TLPFF - Teleperformance Stock: Not As Cheap As You Might Think

2023-11-16 08:00:00 ET

Summary

- Teleperformance stock is trading at a significant discount, down 70% from its all-time high - but does that make it a veritable deep value opportunity?

- In this article, I will discuss the business model of Teleperformance SE and take a look at its profitability, balance sheet quality and dividend safety.

- I will highlight major investment risks, discuss the recent controversies and touch on the potential threat of AI to Teleperformance's business model.

- I will also provide a multiple - and DCF-based valuation of TEP stock and explain why it is not as cheap as it looks at first glance.

Introduction

The stock of multinational business services provider Teleperformance SE ( TLPFF , TLPFY ) looks like a real deep value opportunity. After a remarkably strong run up to $450 in the fourth quarter of 2021, the stock has reversed course and is now trading 70% below its all-time high - currently at $142. In euros (Teleperformance's primary listing is on the Euronext Paris stock exchange, ticker TEP), the severity of the sell-off is not much different.

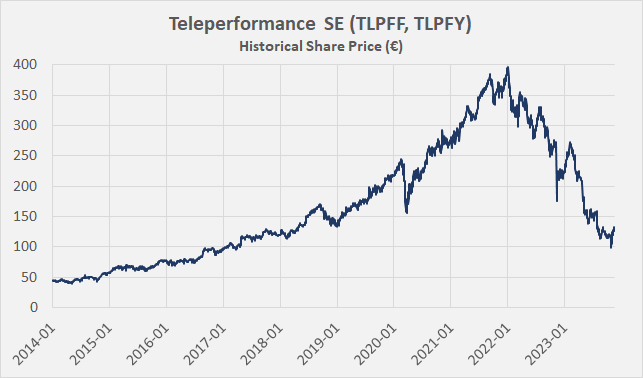

Looking at the chart in Figure 1, one could argue that the recent underperformance is merely a case of mean-reversion from a significant overvaluation of TEP stock during the post-pandemic stock market frenzy. However, considering that the stock is currently trading at levels last seen in 2018 (it even briefly dipped below €100 in October), there must be other reasons for the extremely poor performance in 2022 and 2023.

Figure 1: Teleperformance SE (TLPFF, TLPFY): Daily closing stock price according to the Euronext Paris (own work, based on TEP's daily closing stock price)

{kind=link}

In this article, I will discuss the company's business model and take a look at its profitability, balance sheet quality and dividend safety. I will also put the current share price in perspective and conclude by explaining whether I currently consider the stock a buy, hold, or sell - also taking account controversies surrounding the company's business practices and the fact that TLPFF stock has recovered very strongly from its recent low of € 96.6 and has risen by almost 40% in less than a month.

As an aside, and before we move on to the main body of the article, U.S.-based investors should know that Teleperformance trades as depositary receipts (ticker TLPFY , 2:1 ratio), but the common shares are also tradable (ticker TLPFF ). However, as the shares are not listed on a major U.S. exchange, the trading volume (OTC) is very low, leading to potentially large bid-ask spreads. It is also important to keep an eye on possible depositary receipt fees and the French withholding tax on dividends .

Business Overview And Reasons For The Underperformance

Teleperformance was founded in 1978 by Daniel Julien, the historical leader of the company, who has been Chairman of the Board and CEO since October 2017 (p. 184, 2022 annual report ). He currently owns 2 % of the company's share capital . What began as a telemarketing company with just ten lines quickly developed into the market leader in France. The company expanded to other European countries beginning in 1986 and opened its first call center in the USA in 1993. Since 2007, Teleperformance has been the global market leader in customer relations management.

The company's range of services includes telemarketing, technical support, visa application management, debt collection, process outsourcing, government services, data analytics and much more. The company's services are offered in more than 300 languages in 91 countries around the world and it currently serves around 1,200 clients. Some of Teleperformance's best-known clients include big tech companies like Meta Platforms, Inc. ( META ), Amazon.com, Inc. ( AMZN ), Apple Inc. ( AAPL ) and even Alphabet Inc. ( GOOG / GOOGL ). Given the company's long history, leading position, global scale, and apparent close relationships with many leading companies, it's fair to say that the company has an economic moat. Nevertheless, Teleperformance needs to constantly advance its technological capabilities and offerings in order to remain competitive.

Due to its business model, Teleperformance has benefited greatly from the trend towards remote working (50% of its employees work from home), which has accelerated massively due to government-imposed lockdown measures during the pandemic. This already suggests that Teleperformance is highly profitable due to its presumably asset-lean approach.

In the context of remote working arrangements, however, the Colombian Ministry of Labor's investigation into alleged labor law violations in November 2022 seems worth mentioning, which caused TEP stock to plummet by more than 30% (see Figure 1). However - and I acknowledge that this type of investigation is certainly of particular importance - Teleperformance has already made negative headlines in 2021, for example in connection with TP Observer , a " risk-mitigation tool that monitors and tracks real time employee behaviour, and detects any violations to pre-set business rules ". And back in April 2020, UNI Global Union and four French labor unions filed a complaint against Teleperformance under the OECD Guidelines for Multinational Enterprises. Many of these controversies, which management addresses on p. 137 of the 2022 annual report, relate in particular to the company's activities in the field of content moderation. Although an independent study by Korn Ferry concluded that the quality of Teleperformance's employee experience in this segment was significantly above the peer group (p. 137, 2022 annual report), management nevertheless decided to withdraw from the most offensive segment of its content moderation offerings. The company also signed a global agreement with UNI Global Union to strengthen its commitment to employee rights (p. 127, 2022 annual report) and more recently with unions in Colombia .

In addition to these developments, the increasing prevalence of artificial intelligence ((AI)) is a key reason for the poor performance of TLPFY stock. The reasoning is simple: AI can replace many of the tasks currently performed by humans. However, in the context of content moderation and the difficulties and controversies associated with it, I think it's fair to point out that AI technologies can actually be a tailwind for Teleperformance.

Another risk in relation to AI is that some of the company's customers (see above) may develop their own technologies and as a result no longer need Teleperformance's services and may even re-emerge as competitors. However, given the long-standing relationships and the obvious value proposition of Teleperformance's offerings, I don't see this as an immediate threat. It would likely take a long time and significant resources for Teleperformance's customers to build their own assets and grow their own customer bases. Figuratively speaking, this is definitely not a low-hanging fruit that the controlling departments of Alphabet, Apple, etc. might be eyeing.

Also, I think it's likely that the resources Teleperformance is drawing on are rather sticky and the company has long-standing relationships in this context as well. Nevertheless, it is important to keep in mind that many of the tasks performed by Teleperformance's employees are relatively simple and can therefore be replaced quite easily. In this context, Teleperformance's global presence and strong local market penetration leaves a positive impression.

Finally, it is important to keep in mind that AI is not something that only emerged in 2023 (even if the performance of certain stocks might suggest this). Teleperformance has been actively deploying AI technologies for many years, and currently at least one of Teleperformance's top five AI products is integrated into more than two-thirds of the company's top 200 client relationships. Management addresses its efforts in this area, for example, in the Q4 2022 earnings call .

Teleperformance's Profitability - The Key To Outperformance?

Teleperformance operates in two segments.

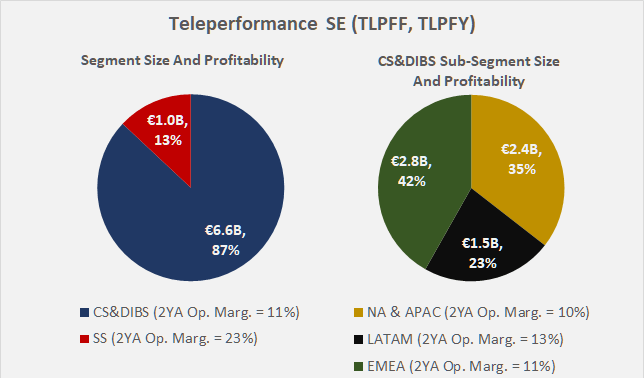

Core Services & Digital Integrated Business Services (CS&DIBS), according to the company (p. 295, 2022 annual report), " includes customer care, technical support and new customer acquisitions, in addition to the management of business processes, digital platform services and the high added-value consulting and data analysis offered by Teleperformance KS" .

Specialized Services (SS) " includes the interpreting services of LanguageLine Solutions, […] visa application management services for government departments offered by TLScontact, the health management business services of Health Advocate, the recruitment process outsourcing services of PSG Global Solutions and the accounts receivable credit management services of AllianceOne in North America ".

Considering that CS&DIBS is Teleperformance's largest revenue contributor (Figure 2, left) and Specialized Services is significantly more profitable, comparatively lower long-term growth in the latter segment would result in a deterioration of the consolidated operating and free cash flow margin. Similarly, CS&DIBS' LATAM segment is by far the most profitable of the three reportable geographic segments, but at the same time contributes the least to revenue (Figure 2, right). This leads to a fairly balanced profitability within the CS&DIBS segment.

Figure 2: Teleperformance SE (TLPFF, TLPFY): Segment revenues and profitability (own work, based on company reports)

{kind=link}

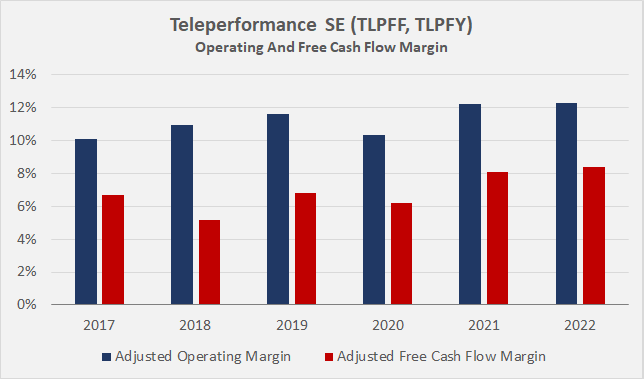

On a consolidated basis, TEP's operating and free cash flow margins have improved over the last six years (Figure 3), which is at least in part attributable to the increasing emphasis on remote working. Management showed cost discipline over the years, maintaining personnel expenses at 66% ± 1% of revenue over the last six years. However, acquisitions likely also helped from a profitability standpoint.

Over the last six years, Teleperformance has spent €2.0 billion on acquisitions, and it is important to note that the company sometimes uses equity as well as debt to finance transactions. For example, the acquisition of Majorel ( announced in April 2023 , not included in the €2.0 billion figure) was the main driver for the increase in outstanding shares from 59.7 million (weighted average 2022) to 64.1 million (as of November 3, 2023 ).

Figure 3: Teleperformance SE (TLPFF, TLPFY): Operating and free cash flow margins; operating earnings have been adjusted for goodwill impairments and free cash flow has been adjusted for stock-based compensation and working capital movements (own work, based on company reports)

{kind=link}

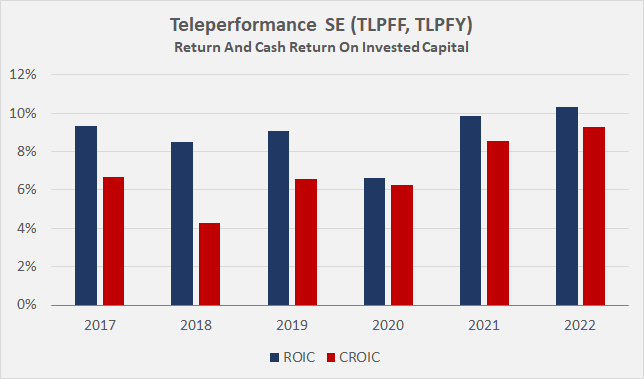

The company has rather modest capex requirements (4.0% ± 0.6% over the last six years). Against this backdrop, I don't think TEP's margins are particularly positive. Granted, the company's profitability is in line with peers , but this only shows how competitive the business process outsourcing sector is. In particular, the difference between operating and cash profitability is disappointing and may indicate poor working capital management. Over the last ten years, the company's days sales outstanding (DSO) and days payables outstanding (DPO) have not been improved. The company may also be struggling to properly integrate acquired entities. The potentially slow depreciation of assets probably also plays a role. Teleperformance's strategy to grow through acquisitions (in addition to organic growth) leads to significant goodwill on the balance sheet, which in turn leads to mediocre returns on invested capital (Figure 4), sometimes even below the company's estimated cost of capital (or cost of equity, in the case of CROIC). Frankly, I would have expected better profitability from a leading outsourcing company.

Against this backdrop, I see the increasing use of AI as a tailwind for Teleperformance, which should help the company to further improve its profitability. However, as the more or less regular acquisitions are a major reason for the rather mediocre profitability, it is important to keep a close eye on the integration of Majorel, which was acquired for €3 billion. The enterprise value of Teleperformance before the transaction, but based on today's share price, is around €11.1 billion, so Majorel is definitely a big chunk to swallow. Of course, merger integration is a major risk to consider before investing in Teleperformance.

Figure 4: Teleperformance SE (TLPFF, TLPFY): Return and cash return on invested capital (own work, based on company reports)

{kind=link}

Balance Sheet Quality And Dividend Safety

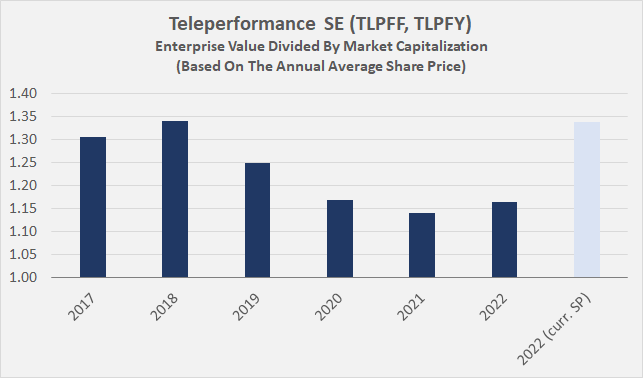

As mentioned above, the company finances its acquisitions not only through debt, but sometimes also through capital increases. Nevertheless, Teleperformance's EV/MC ratio (enterprise value divided by market capitalization) indicates a significant amount of debt, but the ratio seems to have improved over the years. However, this is largely due to the use of the average annual share price in Figure 5 and the strong performance of TEP shares. Based on the current share price and shares outstanding, the ratio is back to the 2017/18 level (light blue bar in Figure 5).

Figure 5: Teleperformance SE (TLPFF, TLPFY): Enterprise value divided by market capitalization (own work, based on company reports)

{kind=link}

However, it is important to remember that Teleperformance relies heavily on operating lease arrangements, which I have included in the enterprise value calculation. I acknowledge that leases are not generally (at least not before the adoption of IFRS 16 ) included in the calculation of enterprise value (and net debt), but given that they are contractual obligations, I think it's prudent to include them in the calculations.

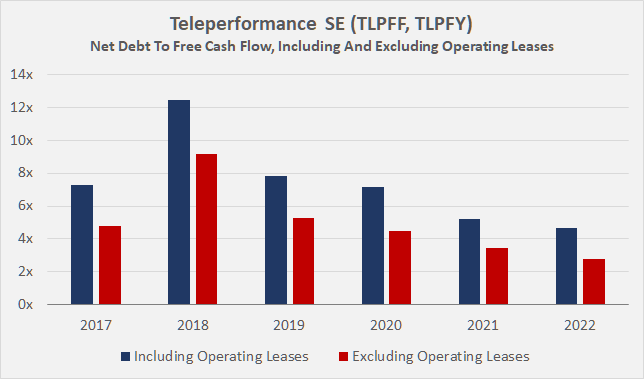

Figure 6 illustrates the impact of operating leases on Teleperformance's net debt. As an aside, and as a word of caution, those conducting their own due diligence should be mindful of IFRS 16 accounting when calculating free cash flow. Payments related to operating leases are now reported as cash flow from financing activities and therefore may be overlooked in traditional approaches (i.e., operating cash flow minus capital expenditures).

Figure 6: Teleperformance SE (TLPFF, TLPFY): Net debt to free cash flow, including and excluding operating leases (own work, based on company reports)

{kind=link}

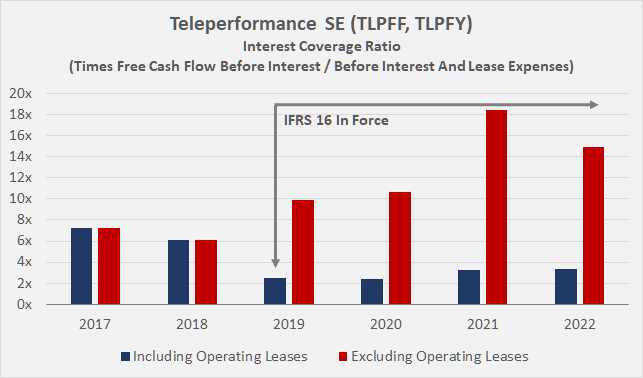

While Teleperformance's leverage in terms of free cash flow ( read here why I prefer this leverage metric) is manageable both without and with lease liabilities, the interest coverage ratio looks quite weak when lease expenses are included (blue bars in Figure 7). Admittedly, Teleperformance's business model appears to be quite predictable and generates stable cash flows, so the weak coverage is not problematic at first glance.

Figure 7: Teleperformance SE (TLPFF, TLPFY): Interest coverage ratio, in terms of free cash flow before interest and before interest and lease expenses (own work, based on company reports)

{kind=link}

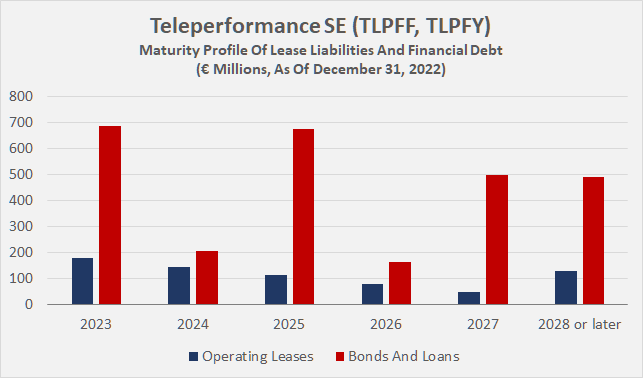

However, I consider the company to be at least moderately cyclical, so it is reasonable to assume that free cash flow will decline in a recession (Teleperformance's operating cash flow declined by 45% in 2008 compared to the previous year). Depending on the severity of the downturn, management may need to consider terminating leases, so it is worth looking at the maturity profile (blue bars in Figure 8). In my view, Teleperformance's lease agreements are very conservative and allow for dynamic navigation (>25% maturing in less than a year).

In contrast to lease contract maturities, however, the maturities of Teleperformance's debt are anything but conservative. (red bars in Figure 8). 19% of the company's outstanding debt is bank loans or credit facilities (some of which are short-term in nature), and almost 60% of TEP's total debt matures within the next two years. Granted, one can assume that the short-term debt has been renegotiated by now, but I think it's still important to keep an eye on the debt, especially given the current interest rate environment. That being said, with its current BBB credit rating (which was upgraded from BBB- in late 2021 ), Teleperformance should have no problem refinancing its debt at market rates.

Figure 8: Teleperformance SE (TLPFF, TLPFY): Maturity profile of lease liabilities and financial debt (own work, based on company reports)

{kind=link}

Against this backdrop, I am somewhat ambivalent about Teleperformance's latest €500 million share buyback program , which comes as a surprise shortly after the partially equity-financed acquisition of Majorel. While the buyback authorization suggests that the stock is a good value (see next section), it sends a different message than the recent capital increase and will obviously reduce the company's financial flexibility.

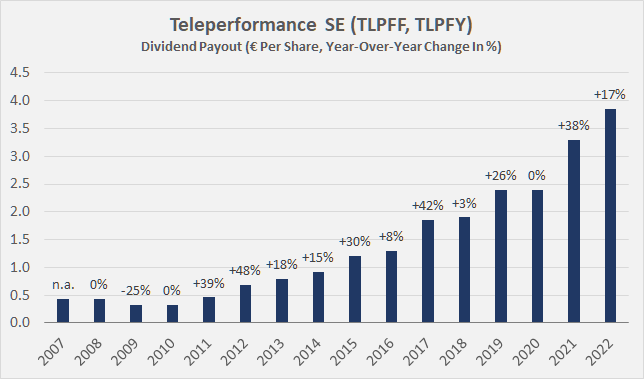

Therefore, I frankly don't think the dividend (current yield of 2.8% based on an annual payout of €3.85 for 2022 ) is particularly safe in a recession. Teleperformance cut its dividend by 25% in 2009, after maintaining the 2007 payout of €0.44 in 2008 (Figure 9). However, given the company's fundamentally shareholder-friendly stance and insider ownership (founder and CEO Julien owns around 1.28 million shares, which equates to €5 million in annual dividends), I would expect the previously cut dividend to be reinstated and grown as soon as circumstances allow (see, e.g., 2021 - 38% growth). It is also worth noting that the company currently only pays out a third of its free cash flow.

Figure 9: Teleperformance SE (TLPFF, TLPFY): Annual dividend payout to shareholders and year-over-year change in percent (own work, based on company reports)

{kind=link}

Valuation Of Teleperformance Stock

With Teleperformance shares down almost 70% from their all-time high - even after the sharp rebound from the October low - it seems reasonable to conclude that this is a bargain opportunity. However, with excessive investor optimism, high disposable income and historically low interest rates contributing to what can only be described as bubble-like valuations in 2021, a closer look is warranted.

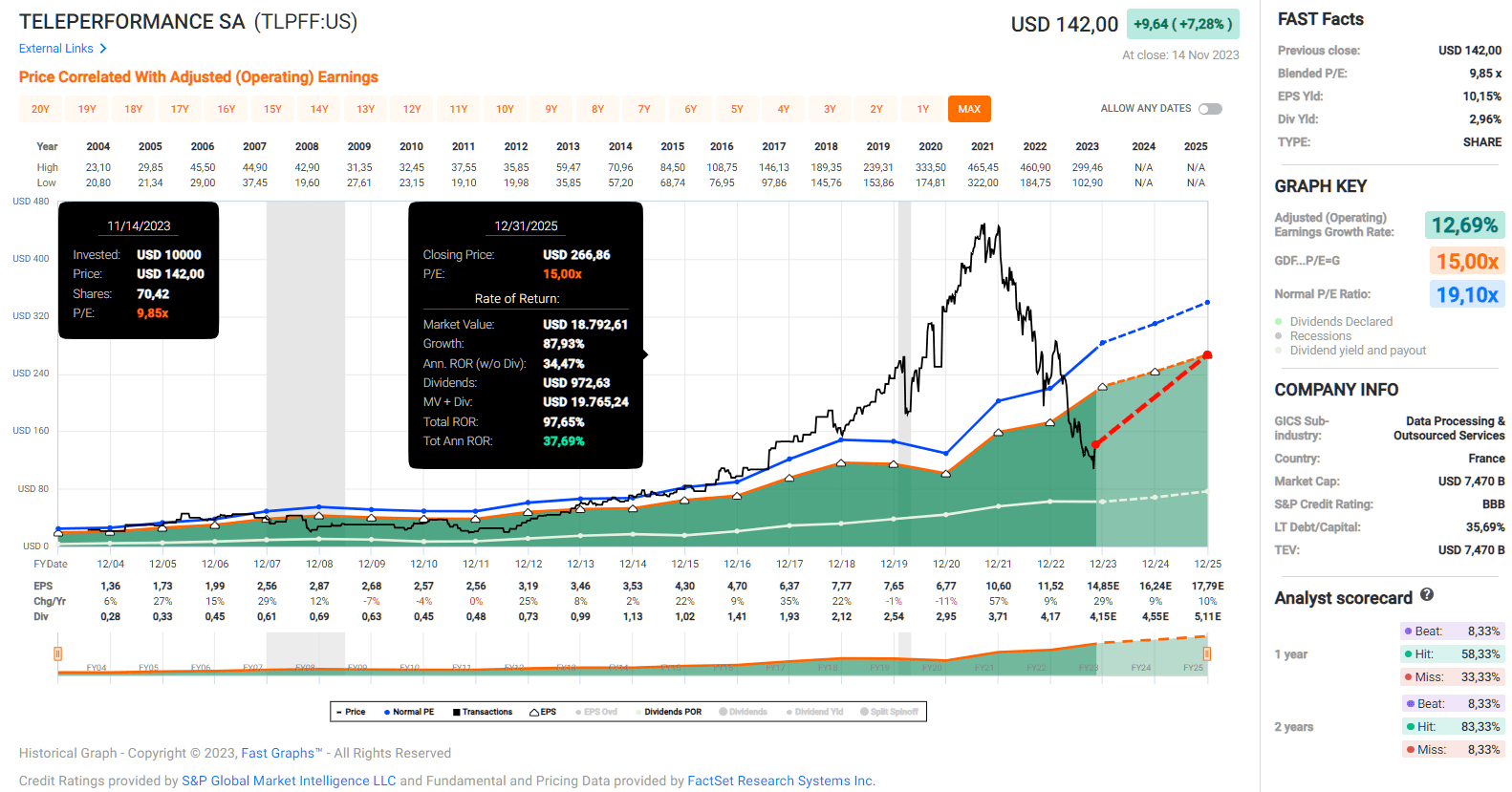

With the caveat that exchange rate effects are inherently taken into account (as mentioned above, TEP's main listing is on the Paris exchange), the FAST Graphs chart is shown in Figure 10. At a current blended price to earnings ratio of 10, an investment in TEP stock today has the potential to generate an annualized return of 38% by 2025 if analysts' growth forecasts hold and the stock returns to an earnings multiple of 15. This is not really a demanding valuation, considering that Teleperformance's earnings grew at a long-term average growth rate of almost 13% and the long-term average P/E ratio is 19 (but of course keep in mind the historically low interest rates).

Figure 10: Teleperformance SE (TLPFF, TLPFY): FAST Graphs chart, based on adjusted (operating) earnings per share (FAST Graphs)

{kind=link}

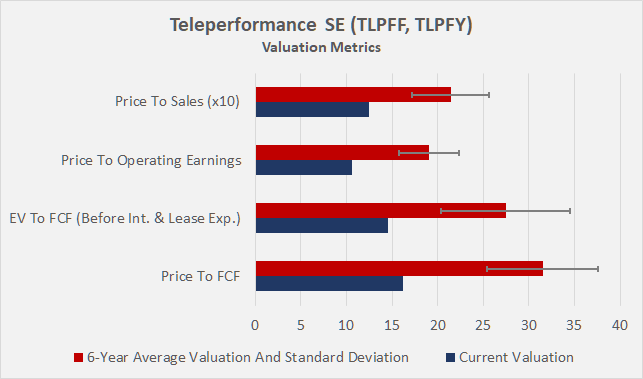

The stock also looks cheap from the perspective of price (market cap) relative to historical free cash flow (the inverse of FCF yield), enterprise value relative to historical free cash flow (before interest and lease expenses), price relative to historical operating income and relative to historical sales (scaled by a factor of 10 for better visibility, Figure 11). It should be noted that I have used three-year averages for free cash flow, operating profit and revenue in order to remain conservative in my valuation.

Figure 11: Teleperformance SE (TLPFF, TLPFY): Multiples-based historical valuation (own work)

{kind=link}

Finally, let's look at the valuation of TLPFY shares through the lens of discounted cash flows ((DCF)). Using 30-year French government bonds ( current yield 3.7% ) as a proxy for the risk-free rate and taking into account the uncertainties related to the business model as well as the mediocre balance sheet, I believe an equity risk premium of 6% is appropriate, resulting in a cost of equity of 9.7%. Based on FactSet's short-term growth estimates and using the average free cash flow for the years 2021-2022 (excluding stock-based compensation), Teleperformance appears only modestly undervalued (Figure 12). Admittedly, the model does not take into account Majorel's expected contribution to free cash flow. However, given the merger integration risk and the potentially less than optimal integration of previous acquisitions (see above), I think it is better to remain conservative here.

All in all, I think it makes sense that TLPFF stock looks less favorable from a DCF perspective than from a valuation based on historical multiples. The stock has undoubtedly gone through a period of overvaluation, which distorts the six-year average of historical multiples, and the DCF valuation takes into account the company's comparatively weak cash profitability.

Figure 12: Teleperformance SE (TLPFF, TLPFY): Discounted cash flow valuation and sensitivity analysis (own work)

Conclusion

Teleperformance is undoubtedly an interesting, founder-led company with a strong history. It seems to be well entrenched with many leading companies and I don't think the topic of AI should be seen as an outright headwind for the company.

In fact, AI is not something that only emerged in 2023 and Teleperformance has been active in this area for some time. But of course, the company must constantly invest in innovation to keep pace with current competitors and big tech companies that could become direct competitors in the more distant future. I am thinking in particular of Microsoft Corp. ( MSFT ) because of its extremely strong position in the corporate environment and the resulting stickiness of its business relationships.

Nevertheless, Teleperformance is undoubtedly a leader in its field. Management is pursuing a path that relies on organic growth but also on acquisitions. The recent acquisition of Majorel is definitely a big chunk to swallow and shows the limits of this strategy - after all, Teleperformance itself is only a €9 billion company with a fairly pronounced level of debt on its balance sheet. Previous transactions seem to have been generally well digested, but the discrepancy between operating and cash profitability suggests that there is still room for improvement. Investors should therefore keep a close eye on how the integration of Majorel progresses.

Given that Teleperformance has what I consider an asset-light business model, I was somewhat surprised that the company is not consistently able to generate excess returns on invested capital. In addition to a possible need to improve the integration of the acquired businesses, this points to a highly competitive environment.

TEP stock is under pressure due to the AI narrative (which I believe is only partially justified and could actually benefit the company from a profitability perspective), the controversies surrounding its content moderation unit (and other business practices), but probably also due to the mediocre balance sheet amid the current interest rate environment.

The heavy reliance on operating leases makes the company's profitability vulnerable to recessions (the contractual obligations can be seen as fixed costs, resulting in significant operating leverage), but it is reassuring to see that the leases are mainly short-term in nature. This provides management with a great deal of flexibility in the event of a prolonged downturn. Conversely, the company has a significant amount of interest-bearing debt with a surprisingly short-term maturity profile, which could lead to refinancing transactions at potentially unfavorable interest rates.

All in all, a certain valuation discount is justified in view of the uncertainties, the competitive environment and the mediocre balance sheet. However, with a P/E ratio of less than 10 and a free cash flow yield of 6%, I believe the stock is trading at a discount to fair value. However, I think that the valuation will only improve sustainably when sentiment around the company improves, Majorel is properly integrated and Teleperformance's ROIC and CROIC are reliably well above the weighted-average cost of capital and cost of equity, respectively.

I personally am not currently interested in buying the stock, mainly because of the extremely sharp rebound over the last few weeks. As a long-term investor, I have time on my side, so I will wait and see if the upswing proves to be sustainable and how the integration of Majorel goes. As with many other European companies, there was only a very concise quarterly update in November, so I don't mind waiting for the full-year results and balance sheet data due in February 2024. However, if the stock falls to the low €100s against the backdrop of a weak overall market and not on company-specific negative news, I could see myself building a speculative entry position immediately.

Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.

For further details see:

Teleperformance Stock: Not As Cheap As You Might Think