TPX - Tempur Sealy: Waking Up To Resilient Demand

2023-08-04 12:47:06 ET

Summary

- Tempur Sealy has been a strong performer, beating consensus estimates and gaining 58% in the last year.

- The company has outperformed the mattress industry, delivering resilient revenue and above-industry EBITDA margins.

- Despite a challenging industry demand outlook, TPX remains a silver lining and is still a buy at 14.5x 1Y Fwd earnings.

Investment Thesis

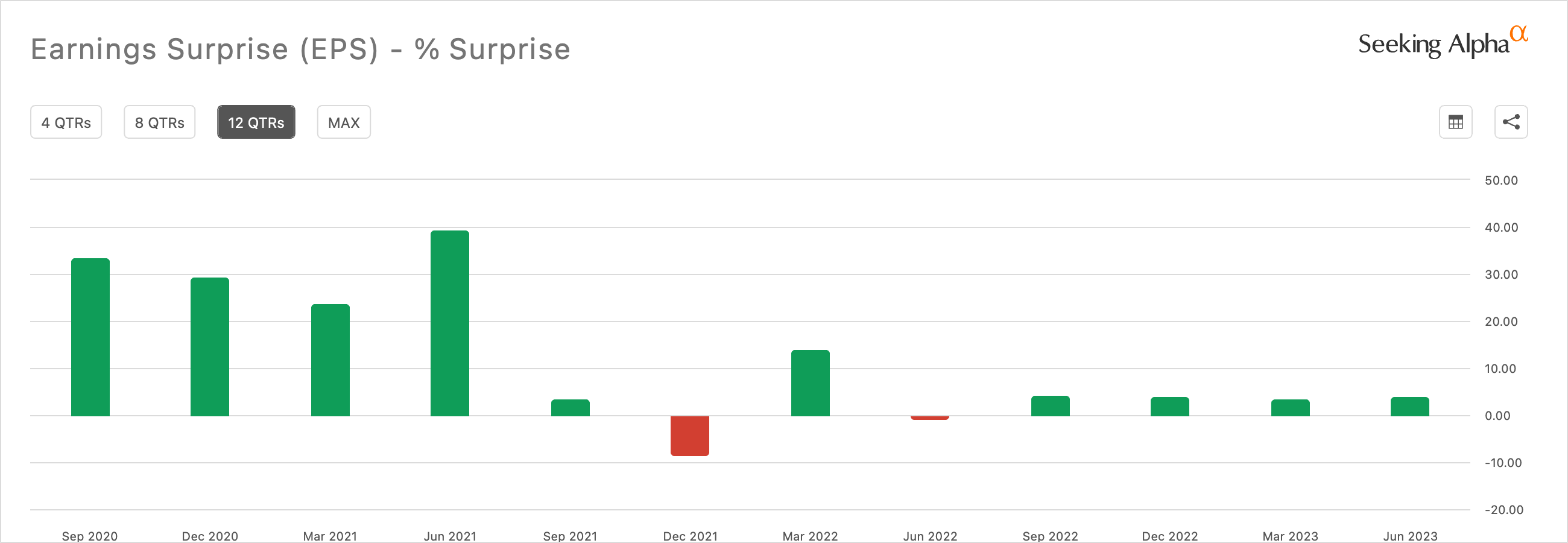

Tempur Sealy ( TPX ) has been one of the strong performers despite a tough macro backdrop gaining 58% in last 1 year and almost at a touching distance of its previous COVID peak. It has consistently beat consensus estimates having surprised the street in 10 of the last 12 quarters.

{kind=link}

Seeking Alpha

TPX has been outperforming the industry delivering resilient revenue and above industry EBITDA margins while other mattress players like Sleep Number ( SNBR ) have been struggling facing demand contraction.

Sleep Number and the mattress industry overall have been operating in a disrupted and challenging macro environment, which has resulted in a historic contraction in demand for mattresses with six consecutive quarters at recessionary spend levels.

- Shelly Ibach, Chair, President & CEO, Sleep Number ( source )

We believe the positive momentum and strong brand resonance amongst its consumers will continue to drive operational outperformance for TPX. Initiate at Buy.

Earnings Corner

TPX market share gains helped them to post a strong Q2 on August 3rd amidst a tough macro backdrop with sales growing 4.8% YoY above the high end of 2Q expectations beating consensus (expected flat growth) by a wide margin. The growth was driven by strong outperformance in North American market (up 5.4% YoY) while the industry was down at least MSD due to strength in new product launches which drove incremental share gains and 13% YoY ASP growth. Adjusted Gross Margins improved 120 bps YoY which was a surprise for the street driven by pricing actions, favorable product mix and moderating commodity costs partially offset by product launch costs and operational headwinds. EBITDA, however, came in line with estimates as higher selling and marketing expenses led to deleveraging of SG&A by 80 bps. Overall, EPS came in at $0.58 marginally beating the consensus estimates at $0.56 highlighting resilience in earnings in our view.

Balance sheet remains strong with cash balance of over $100 mn, inventory levels decreasing 5% QoQ at $529 mn and Net debt/ EBITDA improving to a comfortable level of 3.1x, almost near their long term target. It guided FY23 earnings downwards at $2.5 - $2.7 (vs $2.6 - $2.8 previously) citing tepid industry trends as it expects only a flat to mildly positive sales growth. All in, the performance remained robust amidst a significantly challenging industry demand outlook and TPX remains a silver lining for the overall mattress industry.

Valuation

Despite the runup in the stock price over the last year, TPX is still a buy at 14.5x 1Y Fwd earnings. We believe TPX will likely lead the industry growth as demonstrated in the past few quarters and that will help drive earnings further. We believe TPX deserves a premium due to stronger brand resonance and market share gains compared to competition, industry leading EBITDA margins and resilient earnings. We believe a 30% premium to its peers is warranted and assign a buy rating at 20x Forward P/E with a target price of $52.

Conclusion

TPX has been a story of long term earnings and cash flow growth story in an otherwise tepid industry. It has strong niche within premium bedding segment with brands such as Stearns & Foster grew double digits in a market that declined by double digits suggesting strong consumer reception and brand resonance. We believe incremental product launches leading to continued market share gains, channel DTC expansion and moderating commodity costs would continue to drive earnings higher. Initiate at Buy.

Risks to Rating

Risks to rating include

1) Any change in consumer spending pattern amidst a tough macro backdrop would significantly pressure sales as the industry is already reeling under pressure staring double digit decline in unit sales. This has already led TPX to revise their earnings downwards and continued sales squeeze amidst a tepid demand outlook may affect the earnings further

2) TPX was recently a victim of cyber attack which led them to shut down their IT systems and temporary stopping its operations. The forensic investigation remains ongoing, and it continues to work to determine whether this incident will have a material impact on its business, operations or financial results. Any negative outcome could significantly impact the business.

3) Higher than expected promotional environment due to current demand outlook could lead TPX to follow suit which would further put squeeze on the margins

For further details see:

Tempur Sealy: Waking Up To Resilient Demand