T:CC - TELUS International: Growth Story Breakdown Drags TELUS With It

2023-07-17 12:16:26 ET

Summary

- TELUS International dropped 31% on July 14 and closed near the lows of the day.

- We look at the reset guidance and whether the valuation is getting appealing.

- We examine the parent, TELUS, finally hitting some of our older price targets and see whether we can pick this up.

Note: Some amounts are referenced in USD and some in CAD.

With the markets hitting their strides and many tech indices rallying even more, it is tough for investors to see a stock move down to new lows. TELUS International ( TIXT ) compounded these woes with a brutal 31% down move on its new guidance. Today, we take a brief look at what this company does and how the guidance plays into their valuation. Then we move on and examine the impact on the parent, TELUS ( TU ) a company we have followed and written about for quite some time.

TELUS International

TELUS International is a technology company which provides IT services for global clients.

{kind=link}

Clients include corporations in technology, gaming, communications and media, eCommerce, finance, banking and credit cards, insurance, travel & hospitality, healthcare, and automotive industries.

TIXT

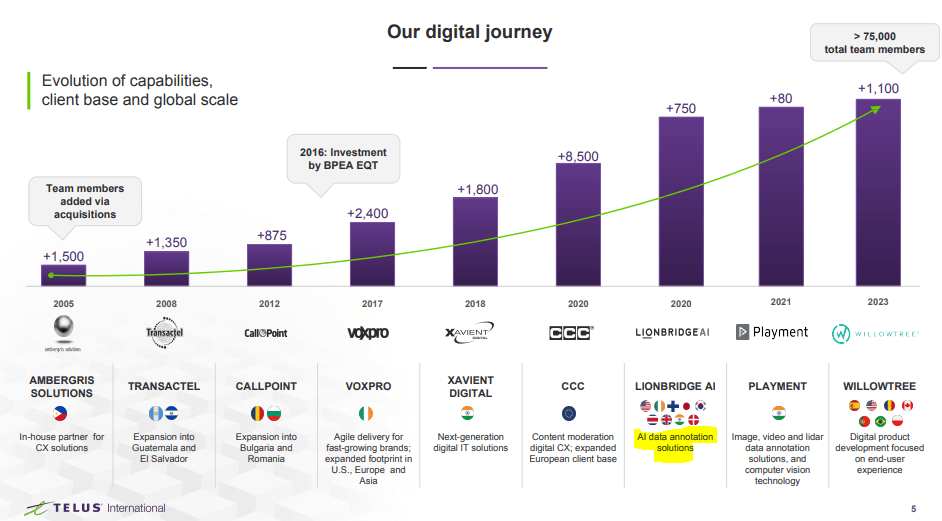

This is a far cry from the regular telecommunications that the parent TELUS is engaged in. TELUS actually started building this side out in 2005 when it acquired a company in the Philippines. The evolution of this company has been fantastic and has been powered by organic growth as well as some big acquisitions like LIONBRIDGE AI.

{kind=link}

That purchase had the two magic letters (A and I) and was done at a time when AI was not actually a craze and also done at relatively reasonable valuations.

Today, TELUS Corporation, announced that TELUS International, a digital customer experience innovator that designs, builds and delivers next-generation solutions for global and disruptive brands, has entered into an agreement to acquire Lionbridge AI, a market-leading global provider of crowd-based training data and annotation platform solutions used in the development of AI algorithms to power machine learning. The acquisition will be at a purchase price of approximately C$1.2 billion consisting of debt and equity, subject to customary closing adjustments. Closing is expected to occur on December 31, 2020.

Lionbridge AI has demonstrated strong financial growth, reporting 2019 revenue of approximately C$260 million, which is up 29 percent year over year, and an EBITDA margin consistent with TELUS International's within the range of 20 to 25 percent. Lionbridge AI's financial performance is underpinned by an attractive business model, long-term client relationships averaging 15 years among its top five clients, and a growing market demand for data annotation services to support the overall increased investment in AI and machine learning. Lionbridge AI has been resilient in the face of COVID-19, and for the nine-month period ending September 30, 2020, the company generated approximately C$230 million in revenue, up from approximately C$190 million in the same period a year ago. Capital intensity for Lionbridge AI is in the low single digits, driving a high simple free cash flow conversion.

Source: TIXT

Those are fairly reasonable multiples for the growth that the company was showing at the time. TIXT however did not show remotely the same discipline while buying WillowTree. They got this at close to 8X trailing revenues .

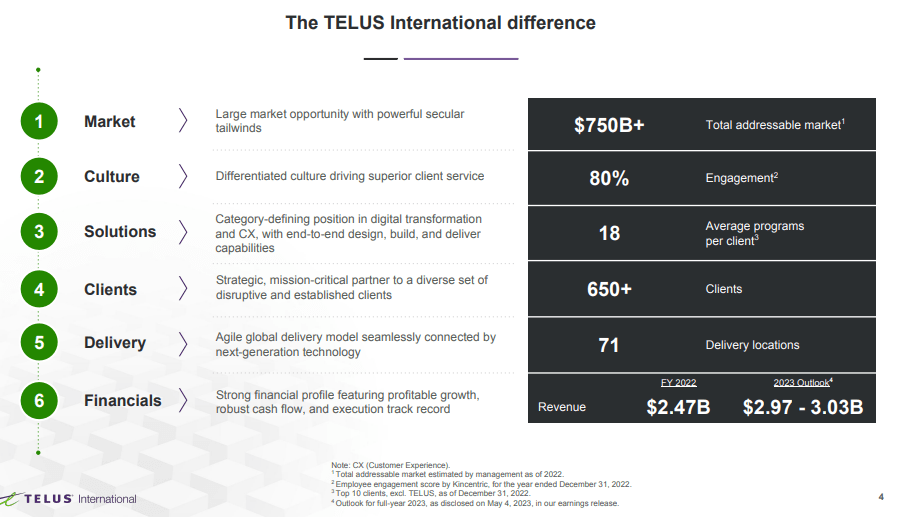

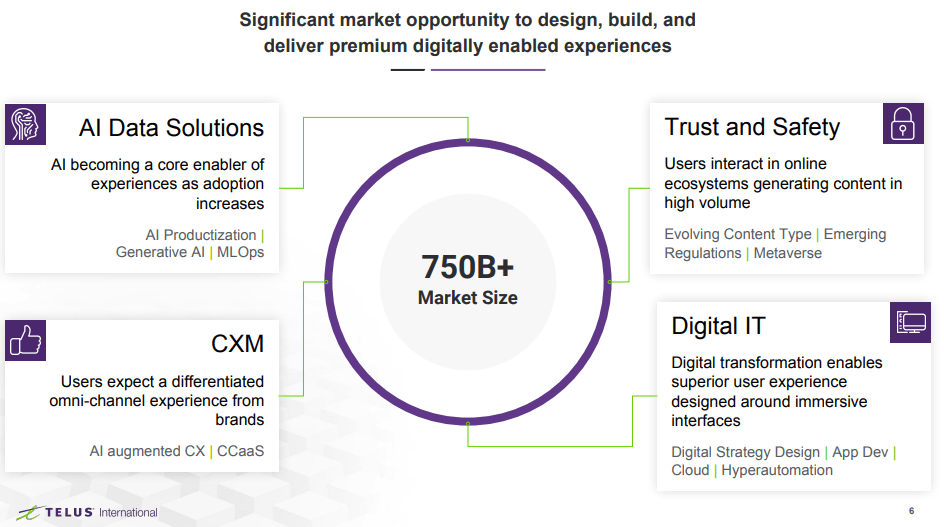

The last presentation of TIXT showed the company guiding for about 20% revenue growth year over year and an addressable market of over $750 billion.

{kind=link}

Of course, the centerpiece of that was AI.

{kind=link}

What Went Wrong?

TIXT guided down to about $2.715 billion for annual revenues, down from almost $3.0 billion.

Revenue in the range of $2,700 to $2,730 million, including $205 to $215 million from WillowTree, representing revenue growth of 9% to 11% on a reported basis, and growth of 1% to 2% excluding WillowTree. This assumes an average exchange rate of one euro to 1.09 U.S. dollars for 2023.

Adjusted EBITDA in the range of $575 to $600 million, and Adjusted EBITDA Margin in the range of 21.3% to 22.0%.

Adjusted Diluted EPS in the range of $0.90 to $0.97.

Source: TIXT

The company cited a challenging demand environment, particularly in the technology vertical and also blamed delays and lower-than-expected activity in new business. This is a huge deal as the slowdown is down to less than inflation rates around the world. Note that we have shown the change in EPS estimates in both US Dollars and Canadian dollars in the next chart.

Outlook & Valuation

Such a dramatic slowdown is consistent with a global recession and cutback in capex. We have already seen the Eurozone declare an official recession. China's growth rates have been struggling, and its property market is in free fall. The technology hub of Asia is telegraphing more serious problems for the sector.

Bloomberg

A longer-term graph shows just how serious the drop is.

Bloomberg

You are going to get a huge pullback and TIXT is going to show more downgrades in the months ahead in our view. Now investors can go "ape" on the AI portion, but there is a lot of competition in this space. A lot of what passes for "AI" like Bots which TIXT develops , has been around for a decade. So investors' primary defense is valuation and not the two magic letters. Here things get tricky, as while there are a legion of comparatives, there are really no exact matches. We have shown 3 companies that best represent the cross-section of what TIXT does in our view. Cognizant Technology Solutions Corp ( CTSH ), Infosys LTD ( INFY ) and EPAM Systems Inc. ( EPAM ), all trade at far higher multiples than TIXT.

The valuation here looks very defensible. The adjusted EBITDA margins are still quite strong relative to the peer group. But TIXT needs to stabilize its revenues and earnings outlook first. It also needs to revamp its market message and not set a new record for how many times it mentions "AI" on its conference call . We think once the smoke clears, TIXT could represent a good opportunity at a reasonable price. We rate the stock a hold for now as it gets a 6 on our pain scale.

The primary factor here is there is no single stock that we know that bottoms with such huge down moves on day 1.

TELUS

TELUS consolidates TIXT's revenues and EBITDA into its own and hence lowered its own guidance as a result.

The update to TIXT's full-year outlook, which now calls for Revenue in the range of US$2.7 billion to US$2.73 billion and Adjusted EBITDA of US$575 million to US$600 million, was revised lower due to more pronounced than anticipated demand challenges in the near-term from certain clients within the technology vertical. Due to TIXT's updated annual outlook for 2023, TELUS is now targeting Consolidated Operating Revenue growth of 9.5 to 11.5 percent (from 11 to 14 percent) and Adjusted EBITDA growth of 7 to 8 percent (from 9.5 to 11 percent).

Source: TELUS

TELUS derives 90% of its EBITDA from non-TIXT means, so the drop in growth shows just how heavily it was leaning on this segment to power gains. The company did try and soften the blow by early release of the subscriber numbers.

"Total Mobile and Fixed customer growth of 293,000, was up 46,000 over last year and represents our strongest second quarter on record. This was driven by strong demand for our leading portfolio across Mobility and Fixed services, backed by our industry-best customer experience, and world-leading wireless and wireline broadband PureFibre networks."

Source: TELUS

TELUS also dropped about 5% on the news and that might have surprised many.

Outlook & Verdict On TELUS

17 months back we gave a CAD$25 price target on TELUS shares.

Telecom industry and see this hedge as a low-risk one, compared to others available. Key catalysts for a revision will likely come as EBITDA growth stalls in 2022. Inflation is not a friend of slow-growing, richly valued companies and TELUS will be no different. We have a CAD$25 (USD$19.50) price target in one year.

Source: One Growth Bubble Waiting To Implode

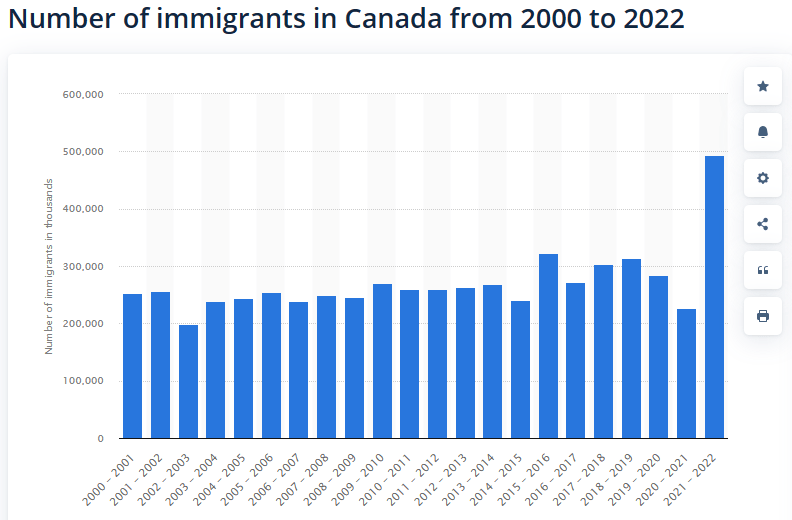

The stock has moved under that and the market is now correctly discounting high growth hopes. One reason we think TELUS took so long to actually drop was the chart below.

{kind=link}

Telecommunications services don't create customers from thin air. They are not going to sell an individual a second cell phone plan if they already have one. So immigration is a big factor and we massively underestimated what would happen here. This brute force has been the reason TELUS has been reporting record numbers. Unfortunately for TELUS, this is likely to change very soon. The mass immigration policy has created unbelievable headaches for provincial governments including delivering adequate healthcare and finding affordable housing.

To put Canada's growth in context, our 2.7-per-cent population increase last year was the highest rate among all OECD countries. To find a higher rate, one would need to look to Africa.

The supply of housing and health care in Ontario is clearly inadequate to meet the needs of people who live in the province now, much less those of newcomers.

At least one million Ontarians lack a family doctor. Emergency rooms shut down sporadically because of a lack of nurses.

The scarcity and high cost of housing in Ontario is well known, but Ontario Premier Doug Ford recently celebrated the news of the record population growth with a cheery tweet saying, "Each and every person needs a place to call home. That's why we're building 1.5 million homes."

To be a little more accurate. Ontario is planning to build 1.5 million homes over 10 years. Considering that 100,000 homes are the most that have ever been built in the province in a year, the target seems a tad optimistic. The situation is made worse by an existing housing deficit. A Scotiabank report last year estimated that Ontario needs 650,000 additional dwelling units just to meet the national average.

Source: National Post

The blowback from this is likely to reach a fever pitch in the next year and a more normalized policy is likely to be put in place. This should take away those glorious growth numbers. Nonetheless, the stock is now approaching our buy range. The yield is a whisker away from 6%.

On our last update we had suggested that being defensive was the name of the game and covered calls would be a better choice for those looking for income. We are now going to actually do some of these over the next few days (with a lower strike point) as the risk-reward is getting favorable. We can generate 10-12% here with lower risk using covered calls and that is a good deal on a quality play like TELUS.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

TELUS International: Growth Story Breakdown Drags TELUS With It