap given the huge drop in its stock price since 2021 and given the intrinsic value calculated previously. The company has shown over the years that it enjoys competitive advantages with solid margins, an adequate level of debt, good revenue growth, and operating margins.

Nevertheless, the qualitative aspect of a company is very important for us, as we stop the assessment as soon as we see something that makes us feel uncomfortable. In this particular case, we do not like how the CEO has handled the problem of the bad working conditions, and, apparently, the problem is still unsolved despite the good results from GPTW and Bureau Veritas.

We do not know how those processes were made in detail, but we can see the facts, and it seems that there are important contradictions between what the CEO says based on GPTW and BV and what is seen in Indeed through the different complaints.

On the other hand, according to the TP's annual report, there are contracts with clients that reward or punish with penalties based on achieving or missing contractual ratios related to operations. We do not know how demanding those ratios are that depend on the negotiations between TP and its clients, so to win a new contract, TP might be accepting very demanding ratios to close the deal, which are finally translated to the employees. This, of course, is not a healthy and sustainable practice by the company.

Anyway, we keep our discipline of only focusing on high-quality companies with management offering full transparency, and that's why we do not rate a buy for this stock according to our own investment style. In the last call for the Q2 2023 results, the CEO appeared with a lack of confidence to please TP's investors. It might be related to the problem associated with the working conditions and the way it was handled despite the different steps taken. In this article, we offered evidence that the problem has not been solved yet, and we do not think that it is a temporary setback.

For further details see:

Teleperformance: Don't Underestimate The Negative Qualitative Aspects