T:CC - TELUS: Disappointing Returns Questionable Allocation

2023-06-20 12:38:10 ET

Summary

- TELUS is suffering from poor capital allocation decisions due in part to its industry and its management.

- Competitive pressures could put pressure on TELUS' ARPU.

- Recent acquisitions outside of core business lines have contributed to poor returns on investments and reduce management's credibility as disciplined and focused capital allocators.

Company Overview

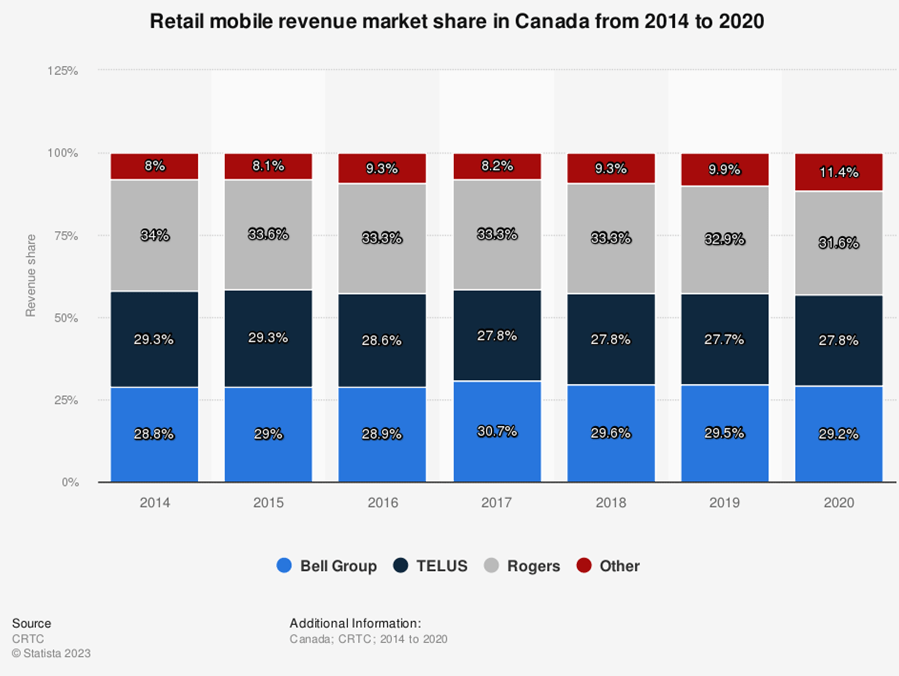

TELUS ( TU ) ( T:CA ) provides fixed and wireless communications network services as one of Canada's "Big 3" telecom. providers along with Bell ( BCE ) ( BCE:CA ) and Rogers ( RCI ) ( RCI.B:CA ). The data below gathered by the Canadian Radio-television and Telecommunications Commission ("CRTC") shows the market share progression up to 2020 and the current pluropoly:

{kind=link}

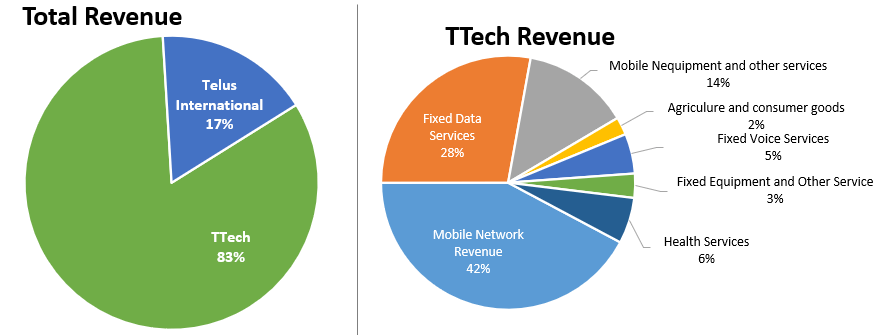

Its reported business segments also include TELUS International ( TIXT ), which was recently spun-off and publicly listed as a separate entity. As TELUS still remains its majority shareholder, that unit's results are consolidated. Here is a segmented view of their revenue as of their last fiscal year-end:

{kind=link}

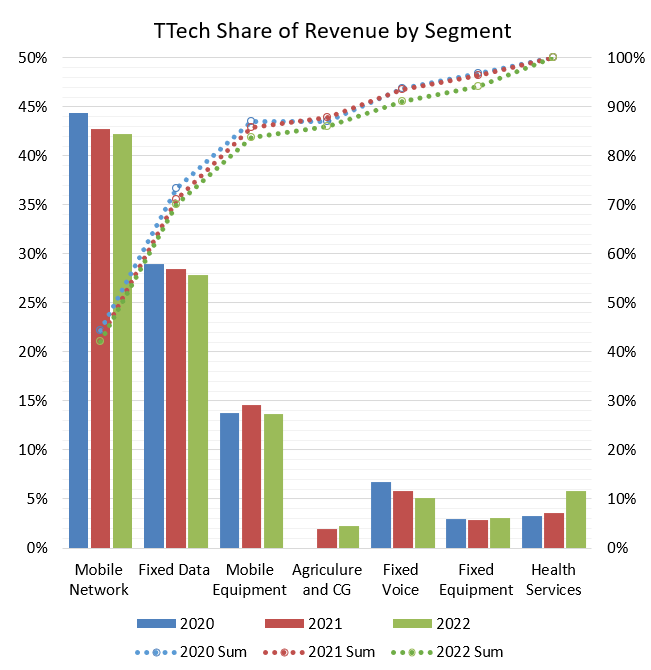

TELUS' revenue is by far driven by its Fixed Data (Internet, TV, Security) and Mobile Network (mobile plans, not including devices) segments. While these two largest segments slightly decreased over the past 3 years in terms of their share of total revenue, the change has not been significant:

{kind=link}

The reason behind my negative rating of TELUS is based on multiple factors which I'll be exploring:

- Competitive Dynamics

- Growth through Acquisitions Strategy

- Falling Return on Investments

- Capital Structure Approach

New Competitive Dynamics

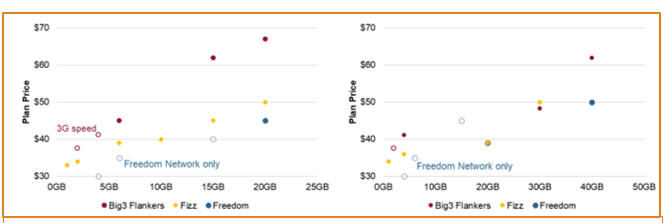

Low-ARPU mobile plans are becoming more common, and while discounts are common, the fact that deep discounts have been matched by the Big3 brands, and not only their flankers, since April indicates that we may be entering a period of elevated competition on the basis of plan price (or value).

The figure below shows Fizz and Freedom Mobile's ( QBR.B:CA ) plan pricing were far below the previous-standing ARPU of the Big3 but that they've nonetheless been matched:

Wireless Prices in April (left) and May (Right 2023) (Market Data)

{kind=link}

This aggressive pricing response is not a change in strategy shared by all three but rather seems to be in response to changing customer preferences. As all three focus on customer acquisition, this has required adapting to the fact that, according to a 2022 consumer survey , a larger importance is placed on a mobile plan's value than anything:

Deloitte

We can see the sensitivity of customers to pricing even amongst TELUS' customer base, which has the lowest churn rate of the Big3 (by 50-100bps):

Company Filings formatted by author

Even if this crude analysis ignores factors such as bundling and provider-specific satisfaction, the apparent correlation between ARPU and mobile churn (lower churn = lower ARPU and vice-versa) makes it clear that despite having the stickiest customer base of Canadian TelCos, pricing also seems to be the key driver of customer retention.

If we expect lower ARPU to be the direction the industry is headed for, we should highlight some factors specific to TELUS' products and network which could afford it an advantage, limiting subscriber losses and ARPU dilution relative to competition.

These factors include bundled ancillary services such as TELUS security, health, Internet or TV, which, if subscribed to in addition to mobile, decrease subscriber churn, increase pricing power for TELUS, and reduce the importance of pricing in customer's decision to switch. In those cases TELUS feels its large offering of services offers it a leg-up of low-price competition.

We'll discuss in the next section how acquisitions have fed into this bundling strategy, but we'll first consider if TELUS' fiber and 5G networks, which account for the lion's share of their last 5-year physical investments, could offer them a lasting leg-up on competition.

Possible Fiber Leg-Up

Fiber networks certainly matter to internet customers. Looking at the share of net adds (new subscribers-lost subscribers) by region, we see that TELUS (which has its Fiber Network in Western Canada) dominates gains in the West whereas Bell (which has its Fiber Network in Eastern Canada) dominates Eastern market share gains:

Net Add share Western Canada (left) vs. Eastern Canada (right) (CRTC)

As none of the lower-priced or flanker brands can offer and bundle fiber and wireless, and that not all Big 3 have a geographical overlap in wireless and fiber networks (ex. Bell not able to compete on fiber in Western Canada), competition for this offering is reduced, increases TELUS' competitive advantage in a way that matters to consumers, and therefore limits pricing pressure and churn increase risks.

Possible 5G Leg-Up

This network advantage is the one I'm most doubtful of translating into a sustainable market advantage.

First, recall from a figure above that 5G ranked below plan value in customer's mobile provider switching considerations. Even more, we can approximate that at most 7% of Canadian smartphone users are more often on 5G networks than LTE etc. from the following:

- 1 in 5 Canadian smartphone users have a 5G device ( Ericsson 2022 )

- ~30% subscriber market share per Big3 player ( CRTC )

- Only 30 to 40% of users with 5G devices and 5G providers are most often on 5G ( Statista )

This is assuming at low-cost "flanker" brands that belong to the Big3 offer 5G networks, which isn't the case for the overwhelming majority.

The large gap between availability and use demonstrates clear lack of consumer enthusiasm for 5G offering. After so much investment, I would say the customer interest is disappointing, that they are willing to take it if offered but will not chase the network upgrade.

In fact, that same 2022 study from Ericsson referenced above concluded that:

Of the 1 in 5 who already have a 5G smartphone in Canada, the majority are not yet on a 5G subscription and need proof of the value 5G brings before making the upgrade.

This passive customer is not what you're looking for after investing billions in a network; as of now it offers any of the Big3 little pricing power, even less considering that the competitive field is shifting in favor of lower priced competition.

As of now, I don't see TELUS' 5G network as a competitive leg-up given that the other Big3 are at a similar stage of development of their network, and that the customers who switch are more likely to do it for the sake of pricing. In a case with equal plans between TELUS and a flanker, the only difference being 5G, I expect the price sensitivity of customers to be very high in favor of the flanker.

Eventually 5G could be offered by all; TELUS will only find itself on par with competitors after having been unable to monetize its investment when it had the lead.

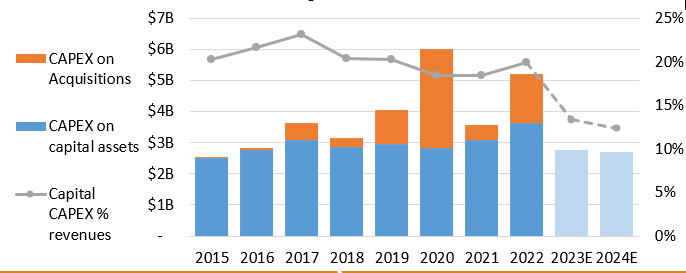

Growth Through Acquisitions

In addition to the capital expenditures on fixed network assets, TELUS has been investing in growth segments, such as health and agriculture, through acquisitions:

{kind=link}

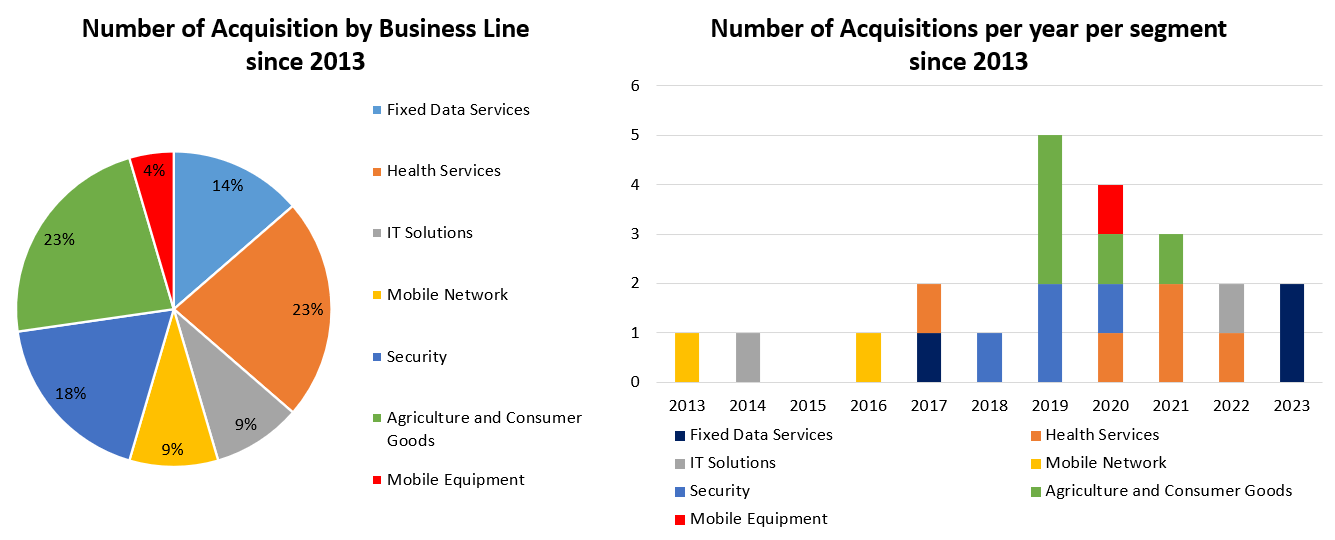

The large acquisition outflows over the past decade, and especially in the last 4 years, has been directed at non-core business lines, namely Security, Health and Agriculture & Consumer Goods:

{kind=link}

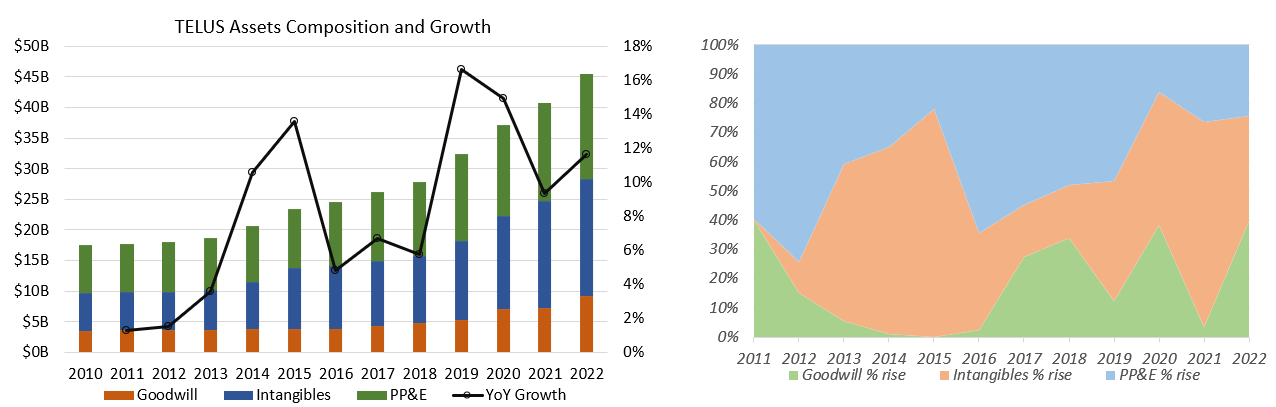

While TELUS does not disclose most of the purchase prices for its acquisitions, we can see that more of the rise in assets over the recent years is accounted for by Goodwill and Intangibles instead of fixed assets.

The chart on the right below shows that an increasingly large part of TELUS' annual total assets increase is due to non-physical assets. I expect most of these Goodwill and Intangible asset recognition to come at the time TELUS acquires companies.

{kind=link}

The lack of physical assets by itself is not a bad thing; after all, TELUS is venturing into some new business segments that may structurally differ in their typical balance sheet composition. However, goodwill cannot be mistaken for anything else than premium paid over book value in acquisitions.

These assets could represent a drag on TELUS' returns on investments if they add to the bottom-line of return metrics but produce little top-line profits growth. We'll return to the decision to retain earnings in the capital allocation section, but we can surely determine at this point that once the decision to retain was made, these acquired businesses are a definite drag on profitability.

The company itself recently mentioned in its investor day meeting that if it were not for its smaller segments of Agriculture and Health, its operating margins would be well into the 40s; they are currently around 38%. Remember that the two segments included represent together less than 10% of revenues and have been where most acquisitions by value have been concentrated. They are therefore generating huge losses.

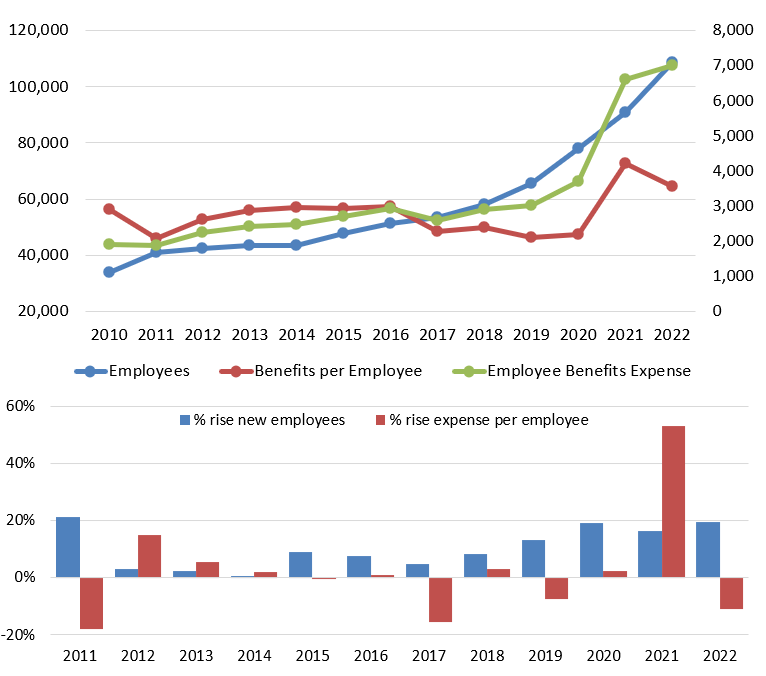

One reason why these businesses are hemorrhaging cash are their payroll burdens; in what seems to be a clear result of acquisitions (as per annual filings) TELUS' overall employee number and benefits per employee have significantly increased:

{kind=link}

Given that we've not seen employee numbers net reduced post acquisitions, the acquired business seem to be inefficient due to industry design or lack of scale. Either way, it is difficult to see how loss generators like these, in business lines whose links to telecom are questionable, have their place in TELUS' capital allocation strategy.

In typical corporate-speak, management touts the synergies between these business units and its core telecom products and services. Security is a clearer link through its acquisition of an established player (ADT) to add a residential service that is extremely sticky, decreasing churn and increasing household revenue. For Health and Agriculture, I personally do not see a material connection that justifies either the acquisition or the current large losses generated by both.

In a relative performance game, you'll hear TELUS management discuss how compared to Rogers' and Bell's investments in media, they feel their non-core ventures are wiser. But capital allocators shouldn't evaluate decisions relatively, they should evaluate opportunities on an absolute basis. In its current situation, if TELUS plans to bring these business units to profitability and eventually spin them out as they did with TELUS International, they will require even more investment, continue to dilute the profitability, and bring questionable "synergies" to its telecom business (even though they claim such synergies exist).

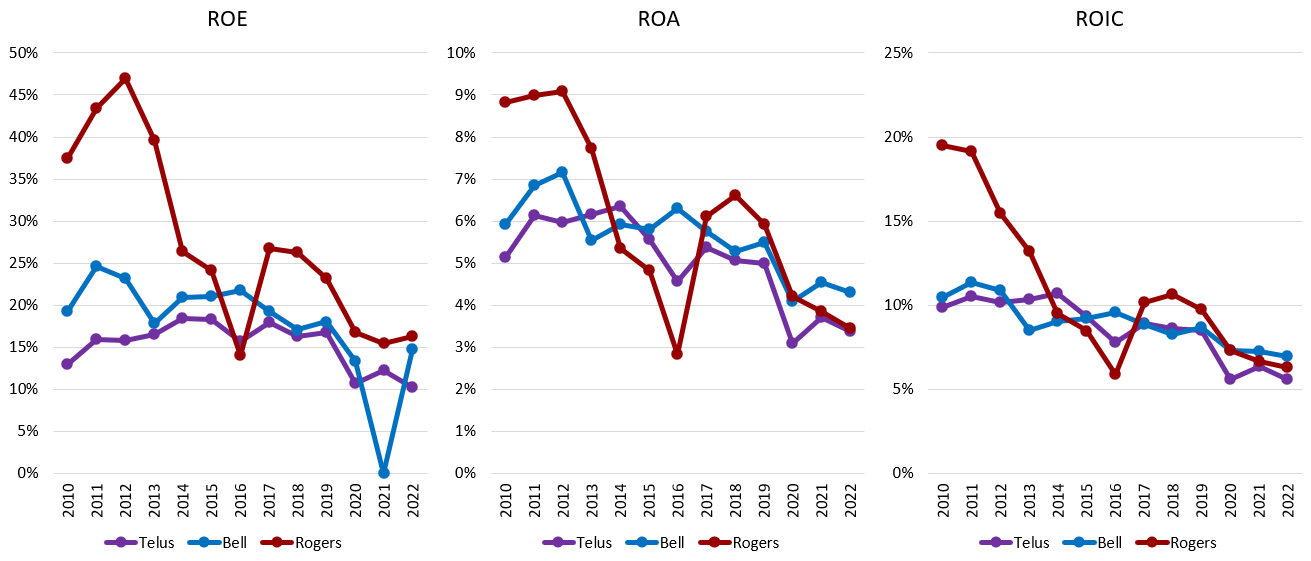

Collapsing Returns on Investment

The simultaneous fall of return metrics across the board hints at a partially structural issue in Canadian Telecom. investments and returns.

{kind=link}

We've discussed possible reasons for this. The top-line has been dragged lower by more a more competitive environment pressuring ARPU and more BYOD plans, as well as more D&A expenses related to heightened fixed asset investments.

The increased equity, asset, and investment capital revolve around the same factors; a lot of retained earnings invested in network assets such as 5G and fiber, and non-core business line acquisitions and investments (Media for Bell and Rogers, and Health/Ag./Security for TELUS).

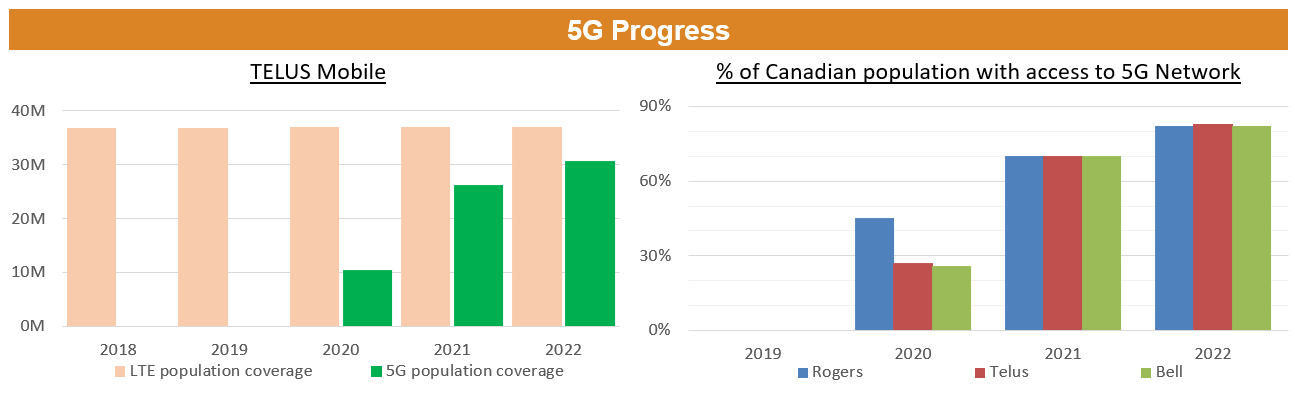

On the 5G front, here are some relevant metrics to measure TELUS's progress relative to its old LTE network and peers:

{kind=link}

While TELUS' 5G network is nearing its LTE coverage rate as Bell and itself have caught up to Rogers' early lead, the coverage metrics on the right are not representative of degree of use by customers; it is more indicative of potential customers. As explained earlier, I estimate usage among mobile users to be at most 7% in Canada, and we've explored why this prevents monetization of fixed investments in 5G.

For fiber progress, we know that TELUS' fiber rollout is complete according to management disclosure. Consumers have been more responsive to this new offering than to 5G, and TELUS' position has been more differentiated, probably not representing as large a share of the drag on return metrics.

Yet we know that the main beneficiaries of this technology are the customers; replacing an entire copper network requires billions of investment, but billions in additional ARPU won't be generated; it will increase ARPU, perhaps reduce churn or slightly mix up market share.

Capital Structure Decisions

Related to the previous points on capital allocation is TELUS' capital structure decisions. Its investments in projects with questionable (so far negative) returns, have led them to a point which far exceeds internal leverage targets.

Company Filings

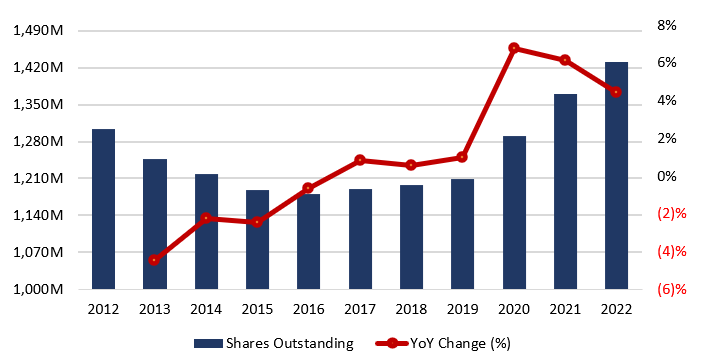

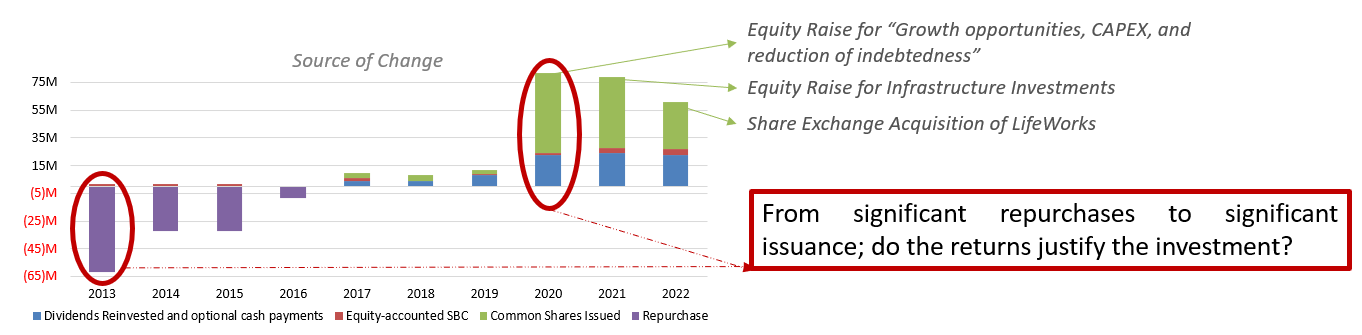

While leverage has been historically steady at this elevated level, investments have not, as management chose to fund projects through equity issuances. As a result, TELUS has gone from being a net repurchaser to, by far, a net issuer of equity:

Net share issuances (repurchases) (Company Filings formatted by author)

{kind=link}

{kind=link}

Equity holders need to ask themselves if they are comfortable with seeing their ownership stake reduced to fund acquisitions; if the value obtained in exchange is accretive to the investor, there is no problem with equity issuances.

However, as I've made clear in the previous points, I do not believe that the funds raised were used for purposes that generate (or will generate over their lifetime) any return justifying the aggressive leverage and issuance.

Some of this is due to structural industry issues (5G and Fibre investments across the board) and some due to non-core investments (Health and Agriculture segment acquisitions).

In any case, recent earnings calls did not feature any analyst questions on the topic of capital structure rationale and allocation, and neither did management stress or outline their rationale or related strategy. I find it therefore even more important for investors themselves to be aware of their approach and to decide if they have confidence in management's strategy.

Conclusion

Given a combination of factors, from the structure of the Telecom industry in Canada to internal capital allocation strategy, I do not have confidence that TELUS is set to generate returns far exceeding its peers or other investment opportunities.

The Big3's decision to first invest heavily in networks to remain competitive, with little ARPU generation, and them seemingly feeling forced to internally allocate to either media or venture, reminds me of a quote by Charles Munger:

You work hard all year and there is your profit sitting in the yard. We avoid businesses like that. We prefer those that can write us a check at the end of the year

I do not feel confident putting my money behind who I judge to be undisciplined capital allocators with little opportunity to reinvest at high rates but a seeming compulsion to retain all earnings.

For further details see:

TELUS: Disappointing Returns, Questionable Allocation