TLPFF - Teleperformance SE: Quality Compounder At A Compelling Valuation

2023-06-26 09:44:30 ET

Summary

- Teleperformance, a leading business services company, has experienced a significant multiple contraction due to content moderation controversies, disappointing Q1 results, and AI risks.

- We do a deep dive into the situation, analyze differing viewpoints on key issues and drivers, and assess the potential implications for investors.

- We recommend building a long position in Teleperformance shares, stressing the compelling valuation and the quality of earnings.

Editor's note: Seeking Alpha is proud to welcome Salix Research as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

We present a long thesis on Teleperformance ( TLPFF , TLPFY ) in light of recent events which have led to a severe derating of the company's valuation multiples. We believe this is an excellent opportunity to accumulate shares of a European quality compounder at a discount.

Teleperformance SE

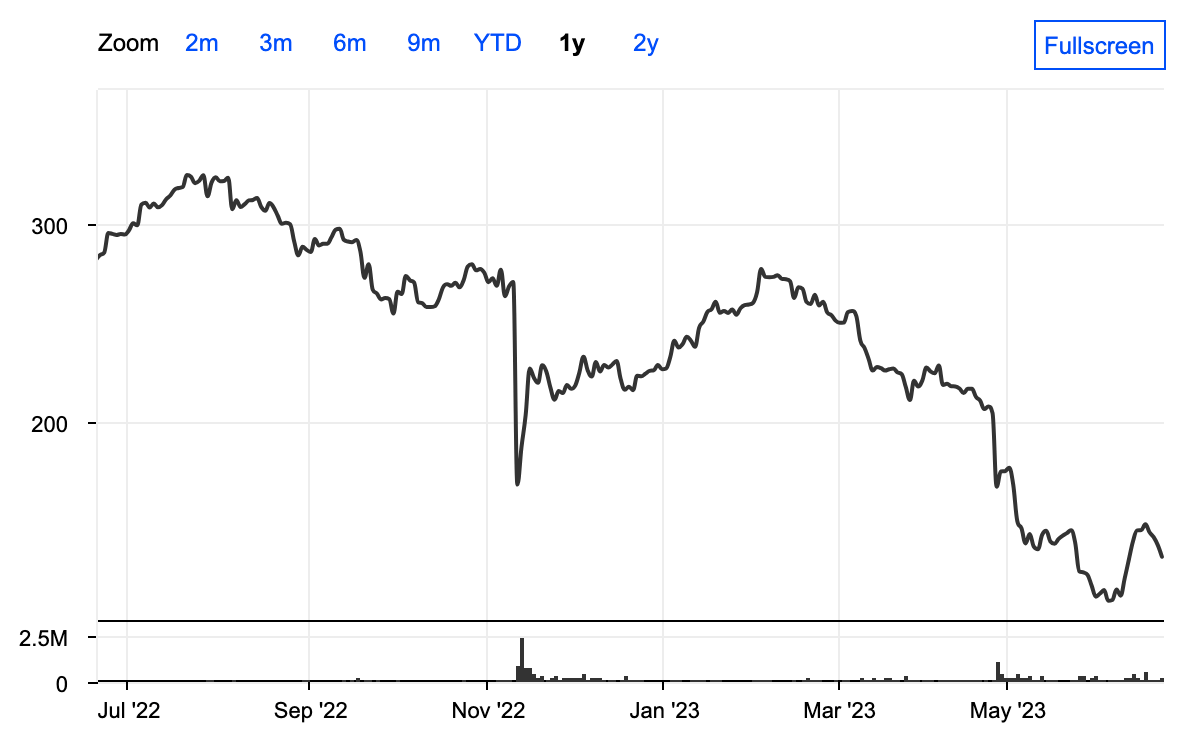

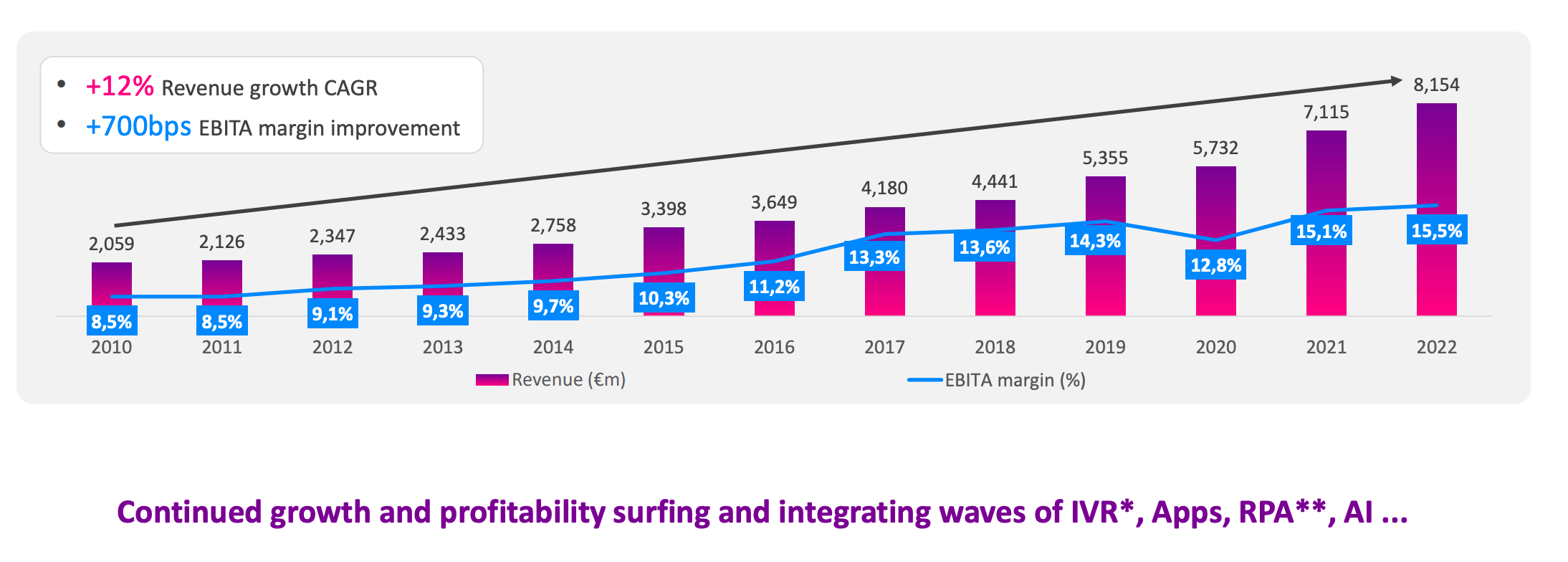

Deemed as one of the best business services companies globally, Teleperformance has been one of the top European compounders of the last two decades, with a strong track record of low double-digit organic growth, margin expansion, e.g., +500 bps between 2015 and 2022, sector-leading margins, and high incremental returns on capital. Over the last years, the business mix has been moving toward higher value-added, higher growth digital solutions, and underlying offshoring trends have provided strong tailwinds for the company. However, for almost a year, Teleperformance seems to have joined the realm of fallen angels, with the stock halving since June 2022, to €151/share, experiencing a severe multiple contraction to circa 10x forward PE (based on an average of a sample of analyst estimates for 2024). We will explore the reasons, analyze differing viewpoints on key issues and drivers, and assess the potential implications for investors.

Is Teleperformance an oversold name that represents an outstanding GARP (Growth at a Reasonable Price) opportunity that could lead to outsized returns? Or has the business deteriorated, and the company merely lost its shine?

{kind=link}

Source: MarketScreener

Content Moderation Troubles

In early August 2022, Forbes published a damning article on Teleperformance's US Trust & Safety division that provides content moderation services to TikTok among other social networks alleging employees were exposed to extremely egregious content including CSAM , and suffered immense psychological trauma as a result. A series of unfavorable articles and testimonials followed suit, and the valuation suffered, culminating in an investigation from the Colombian Ministry of Labour. The company was remarkably proactive in addressing the issues, holding multiple investor and analyst calls with a wide array of managers and specialists; site visits in 6 countries, and conducting multiple internal and external audits including one by Bureau Veritas to calm investor sentiment. Although audits cleared the company of any fault, valuation pressure from the markets remained intense and management decided to exit highly egregious content moderation.

Content moderation was seen for years as one of the most promising segments given the exponential rise in content generation and the subsequent need for "policing" the internet. Exiting only one part of the content moderation business proved to be impossible, given the lack of adequate processes in place, and could potentially lead to significant market share losses in the rest of the Trust & Safety business hence in March this year the company reversed the decision. We believe content moderation is an intricate and challenging business, often leading to bad press and public relations mishaps, however, it is an essential service to the public much like the police, firefighters, doctors, etc. Providing an essential service should in our belief be rewarded rather than punished from an ESG and public relations perspective.

While it's important to pay attention to the points raised by a minority of content moderators, we believe Teleperformance has done a great job explaining the merits of the business and has properly assured the markets on employee treatment policies, providing robust data backed by trusted third parties. Hence any overhang related to content moderation should be considered resolved. In this context, we believe future instances of negative news flow around content moderation should have a much smaller effect on the stock price. Detailed presentations are available to the public on the company's investor relations page.

{kind=link}

Disappointing Q1 And Lower Revenue Guidance

Teleperformance disappointed investors during the Q1 update , as it downgraded organic growth estimates for 2023 by 1% to 9% at midpoint. We would like to emphasize that EBITA margin estimates for the year have been upgraded by 30 bps, however, leaving the bottom line estimated for the year largely unchanged. The downgrade can be mostly attributed to slower customer decisions due to macroeconomic concerns and larger offshoring which is revenue-dilutive and margin-accretive. The macro concerns have been industry-wide and do not affect only Teleperformance. As we gain more clarity during the Q2 report regarding full-year guidance, which we believe will be maintained also thanks to new contacts, the stock should rerate.

Generative AI

A major concern is AI risk, given the amount of volume that can be automated. ChatGPT has been a significant investment theme in 2023 producing many winners and losers. Across sectors, companies that could be adversely affected by generative AI such as Chegg (CHGG) have derated sharply. We believe Teleperformance does not deserve such a sharp derating given its impressive track record of growth despite AI in the last 5 years, its own generative AI solutions , and the likely emergence of a new type of business for Teleperformance: helping clients implement and use generative AI. Teleperformance has successfully navigated many technological shifts in the past, albeit not as large as this one, and has demonstrated incredible flexibility and innovation.

Teleperformance and AI presentation Teleperformance and AI presentation

{kind=link}

{kind=link}

Source: Teleperformance and AI presentation

Majorel transaction

At ca. 9x EBITDA, we believe this is a just allocation of capital and we are optimistic about the prospects of this acquisition . Opportunistically acquiring a leading global player in the wave of broader industry consolidation, at a reasonable price with synergies at potentially 2-3x target EBITDA is highly commendable.

Valuation

The multiple contraction has been sharp. Over the last decade, the median forward PE has been around 18x, and over the last 5 years, it has been between 20x and 30x. It now stands at ca. 10x. We find this valuation extremely compelling. 10x PE is remarkably cheap for a high-quality European large-cap, leading business services company growing organic sales at GDP+ rates - most likely in the range of mid to high single digits over the medium term - with significantly improving margins and healthy cash flow generation which is reinvested at attractive rates of return or given back to shareholders through dividends and buybacks.

While we understand investors' concerns regarding content moderation, full-year guidance revisions, and AI risk, we believe those do not justify this type of multiple, and see this as an attractive opportunity.

The margin of safety is quite compelling - even if worst-case scenarios would come to light, we do not see much potential downside from here given where Teleperformance is trading. In fact, it appears as if worst-case scenarios are already baked into the share price, with any positive information around these issues likely becoming a catalyst for a rerating.

On a relative valuation basis, we value Teleperformance at 15x forward earnings, still at a significant discount to historical multiples to reflect these uncertainties. Based on a diluted EPS estimate of €15/share in 2024, that would mean a target price of €225 or an upside of 47%. We would like to emphasize that 15x is a much lower multiple vs. the last years.

Alternatively, using EV/EBITDA evaluation, we could get to an EBITDA of €1.85 billion in 2024 growing ca. 6% from this year. This assumes no margin expansion, hence the growth is similar to the total growth of the group sales in 2024, which we estimate at 6% (both numbers are lower than analyst consensus). Assuming a multiple of 8.5x, which is at the low end of the 10-year historical multiple and subtracting net debt and making other EV adjustments that would result in a market cap of €14.3 billion and a share price of €242.

We would argue that based on the growth, diversification, business mix, and earnings quality Teleperformance's true peers should not only include Customer Experience companies like Concentrix (CNXC), Majorel, and Atento (ATTO), but also IT Services companies such as Accenture (ACN), Infosys (INFY), etc., and high-quality European Business Service names such as Bureau Veritas (BVRDF), Rentokil (RTO), SGS (SGSOF), etc. The latter groups trade at nearly double Teleperformance's forward PE multiple.

We also perform a DCF valuation of Teleperformance. We arrive at an FCF of €981 million in 2023 and use an FCF growth rate of 6% in 2024 in line with EBITDA growth, and 5% for the following years, fading all the way to 2% in 2030, assuming Teleperformance will be merely able to achieve OECD GDP level growth from 2030 onwards. We use a WACC of 7.5% based on the CAPM Model and a terminal growth rate of 2%. We finally arrive at a market cap of €13 billion, or a share price of €220, which provides a satisfactory sanity check for our exercise. As DCFs are very sensitive to even small assumptions regarding long-term growth rates and cost of capital assumptions, we rely mostly on our relative valuation and use DCF only as a sanity check.

A blended valuation (50% intrinsic, 50% relative) points to a share price of €227/share ($247/share) or 50% upside.

{kind=link}

{kind=link}

Risks

Risks that could challenge our long thesis on Teleperformance include adverse macroeconomic conditions leading to a decline in growth and a downward guidance revision for the fiscal year 2023, further negative news outflow around the content moderation business, inability to properly integrate Majorel and execute synergies despite Teleperformance's strong M&A track record, cannibalization from generative AI leading to market share losses, and key man risk as CEO and founder Daniel Julien eventually retires although this is not likely to happen soon.

Conclusion

We recommend building a small long position in Teleperformance shares, paying close attention to the Q2 report on July 26th, 2023, and in case a positive outlook is confirmed and full-year guidance is maintained, accumulating more shares.

For further details see:

Teleperformance SE: Quality Compounder At A Compelling Valuation