TLSNF - Telia: The Upside May Be Far Off But It's A Solid Yield

2023-04-26 16:23:15 ET

Summary

- Telia is a relatively large holding in my portfolio - over 3% at this time, and I've added to it as the company dropped.

- Telia is typically a fairly simple investment - Buy below X, sell above Y. However, for the time being, I see it likely that we'll stay below 30 SEK.

- Telia has some near-term pricing challenges that will take some time to get away from.

- Until then, however, the yield of over 7.5% makes this a very serviceable income investment - and that's what I use it for. An income investment with a massive upside.

Dear readers/subscribers,

Since my last article, Telia ( TLSNF ) has actually outperformed the market - if only slightly.

Telia Article (Seeking Alpha)

I've been very clear on how I see Telia in 2023 and for the next 1-2 years. It's the equivalent of a higher-yielding bond - over 7% is what you get here annually, and that yield is well covered. My approach for Telia has been simple for many years - simply "BUY" below a 30 SEK share price, and once it goes above 36-37, it's time to look at how long you want to keep it. This may be somewhat simplified, but it's a strategy that's worked very well for me.

It's time for a quick update on this company, to see what we've got going for us here.

Telia - Let's look at the upside again

Telecommunication companies haven't been the most popular sort of investment for some time here. The companies, including Telia, have been declining over the past few years due to increased interest rates, churn, and 5G rollout costs/CapEx. Telia compounds this issue by also being a content creator, a combination I'm not a big fan of. That's also why this company is the smallest telco holding I currently have, compared to things like Tele2 ( TLTZF ) and Telenor ( TLSNY ).

A few things out front that I haven't been excessively clear on previously. Telia is actually one of the lesser-profitable businesses in the telco segment compared to other relevant companies. However, it's financially safe, and it's with little doubt, one of the most undervalued telcos in all of the Nordics. With Tele2 back above 100 and Telenor back above nearly 130, we've seen some significant recovery for both of these companies.

So, Telia is not the best, the most profitable telcos out there. Many telcos outside of Sweden are better capitalized. However, it's also one of the few companies almost majority-owned by the Swedish state. As things stand, over 43% of the company's voting shares are owned either by the state, or Telia itself. Aside from that, it's a mix of institutional investors from various geographies around the world.

The company also owns one of the best infrastructures in all of Sweden, and despite challenges, recent results more or less confirm the through-cyclic upside. Revenue growth is good, EBITDA was somewhat down, but churn was manageable.

{kind=link}

Mind you, Telia didn't report as solid revenues as Telenor ( TELNY ). The trends here are not as good. For the dividend, the company has confirmed the 2 SEK level, which is only slightly below what the company paid last year, which is what we want to see for Telia - that high dividend compared with the potential for double-digit upside, which allows the market outperformance not this year, but over the next 2-4 years. That is why I own over 3% in Telia.

Remember, and as I've written before:

Unlike Telenor Telia doesn't have attractive, ancillary third-world markets anymore. Those failed, and Telia mostly had to pay through the nose to get out of them. That's also part of the reason for the very negative share price trend you're seeing when you look at Telia because things are down and are going even lower. The 5-year trend is negative at a 37.2% RoR.

(Source: Telia Article, Seeking Alpha)

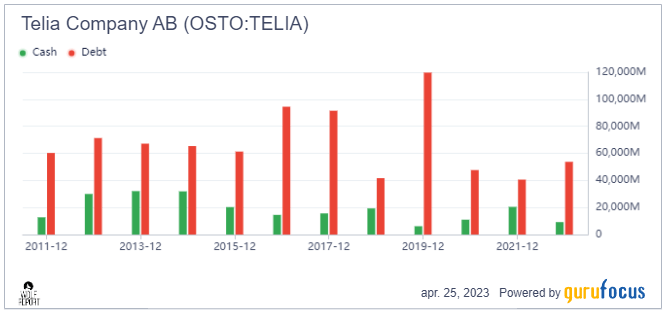

However, the company has been able over time to cut back on a lot of debt.

{kind=link}

The company remains primarily a Swedish business. 46.4% of operating revenues are Swedish, around 18.7% for Finland, 16.5% for Norway, and the rest in a mix of other nations.

My main issue with Telia is, to put it frankly, that the business for a long time has been very poorly managed. The company's management has failed to create shareholder value for several years. Generally speaking, faith in management has been lacking - at least until the new CEO, Allison Kirkby took the reins. This is the woman that turned around Tele2 and turned it into a cash-minting machine to where I have received massive dividends for several years. I don't usually invest only based on management - and I don't do this here either - but it's definitely management-dependent to a degree here.

I also see improvements in company trends that give me hope for the future - aside from the valuation. Remember, Telia has been in its transformation phase, or within its strategic roadmap for over 2 years at this point. They've managed to reduce churn, and despite my dislike for content, they've managed to aggregate user services including things like C More, HBO, Netflix, Cloud, and 5G+. The company's 5G network is now available to more than 70% of the Nordic/Baltic population, which is impressive.

What I am most interested in is how Telia intends to fix its cost problems - inflation, rising energy costs, and other issues. While revenues are up and adjusted for energy costs, EBITDA would have actually been up 2.6% YoY which would have been in line with mid-term guidance, this is of course not what happened - because energy costs are actually what they are at the moment.

So, what is Telia doing?

The company is dismantling its legacy faster than before, introducing energy-saving tech for its infrastructure. Overall, the downward trajectory in EBITDA hides how well the company's revenue growth has been progressing, such as Finland being up for the seventh consecutive quarter of growth. Again, excluding energy costs, EBITDA would have been good here as well.

Advertising revenue, if you dig down into results, was bad. But I expected this. As we see macroeconomic downturns, advertising revenues are one of the first things to go as companies re-assess their marketing spend. This is also part of the reason I am not a big fan of telcos mixing content or TV into their sales mix - there's volatility here that is anything but conducive to the stability and income generation that telcos are supposed to deliver.

The company targets further improvements. Ad revenue was actually up 17% if you look at company presentations, but I don't give them much credence for this - this was mostly Tv4 Play. There's too much Pay TV in the mix, and as expected, this not only dragged things down to flat, it went negative as a whole, and Pay TV remains very challenging. The company now targets a full C More integration into TV4 by the end of this fiscal, and this is something I view as positive.

As you can see here, there are plenty of risks to consider in the mix going forward. The one positive we can really ascribe to Telia is the stability and state of its infrastructure, which is second to none in all of the Nordics. Telia maintains one of the best coverages, especially in rural areas out there. I use the company's services on the corporate side, and I'm very pleased both with performance and on the customer service side (and I'm a demanding customer).

However, I don't see any immediate or massive improvement in the company's near-term future. CapEx due to the ramp-up will remain high. FCF was poor - down over 70%, and likely to remain down due to NWC, Cash CapEx, and continued inventory turnaround challenges because again - macro. Net debt is up slightly due to lower results as well as negative FX - the weak SEK is doing some companies no favor.

However, on a high level, I'm seeing "sparks" of operational improvements. Transformation to digital is working well, legacy dismantling is more than 50% done, integrations are on track, the rollout of 5G is actually ahead of plan, Fiber and Coax-connected homes are up to 6.4M, a Pan-Nordic tower platform has been established, and the EV of this has been estimated at over 26B SEK, and other targets are working.

I believe that investors who do not buy this admitted average-class telco company may regret this in 2-3 years when we see targets of 35-40 SEK again, and I will be trimming at profits of 60-80%.

Telia 1Q23 results

While this was being written and published, we had time to get 1Q23 results. As this is being submitted, the company is up almost 5% in a single day, touching 28 SEK native share price. The reason for this is as follows.

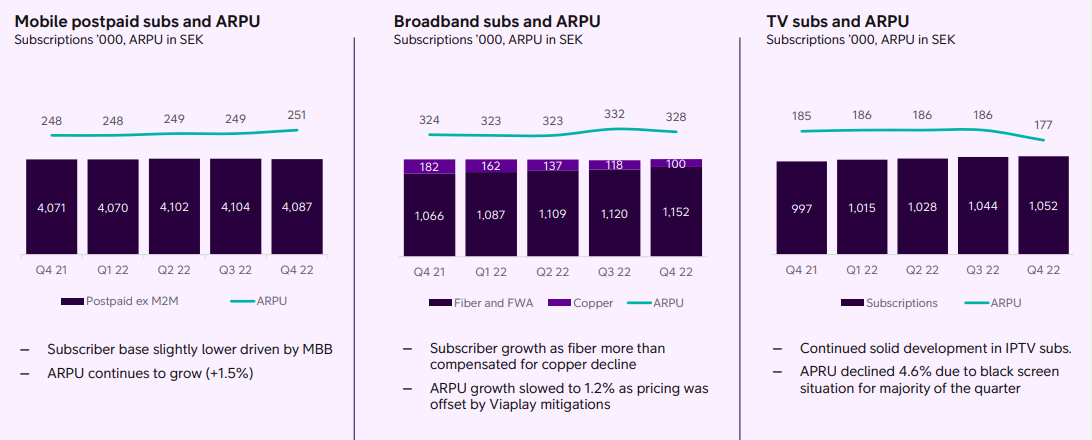

Many of the things I touched upon above, in terms of strategic goals being hit, are seeing more and more positive indicators. For 1Q, this came in the form of service revenue and mobile revenue growth. Revenue growth is actually accelerating for Telia, with a 2.4% overall LFL growth, while adjusted EBITDA is finally back to growth at a 1.6% YoY growth rate.

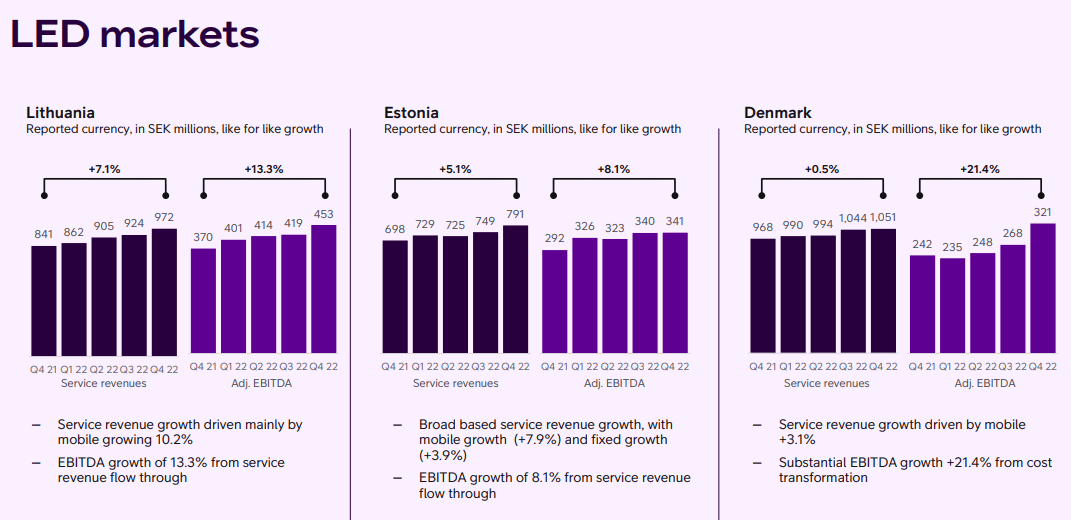

The LED markets, meaning Lithuania, Estonia, and Denmark, are continuing to drive higher growth rates - double digits in some cases here as in 4Q, so also in 1Q23.

{kind=link}

The company continues to check off strategic check marks, such as increasing its 5G coverage, and was recently awarded, in Finland, as the best quality network in the world by Opensignal. Telia is also ranked 1st by the FT among climate leaders, which showcases the company's progress in its qualitative infrastructure portfolio.

To put it simply, as of 1Q23, Telia expects all metrics to improve for the full year. The company also has finalized its agreement to divest Telia Denmark to further focus its ambitions, for proceeds of about $1B. This payment corresponds to around 8.9x EBITDA, which can be compared to Telia's own current valuation of less than 6.5x EBITDA. This is still subject to regulatory approvals, but Telia expects this to close within 12 months at the latest.

Proceeds?

Forget extraordinary dividends - the cash will be used to delever. As of 1Q23, the company had slightly over 75B SEK in debt net of available cash. Cutting it by another 10B SEK would lower this close to the 65B SEK mark, which would be below 2.3x net debt/EBITDA.

None of the operating geographies really posted any surprises or superb numbers. It was all mostly stable - but a reversal to positive, which I have been expecting for some months. given that I bought a slew of shares below 26 SEK, I'm happy with the solid growth I'm getting here. Furthermore, Telia also confirmed the 2 SEK dividend. At 28 SEK, this is still 7.1%, which is still excellent.

TV, which has been the black sheep for a few quarters now, is still problematic. Pay TV revenues have stabilized for the time being, and digital ads are still growing, but EBITDA is still down due to content expansion. This constant battle for content and expansion is part of why I believe that these content operations have nothing or very little to do with a solid telco. It is by far the largest negative and risk about Telia, despite a nearly 10% increase in ARPU due to price increases.

The company's cost cuts aren't going that well either. While resource costs are lower, other costs associated with IT and travel are actually up. Telia now acknowledges the transformation agenda for costs remain, but acknowledges its challenges here.

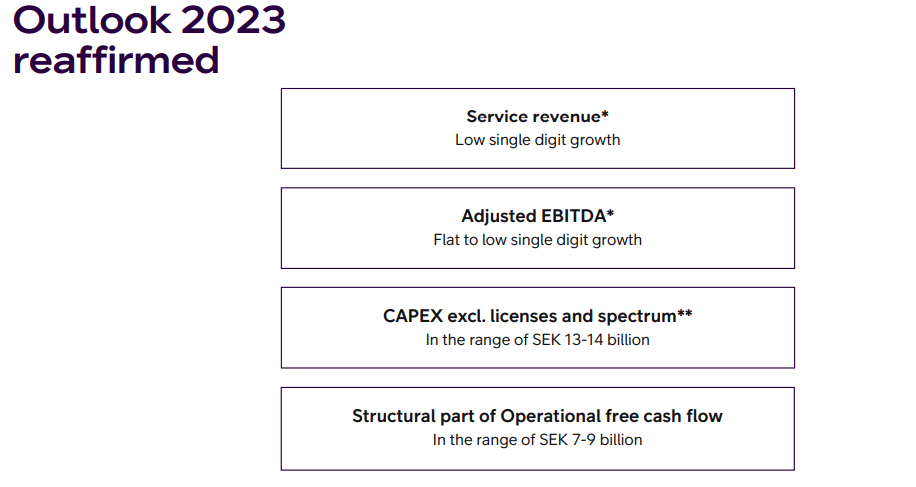

CapEx, at the very least, is down and expects to be continuing to go down, with an expected 13-14B SEK worth of CapEx for the full year.

{kind=link}

Let's look at valuation.

Telia's Valuation - bottom-level, no matter how you slice it

The company's ratios, nearly all of them, are close to their 10-year lows. For Telia, this means they are very low because Telia hasn't been on the stock market for much longer than that. You know how it works in behavioral heuristics and some of the fallacies and biases here. I argue that Telia's current pattern of declining further and further can begin to go into the recency heuristic, wherein people give far too much weight to an event happening again - Telia going even lower if it recently has happened. In this case, I believe the underlying trends for the company are being disregarded, in combination with the less-than-cheap valuation we have here.

To stick to a negative view of Telia here, you have to make the following argument or stick to the following stance.

A Telco like Telia is worth less than 1.5x sales.

And I'm not talking about it being valued at 1.45x - I'm talking about Telia actually being lower than 1.15x when it's typically valued close to a mean of 1.9x, a high of 2.52x, and a low of 1.09x historically.

You also have to value it at less than 6.5x EBITDA and call it fair, as well as less than 2.2x revenues. All of these very basic trends are numbers where I would say that these are clearly too cheap if the company has any sort of improvement potential. Based on the transformation program, the goals the company is hitting, and underlying improvements, I say that this is likely. GAAP-equivalent EPS hit negative in 2022 - I believe this will normalize in 2023 already. I expect Telia to generate around 1.2-1.3 here. This puts me below S&P Global where the average forecast is around 1.4. Beyond 2023, things become hard to forecast - but I believe expecting the company to manage that sort of level is fair - and this is not a forecast I am alone in having.

Telia Forecast (S&P Global/TIKR)

{kind=link}

If these forecasts hit close to home, and that 7% yield is something that is "safe" and covered, I do not believe an upside to 35 SEK is outlandish. 35 SEK also happens to be my most recent PT, although I'll reiterate that anything that begins with a "2" in the native ticker is something that should really grab your attention. At that valuation, you're not quite buying the company at less than the value of its tangible book, but you're getting close to it, with the LTM P/B on a per-share basis down to 1.6x compared to a high of over 2x.

Telia isn't the best nor the most profitable telco out there. But with Telenor and Tele2 up, if I had any room to grow my Telia position, the realistic upside here would see me do that. Even at a 15-17x P/E on a forward basis, the company's implied share price based on current estimates goes to 33-37 SEK, and if you heed the company's normalized 20x P/E premium that goes up to over 40 SEK/share. Even net of the dividend , that's more than 55% total RoR.

That is why my thesis is as follows.

Thesis

- Telia, together with Telenor and Tele2, are Scandinavian-leading telecommunication businesses. Telia is by far the cheapest one of these at this time and is yielding over 7%+ with a covered yield that's already been confirmed for this year.

- I believe at this valuation, the company has a massive sort of upside, and should not be underestimated. I view this company as a "BUY" here.

- My price target for Telia is 35 SEK - specifically, I believe anything below 30 SEK is a "STRONG" Buy, and anything above 38 is where you should start pruning your position.

- I can't buy more due to my exposure, but I would if I could.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Telia fulfills every single one of my criteria, making it a clear "BUY" here.

For further details see:

Telia: The Upside May Be Far Off, But It's A Solid Yield