TDS - Telephone And Data Systems Is Broken Without United States Cellular

2023-11-28 01:34:33 ET

Summary

- Q1 and Q2 analysis led to a sell recommendation for Telephone and Data Systems due to financial concerns, contradictory growth strategy, and overvaluation.

- TDS's capital investments are not paying off, profitability is declining, and the potential sale price for US Cellular does not support the stock's valuation.

- Given its unclear path to profitability and immediate losses, the company's valuation is largely based on the sale prospects.

I am revisiting my Q1 and Q2 thesis on Telephone and Data Systems (NYSE: TDS ) in light of Q3 earnings.

Looking back on my Q1 analysis, three key factors played a role in my sell recommendation:

- I didn't believe the financials could support the high 8% dividend yield over the next several years.

- Management's clearly articulated strategy for growth was in direct contradiction with their earnings guidance.

- Valuation multiples were significantly inflated, signaling an overvalued stock.

Following Q2, my recommendation continued to be a sell despite the announcement about a potential sale for US Cellular. My concerns were:

- TDS had lost money two quarters in a row and would still be unprofitable without US Cellular.

- TDS had lead cable exposure, not to the degree of AT&T and Verizon, but still a risk they can't afford.

- Valuation multiples were still elevated well above historical levels, and the $1.8+ billion market cap was not supported by the potential sale price.

Since my last analysis, the share price is up another 10% as Verizon, AT&T, and T-Mobile have all expressed an interest in US Cellular. Despite the interest, I continue to believe TDS is substantially overvalued and maintain my sell rating. TDS's capital investments are not paying off, their profitability continues to decline, and the potential sale price for US Cellular doesn't support the valuation given the state of TDS's business.

Capital Investments Are Not Paying Off

Capital from a potential sale is only helpful if it increases the company's future value. That means increasing cash flow either from investment or from reducing expenses. Unfortunately, TDS's existing investments are not paying off despite being a core strategic priority.

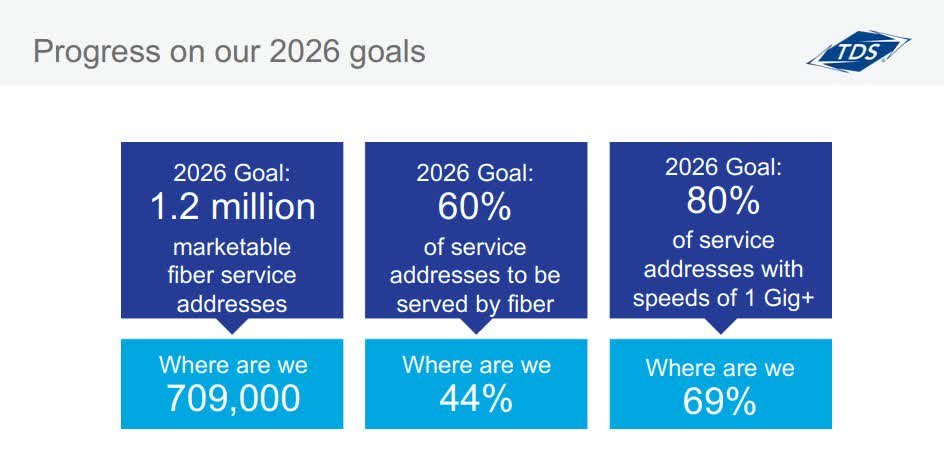

TDS has set aggressive goals for 2026 around fiber investment to set the stage for growth.

{kind=link}

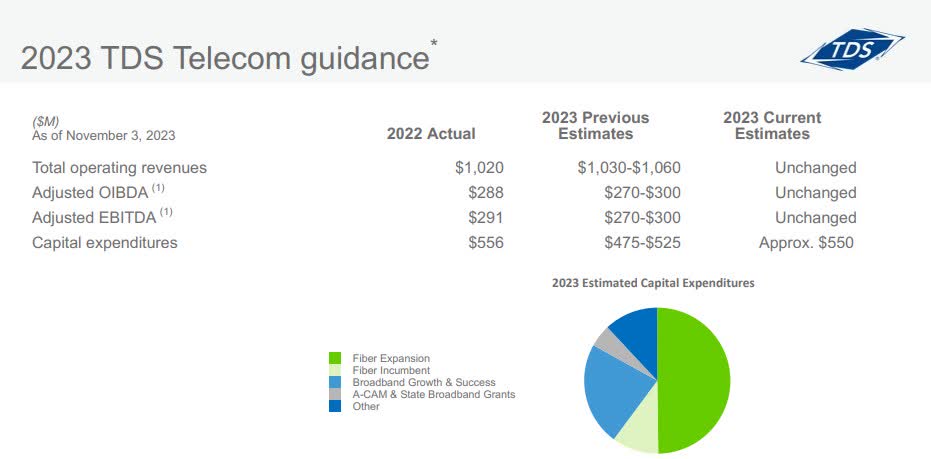

In Q3 earnings, they even increased capital investment guidance this year to stay on track for 2026.

{kind=link}

And TDS has successfully expanded its fiber footprint, growing addresses served by 11% this year.

Fiber Footprint (TDS Investor Relations)

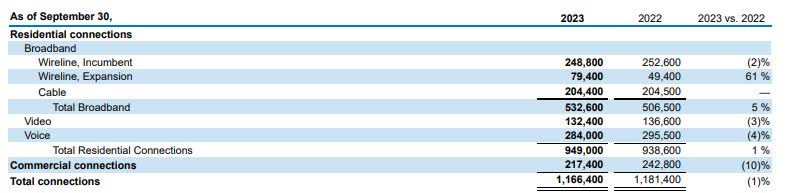

However, the investments aren't paying off. Despite a 5% increase in residential connections, revenue per connection only grew by 3%, falling behind average telecom inflation at 6%. And the growth from residential fiber just barely offset declines in high-margin commercial and wholesale businesses.

{kind=link}

TDS's significant capital investments today aren't moving the needle, so I don't believe an additional influx of cash would drive value.

Profitability Continues To Decline

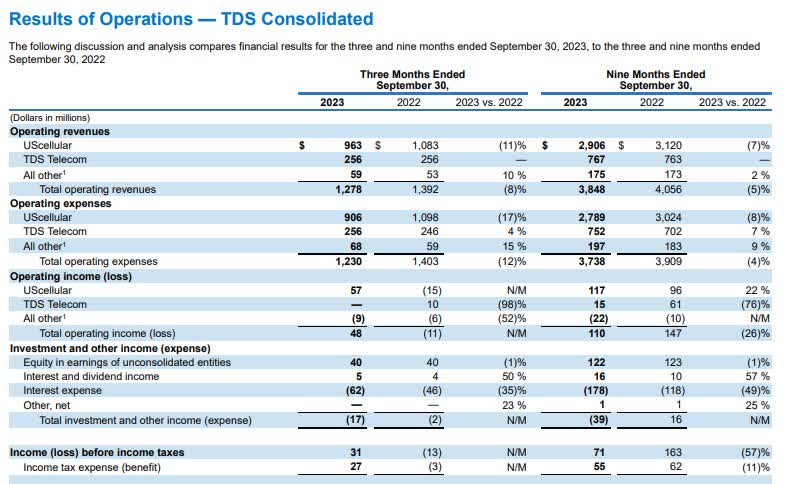

In addition to investments, TDS remains very unprofitable without US Cellular. In Q3, the core TDS business posted flat revenue and break-even operating income. Tacking on corporate overhead, TDS, excluding US Cellular, lost $9 million in the quarter prior to interest and non-consolidated entities, down $13 million from the profitable prior year Q3.

{kind=link}

TDS is also hemorrhaging connections faster than fiber installs can replace, which reduces near-term revenue potential even further.

{kind=link}

I find the declines in commercial and wholesale especially concerning, as these tend to be higher-margin and longer-term contracts that you can rely on for stable cash flow.

Revenue cause of change (TDS Investor Relations)

In Q3 earnings , management focused almost exclusively on the fiber build-out and didn't provide any clarity for a return to profitability. TDS without US Cellular is dead on arrival without a growing, cash-flowing business.

Potential Sale Price Doesn't Support Valuation

If there is any question about the value of TDS versus USM, look no further than market cap where TDS has a negative value excluding USM.

{kind=link}

Prior to the sale announcement, TDS had a market cap just below $1 billion, while USM had a market cap near $1.5 billion. This implies a market value of -$0.2 billion for TDS adjusting for their ownership stake in USM.

Raymond James has estimated a potential sale value at $2.5 billion, based on Verizon's purchase of Tracfone. I came to a value of $1.4 billion in my Q2 analysis based on book value of assets and a 20% premium for tower assets. However, I like Raymond James's analysis better looking at Tracfone and spectrum, so I will range from $2 to $2.5 billion.

At an 83% ownership share, this would increase the implied value of TDS from -$0.2 billion to $1.6 to $2.1 billion. With market cap today at $2.17 billion, this implies downside potential of 0.3% to 35% depending on final sale price.

Keep in mind that on a DCF basis, TDS by itself would be at or near zero today, given the short-term losses and unclear path to profitability. The value is based on cash from sale alone.

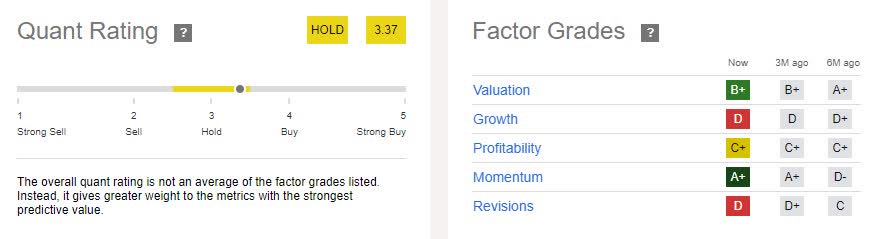

The quant rating is a little bit more optimistic than I am at a hold, but profitability and revisions weigh down the rating, and this is still for a consolidated company with the benefit of US Cellular's profitability.

{kind=link}

Upside Potential

The strongest upside potential is a sale price upwards of $2.5 billion for US Cellular's assets. While all three major telecoms are interested, I still believe there is a limit to how high they will go as the industry struggles and cash flow is challenged. Competition is fierce, and the telecoms are investing heavily in 5G and fiber, which require heavy cash outlay for uncertain profit. As an example, AT&T's cash flow doesn't currently cover both capital investment and investor returns. There is only so far the big three can go, especially for a company operating in a limited geography.

However, if a sale does go through above the estimated range, TDS's stock value could see significant upside potential.

Verdict

Despite the current interest in US Cellular's assets, the potential sale price ceiling and the ongoing challenges in the telecom industry, particularly the heavy investments in 5G and fiber, cast a shadow over the optimism for TDS's stock.

Given its unclear path to profitability and immediate losses, the company's valuation is largely based on the sale prospects. While there is potential for upside should the sale price exceed expectations, the inherent risks and competition in the market, combined with the current state of TDS and the industry, give me significant concern about the future of the business. With that said, I maintain my sell rating at this time, especially for longer-term investors given the recent run-up in share price.

For further details see:

Telephone And Data Systems Is Broken Without United States Cellular