USM - Telephone and Data Systems Is A Definite Buy If USM Is Sold

2023-10-25 05:53:51 ET

Summary

- Telephone and Data Systems may be planning to divest its stake in UScellular, causing TDS shares to soar by 93%.

- TDS has been experiencing declining financial performance, indicating the need for a strategic change.

- The potential sale of TDS's USM stake could significantly reduce TDS's long-term debt and bolster its cash reserves. Thus, I rate TDS a "buy" with a $26.10 price target.

- However, TDS's governance structure, dominated by the Carlson family, and yet-to-be-finalized sale details pose substantial risks.

The speculative plan of Telephone and Data Systems ( TDS ) to divest its stake in UScellular ( USM ) has noticeably stirred the market, sending TDS shares soaring by 93% and highlighting a potential financial transformation. I believe that if the USM stake is sold, TDS could be a "buy" up to $26.10 per share. Generally, the phrasing used in the announcement suggests to me that there's a reasonable chance of the sale going through. Nonetheless, it's vital to recognize the risks tied to the governance structure and the yet-to-be-finalized details of the sale. Should the sale fall through, it would signify a substantial downside for current shareholders.

Business Overview

TDS, listed among the Fortune 1000 companies, is a multifaceted telecommunications entity that runs its operations chiefly through two subsidiaries - UScellular, of which it owns 83% , and TDS Telecom, a wholly-owned subsidiary. Together, they offer communication services to approximately 6 million connections across the United States. Additionally, TDS has diversified with two other subsidiaries, OneNeck, specializing in hybrid IT solutions such as cloud and hosting services, and Suttle-Straus, which operates in the printing business sector.

Raymond James 2023 Institutional Investors Conference

TDS Telecom, based in Madison, Wisconsin, with a workforce of 3,500, delivers high-speed internet, TV, and voice services to around 1.2 million connections in rural and suburban areas across the US. It was established in 1969 by LeRoy T. Carlson as a part of Telephone and Data Systems, Inc., which aimed to bring advanced technology to smaller communities by acquiring local telephone companies. While retaining its original mission, TDS Telecom has grown to include cutting-edge internet, TV, and phone services, with internet speeds reaching up to 8 Gigabit. Besides serving individuals, the company offers businesses various advanced communication solutions and services.?

Disappointing Performance

The financial data for TDS Telecom for the periods ending June 30, 2023, and 2022 reveals a declining financial performance YoY, with a notable decrease in net income across both three and six-month periods, possibly indicating operational or market challenges. 1H2023 showed a net loss of 22 million, compared to net income of 61 million in 1H2022. EBITDA declined 11% in 1H2023 YoY, from $345 million to $307 million. This significant dip highlights the need to reassess TDS Telecom's operational strategies to improve its financial health. And in fact, it looks like the only way out for TDS might be through M&A, and here is where its 83% stake in USM comes into play.

For context, USM is the fifth-largest mobile network operator in the U.S. and, headquartered in Chicago, extends its customers' high-speed internet, TV, and voice services. It serves individual consumers and caters to business sectors by offering VoIP, dedicated internet, and other advanced communication solutions. With a solid footing in the U.S. wireless market, USM operates robustly, boasting a substantial customer base of 4.7 million retail connections, of which 4.2 million are postpaid and 0.5 million are prepaid. Its operational network spans 21 states, orchestrated by approximately 4,600 associates, and is structured around 4,341 owned towers with 6,952 cell sites in service.

Q2-2023-Earnings-Presentation-Final

Potential Sale of TDS's Stake in USM

On August 4, 2023, a notable update emerged when the Boards of TDS and USM decided to explore strategic alternatives for USM, suggesting potential changes in ownership structure. Following this announcement, shares of USM and TDS soared by 93% as the market saw this as a promising opportunity for the company. The Carlson family holds a 73% stake in US Cellular, and while they own about 10% of TDS, they effectively control it through super-majority voting rights, thereby also controlling USM. In June, investor Mario Gabelli expressed interest in nominating directors for TDS's board at the upcoming shareholder meeting. Although Gabelli had previously attempted to persuade the Carlson family to sell without success, the recent Board's decision might alter this scenario. And if TDS sells its USM stake, I believe it'd unlock significant shareholder value.

In fact, following the update, JPMorgan revised its outlook on the company. The agency upgraded the company's rating to "Overweight," concurrently increasing the price target to $52 from an earlier lower estimate of $24. I think this upgrade reflects a positive reassessment of the company's future financial prospects, catalyzed by the strategic decision to explore ownership structures. This move, I believe, could potentially unlock untapped value or foster operational enhancements that may have prompted JPMorgan to envisage a higher price target for the company's stock.

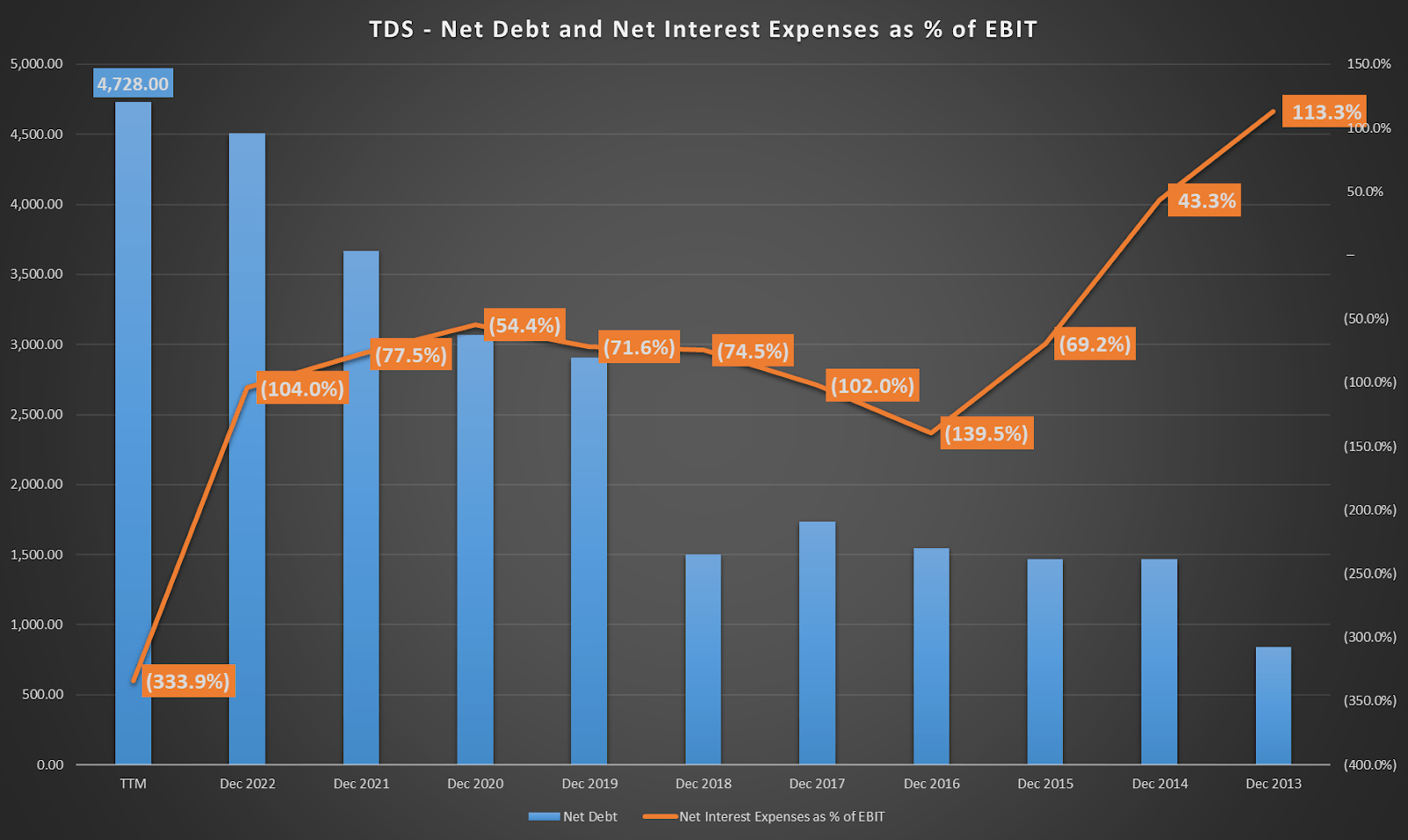

TDS's Perilous Financial Health

The last 10-Q TDS and its subsidiaries underscored a pattern of negative free cash flows that extended through the first half of 2023. Historically, TDS navigated its financial waters by leveraging a blend of existing cash, investment balances, and external financing, supplemented by asset sales and operational cash flows, to meet its operational and debt service requisites.

{kind=link}

As you can see, TDS has racked up a substantial amount of debt over time, and its interest payments are unsustainable. In my view, while in theory, TDS should have enough potential liquidity to continue as a going concern for now, over the long run, it'll continue destroying value unless this situation is addressed. For context, TDS's revolving credit agreement, export credit financing agreement, and receivables securitization agreement, among others, are crucial cogs in the TDS financial machinery. In fact, Standard & Poor's revised credit rating outlook to negative in June 2023 shows how grim TDS's financial situation is. After all, credit ratings are a barometer of financial health, and TDS's BB rating denotes financial stress, which I think is unbearable at this point.

TDS Valuation Analysis

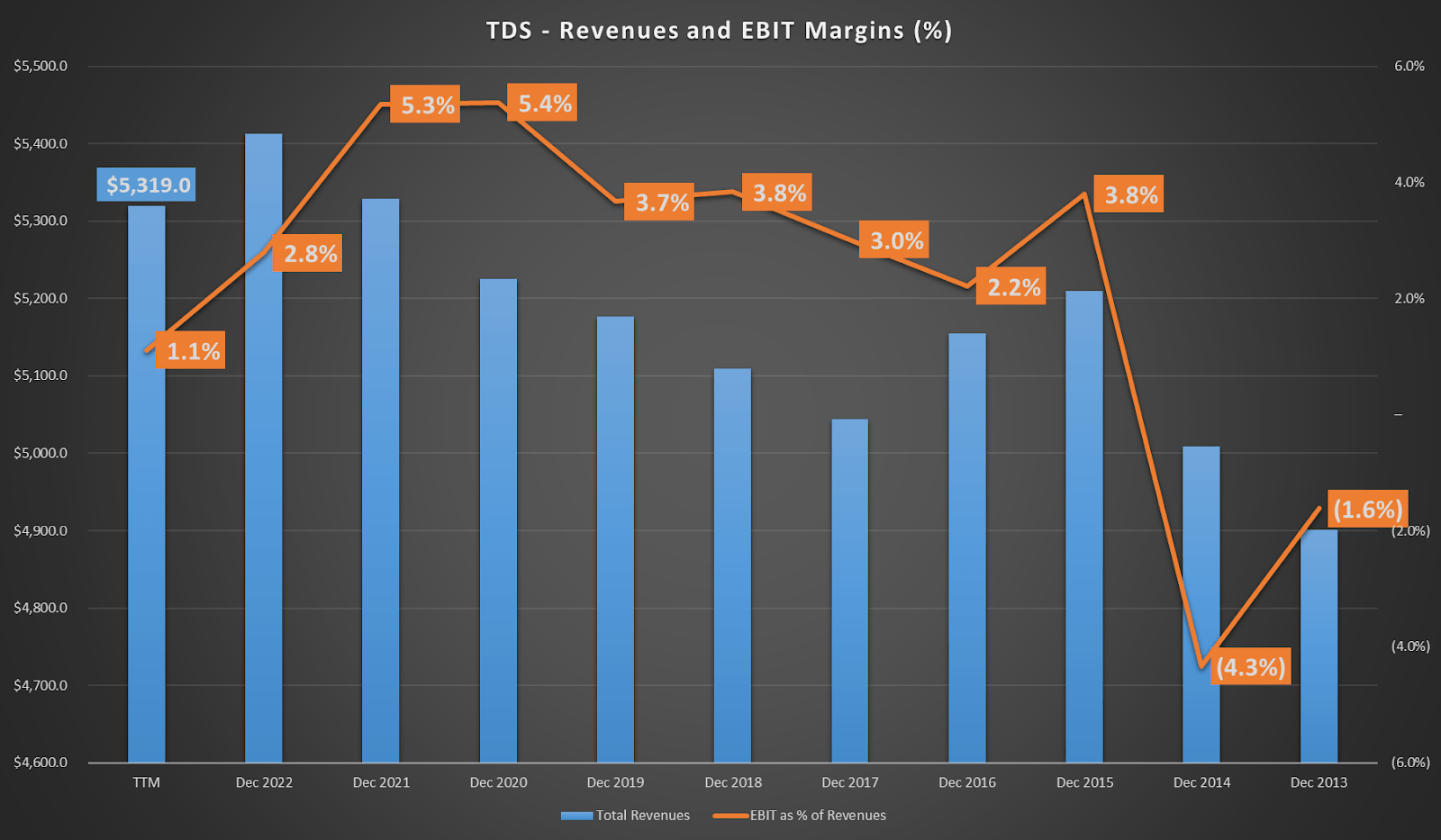

From a valuation standpoint, utilizing a standard Free Cash Flow to Firm DCF model presents a challenging valuation for TDS. Given its current performance trajectory, the company generates approximately $5.3 billion in revenues yet harbors slim EBIT margins of 1.1%. Although TDS has improved margin over time, its current margins are below the 5.4% EBIT margin achieved in 2020.

{kind=link}

So, assuming a fairly optimistic revenue growth trajectory alongside a gradual reversion to the EBIT margins seen in 2020, the current valuation of TDS still appears unjustified. The financial outlook is quite dismal because my model indicates a negative fair value for TDS, primarily due to its substantial debt load. To illustrate this, I have input TDS's current figures into this valuation model, with the results in the table below.

Author's elaboration.

However, TDS holds approximately 83% of USM, a publicly traded entity with a market capitalization of $3.56 billion. Theoretically, this places the value of TDS's stake at around $2.95 billion. Yet, upon sale, a slight premium may be paid for TDS's stake. Thus, we'll round off the value to $3 billion for simplicity. Bearing this in mind, I have utilized the latest figures from TDS and USM to ascertain the value of TDS should it divest its USM stake at $3 billion.

Hypothetically, upon the sale of TDS's entire stake in USM, TDS undergoes a financial reshuffling to reflect the transaction in its consolidated balance sheet, adhering to the principles of US GAAP. Initially, TDS's consolidated long-term debt would be $3.872 billion, but it'd also encompass USM's long-term debt of $3.105 billion. With the sale, TDS would deconsolidate USM's financials from its own, including removing USM's long-term debt from its consolidated balance sheet. This action results in a new long-term debt net figure of $767 million for TDS, obtained by subtracting USM's long-term debt from TDS's original consolidated long-term debt. Simultaneously, the sale injects $3 billion into TDS's coffers, which is added to its cash balance. Initially, TDS would have consolidated cash and cash equivalents of $251 million, including USM's cash balance of $186 million. Post-sale, TDS must also deconsolidate USM's cash balance from its own. This adjustment leaves TDS with a cash balance of $65 million before accounting for the sale proceeds. Adding the sale proceeds to this adjusted figure elevates TDS's cash and cash equivalents to $3.065 billion.

Author's elaboration.

Interestingly, the valuation makes much more sense if we price TDS's standalone EBIT at the sector's EV/EBIT multiple. This transaction significantly alters TDS's financial posture, reducing its long-term debt while considerably bolstering its cash reserves. The implied market cap for TDS standalone would be about $2.75 billion, indicating a 45.2% upside from the current levels. Thus, I'd argue that assuming the sale goes through, then TDS is a good buy, up to $26.10 per share.

Downside Risks

However, it's noteworthy that the Carlson family has consistently opposed selling the USM stake. Their risk-reward proposition differs from average TDS investors due to their majority ownership of voting power within the TDS Voting Trust . The TDS Voting Trust is a pivotal entity in TDS's governance structure, embodying over 50% of the voting power for electing directors as per NYSE's "controlled company" classification. A substantial portion of the influential Series A Common Shares, pivotal in electing directors and other key decisions, resides in this trust until 2035, centralizing control. Walter C.D. Carlson, a trustee and beneficiary of this trust, holds a significant position as the non-executive Chair of TDS's Board. This architecture, board positions, and distinct share classes consolidate control within the Carlson family.

While the current sentiment toward selling TDS's stake in USM appears promising, the reality underscores that the deal is yet to be finalized. Moreover, even with a genuine intention to sell, the specifics of the sale remain undisclosed. If the deal falls through, or if the Carlsons oppose the sale once again, TDS shareholders could find themselves tethered to a company grappling with a formidable debt load. This scenario presents a significant downside risk for existing shareholders. For perspective, TDS shares soared by 93% upon the hint of a potential sale, but this gain could evaporate quickly if it emerges that the sale won't materialize. So, if you buy TDS at these levels hoping for the upside due to USM being sold, you must also be aware of the substantial headline risks involved.

However, given that the news mentions "the board" decided to explore strategic options, it implies that the Carlsons have consented. This is because they own the majority of the board seats. Hence, I am inclined towards the bullish scenario where TDS sells its USM stake, potentially unlocking significant shareholder value for TDS shareholders. Consequently, I rate TDS as a "buy" up to $26.10 until more details on the sale are disclosed. However, please be aware of the risks associated with this speculative situation. If you invest in TDS, ensure it's only a smaller portion of your portfolio.

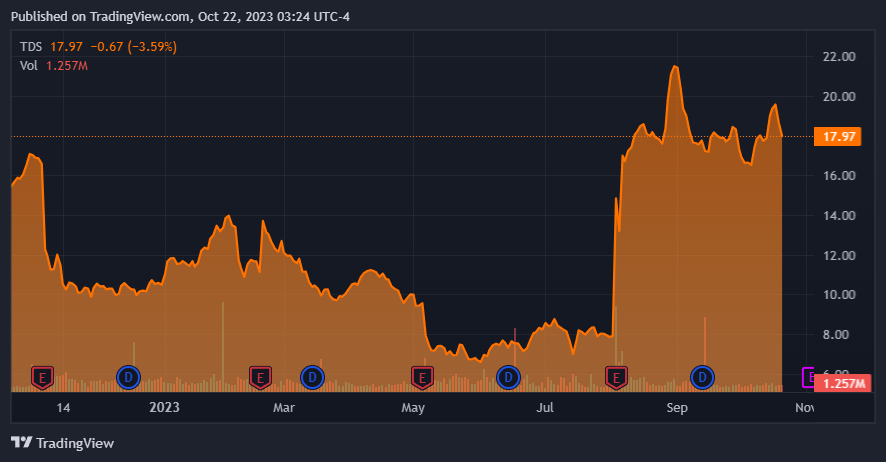

Investors are betting on TDS selling its USM stake. (TradingView.)

{kind=link}

Conclusion

The speculative notion of TDS selling its stake in USM has positively stirred TDS's stock, signaling a potential financial resurgence. Hence, I assign a "buy" rating for TDS with a price target of $26.10 per share, contingent on the successful completion of the sale. The market's enthusiastic reaction resonates with the perspective that this sale could mark a pivotal moment for TDS. Nonetheless, the Carlson family's historical involvement in the company's governance, coupled with the yet undisclosed details of the sale, inject a dose of uncertainty into this hopeful narrative. Therefore, investors should maintain a cautiously optimistic stance, ensuring a thorough understanding of the embedded risks. Should the Carlsons have a change of heart, or if the sale doesn't unfold under favorable terms, existing TDS shareholders might find themselves tethered to a cash-draining entity with an unjustifiable valuation. Furthermore, the shares might relinquish the recent uptick triggered by the sale speculation. So, investors should know that TDS is a speculative "buy."

For further details see:

Telephone and Data Systems Is A Definite Buy If USM Is Sold