TLPFF - Teleperformance: More Concrete Upside From AI I Still Say 'BUY'

2023-06-27 10:22:34 ET

Summary

- Teleperformance, a leading call center company, is expected to deliver significant outperformance in the next 3-5 years with potential returns of 200-300%.

- The company's recent acquisition of Majorel is expected to bring synergies and scale to its operations, with a revenue target of €10B before 2025.

- Despite macro-level challenges, Teleperformance continues to report robust growth and is considered undervalued and underappreciated in the market.

My Dear readers/followers,

I've been beating the drum on and off for Teleperformance (TLPFF) on almost a monthly basis at this time since I started buying it back in March/April of 2023. The company is what I believe to be a massive 3-5 year outperformer - by which I mean that I believe you could potentially make returns of 200-300% in the right circumstances.

It will take time. The company has fallen from grace - by which I mean it's fallen very far from its heights, at which point the price would have made me overlook it within a few minutes.

But now, the company is in a very attractive overall position. I believe that the outperformance we're likely to see here is significant - and I'll show you why here, how come the company may deliver over 65% returns per year, and why my bearish case is triple digits for this investment.

Teleperformance and its massive upside

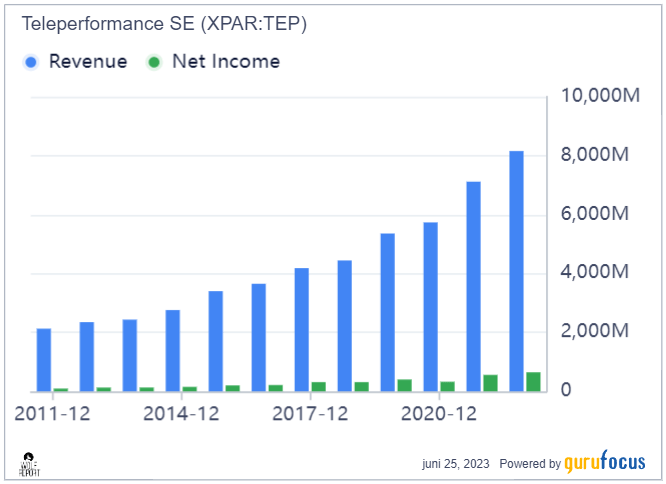

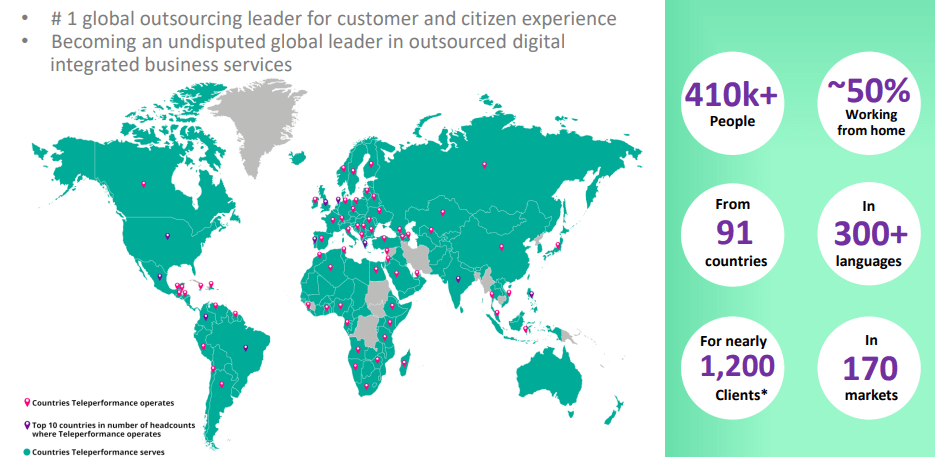

Teleperformance is one of the largest call center companies on earth. It has proven, over a substantial time period, that given time it can generate revenues and an unbroken line of profit/net revenue for over a decade.

Teleperformance revenue/net (GuruFocus)

{kind=link}

Typically a trend like this should mean that we have a very solid valuation, earnings, and profitability line over a long timeframe - and indeed we do, with the exception of 2020, which due to COVID-19 and other factors saw the company's earnings decline - at least for a year before bouncing back up massively.

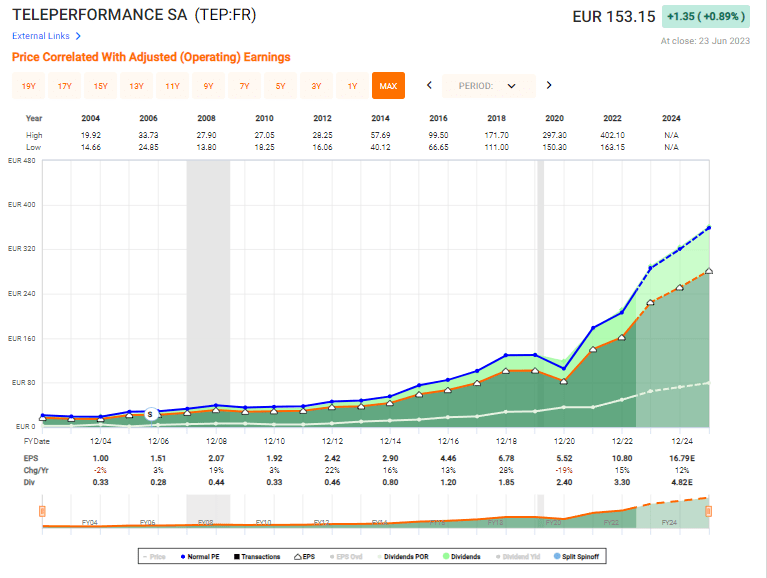

Teleperformance Earnings (F.A.S.T graphs)

{kind=link}

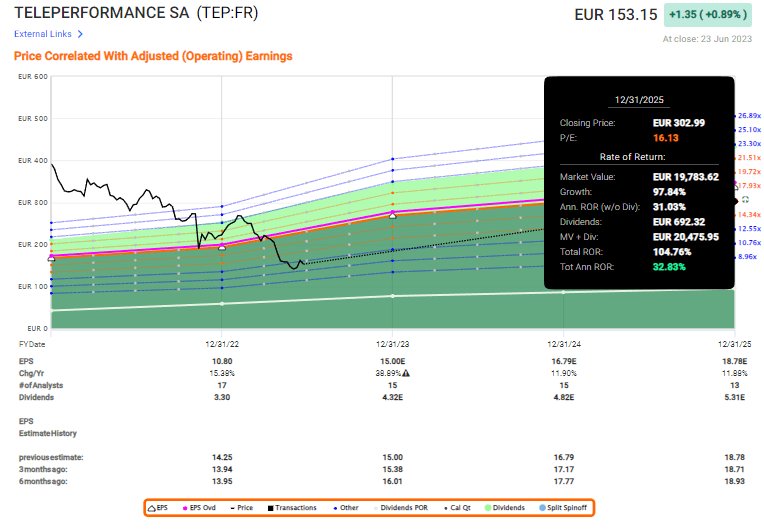

It is not the company's "fault" that the market decided to first undervalue it until 2014, before going on a massive premiumization spree that culminated in a share price of closing on €400 for the native per share , before dropping back down to a meager €153 /share today. The company's earnings and/or growth rate never dictated that this should happen. The overvaluation to over 40x P/E was an anomaly that, as a valuation investor, I say never should have happened. If I had held the stock at the time - I definitely would have sold it well before that €400/share, probably around €290-€300/share given the trends in earnings we saw at the time, maybe even before.

However, the charm we find in these sorts of investments is that we can take advantage of such mistakes and trends. The crash has left the company in a stumble, and the current €153/share price represents a significant discount to any forecast if looking at any peer on any market today.

The company is clearly in the upper percentiles in terms of profitability. If we look at call center operators specifically, the comparison looks even better. No one part of the company's business model or profitability stands out as "negative" or too expensive. COGS and OpEx are attractively tiered, and managing a nearly 8% net margin in this business is cause for compliments in my book.

The company gave us 1Q23 in late April of 2023. There were no signs of any sort of deterioration, significant pressures, or issues worth noting in that specific report. Excluding the temporary covid-19 contracts, Teleperformance managed 8.6% LFL YoY growth, with a sustained growth outlook for 2023 even when including the COVID-19 impacts. The company revised the forecast, with no impact on TEP value creation.

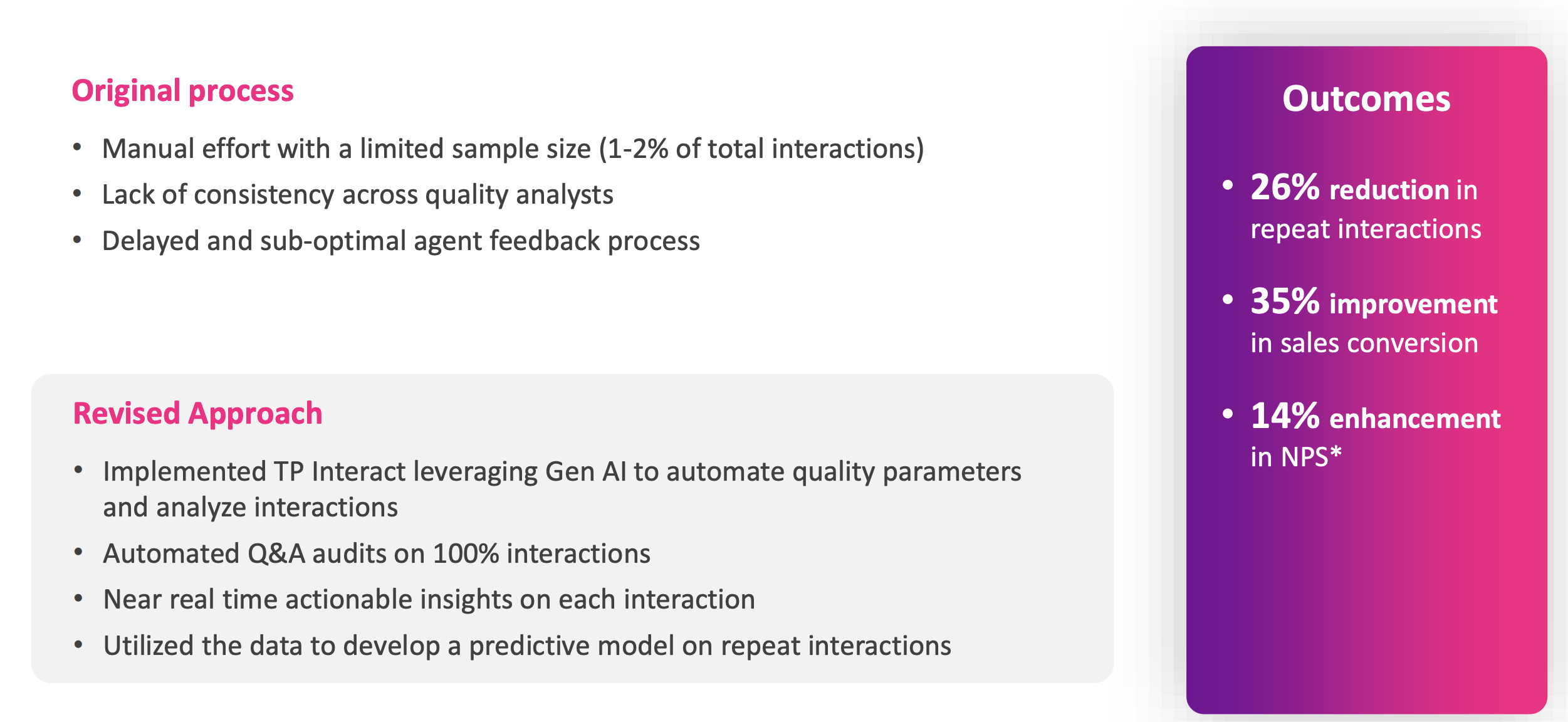

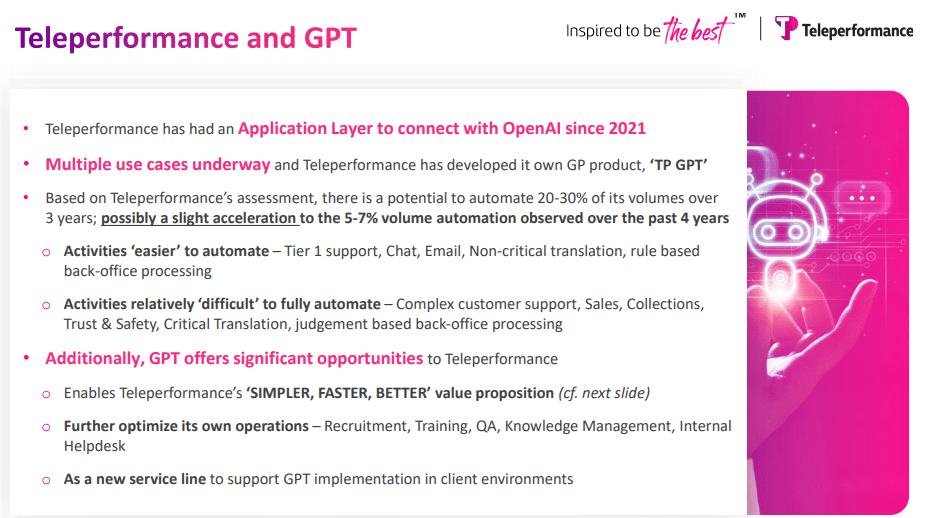

What instead warrants a thesis update here is the company's increased appeal in terms of AI, which the company reported only a few days ago. The company's ambition here is, through its new "GenAI" taskforce, to implement the use of GenAI products into client operations, and work it into the entire value chain within the company. We're talking recruitment, training, client management and operations. So far the adoption by everyone has been slow, including Tech Majors, but TEP expects this to change with results from relevant cases - such as the one below.

{kind=link}

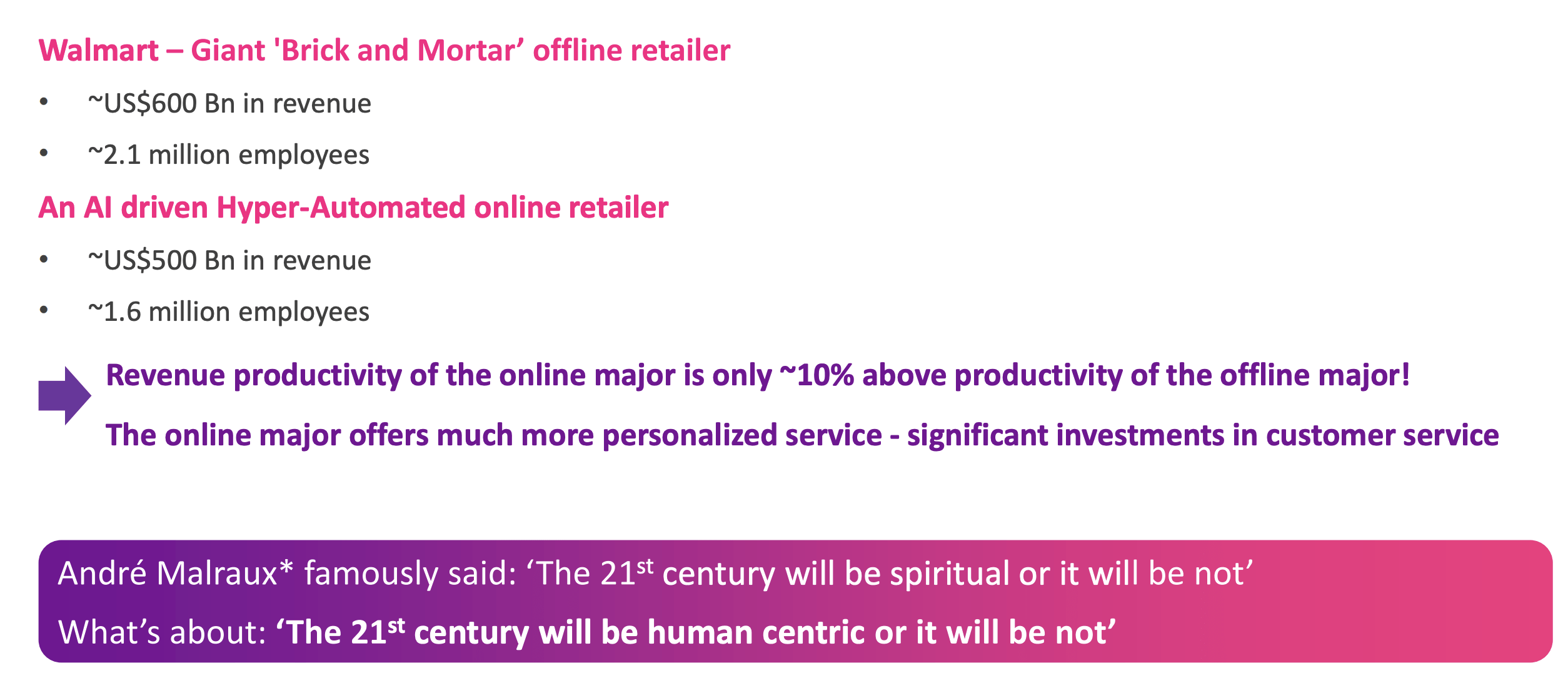

There are other case studies as well, showing significant reductions in handling time for Automotive majors as well as double-digit increases in customer satisfaction ratings. This speaks for the use of AI in many fields where TEP is active. Up until now, we've mostly had a more general description of what the company means to do here - but now we have concrete and relevant case studies where companies can see actual data-driven improvements in relevant metrics specific to TEP. Even in real estate, there was a case study showing a near-double-digit decrease in handling time.

The company's key takeaways here, presented a week ago, is the need for robust security at every layer, close supervision from humans along the chain, and process knowledge and systems to design the right solutions. TEP is a company the size enough to manage this, being one of the largest companies in the field here.

For those interested in more concrete examples, the company recently published a presentation that includes "call examples" where these technologies are used. These can be found here.

{kind=link}

In short, the appeal from AI is one of the latest reasons why I consider TEP to be an even stronger "BUY" than before.

In one quarter alone, TEP generated over €2B worth of top-line sales, and these sales came with growth from nearly all segments. Strong momentum in core services, with customers both in social media, travel, fintech/financial and government agencies - it all grew. The company continues to expand its offshore activities serving NA. This had a slightly negative top-line impact, but given the lower margins the company was able to squeeze out due to lower costs, the net effect was still a positive one.

The quarter saw the first positives of China reopening, with new contracts.

TEP now expects full-year revenue growth of 8-10% for the full year - that's excluding COVID-19, with an EBITDA margin target of 16% for the year, up 30 bps.

Teleperformance IR (Teleperformance IR)

The company recently made a massive M&A that had significant share price effects due to the purchase price. The purchase of Majorel brought a €30/share price consideration for a total of €3B - incidentally almost the amount the company's share price fell the day that deal became public. The addition of Majorel will significantly add synergies and scale to TEP operations by:

- Complementary capabilities in already existing as well as new/expanded geographies, with TEP's NA strength complemented by Majorel's European coverage.

- Scaling up Asia/Africa.

- Deepening expertise in several fields - Tech, Banking, Insurance, Travel, Energy, utilities, Retail, FMCG, government, and automotive verticals. Plenty of sub-sectors are likely to see an upside here.

- Leaner and better management/operating structure

This transaction brings with it a proforma 2022 EPS accretion in the first year before synergies, and double-digit EPS accretion, including run-rate cost synergies, after that. We can expect a significant upside from this transaction in the longer term, around €100-€150 in efficiencies, scale, and product development alone. The company hasn't incurred any negative rating change, due to a proforma leverage of 1.8x to 2023E EBITDA, which means the company is even after Majorel, free to move on other M&A.

The company objective is to reach a €10B revenue target before 2025E - and thanks to Majorel, the company now believes this to be possible as early as 2 years before, in 2023E.

{kind=link}

Teleperformance is an undercovered, undervalued, and underappreciated company. Despite a multitude of macro-level challenges and recessionary worries, both the top and the bottom line continue working as expected, reporting robust growth. The company already has the sort of international scale and appeal that I typically look for in a deep/large investment.

{kind=link}

What we as investors want to make sure of at this juncture is that the company has the ability to deliver continued growth and not see any material decline or issues in the near term. As long as this is the case, I can remain at a high conviction that this investment will generate near-term outperformance - even if it continues to trend negatively for a while forward.

As you know, certain companies can trade negatively and in direct opposition to their expected growth for a long time. But eventually, things do normalize and the market realizes the company's potential. Teleperformance has already been through this process once or twice in the last 20 years - so it wouldn't surprise me in the least that the company does so again.

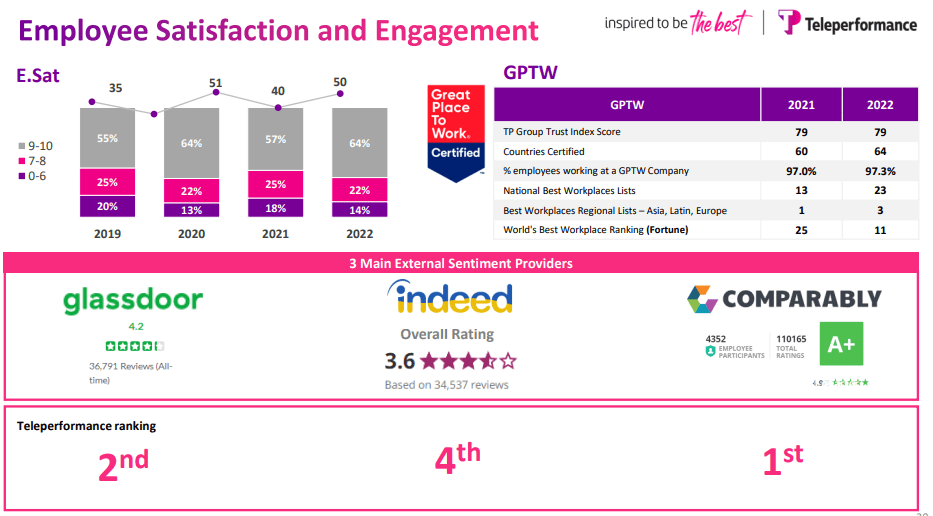

This company is run by a capable management team with an international profile and decades of company and sector experience. It's also one of the better places to work that you can find in the sector.

{kind=link}

Combine this with excellent profitability, and you'll find arguments and reasons as to why I consider the lawsuit claims and legal issues that are currently weighing things down are little more than temporary noise.

Risks, aside from these lawsuits which are related to how content moderation services leading to Core/Digital services growth were achieved by engaging in potentially inappropriate or criminal activities, are instead relegated to continued underperformance as a result of sentiment. I would say that another risk is that growth might not be as high as the company expects - and this is of course a risk - but the fact is the company very clearly stated its growth estimates, and these are close to 8-9% given current sentiment and levels of offshorization. Global clients are asking companies like TEP to provide them with these services - which means that we could instead view a risk for the company that such offshorization and regulatory environments in nations that are target for such moves can be complex to navigate. The company, as a result of this, also increased its margin guidance.

I can also mention as a risk, or a consideration at least, that the company does not do (often at least) share buybacks. They recently stated that despite the low level, this is not the company's policy, and the low valuation has not changed this.

Another risk is therefore that the tepid trend may continue for some time to come - because despite outperformance and positives, it has not meant a clear catalyst for the company moving higher.

I give you my updated/reiterated valuation thesis for Teleperformance.

Teleperformance - A lot to like, upside between 100-300% in the next 3-4 years.

My objective in this article is to give you a good reason to understand my target for the company as well as my rating, which is a solid "BUY". You may recall that my conservative PT is €275/share. I'm not changing this target even a cent for this article. If anything, I would consider increasing it - and once the lawsuits are dealt with, I very well may.

The reason why I am so convinced Teleperformance will outperform is simple - growth and valuation.

Growth comes in the form of EPS expansion. The addition of Majorel and the company's own growth is estimated to add anywhere from between 20-40% to the 2023E EPS number for the company - which will also likely serve to increase the dividend to at least €4/share, which implies a yield of almost 2.7% here.

Beyond that, the growth for the years after is still likely to be double digits as synergies and run-rate efficiencies are added to the bottom line - with potentially more transactions on the way. Based on this, the growth estimate isn't even all that bullish here - it's average. There's a possibility for lower, high-single-digit growth, but that's really all I see in my sensitivity analyses. If you believe the company could go negative, I'd need a scenario spelled out for that - because I don't consider it remotely realistic.

As of now, the 3-year annualized average growth estimate in EPS is almost 18% for this company. Based on an average 2022-2023 estimate, the company now trades at a blended P/E of below 12x, compared to over 40x a few years back. The upside to a 16-17x P/E, which should be the least we expect brings with it a valuation -related upside of triple digits.

{kind=link}

What you see there is the bearish case. That's really as conservative as I can possibly make it because it doesn't even take into consideration that 10 years of history puts TEP at an average premium of above 24x. If you allow that 10-year premium to play a role and act as a reversal, you could get a RoR of 200% there, with an annualized average of 54.65% on the basis of a 23.95x 2025E P/E.

Analyst accuracy to that?

Over 90% or beating estimates . Most of the misses in that is from the past few years as well when the analysts failed to forecast the slight drop-off of 2020.

Simply put both the valuation and growth portions of the thesis make for a very attractive prospect here. The peers that exist don't come close to offering the same sort of scale, looking at market cap or earnings (Source: GuruFocus). Peers include companies like Telus ( TU ), Concentrix ( CNXC ), Atento ( ATTO ), Sykes, TTEC ( TTEC ), and Webhelp, but I'd still prefer Teleperformance.

Other analysts mostly agree with my assessment - though they go further in their targets. 15 analysts cover the company, coming in at a target range with a €220/share low range target and €380/share high range. That's an average of €301, with 12 out of 13 analysts at a "HOLD", 1 at "no opinion" and no one at a "SELL".

I add my voice to this chorus here - though I stick to my conservative average of €275/share for the time being, curious to see the legal distractions play out - though I do see them as nothing more than that - distractions.

My thesis for Teleperformance is the following.

Thesis

- Teleperformance is a superb company in the call center and general business service outsourcing field. I consider the company to be one of the finest around, and due to a combination of fundamental strength and excellent upside, to be a "buy" here.

- I've been buying shares throughout April and May as well as June, and continue to add to my position here.

- The recent appeal includes the company's presentation and focuses on AI, which comes with multiple clear use cases which give us an indication of the future potential of where the company might go.

- The "buy" is stated based on a conservative target share price of €275/share - and by giving it that target, I'm 10-20% lower than the average analyst, due to my always discounting conservatively. However, I believe this company has the very real potential to outperform.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

Because the company fulfills every single criteria I have, this one is one of my strongest "BUYs" at this particular time.

For further details see:

Teleperformance: More Concrete Upside From AI, I Still Say 'BUY'