ETD - Tempur Sealy International Q1 2023 Preview: Some Upside Is Still Warranted

2023-05-07 06:25:46 ET

Summary

- Tempur Sealy International is due to announce financial results for the first quarter of its 2023 fiscal year on May 9th.

- Leading up to that point, analysts seem rather pessimistic while management was previously optimistic.

- This is creating a very interesting situation that, when coupled with how shares are priced, could lead to further additional and warranted upside.

Although there are many different investment strategies that people can follow, from my experience, value investing tops them all. It is not without its risks and downsides. However, the concept of buying a company on the cheap really resonates with me. Even during times when companies are experiencing weakness, whether that be on their top or bottom lines, or both, buying stocks that are trading on the cheap can result in some attractive upside. One great example of this in recent months can be seen by looking at sleep centric business Tempur Sealy International ( TPX ).

Even though the company experienced some weakness from 2021 to 2022, the 2023 fiscal year is looking up. Having said that, leading into the first quarter earnings release for the company's 2023 fiscal year, analysts aren't exactly optimistic. On the one hand, this could mean that the company is just starting the year off weak and will get stronger as the year goes on. Or it could mean that analysts are incorrect, or that management is incorrect in its own assumptions. No matter how you stack it, this does create a rather interesting scenario where investors could capture some nice upside, or be subjected to some pain. Given the company's operating history and how attractively priced shares are on an absolute basis, I choose to remain bullish. But I also recognize that the easy money has already been made in this name for now.

Assessing past weakness

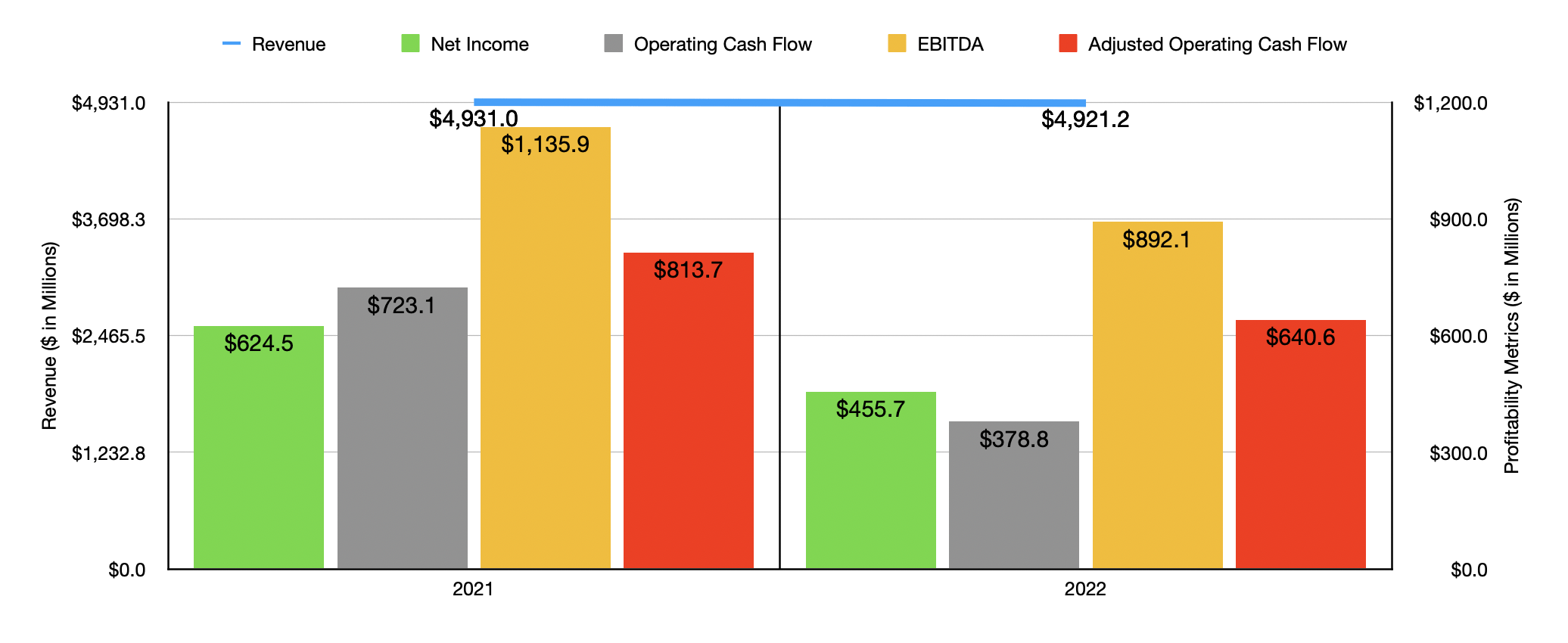

The 2022 fiscal year was not exactly a great time for shareholders of Tempur Sealy International if the focus was not on stock returns, but instead on fundamental performance. During that year, revenue came in at $4.92 billion. That was down marginally from the $4.93 billion the company reported for 2021. Given all of the economic uncertainty we have been contending with, this is not the worst thing that could happen. But the company did experience a lot of pain on its bottom line. Net income for the company dropped from $624.5 million in 2021 to $455.7 million last year. Other profitability metrics followed a similar trajectory. Operating cash flow, for instance, went from $723.1 million to $378.8 million. Even if we adjust for changes in working capital, it would have fallen from $813.7 million to $640.6 million. Meanwhile, EBITDA for the company declined from $1.14 billion to $892.1 million.

{kind=link}

These rather substantial declines were driven by a couple of different factors. One of the most significant involved a decline in the company's gross profit margin from 43.8% to 41.6%. This drop, according to management, can be chalked up to weakness across the board. For instance, in North America, gross margin declined by 2.8%, with 1.7% of this drop caused by operational headwinds and the remainder largely associated with expense deleveraging. Higher manufacturing ERP system transition costs, as well as other factors, comprised the remaining $16.9 million of decline in gross profit. Internationally, gross margin dropped 2.1%. 1.2% was driven by an unfavorable product mix as consumers focused more on the low margin value products the company offers as opposed to the higher margin premium ones. Acquisition activity, as well as increased costs, accounted for the rest of the pain. The situation would have been worse had it not been for an increase in royalties that had a positive impact on margin.

Looking forward

Given the rough 2022 fiscal year and the fact that economic conditions are now even more worrisome than they were then, you might think that now is a good time to avoid the stock entirely. But management seems optimistic. Currently, they are forecasting sales growth to be in the mid single digit range. They also believe that earnings per share should be between $2.60 and $2.80. At the midpoint, this would translate to net profit of $486.8 million for the year. That would imply a modest increase over what was seen in 2022. If we assume that other profitability metrics will rise at the same rate, then we would expect adjusted operating cash flow of $684.3 million and EBITDA of $953 million.

{kind=link}

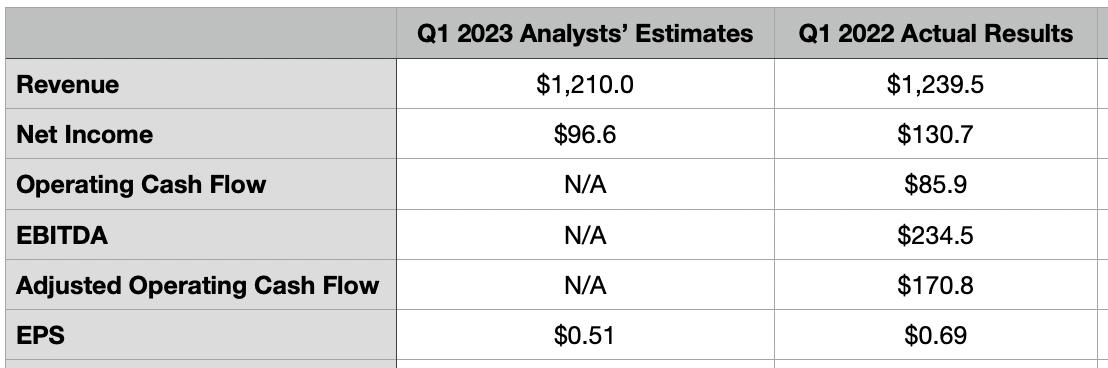

Interestingly, analysts don't seem to be all that optimistic at the moment. Before the market opens on May 9th, the management team at Tempur Sealy International is expected to announce financial results covering the first quarter of the company's 2023 fiscal year. At present, analysts believe that revenue will come in at $1.21 billion. This would actually represent a decline from the $1.24 billion the company reported the same quarter one year earlier. There does not seem to be much in the way of data to support the view of a weakening on this front. According to the International Sleep Products Association in a report issued late last year, the expectation is that both total mattress units and mattress dollar sales will grow by about 1.5% this year. But it is possible that a change in economic circumstances could cause consumers to delay purchases on an item that doesn't usually have to be purchased immediately.

The bottom line is also a point of contention. Even though management is forecasting earnings growth for the current fiscal year, analysts believe that earnings per share in the first quarter will be $0.51. By comparison, earnings per share in the first quarter of 2022 came out to $0.69. This translated to $130.7 million in net profit. Although there have not been forecasts when it comes to other profitability metrics, it would be wise for investors to pay attention to them. For context, operating cash flow in the first quarter of 2022 was $85.9 million. If we adjust for changes in working capital, it was $170.8 million. And finally, EBITDA was a rather lofty $234.5 million.

{kind=link}

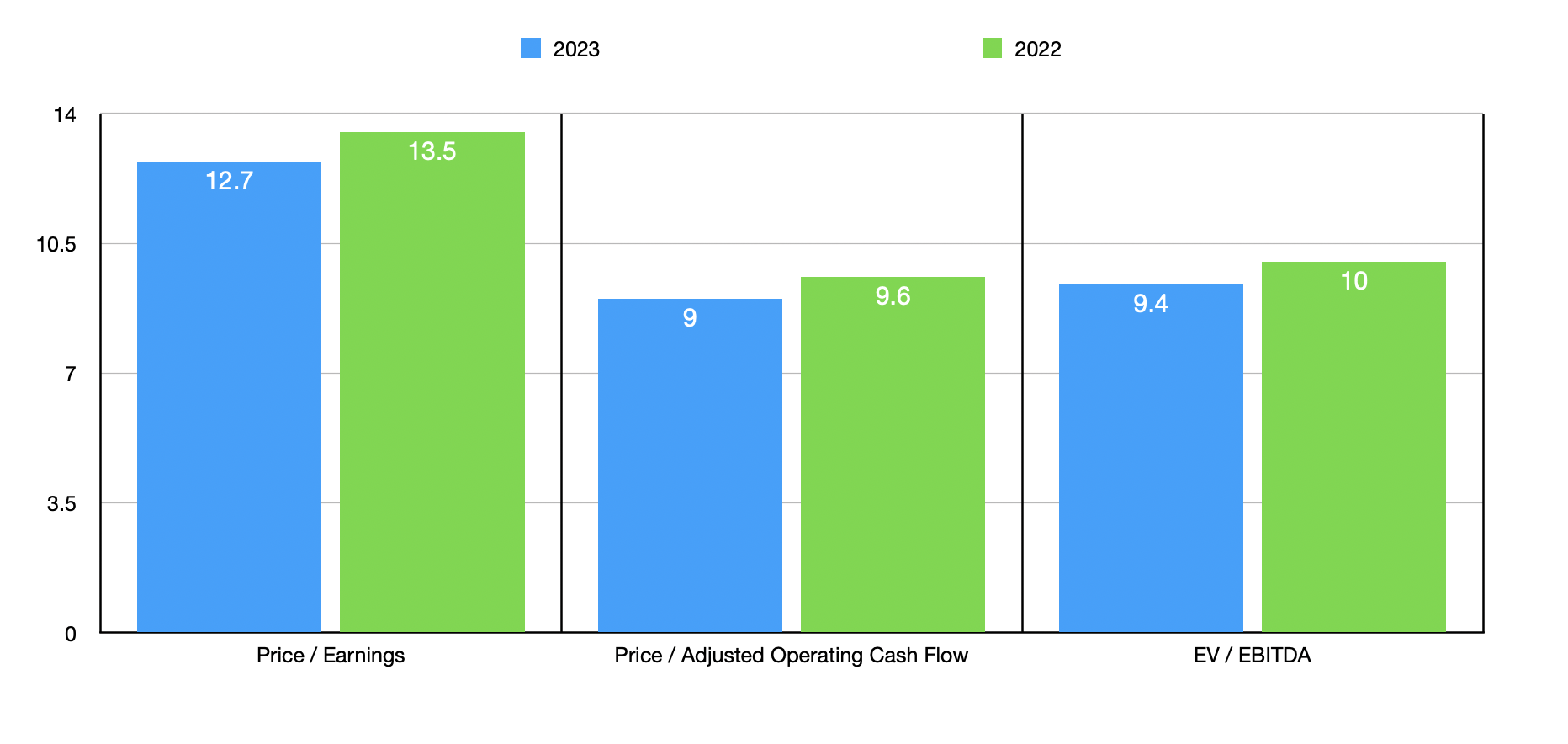

Obviously, there is uncertainty about the future at this time. But if we assume that management can at least match what it achieved in 2022, shares of the company don't look expansive at all. As you can see in the chart above, I priced the company using data from 2022 and estimates from 2023. And as part of my analysis, I also compared the company to five firms that have some similarities to it. These can be seen in the table below. On a relative basis, Tempur Sealy International does look a bit lofty. On a price to earnings basis, two of the five firms were cheaper than it. But when it comes to the price to operating cash flow approach and the EV to EBITDA approach, four of the five companies were cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Tempur Sealy International |

| 13.5 |

| 9.6 |

| 10.0 |

| Leggett & Platt ( LEG ) |

| 16.4 |

| 9.0 |

| 9.9 |

| Mohawk Industries ( MHK ) |

| 321.2 |

| 7.3 |

| 13.3 |

| La-Z-Boy ( LZB ) |

| 7.1 |

| 7.6 |

| 2.6 |

| Ethan Allen Interiors ( ETD ) |

| 6.2 |

| 6.7 |

| 3.1 |

| The Lovesac Company ( LOVE ) |

| 15.0 |

| 23.0 |

| 6.9 |

Takeaway

Based on all the data provided, I must say that I am quite optimistic about Tempur Sealy International from a valuation perspective and a fundamental perspective. The company may not be the cheapest player on the market, but it is a quality operator that should continue to create value for its investors in the long run. Since I last wrote about it in November of last year when I rated it a ‘buy’, shares have seen upside of 16.8% compared to the 4.4% rise experienced by the S&P 500. I would argue that the easy money by now has certainly been made. But I do also feel comfortable with the idea that some additional upside could be on the table. As such, I've decided to keep the ‘buy’ rating I had on the stock previously.

For further details see:

Tempur Sealy International Q1 2023 Preview: Some Upside Is Still Warranted