TLSNF - Telia: It's Basically A 7-8% Yielding Telco Bond With Upside

Summary

- I'm heavily invested in Swedish Telia, one of the largest telco operators in the nation. The company has seen significant pricing pressure in terms of valuation.

- In this article, I'll revisit one of the largest Scandinavian telcos, and the thesis to be made for the company going into 2023.

- I view the valuation as a positive one, and I consider Telia to be a "BUY" at this time.

Dear readers/followers,

We'll look at Telia (TLSNF) today. I find this company interesting at this time because it's a very "simple" play - as simple as telco plays get. Essentially, you can summarize the thesis in a few words: "Buy below 30, Sell above 37-38."

Oversimplified, perhaps - but accurate, as I see it. This company is part of the backbone of the Swedish telecommunication network. It has a very attractive yield, coming to a current confirmed yield of over 7.6% for the 2023 calendar year.

In this article, I'll show you the reason why at around 26 SEK native, this one is a company I'm going to "full exposure" to. I always want at least a full 5% in Telia, especially when it's as cheap as this.

Telia for 2023 - the up and down continues

Telia goes up and down. The downside we're seeing here is lower than we've seen before, but it's also natural given the current pressures Telia is actually seeing.

However, the current share price development might give you the impression that Telia is not delivering sales or earnings. This is not the case - it's simply a fact of the company delivering fewer sales and earnings than might be expected. However, this is not to be mistaken for actual good results, which I do believe Telia has posted.

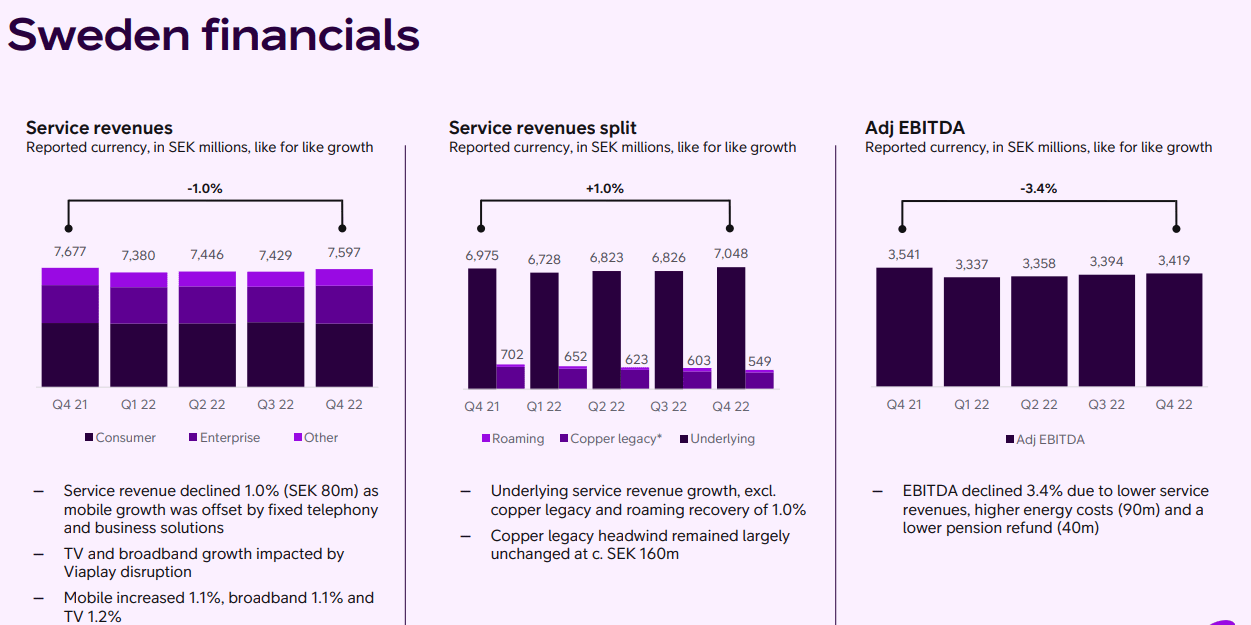

For 4Q22, sales revenues increased by 2.1% YoY, which came from improvements across all units , and the company's transformation continues in line with its estimates and plans. Macro has been brutal, but we as investors shouldn't mind this, knowing the underlying quality of what we're investing in. The bottom line from Telia is still relatively heavily impacted - we're down 1-2% on EBIT/EBITDA level, much due to energy costs, and SCM constraints.

The issues for Telia can be summarized as supply chain constraints, elevated inventory levels, as well as a significant near-20B non-cash impairment due to higher interest rates. All of these factors are working in concert to push this company down to levels that I don't view the company as being justified to trade at.

Telia didn't report as solid revenues as Telenor (TELNY). The trends here are not as good.

{kind=link}

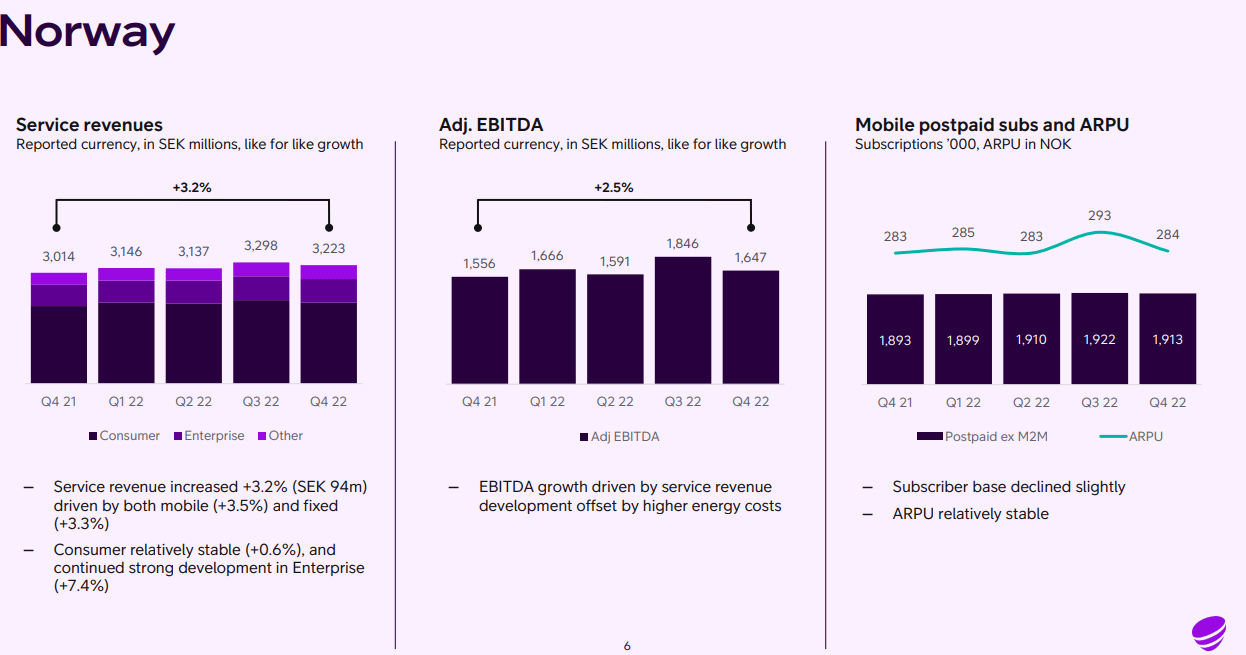

The company also has a substantially different mix in terms of sales. However, while EBITDA declined, so did operating expenses, and the company's leverage at 2.53x is at the level of peers, or even better than peers here. For the dividend, the company has confirmed the 2 SEK level, which is only slightly below what the company paid last year. Finnish numbers are better than Swedish, but on the whole of it, it wasn't the greatest sort of year for Telia, even if the company managed to hold its own and not lose too much to churn or other costs during a difficult time. The Norwegian geography is being missed out on here, because results here were actually very solid.

{kind=link}

Unlike Telenor, Telia doesn't have attractive, ancillary third-world markets anymore. Those failed, and Telia mostly had to pay through the nose to get out of them. That's also part of the reason for the very negative share price trend you're seeing when you look at Telia.

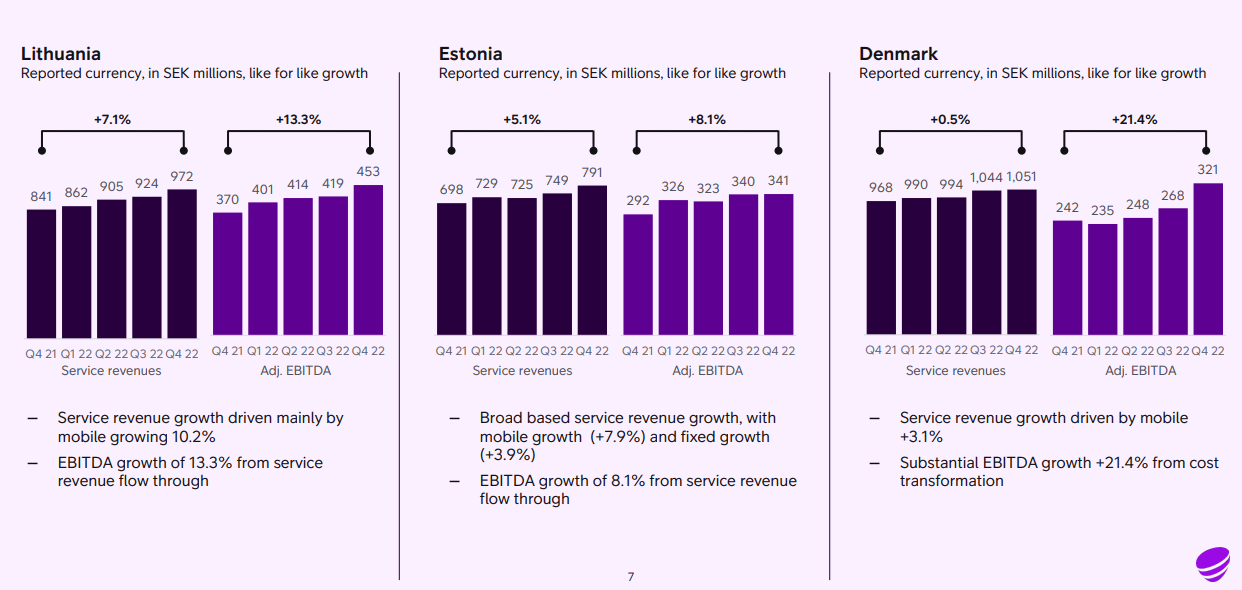

As of now, Telia still has working and profitable operations in the Baltics - and those are working quite well. What's more, they're profitable and growing quite a bit.

{kind=link}

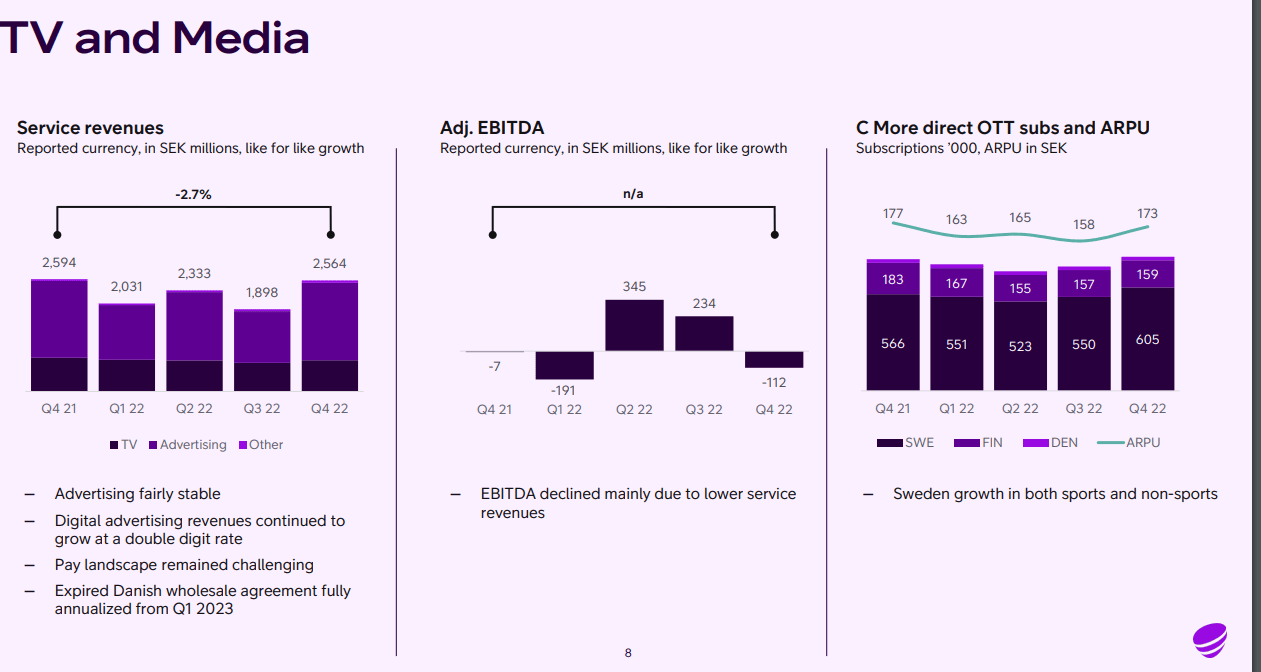

The reason I like Telia the least out of all my Scandinavian Telco is the company's, as I see it, wrongful move into TV and Media. I am of the opinion that an ad-driven, volatile media/content segment has no attractive synergies next to infrastructure-driven telecommunications. It might sound like the two are closely related - but history with telcos like AT&T ( T ) has proven that this is difficult to actually manage to pull off.

TV & Media this quarter shows us why I'm fairly conservative with such things, and why I don't necessarily see this as a good idea for a telco to go into. It doesn't mesh well with the conservative nature of infrastructure cash flows.

{kind=link}

Highlights for the quarter include a more efficient organization, that despite lower pension refunds, manages to work at lower resource costs, including lower marketing, spending, and lower travel expenses and the like. Most of the company's expenditure numbers are presented ex-energy, as is the trend now due to the high energy costs - but lower resources and savings in the IT sector nonetheless are positive here.

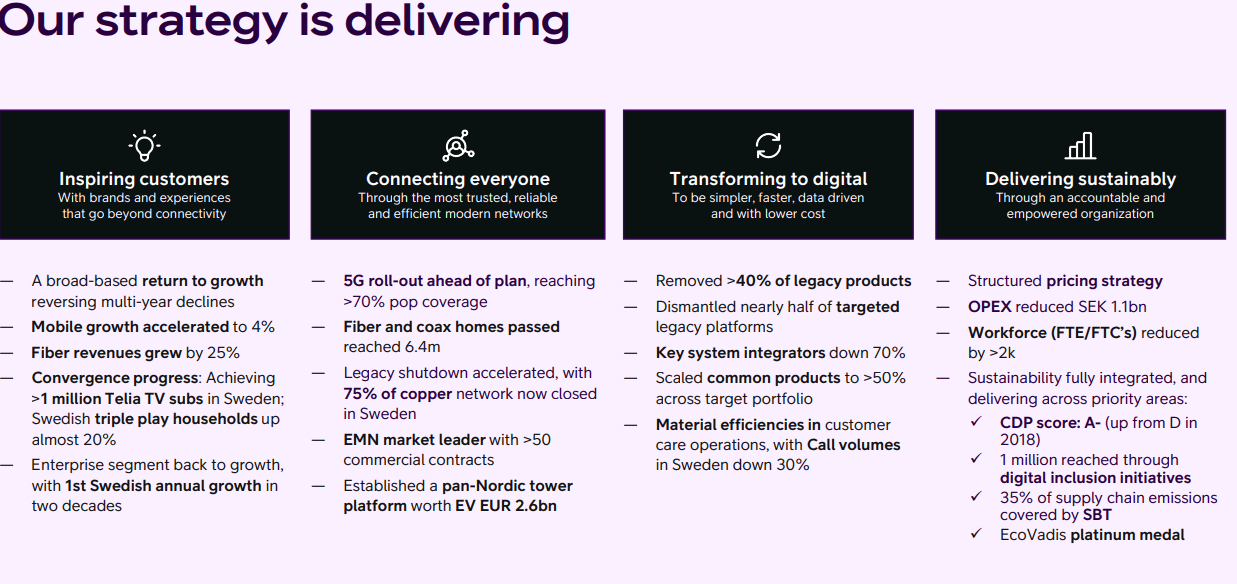

What I view as mostly positive here is the company's ongoing transformation strategy. The CEO in charge is the woman, Allison Kirkby, that managed to turn around Tele2 ( TLTZF ), which is the reason I have a fair bit of faith in what we're going to see for Telia going forward.

The strategy is already delivering "dividends" here.

{kind=link}

However, the company's problems that we've been seeing are more or less exactly as I was expecting. The pay-TV landscape is a competitive and complex world, and hard to monetize - as virtually all non-leading streamers have found. Inflation and SCM are ongoing, and interest rates are challenging the ways that Telia's vendors and financing programs work, as there is a limit to the sort of interest rates consumers will accept.

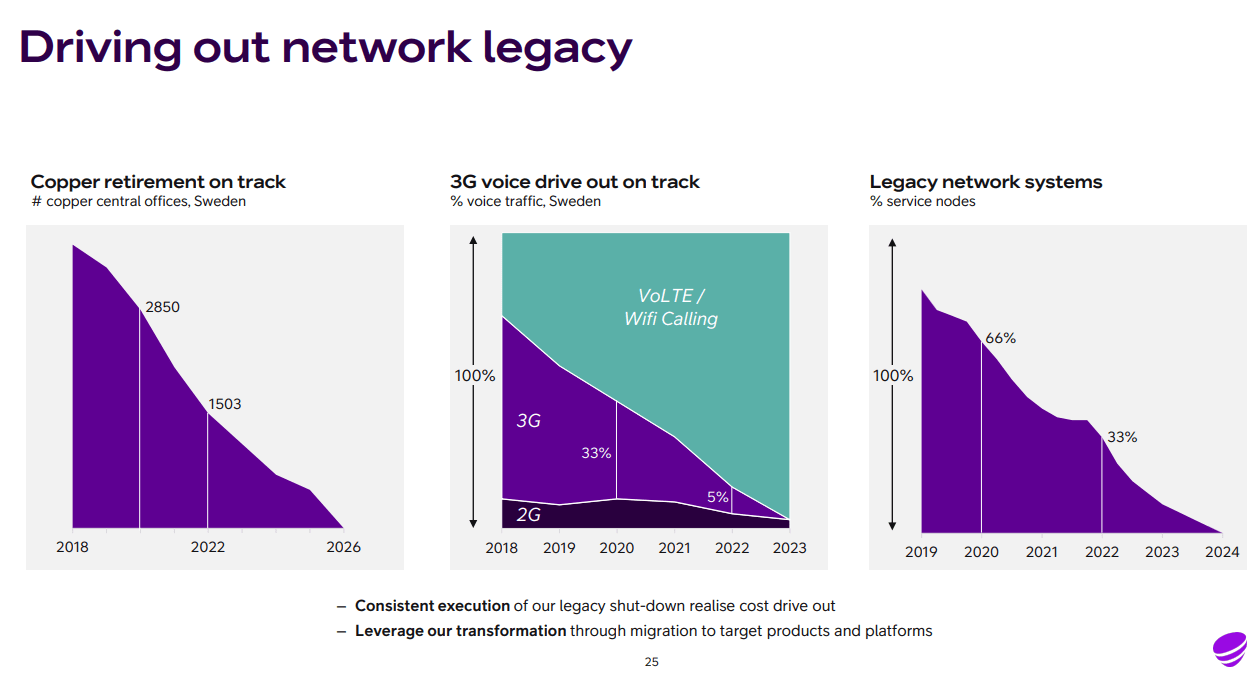

Still, Telia remains ahead in the modernization of the infrastructure and networks, with a leading overall network position in most countries. This, I believe, is what in the end will allow Telia to recapture somewhat more normalized, higher valuations and fair values here.

The company is busily working to phase out its legacy systems...

{kind=link}

...and like many companies, is increasing the overall efficiency of its workforce. Overall, I would argue that Telia is in a very good position and valuation going into the fiscal of 2023.

Telia Company is the largest telecommunications operator in all of Sweden. It provides a mix of services to customers across the country, as well as select other markets, both core, and growth. A relatively low indebtedness and a strong, near-40% government stake comes in and complete the picture we're seeing here.

Let's move to company valuation and the biggest argument for why Telia is a "BUY" at this time.

Telia - The company valuation

As things stand now, the valuation for Telia is extremely positive, with a great overall upside to go by. The overall analyst forecasts for this company remain elevated here. 19 analysts follow Telia, and they go at around 30 SEK/share, down from around 38 SEK back in September of last year. This shows you the degree of overreaction that I believe Telia is being subjected to here.

The range goes from around 22 SEK low to around 44 SEK high - a massive range, truly. Half of the analysts believe Telia will outperform, and the other half that it will underperform. I've rarely seen such a split coverage of a business such as this one.

The reason I am so positive about Telia is the underlying qualities of the company's infrastructure and cash flows. I call your attention to the GAAP and forecasts that are relevant for Telia here and going forward. It's likely that these earnings are going to remain strained for the foreseeable future while the company gets "its house" in order. However, Telia has shown us that the dividend won't go below the "floor" level of around 2 SEK. At these valuations, this is a very attractive overall level of dividend.

Furthermore, the company compared to any and all peers Telia have is cheap. This is even compared to Tele2 and Telenor, and more to other Scandinavian peers.

So with comps and analysts of the same mind at today's share price, how does Telia line up when it comes to things like DCF and the like? Well, quite positive here as well.

Applying a double-digit discount rate and a terminal growth rate at GDP level or slightly below, we get a range of fair value starting at 26 SEK and going all the way up to 35 SEK. Those are some fairly extreme ranges, but we can narrow this down by accounting for the safe yield, and the safety of the company overall, which leads me to go to at least 33-34 SEK in terms of a DCF share price target.

The upside for a fair value of this level is above 14%, which is a high overall upside. When combining this with a 7%+ yield, you can see that the potential upside is well over 20% here and that with investing in Sweden's most significant owner of infrastructure.

Telia, Tele2, and Telenor has always been a sort of "trifecta" to me. I own significant stock in all of these companies, and I'm actually green in all of them except Telia due to the massive dividends these companies have paid over time. What's more, I fully expect these companies to appreciate and revert back to more normalized levels, which would bring their respective RoR to well over 30% each, once normalized.

Telecommunications is a non-optional sector in terms of infrastructure. Everyone needs it. While we're currently in a downturn due to margin pressures from inflation, cost increases, and excessive Capex as a % of sales, these things will revert with time. I believe those that haven't invested in telecommunications, at the time, will regret this deeply.

In the end, it's a "quality for cheap money" argument - and those are the types of investments I love doing. It doesn't matter a whit to me how long it takes for the normalization to occur. I'm happy taking the dividends and buying more in the meantime.

In fact, I recently bought another 0.5% in Telia as it touched 26 SEK.

So, this is my thesis for Telia going into 2023.

Thesis

- Telia, together with Telenor and Tele2, are Scandinavian-leading telecommunication businesses. Telia is by far the cheapest one of these at this time and is yielding over 7.6% with a covered yield that's already been confirmed for this year.

- I believe at this valuation, the company has a massive sort of upside, and should not be underestimated. I view this company as a "BUY" here.

- My price target for Telia is 35 SEK - specifically, I believe anything below 30 SEK is a "STRONG" Buy, and anything above 38 is where you should start pruning your position.

Remember, I'm all about : 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Telia fulfills every single one of my criteria, making it a clear "BUY" here.

For further details see:

Telia: It's Basically A 7-8% Yielding Telco Bond With Upside